Sample Category Title

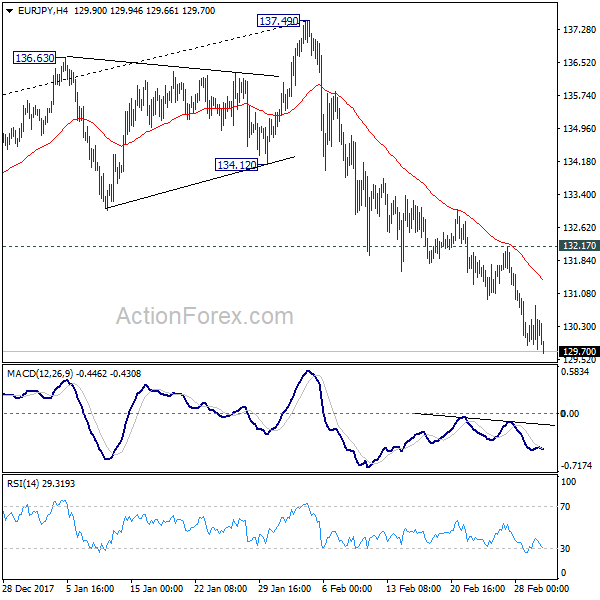

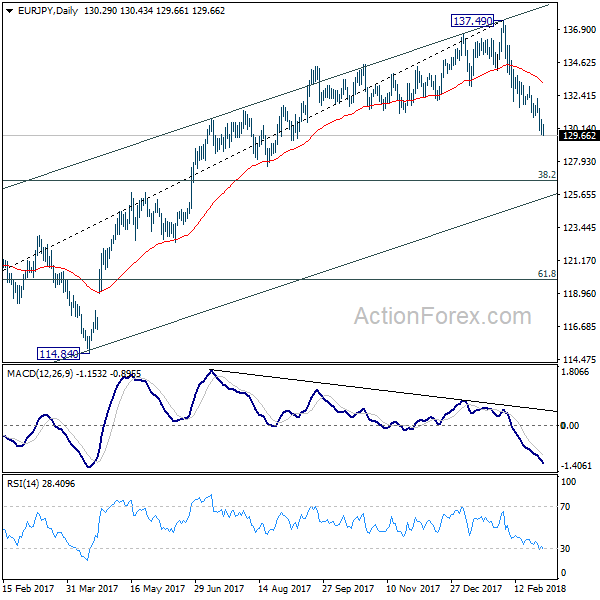

EUR/JPY Daily Outlook

Daily Pivots: (S1) 129.57; (P) 130.54; (R1) 131.05; More....

Intraday bias in EUR/JPY remains on the downside as fall from 137.49 is in progress. As noted before, a medium term top is likely in place at 137.49 on bearish divergence condition in daily MACD. Deeper decline should be seen to 126.61 medium term fibonacci level next. On the upside, break of 132.17 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, current development argues that rise from 109.03 has completed at 137.49, on bearish divergence condition in weekly MACD. Deeper fall should be seen to 38.2% retracement of 109.03 to 137.49 at 126.61 first. On the upside, break of 137.49 is needed to confirm medium term rise resumption. Otherwise, risk will now stay on the downside even in case of strong rebound.

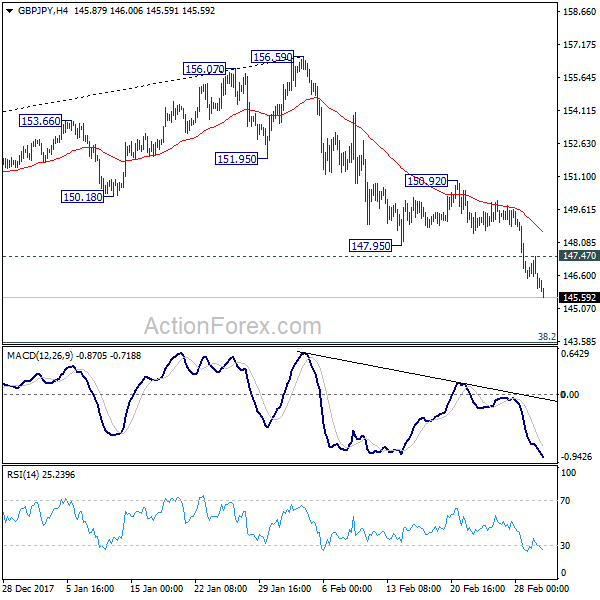

GBP/JPY Daily Outlook

Daily Pivots: (S1) 145.73; (P) 146.60; (R1) 147.20; More...

GBP/JPY's decline is still in progress and reaches as low as 145.62 so far. Intraday bias remains on the downside for 143.51 medium term fibonacci level next. On the upside, above 147.47 minor resistance will turn intraday bias neutral first. But outlook will remain bearish as long as 150.92 resistance holds, in case of recovery.

In the bigger picture, the case for medium term reversal continues to build up on loss of medium term momentum as seen in weekly MACD. Also, firm break of 146.96 should now indicate rejection by 55 month EMA (now at 154.60) and add to that case of reversal. Deeper fall would be seen to 38.2% retracement of 122.36 to 156.59 at 143.51 and then 61.8% retracement at 135.43. This will now be the preferred case as long as 150.92 resistance holds.

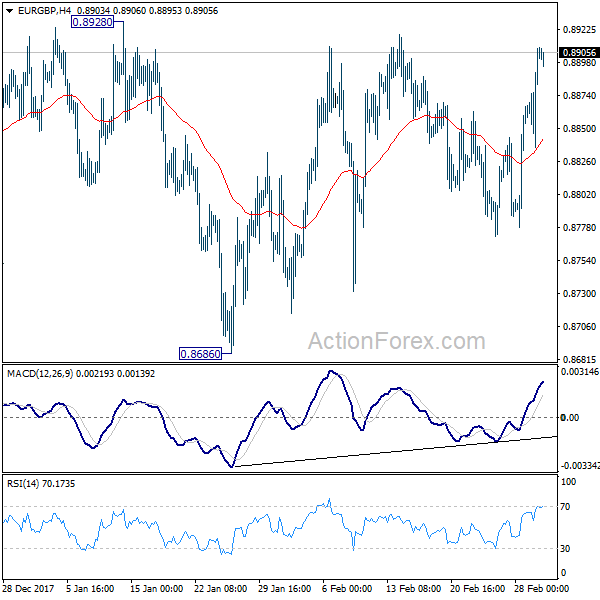

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8857; (P) 0.8883; (R1) 0.8929; More...

Intraday bias in EUR/GBP remains neutral at this point as it's bounded in range of 0.8686/8928. Also, outlook stays mildly bearish with 0.8928 resistance intact. On the downside, firm break of 0.8686 will resume whole decline from 0.9305. As 61.8% retracement of 0.8312 to 0.9305 should then be taken out too, deeper decline would be seen to retest 0.8303/8312 support zone. Nonetheless, on the upside, break of 0.8928 will indicate near term reversal and turn outlook bullish for 0.9304 resistance.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Market Update – Asian Session: Protectionism Concerns Weigh On Asian Markets

Headlines/Economic Data

General Trend:

Steelmakers trade broadly lower after Trump Admin formally announces tariffs on aluminum and steel imports

USD/JPY hits 2-week low

(JP) BOJ Gov Kuroda: Will be considering exit around Fiscal 2019 because of the chances of hitting inflation target at that time - Parliament comments

China National People’s Congress to start on Monday, March 5th, will set economic targets for the coming year; Expected to keep GDP growth near or above 6.5% - Xinhua

Australia/New Zealand

ASX 200 opened -0.5%; closed -0.7%

ASX 200 Telecom Index -1.7%, Resources -1%, Energy -0.9%, Financials -0.5%

(AU) Australia Trade Min Ciobo: To seek exemption from US steel tariffs

(NZ) New Zealand Feb ANZ Consumer Confidence: 127.7 v 126.9 prior

(NZ) New Zealand Jan Building Permits M/M: +0.2% v -9.6% prior

(NZ) Citigroup pushes back RBNZ rate hike call: Now sees rates on hold until Q1 2019 vs prior expectation for rate hike in Q3 2018

China/Hong Kong

Hang Seng opened -1.4%, Shanghai Composite opened -1.8%

Hang Seng Energy Index -2%, Info Tech -1.9%, Financials -1.8%, Property/Construction -1.2%

Shanghai Composite Property Index trades at around flat levels

Chinese industry groups react to US decision to adopt sanctions on steel and aluminum: (CN) China Metals Association: China among nations likely to 'retaliate'

(CN) China Iron and Steel Association (CISA) Official: US tariffs related to steel and aluminum are 'stupid' trade protection measure

(US) White House Official: Talks with China Economic Adviser Liu He were 'frank and constructive'; US underscored the importance of achieving balance and reciprocity in the economic relationship with China.

Japan

Nikkei 225 opened -1.8%; closed -2.5%

TOPIX Iron & Steel index declines over 3% after US trade move

Japanese automakers decline after US announcement related to tariffs and gains in the Yen

Nikkei weighted Fast Retailing [9983.JP] declines over 2% ahead of Feb sales figures (reported Jan figures after the close)

(JP) Japan Jan Jobless Rate: 2.4% v 2.8%e (multi-decade low*)

(JP) Japan Feb Tokyo CPI Y/Y: 1.4% v 1.4%e; Ex-Fresh Food (Core) Y/Y: 0.9% v 0.8%e

(JP) Japan Feb Monetary Base Y/Y: 9.4% v 9.7% prior;

(JP) BoJ Gov Kuroda: Reiterates will consider further easing if needed and will adjust policy to reach target if needed.

(JP) Japan Fin Min Aso: Won't comment on FX market; Carefully watching effect of labor shortage on economy, clear that there is a labor shortage in Japan

(JP) BoJ Gov Kuroda Upper House confirmation hearings set for March 6th; The confirmation hearings for the Dep Gov Nominees set for March 7th

Korea

Kospi opened -0.9%

(KR) South Korea Feb Nikkei PMI Manufacturing: 50.3 v 50.7 prior

(KR) South Korea is expected to nominate new Bank of Korea (BoK) chief on Monday - South Korean Press

(KR) South Korea held meeting on possible impact of US steel tariff; plans to reach out to US officials regarding its tariff plan

(KR) South Korea Pres Moon reportedly plans to send special envoy to North Korea soon - South Korea press

Other Asia

(IN) India Steel Sec: No immediate impact of US trade curbs on imports; Trump Administration is 'stretching' security clause as a barrier for steel imports to the US.

(TH) Thailand Feb Nikkei PMI Manufacturing: 50.9 v 50.6 prior

(TH) Thailand Feb CPI M/M: -0.2% v -0.1%e; Y/Y 0.4%* v 0.7%e

(TW) Taiwan Premier: No need to 'panic' about inflation

North America

US equity markets closed broadly lower: Dow -1.9%, S&P500 -1.3%, Nasdaq -1.3%, Russell -0.3%

S&P500 Industrials -2%, Financials -1.7%, Tech -1.7%

(US) Pres Trump: US will institute tariffs next week; will impose 25% tariffs on steel and 10% on aluminum imports - comments at White House

(US) Fed Chair Powell: there's no strong evidence of a decisive move higher in wages; Reiterates gradual rate hikes are expected to be the appropriate path - Senate testimony

(US) Fed's Dudley (dove, FOMC voter): Four 25bps rate hikes would still be a gradual pace; Can't be too aggressive about rate hikes because inflation is still below target

(US) PIMCO economist Rich Clarida likely front runner for Fed deputy role – press-(US) Former Fed Chair Greenspan: bond market unwind will ultimately bring us into state of stagflation; As real interest rates rise, it's inevitable that the effect on equity prices is negative - CNBC

Park Hotels & Resorts [PK]: China HNA said to plan to sell entire 25% stake which may be worth $1.4B - US financial press

Looking Ahead: Canada Q4 GDP due for release

Europe

(EU) Reportedly ECB unlikely to signal any policy changes at March 8th meeting, but might discuss dropping easing bias language – press

(EU) Likelihood that ECB's Weidmann will replace Draghi is said to be increasing; Reportedly Weidmann gaining support as Germany agrees to support Spain's De Guindos as next ECB Vice President - press

(EU) EU's Juncker: EU will "react firmly" to T rump administration tariffs; will bring forward countermeasures

(ES) Reportedly Puigdemont may drop his effort to return to Catalan Presidency - Spain press

(UK) Prime Min May: Brexit deal must give UK control of its borders, laws and money; deal must protect people's jobs; Will set out 'five tests' for Brexit deal - preview of March 2nd speech

(UK) PM May spokesperson: held constructive talks with Tusk today; called EU Commission draft text unacceptable

Technicolor [TCH.FR]: InterDigital makes binding offer to acquire Technicolor’s patent licensing business for $150M in cash

Levels as of 01:00ET

Hang Seng -1.4%; Shanghai Composite -0.5%; Kospi -0.8%

Equity Futures: S&P500 -0.1%; Nasdaq100 +0.1%, Dax -0.2%; FTSE100 -0.2%

EUR 1.2259-1.2288 ; JPY 105.93-106.32; AUD 0.7749-0.7775 ;NZD 0.7247-0.7277

Feb Gold +1% at $1,318/oz; Feb Crude Oil flat at $60.98/brl; Mar Copper +0.4% at $3.138/lb

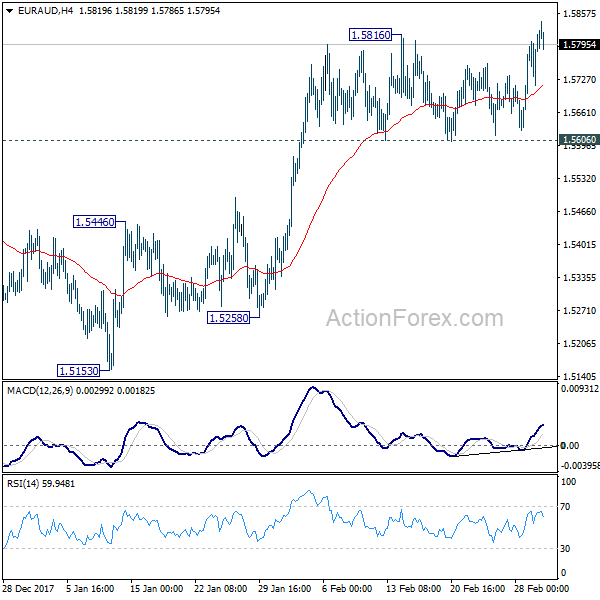

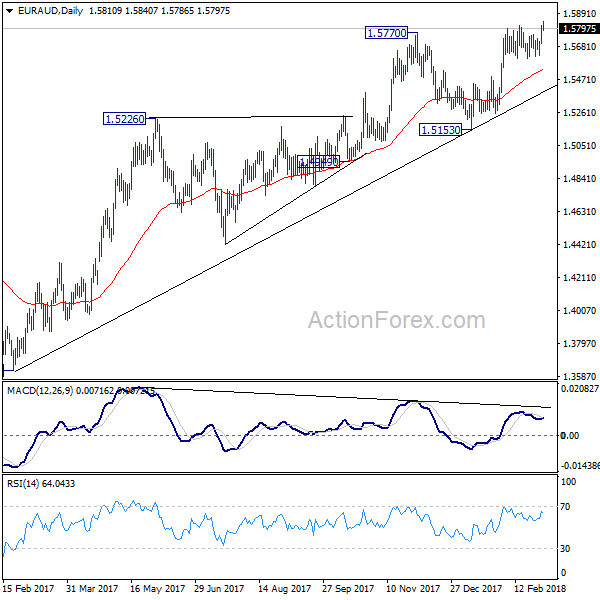

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5737; (P) 1.5776; (R1) 1.5852; More....

The breach of 1.5816 suggests that EUR/AUD's medium term rise is resuming. Intraday bias is now on the upside for 1.6587 key long term resistance. In any case, outlook will remain bullish as long as 1.5606 support holds, in case of retreat.

In the bigger picture, medium term rise from 1.3624 is not completed yet. Sustained break of 1.5770 will extend the rise to retest 1.6587 (2015 high). However, considering bearish divergence condition in daily MACD, break of 1.4949 cluster support (38.2% retracement of 1.3624 to 1.5770 at 1.4950) will indicate medium term reversal. And there is prospect of retesting 1.3624 low in that bearish case.

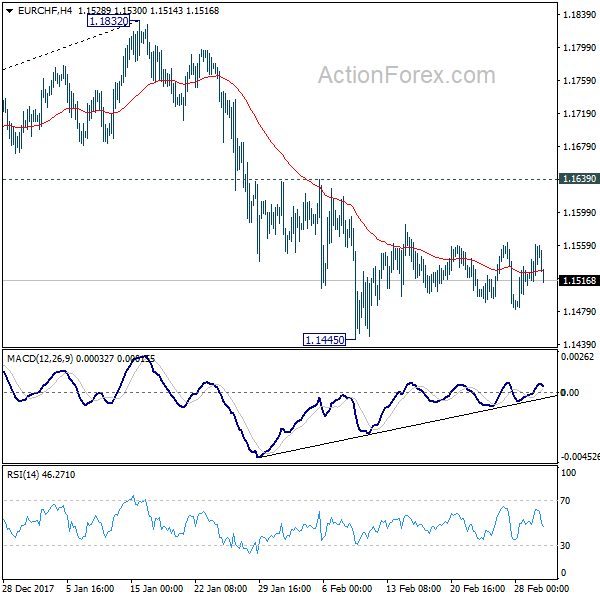

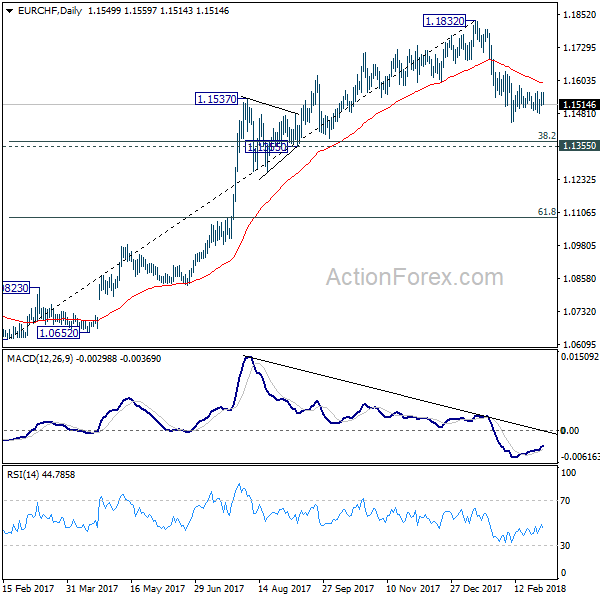

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1521; (P) 1.1540; (R1) 1.1571; More...

No change in EUR/CHF's outlook as consolidation from 1.1445 is extending. Outlook stays mildly bearish with 1.1639 resistance intact and deeper decline is expected. Break of 1.1445 will resume the corrective fall from 1.1832 and target 1.1355 cluster support (38.2% retracement of 1.0629 to 1.1832 at 1.1372.) At this point, we'd expect strong support from there to contain downside and bring rebound.

In the bigger picture, a medium term top should be in place at 1.1832 on bearish divergence condition in daily MACD. But there is no indication of long term reversal yet. As long as 1.1198 resistance turned support holds, we'd still expect another rise through prior SNB imposed floor at 1.2000.

Fed Is Unlikely To Hike Rates Aggressively

Today, we have published the fifth and last document in our series on inflation and what it means for financial markets. In this document , we look at the FX implications of the inflation and fixed income out look out lined in the first four pieces, Part 5: FX and inflation - US inflation outperformance + comfy Fed = weaker USD.

This morning we also published ECB Preview - Striking a compromise, 2 March, ahead of next week's meeting. In short , we expect the ECB to strike a compromise between the doves and the hawks by removing the QE flexibility bias but have no discussion on rate hikes. We expect Mario Draghi to strike a relatively dovish tone at the press conference. For expected market react ions, see the full document .

Market movers today

In the UK, PM Theresa May is speaking about her vision on Brexit today. Leaks suggest that May will stick to her demands for a tailor-made UK deal and that contents of the speech were changed in the last minute amid her Cabinet remaining heavily divided.

On Sunday in the Eurozone, we have a Super Sunday with the Italian election and the SPD's decision on whether to join the German government or not. F

In the Scandies, focus is on Danish FX reserve data, Norwegian NAV labour market report and investment survey in Sweden. For more details, see ‘Scandi Markets' on page 2.

Selected market news

Global market sentiment remains heavily influenced by developments in the US amid rising speculations that the Fed could soon signal a higher tightening pace whilst the risk of a global trade war has risen on the out look of more protectionist US policies. The US fixed income rally has continued and most Asian equity indices have followed US counterparts into red territory.

Yesterday evening, US President Donald Trump announced that his administration contemplate imposing substantial tariffs on imports of steel and aluminium. We emphasize that while higher tariffs create a worse growth-inflation trade-off, both steel and aluminium only make up a very small part of US imports, cf. this chart. However, the move is likely to trigger retaliation from the EU, Canada and China meaning that the risk of a global trade war that potentially could derail the global recovery has risen considerably on the announcement .

The strong ISM manufacturing report yesterday added fuel to market speculations of Fed potentially revising higher its dot plot to four 2018 rate hikes at the forthcoming meeting in March. The accompanied ISM sector statements indicated rising import price pressures, rising capital equipment expenditures following the tax reform as well as labour shortages in some industries. Meanwhile short ly after the ISM release, Fed chair Powell toned down his hawkish remarks from Tuesday, partly reversing the more aggressive Fed pricing and halting the slide in EUR/USD. Overall our view remains, that the Fed is unlikely to hike rates aggressively this year. We might get a fourth rate hike this year but a fifth seems unlikely and at this stage our base case remains three.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7722; (P) 0.7746; (R1) 0.7779; More...

A temporary low is in place at 0.7712 and intraday bias is turned neutral first. Near term outlook remains bearish with 0.7892 resistance holds. Below 0.7712 will extend the fall from 0.8135 to 100% projection of 0.8135 to 0.7758 from 0.7988 at 0.7611.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed.

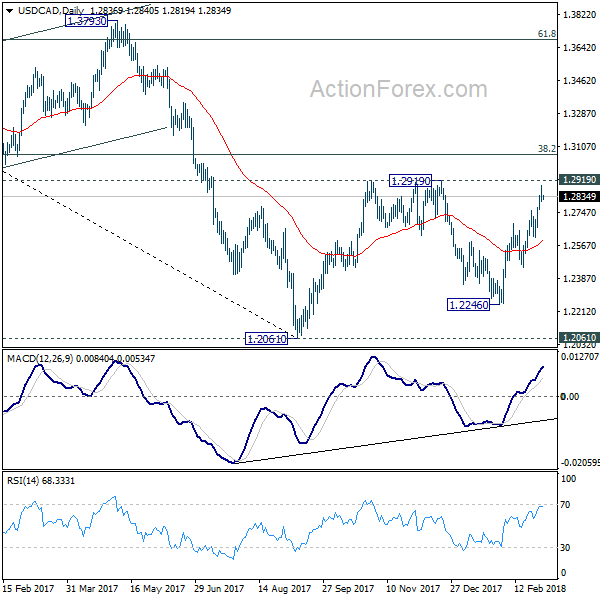

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2796; (P) 1.2845; (R1) 1.2882; More....

At this point, intraday bias in USD?CF remains on the upside for 1.2919 key resistance. We'd be cautious on strong resistance from there to limit upside. But a firm break there will carry larger bullish implication. On the downside, below 1.2757 will turn bias to the downside. Further break of 1.2614 will indicate completion of the rebound from 1.2246 and turn outlook bearish.

In the bigger picture, the rebound from 1.2246 is mixing up the medium term outlook. Nonetheless, USD/CAD is staying below falling 55 week EMA (now at 1.2771), hence, the bearish case is in favor. That is, fall from 1.4689 is not completed yet. Sustained break of 1.2061 key support will carry larger bearish implication and target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. However, firm break of 1.2919 will revive the case of medium term reversal and turn outlook bullish.

USD/JPY Daily Outlook

Daily Pivots: (S1) 105.85; (P) 106.53; (R1) 106.90; More...

USD/JPY's break of 106.37 minor support suggests rebound from 105.54 has completed. Intraday bias is turned back to the downside. Break of 105.54 will resume larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. In any case, break of 108.27 resistance is needed to indicate trend reversal. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.