Sample Category Title

Bitcoin Gets Support From An Unlikely Source

February was a good month for bitcoin. Its price moved from a low of $5,817 to end the month above $10,000.

In the recent weeks however, the cryptocurrency has been in consolidation move with its price fluctuating between $11,744 and $9260.

The recent bullish move can be attributed to the lack of any major regulatory news from the leading countries like US, Japan, and the European Union.

A common argument against bitcoin and other currencies is that it does not have any value. This argument was deconstructed yesterday by a former senior America regulator.

In an interview with Barron’s, Sheila Blair argued that the argument that bitcoin had no intrinsic value was overblown. She argued that using the same logic, other fiat currencies would be worthless as well. She said:

‘I don’t think we should ban it — the green bills in your pocket don’t have an intrinsic value, either. The value is based on what others think is its value. That’s true of any currency.’

Sheila Blair is a highly respected professional in the country. During the financial crisis, she was the head of the Federal Deposit Insurance Corp (FDIC) which insures bank deposits. She served the institution for more than 5 years.

As shown below, the pair started moving up on 6 February. The pair has now completed the first and second phase of an impulse Elliot Wave which means that the current upward trend will continue. In an Elliot Wave, the third phase is usually the longest.

Active Week Keeps On Giving With Eurozone, North American Data

A deluge of economic data will make its way through the financial markets on Friday, capping off a highly active week in the markets. The final session of the week will deliver reports from the Eurozone, United Kingdom, Canada and the United States.

Action begins at 07:00 GMT with reports on German import prices and retail sales. On the sales side, retail receipts are forecast to climb 0.9% in January following a 1.9% decline in December. Based on estimates, this should translate into year-over-year growth of 3.5%.

Italian GDP will be delivered at 09:00 GMT, followed by a report on Eurozone producer prices one hour later. Eurozone PPI is forecast to grow 0.4% in January and 1.6% annually.

In between those releases, the Chartered Institute of Purchasing and Supply will release the United Kingdom's construction PMI for February.

Shifting gears to North America, the Canadian government will issue its quarterly report on GDP at 13:30 GMT. The Canadian economy is forecast to grow 2% between October and December, up from the 1.7% advance during the previous quarter.

In the United States, the University of Michigan will deliver its February consumer sentiment index at 15:00 GMT.

Energy traders will also be keeping a close eye on the weekly rig count report courtesy of Baker Hughes. The oilfield services provider reports on active US oil rigs on a weekly basis. Another week of gains will likely fuel concerns that shale producers are flooding the market, which could put a stop to the months long advance in oil prices.

In terms of monetary policy, European Central Bank (ECB) executive Yves Mersch will deliver a speech in the morning. UK Prime Minister Theresa May is also scheduled to deliver a speech on Friday.

EUR/USD

Europe's common currency staged a recovery on Thursday but remains well off multi-year peaks from last month. The EUR/USD exchange rate was last seen trading at 1.2271, where it was little changed. With the recent advance, the pair is eyeing the 1.2330 resistance. A clean break above this level is expected to bring the bulls back to market.

GBP/USD

Cable staged a modest recovery attempt on Thursday, as Brexit fears continued to weigh. GBP/USD was last seen trading at 1.3781, unchanged from the previous close. Immediate support is located at 1.3720, followed by 1.3685. On the flipside, resistance is located at 1.3765.

USD/CAD

The USD/CAD has peeled back from recent highs but continues to trade well above 1.2800. The pair held on to the 1.2832 level in early Asian trading, with the bulls eyeing 1.2900. To get there, it needs to get over the mid-1.2800 region. On the opposite side of the ledger, immediate support is seen at 1.2845

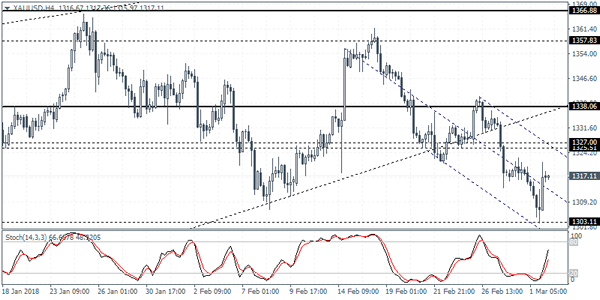

XAUUSD Intraday Analysis

XAUUSD (1317.11): Gold prices closed with a doji pattern yesterday with price action indicating a corrective move to the upside. Following the breakdown of the support level near 1327 - 1325, gold prices briefly tested the 1303 level before reversing strongly. We expect to see the upside momentum, pushing gold prices back to the breached support level where resistance could now be established. Watch for a reversal at this level as we expect the declines to continue lower back to 1303 level.

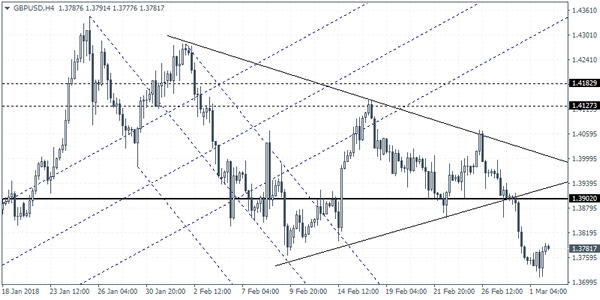

GBPUSD Intraday Analysis

GBPUSD (1.3781): The British pound braces for a volatile day as the British Prime Minister Theresa May and the BoE Governor, Mark Carney are expected to speak today. Following the strong declines earlier this week, GBPUSD managed to stabilize as price action was seen closing with a spinning bottom pattern on Thursday. This could suggest some near term upside in GBPUSD. A reversal could potentially signal an upside correction as price action could be seen rising towards 1.3900 where resistance is likely to be established.

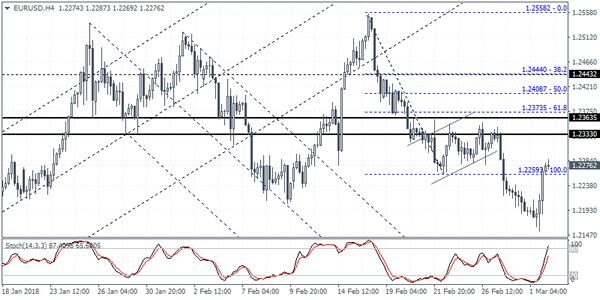

EURUSD Intraday Analysis

EURUSD (1.2276): The EURUSD was seen closing with strong gains as price action posted a bullish engulfing pattern on the daily chart. This could suggest some upside momentum in price action. Currently, EURUSD is seen trading near the 1.2260 level. A reversal near this price level could suggest the bearish trend being resumed. However, further continuation could put EURUSD on path to retest the major resistance level near 1.2333 and could invalidate the bearish flag pattern. Watch for a hidden bearish divergence on the 4-hour Stochastics indicator which could signal a move to the downside.

USD Whipsaws, Busy Day For The GBP

The U.S. dollar whipsawed yesterday after the Fed Chair, Jerome Powell returned to testify to the U.S. Congress as part of the two day semi-annual testimony. In his recent remarks, Powell said that there were "no signs of wage inflation" as yet but more gains can come before inflation starts to rise. Powell also said that the labor market could continue to strengthen without causing inflation to rise.

The remarks were seen to be toned down compared to the first statement where the markets understood Powell's comments to be more hawkish.

The U.S. President Trump announced yesterday that new tariffs for steel and aluminum imports would come into effect next week. The U.S. is set to raise the tariffs on imports by 25% and 10% respectively. The equity markets reacted strongly by closing weaker on the day.

On the economic front, the Fed's preferred gauge of inflation, the core PCE price index was seen rising 0.3% on the month, matching estimates and accelerating from 0.2% previously. The ISM manufacturing PMI accelerated to 60.8 beating estimates of 58.7 and extending from January's 59.1.

Looking ahead, the economic calendar today will see the release of the UK's construction PMI. Economists forecast a print of 50.5 which is slightly higher from January's 50.2 print. The British PM May is expected to speak later today while the BoE Governor Carney is also scheduled to speak.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.2256

The reversal at 1.2160 support should be considered corrective and current resistance at 1.2280 is expected to initiate a new slide, towards 1.2090. Key intraday support lies at 1.2220.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2280 | 1.2460 | 1.2220 | 1.2160 |

| 1.2350 | 1.2560 | 1.2160 | 1.2090 |

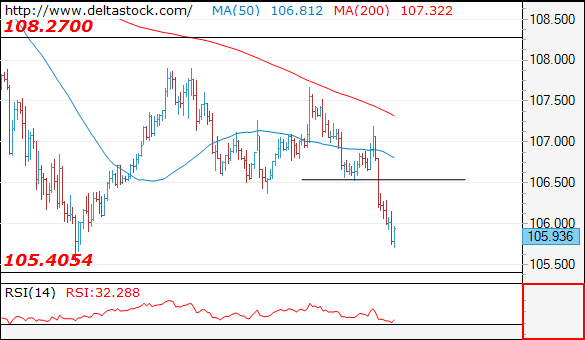

USD/JPY

Current level - 105.93

The bias is negative after the break though 106.50, as the pair is ready to test the lower boundary of the current range, at 105.50. My outlook is counter-trend against 105.50, for an upswing towards 108.30.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 106.50 | 108.30 | 105.40 | 105.40 |

| 107.60 | 110.40 | 104.30 | 102.40 |

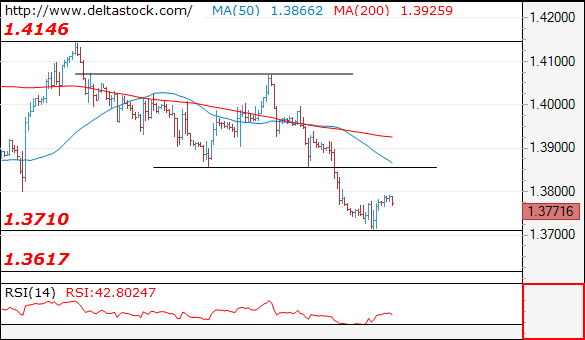

GBP/USD

Current level - 1.3771

Intraday allow a corrective rebound towards 1.3850, before another drowning towards 1.3620 major support.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3850 | 1.4280 | 1.3710 | 1.3620 |

| 1.4070 | 1.4340 | 1.3620 | 1.3620 |

USDCAD Holds Around 2-Month High, Bullish Bias But Possibility Of Overstretched Rally

USDCAD has advanced considerably to a more than a 2-month high of 1.2895 during Thursday’s session, however, it ended the day slightly above its opening level. The price posted the fourth straight bullish day and the aggressive positive rollercoaster started after the rebound on 1.2460 support level. The short-term momentum indicators seem to be in agreement with the positive scenario.

Technically, in the daily timeframe, the MACD oscillator is rising with strong momentum above its trigger and zero lines, while the RSI indicator is flattening slightly below the overbought zone, suggesting that the latest upswing may be running out of steam and that the risk of a near-term correction is high.

In case of a break above the 1.2910 strong resistance level, which is holding near the 50.0% Fibonacci retracement level of the downleg from 1.3800 to 1.2060, the pair could extend its gains towards the 61.8% Fibonacci mark at 1.3130.

On the flip side, if the 38.2% Fibonacci level fails, then the focus could shift to the downside and USDCAD could touch the 1.2460 support barrier. As a side note, the price needs to go through the 20 and 40 simple moving averages at 1.2631 and 1.2520 respectively at the time of writing.

Stocks Slip & USD Weakens As Risk-Off Returns With Announcement Of US Tariffs On Steel & Aluminium

Yesterday, the US announced Tariffs on Steel and Aluminium, which prompted an outcry from various global leaders and an acceleration in the risk-off bias affecting markets this week. The White House signalled a 25% tariff on Steel and a 10% tariff on Aluminium, starting next week. EU’s Junker said that he strongly regrets US restrictions on steel and aluminium affecting the EU, which will react firmly to defend interests with a proposal for WTO compatible countermeasures against the US within the next few days. The Canadian Trade Minister said any US tariff quota imposed on Canadian steel would be unacceptable. S&P 500 sold off to 2670.00, with the Dow Jones down to 24533.0, while Gold moved up to 1320.20. In FX, USDJPY fell from 107.193 to a low of 106.161 but has continued overnight to reach 105.744. GBPUSD reached a high of 1.37846, while EURUSD got up to 1.22726.

Polish Purchasing Manager Index (Feb) was 53.7 v an expected 54.1, from 54.6 previously.

Swiss Real Retail Sales (YoY) (Jan) was -1.4% v an expected 1.1%, from 0.6% previously, which was revised up to 0.7%.

German Markit Manufacturing PMI (Feb) was 60.6 v an expected 60.3, from 60.3 previously. EURUSD moved lower from 1.22010 to 1.21797 after this data.

Italian Unemployment (Jan) data was released, coming in at 11.1% against an expected reading of 10.8%, from 10.8% previously, which was revised up to 10.9%.

Eurozone Markit Manufacturing PMI (Feb) was 58.6 v an expected 58.5, from 58.5 previously.

UK Markit Manufacturing PMI (Feb) was 55.2 v an expected 55.0, from 55.3 previously. Consumer Credit (Jan) was £1.357B v an expected £1.40B, from a prior £1.52B, which was revised up to £1.58B. Mortgage Approvals (Jan) were 67.478K v an expected 62.000K, from a previous 61.039K, which was revised up to 61.692K. GBPUSD initially moved higher to 1.37636 before selling off to 1.37272 after this release.

Eurozone Unemployment Rate (Jan) data was released as expected, with a reading of 8.6%, from 8.7% previously, which was revised down to 8.6%. This was the lowest level for this data since the highs of 12.2% in October 2013 and compares well with the 2003 to 2005 period. EURUSD moved higher from 1.21796 to 1.21958, as the EUR gained strength from the positive data.

US Personal Consumption Expenditures – Price Index (YoY) (Jan) was 1.7% v an expected 1.6%, from 1.7% previously. Core Personal Consumption Expenditures – Price Index (MoM) (Jan) was as expected at 0.3%, from 0.2% previously. Personal Consumption Expenditures – Price Index (MoM) (Jan) was 0.4% v an expected 0.0% from 0.1% previously. Personal Income (MoM) (Jan) was 0.4% v an expected 0.3%, from 0.4% previously. Personal Spending (Jan) was as expected at 0.2%, from 0.4% previously. Core Personal Consumption Expenditures – Price Index (YoY) (Jan) was as expected, unchanged at 1.5%. Continuing Jobless Claims (Feb16) were 1.931M v an expected 1.930M, from 1.875M previously, which was revised to 1.874M. Initial Jobless Claims (Feb 23) was 210K v an expected 226K, from 222K previously, which was revised down to 220K. USDJPY moved higher from 106.755 to a high of 107.043 as a result of this data.

Canadian Current Account (Q4) was -16.35B v an expected -17.80B, from -19.35B prior. USDCAD fell from 1.28638 to 1.28408 after this release. Canadian Markit Manufacturing PMI (Feb) was released at 55.6 against an expected 55.8, from 55.9 prior.

US Markit Manufacturing PMI (Feb) was 55.3 v an expected 55.9, from a prior read of 55.9.

US Fed Chairman Powell testified on the Semi-annual Monetary Policy Report before the House Financial Services Committee, in Washington DC. He made the following comments: The US economy is near full employment but force participation and wage growth still have some slack. “More strengthening can take place in the jobs market before wage inflation”. He said that there is “No evidence the economy is currently overheating” and he would expect to see more wage hikes adding “That’s what we’re waiting to see”. He said that, in order to prolong the recovery, we believe “gradual” hikes are the best course of action and 4 hikes would be considered “gradual”.

US ISM Prices Paid (Feb) was 74.2 against an expected of 70.5. The previous reading was 72.7. ISM Manufacturing PMI (Feb) was also out at this time, coming in at 60.8 against an expectation for a number of 58.7, from 59.1 prior. Finally, Construction Spending (MoM) (Jan) was 0.0% v an expected 0.3%, from the previous reading of 0.7%, which was revised up to 0.8%. USDCAD dropped to 1.28124 but recovered to 1.28550 as a result of this data.

New Zealand Building Permits s.a. (MoM) (Jan) was released at 0.2%, from -9.6% previously, which was revised up to -9.5%.

Japanese Job/Applicants Ratio (Jan) was 1.59 v an expected 1.60, from 1.59 previously. Unemployment Rate (Jan) was 2.4% v an expected 2.7%, from 2.8% previously.

EURUSD is unchanged overnight, trading around 1.22627.

USDJPY is down -0.30% in early session trading at around 105.904.

GBPUSD is unchanged this morning, trading around 1.37781.

Gold is up 0.04% in early morning trading at around $1,317.10.

WTI is down -0.77% this morning, trading around $60.82.

Major data releases for today:

At 08:10 GMT, ECB’s Mersch is expected to deliver a speech, with any mention of monetary policy or an end to QE likely to influence EUR markets.

Tentative – UK PM May is expected to deliver a speech on Brexit progress and the ongoing negotiations with the EU. Of particular interest will be policy on trade regulations and the Northern Irish border. Her comments could impact GBP and EUR markets.

At 09.30 GMT, UK Construction PMI (Feb) will be released and is expected at 50.5 with a prior number of 50.2. GBP crosses may experience volatility if the number differs from the expected reading. This data is based on a survey of purchasing managers, with a reading above 50 indicating expansion and below 50 indicating contraction. This number has been trending down since a high of 64.7 in February 2014. Positioned close to 50, there is a danger that the trend is maintained and contraction is experienced, which would be negative for the GBP, as occurred in October 2017.

At 10:00 GMT, BOE Governor Mark Carney is due to speak about the evolution of money and the emergence of cryptocurrencies, in London.

At 10:00 GMT, Eurozone Producer Price Index (YoY) (Feb) is expected to be 1.6% from 2.2% previously. EUR crosses could be moved by this data, with a positive reading greater than the consensus adding strength to the EUR.

At 13:30 GMT, Canadian Gross Domestic Product (MoM) (Dec) is expected at 0.1%, with a prior reading of 0.4%. The range of this data point since 2010 has been between +0.6% and -0.6%, and a reading outside of this range would result in a larger market reaction. Gross Domestic Product Annualized (QoQ) (Q4) is expected at 2.0%, with a prior reading of 1.7%. CAD pairs could experience volatility before and after this data is released.

At 18:00 GMT, Baker Hughes US Rig Count numbers will be released. The prior number last Friday showed that there were 799 Oil rigs in operation. WTI Oil traders will be paying close attention to this number as they look to the week ahead, with an increase from the prior week showing an expansion and indicating an increase in the volume of crude oil drilled. In the context of supply and demand, this would mean an increase in supply. The Number of operational rigs has not been at the 800 level since 2015.

Currencies: Trade War Fears Block USD Rebound, For Now

Sunrise Market Commentary

- Rates: US protectionism spoils risk sentiment

US protectionism caused a sell-off on stock markets from which core bonds profited via safe haven flows. Last month, the same news triggered weakness in core bonds on fears of retaliation from China via lower Treasury purchases. For now, we think of it as a healthy correction. The German 10-yr yield tests important support at 0.62% - Currencies: Trade war fears block USD rebound, for now

The dollar rebound was blocked by a less hawkish comments of Fed's Powell and, even more, by US president Trump's announcement of import tariffs on an steel and aluminum. US trade policy and EMU politics will be the main drivers for USD trading today. Sterling traders will closely monitor whether PM May can ease EU/UK tensions with her Brexit speech.

The Sunrise Headlines

- Stock markets in Asia extended WS's rout (-1.5%), as investors were spooked by the specter of a global trade war after President Trump announced the US would impose hefty tariffs on steel (25%) and aluminium (10%) imports.

- Japan's jobless rate fell to an almost 25-yr low in January (2.4%), while the job-to-applicant ratio remained at a 44-yr high (1.59). Tokyo CPI ex-fresh food rose faster than forecast in February (0.9% Y/Y).

- President Trump is likely to nominate Columbia University economist Clarida to become Fed vice chair, according to the WSJ. He is a Republican economist whom colleagues describe as more of a pragmatist than an ideologue.

- NY Fed governor Dudley said that 4 rate hikes this year would still be gradual. Fed chair Powell sounded somewhat less hawkish on his 2nd day of testimony before US Congress, adding that the US economy is not at risk of overheating.

- Catalonia's former leader Puigdemont pulled back from a bid for a second term in office, dealing a blow to the Spanish northeastern region's secessionist movement. However, it might open the regional political deadlock.

- ECB policymakers are likely to discuss a small tweak in their communication stance at their March 8 meeting but no major policy shift is expected, three sources with direct knowledge of the discussion said.

- Today's eco calendar is uneventful apart from the UK with PM May's Brexit speech and the construction PMI

Currencies: Trade War Fears Block USD Rebound, For Now

Trump's tariff plans block USD rebound

The dollar first gained modest further ground yesterday; a continuation of the post-Powell rebound. The 2-yr US/German yield differential grew to 280 bps, the highest since 1997! US data (claims and ISM) were strong. PCE deflators printed as expected (0.4% M/M and 1.7% Y/Y). EUR/USD set a minor low below 1.2165. However, in yesterday's Q&A, Powell was less hawkish than on Tuesday (no overheating of the economy). Later, the dollar was hammered as US president Trump announced tough import tariffs on steel and aluminum. US equities, US yields and the dollar nosedived. EUR/USD closed at 1.2267. USD/JPY finished at 106.24.

Trump's action on import tariffs dominates the overnight price action. Most Asian equity indices are trading in negative territory. Japan underperforms (losses of up to 2.0%). Losses in China stay modest. The Japanese jobless rate declined sharply to 2.4% and Tokyo inflation was a touch higher than expected. BoJ's Kuroda sees a chance of hitting 2% inflation in FY 2019. At that time he will consider the timing of the exit. This is sure something to keep an eye on! USD/JPY dropped below 106. EUR/USD trades in the 1.2270 area.

The focus for (FX) trading will be on the US import tariffs and its consequences for global trade, and on European politics (Italian election and SPD approval of new government). A reaction of trading partners to the US tariffs might sent shivers through markets, but we don't expect this theme to become a lasting negative for markets or the dollar. EMU politics was seldom a big issue for global (FX) trading. Some euro caution ahead of the weekend is possible, but nothing more than that. Yesterday's rejected test of the EUR/USD 1.2165 area is slightly disappointing for USD bulls ST. However, the battle might not be over yet. If the dust on the tariffs issue settles, a retest remains possible.

Today, all eyes in the UK and EU are on PM May's speech. She brings her view on the partnership with the EU. She might advocate a trade deal deeper than anywhere else in the world. However, the EU probably will consider this cherrypicking. We doubt the speech will bring a breakthrough. Sterling already lost some ground on Brexit-uncertainty this week. EUR/GBP again nears the 0.8930 area. A break would again bring the 0.9033 range top on the radar. We expect no break.

EUR/USD: test of 1.2165 rejected as Trump announces import tariffs on steel and aluminum