Sample Category Title

Currencies: EUR/USD Tests Key Support. Sterling Feels Brexit Headwinds

Sunrise Market Commentary

- Rates: Consolidation on core bond markets

Monthly US PCE readings are expected at relatively high levels while consensus forecasts a small setback in the manufacturing ISM, but we see downside risks. Any rebound of US Treasuries will probably be short-lived with Fed Powell's comments in mind. The Bund tends to outperform in recent days ahead of this weekend's European political risk. - Currencies: EUR/USD tests key support. Sterling feels Brexit headwinds.

Optimistic comments of Fed Powell kept the dollar near recent highs. EUR/USD is testing the 1.22/1.2165 support area, but a real break didn't occur yet. Today's US data maybe won't be strong enough to force the break, but the battle will continue. Sterling is sold as Brexit tensions are mounting ahead of PM May's Brexit speech tomorrow.

The Sunrise Headlines

- US equity markets lost another 0.75% (Nasdaq) to 1.5% (Dow) yesterday. Asian markets lose ground as well this morning with Japan underperforming (-1.5%) and China outperforming (small gains).

- President Trump is set to announce steep tariffs on steel (25%) and aluminium (10%) imports in what would be one of his toughest actions yet to implement a hawkish trade agenda that risks antagonizing friends and foes alike.

- Growth in China's manufacturing sector unexpectedly picked up to a six-month high in February (Caixin PMI: 51.6 from 51.5) as factories rushed to replenish inventories to meet rising new orders.

- Theresa May said that no UK prime minister could ever accept new EU proposals that could keep Northern Ireland under the bloc's rules, as she hit out at Brussels first draft of a Brexit treaty.

- BoJ Kataoka cautioned against a premature exit from the BOJ's ultra-loose monetary policy and called for a ramping up of the bank's massive stimulus programme.

- Brent crude dropped from $67.5/barrel to $64.5/barrel the past two days. US crude stockpiles unexpectedly rose to the highest level YTD. Meanwhile, a shale boom sent US production to a record high in November.

- Today's eco calendar heats up in the US with PCE deflator, manufacturing ISM, weekly jobless claims. The UK manufacturing PMI and EMU unemployment rate will also be published. Fed Powell speaks. Spain and France tap the market

Currencies: EUR/USD Tests Key Support. Sterling Feels Brexit Headwinds

EUR/USD test of 1.22/1.2165 continues

The (trade-weighed) dollar held near the post-Powell top yesterday, but there were no big follow-through gains. EMU inflation (1.2% Y/Y) was soft but with little impact on FX. US yields/interest rate differentials didn't rise further. Markets want confirmation on Powell's optimistic assessment from US data. EUR/USD hovered close to, but mostly slightly north of 1.22 (close 1.2194). USD/JPY suffered a late session setback as equity sentiment dwindled. The pair closed the session at 106.68.

Most Asian indices are trading in negative territory. China outperforms. The Caixin manufacturing PMI was marginally stronger than expected contrary to the ‘official' PMI's yesterday. Japanese data, including Q4 capital spending, were OK. Even so, BOJ officials confirm the need for further policy stimulation. Those monetary interventions don't weaken the yen for now. USD/JPY is holding in the 106.50/85 area. EUR/JPY struggles no to fall below 130. EUR/USD (near 1.2190) tries to sustain below the 1.2206 neckline. USD strength prevails except for USD/JPY.

US income and spending data and the manufacturing ISM have market moving potential today. The PCE deflator is expected at 0.4% M/M and 1.7% Y/Y. The consensus for the monthly rise is quite high. A positive surprise won't be easy. The ISM manufacturing is expected at 58.7 from 59.1. We see downside risks. In a daily perspective, the data probably won't support further USD gains. Equity sentiment and the second part of Powell's hearing before Congress are wildcards. A negative equity sentiment was a tentative USD supportive (ex USD/JPY) of late. We advocated consolidation of EUR/USD in the 1.25/1.2165 range ahead of the Powell hearing. The Powell comments brought the range bottom within reach. Chances on a break are growing if the key early month US data confirm solid US growth. Preparing a revisit of the 1.20 level? Further EUR/JPY losses might also weigh EUR/USD.

The open rift between the EU and the UK on the EMU draft Brexit text weighed on sterling yesterday. EUR/GBP jumped back higher to the 0.8850 area. Today, the UK manufacturing PMI is expected to ease slightly from 55.3 to 55.0. Sterling might be slightly more sensitive to a negative surprise than to a positive one. Still, the focus remains on tomorrow's Brexit speech of PM May. There are no signs that the EU and the UK will reach a compromise soon. Sterling will probably stay in the defensive, but we don't see a break out of the 0.87/0.9033 range.

EUR/USD: testing key 1.2206/1.2165 support.

Sterling Stumbles Into March While Dollar Extends Gains

Market optimism over a 'soft Brexit' outcome sharply deteriorated on Wednesday, after the European Union published a draft withdrawal agreement calling for Northern Ireland to stay in the customs union.

Theresa May flatly rejected the European Union's conditions, calling the proposal unacceptable and one which 'undermines the constitutional integrity of the UK'. With EU's chief Brexit negotiator Michel Barnier stating that a transitional deal was not guaranteed, fears are likely to heighten over a possible Brexit 'no deal' scenario. Sterling could be instore for further punishment moving forward, as the renewed Brexit jitters continue to weigh heavily on sentiment.

Some attention may be directed towards the UK manufacturing PMI report this morning, which is expected to print at 55.1 in February. While a figure that exceeds market expectations could offer the Pound some minor support, the currency is likely to remain more concerned with Brexit developments.

Taking a look at the technical picture, the GBPUSD is under intense selling pressure on the daily charts. The breakdown and daily close below 1.3850 could invite a decline towards 1.3750 and 1.3670, respectively.

Dollar higher ahead of Powell's second testimony

The Dollar held its ground against a basket of major currencies on Thursday morning ahead of the second session of Federal Reserve Chairman Jerome Powell's testimony later in the day.

Hawkish comments from Powell have fuelled market speculation of the Federal Reserve raising US interest rates four times this year – ultimately supporting the Dollar. Market expectations of higher US rates could intensify further if the new Fed head doubles down on hawkish comments made earlier in the week.

Taking a look at the technical picture, the Dollar Index is bullish on the daily timeframe. Prices are approaching the 50 Simple Moving Average while the MACD trades to the upside. A daily close above the 90.55 level could encourage a further incline higher towards 91.00.

Currency spotlight – EURUSD

The Euro weakened against the Dollar on Wednesday, following reports of Eurozone inflation slowing to a 14-month low at 1.2% in February.

Euro bears received further inspiration in the form of political uncertainty, thanks to the looming Italian national election on Sunday. With the Dollar boosted by heightened expectations of higher US interest rates, the EURUSD found itself under heavy selling pressure. From a technical standpoint, the EURUSD is turning increasingly bearish on the daily charts. Prices are trading below the 50 Simple Moving Average while the MACD has crossed to the downside. A breakdown and daily close below the 1.2180 level could invite a decline towards 1.2090.

The Fed’s Jerome Powell Is Due To Testify Before The Senate Banking Committee

Market movers today

Today, we are publishing the fourth paper in a series of five on inflation and what it means for financial markets. In this paper we look into what it means for fixed income. See Part 4: EUR Fixed Income - Misaligned rates and inflation markets .

In the US, we have two important data releases. Based on the higher-than-expected CPI data in January, we estimate PCE core rose 0.3% m/m (close call between 0.3% and 0.4% in the case of CPI, so do not be surprised by a 0.4% print here). We think this would be enough to lift the PCE core inflation rate to 1.6% (consensus 1.5%). ISM manufacturing is also due out today and we estimate the index to have been broadly unchanged around the current level of 59.1. We have seen mixed signals from Markit PMI and regional PMIs.

The Fed's Jerome Powell is due to testify before the Senate Banking Committee but we do not expect him to say anything new. In our view, Powell was slightly hawkish on Tuesday, see Flash Comment US: Powell says 'personal outlook has strengthened'.

In the UK, we estimate the PMI manufacturing index stayed around 55.3 in February. Also, keep an eye on any new Brexit comments and possible leaks from PM Theresa May's speech tomorrow (usually leaked late afternoon).

In the Scandies, PMI manufacturing is due in both Norway and Sweden.

Selected market news

Risk sentiment soured yesterday as investors worry about faster Fed rate hikes and some signs that the global cycle is weakening. The losses in the stock market should also be seen in the light of the recent market recovery, which may have been used by investors to take some risk off the table. Bond yields retreated again yesterday, adding to signs that the big bond market sell-off seen in the first two months of the year is over for now. US data also surprised on the downside again as Chicago PMI fell to 65.7 in February from 61.9 and pending home sales dropped 4.7% m/m in January. Bonds also got some tailwind from a slide in oil prices following data, which showed a rise in US oil inventories.

In China, the private version of manufacturing PMI from Caixin surprised on the upside rising to 51.6 in February (consensus 51.3) from 51.5 in January. It is in sharp contrast to the official PMI manufacturing from NBS released yesterday, which surprised strongly on the downside. Which one is right? We belief the true picture is somewhere in the middle. That China is slowing but only moderately - as also signalled by the development in global metal prices where the upward pace has eased somewhat but not pointed to a sharp slowdown in demand.

US President Donald Trump warned China again yesterday on the trade front, saying that the US will use 'all available tools' to protect the US from China's state-driven economic model, which he says undermines global competition, see Bloomberg . The warning came in the President's annual report to Congress on his trade-policy agenda.

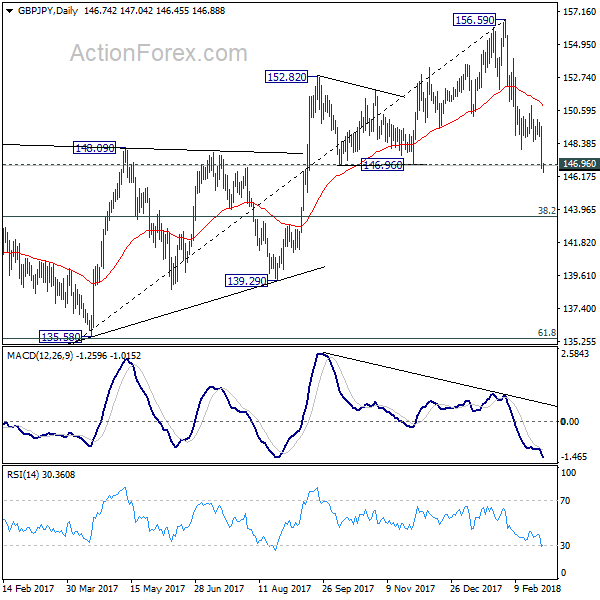

GBP/JPY Daily Outlook

Daily Pivots: (S1) 145.82; (P) 147.67; (R1) 148.62; More...

Intraday bias in GBP/JPY remains on the downside as fall from 156.59 is in progress. Considering bearish divergence condition in daily MACD, firm break of 146.96 will be another sign of medium term trend reversal. And GBP/JPY should target 143.51 medium term fibonacci level next. On the upside, break of 150.92 resistance is needed to confirm short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, the case for medium term reversal continues to build up on loss of medium term momentum as seen in weekly MACD. Also, firm break of 146.96 will indicate rejection by 55 month EMA (now at 154.60) and add to that case of reversal. In that case, deeper fall would be seen to 38.2% retracement of 122.36 to 156.59 at 143.51 and then 61.8% retracement at 135.43. Meanwhile, break of 156.59 will extend the rise from 122.36 to 61.8% retracement of 195.86 to 122.36 at 167.78.

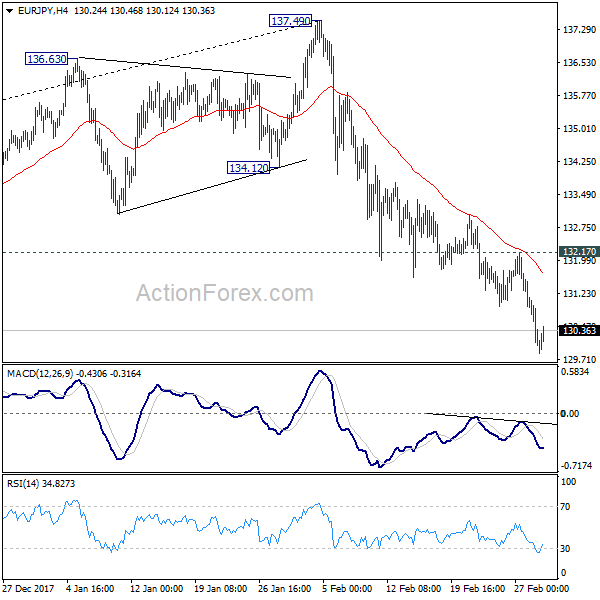

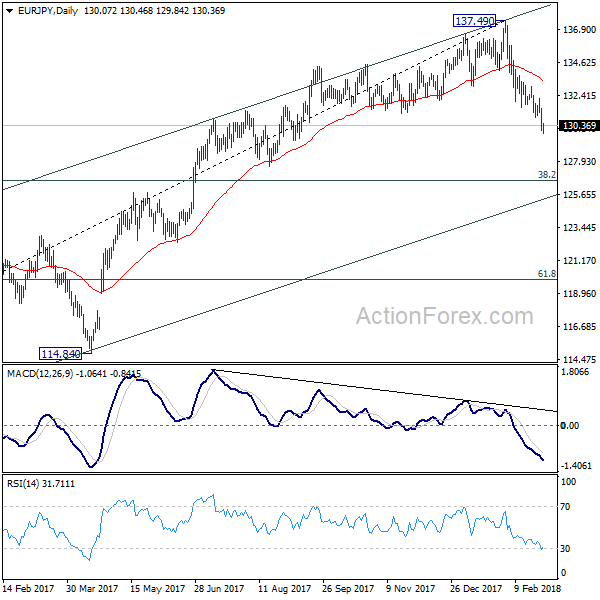

EUR/JPY Daily Outlook

Daily Pivots: (S1) 129.57; (P) 130.54; (R1) 131.05; More....

Intraday bias in EUR/JPY remains on the downside as fall from 137.49 is in progress. As noted before, a medium term top is likely in place at 137.49 on bearish divergence condition in daily MACD. Deeper decline should be seen to 126.61 medium term fibonacci level next. On the upside, break of 132.17 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, current development argues that rise from 109.03 has completed at 137.49, on bearish divergence condition in weekly MACD. Deeper fall should be seen to 38.2% retracement of 109.03 to 137.49 at 126.61 first. On the upside, break of 137.49 is needed to confirm medium term rise resumption. Otherwise, risk will now stay on the downside even in case of strong rebound.

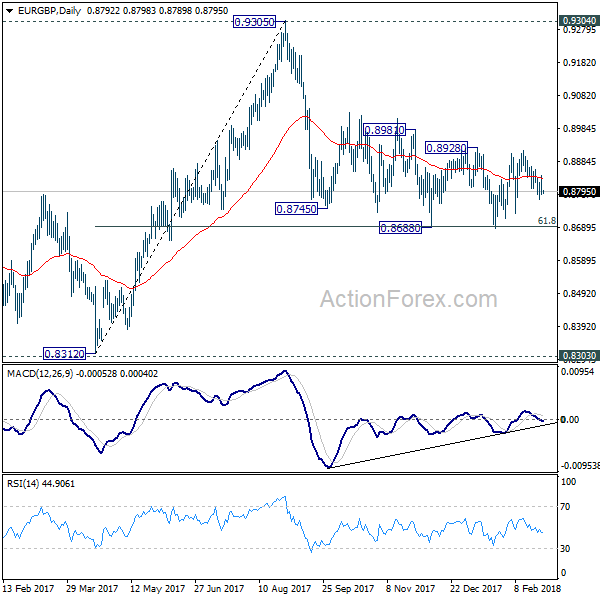

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8805; (P) 0.8835; (R1) 0.8892; More...

Range trading continues in EUR/GBP inside 0.8686/8928. Intraday bias remains neutral. Also, outlook stays mildly bearish with 0.8928 resistance intact. On the downside, firm break of 0.8686 will resume whole decline from 0.9305. As 61.8% retracement of 0.8312 to 0.9305 should then be taken out too, deeper decline would be seen to retest 0.8303/8312 support zone. Nonetheless, on the upside, break of 0.8928 will indicate near term reversal and turn outlook bullish for 0.9304 resistance.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

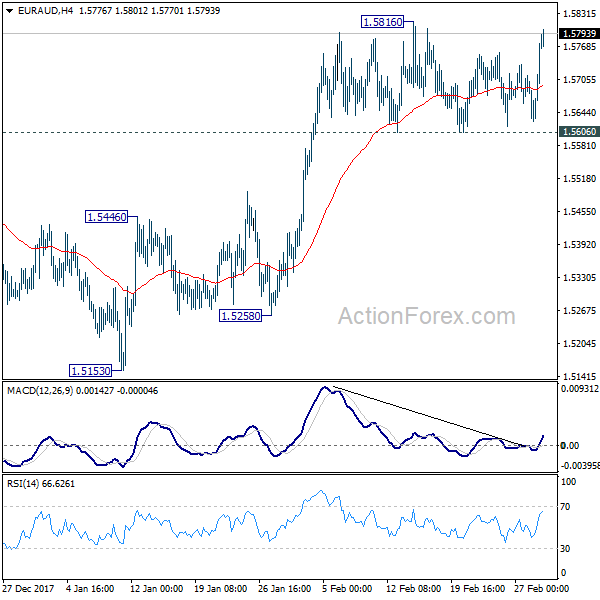

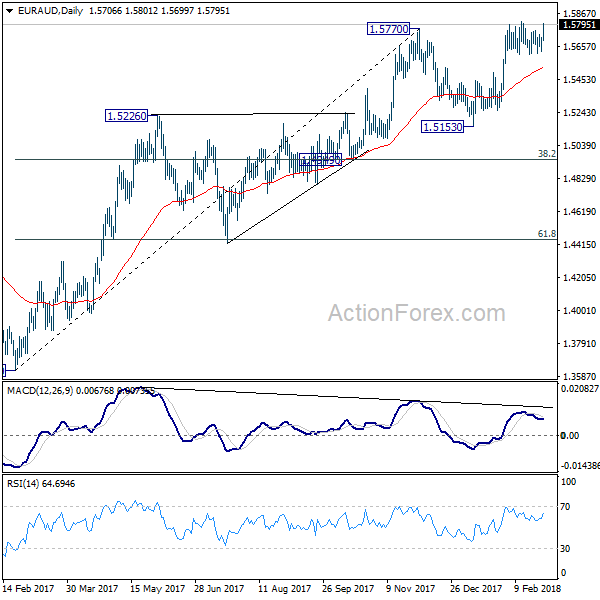

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5651; (P) 1.5683; (R1) 1.5740; More....

At this point, EUR/AUD is still bounded in range below 1.5816 and intraday bias stays neutral. With 1.5606 support intact, near term outlook remains bullish for further rally. On the upside, break of 1.5816 should now confirm resumption of medium term rise from 1.3264. In that case, EUR/AUD should target 1.6587 key long term resistance. Meanwhile, firm break of 1.5606 will argue that a short term top is formed. Intraday bias will be turned back to the downside for 55 day EMA (now at 1.5531) and below.

In the bigger picture, medium term rise from 1.3624 is not completed yet. Sustained break of 1.5770 will extend the rise to retest 1.6587 (2015 high). However, considering bearish divergence condition in daily MACD, break of 1.4949 cluster support (38.2% retracement of 1.3624 to 1.5770 at 1.4950) will indicate medium term reversal. And there is prospect of retesting 1.3624 low in that bearish case.

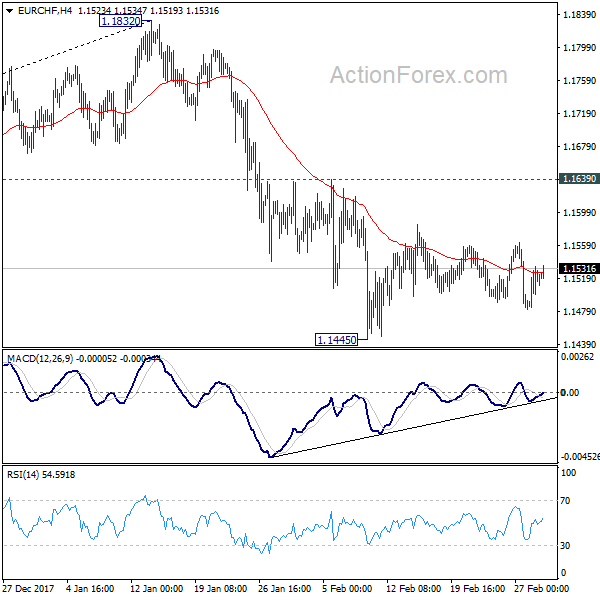

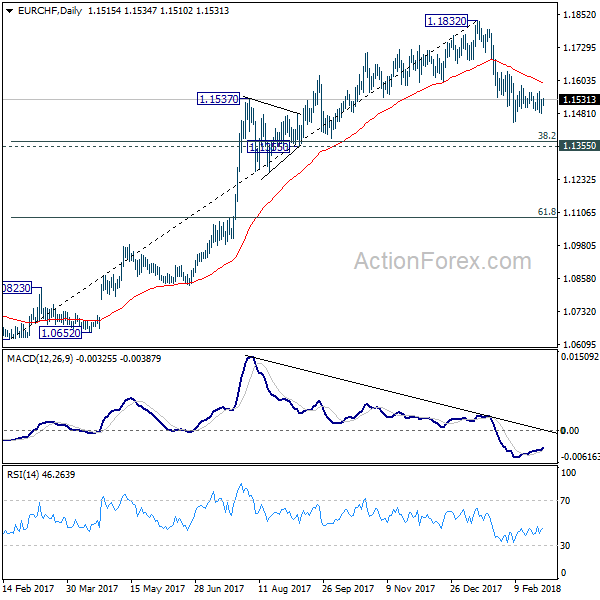

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1487; (P) 1.1510; (R1) 1.1540; More...

Intraday bias in EUR/CHF remains neutral as the consolidation from 1.1445 is still in progress. Outlook stays mildly bearish with 1.1639 resistance intact and deeper decline is expected. Break of 1.1445 will resume the corrective fall from 1.1832 and target 1.1355 cluster support (38.2% retracement of 1.0629 to 1.1832 at 1.1372.) At this point, we'd expect strong support from there to contain downside and bring rebound.

In the bigger picture, a medium term top should be in place at 1.1832 on bearish divergence condition in daily MACD. But there is no indication of long term reversal yet. As long as 1.1198 resistance turned support holds, we'd still expect another rise through prior SNB imposed floor at 1.2000.

Market Update – Asian Session: China Caixin PMI Assures Markets Of Growth

Headlines/Economic Data

General Trend: Asian equity markets trade mixed after earlier declines in the US

China Feb Caixin PMI Manufacturing index rises to 6-month high, despite decline seen in the official index

Aluminum Corp of China (CHALCO) said there was no ‘major’ information to be disclosed following its share price declines

Chinese aluminum and steel names under pressure as markets expect President Trump to announce 20 and 25% tariffs respectively

President Trump said to plan emergency meeting with steel and aluminum execs on Thursday

Meanwhile, China President Xi’s top economic adviser is expected to meet on Thursday with top Trump Administration officials, including Treasury Sec Mnuchin

BoJ dovish dissenter Kataoka reiterates more easing is needed

US dollar (USD) in focus ahead of Fed Chair Powell’s second day of testimony

Japan

Nikkei 225 opened -0.8%; closed -1.6%

TOPIX Iron & Steel Index -1.8%, Electric Appliances -1.6%

Japan mega-banks trade broadly lower, track earlier declines in the US financial sector

Automakers decline after Wednesday’s gain in the Yen

(JP) JAPAN Q4 CAPITAL SPENDING EX SOFTWARE: 4.7% V 2.7%E; CAPITAL SPENDING Y/Y: 4.3% V 3.0%E; Company Profits: 0.9% v 5.5% prior; Company Sales: 5.9% v 4.8% prior

Kawasaki Heavy,[-5.5%], 7012.JP Confirms quality problem with N700-Series Shinkansen car undercarriages

(JP) Japan final Feb PMI Manufacturing: 54.1 v 54.0 prelim

(JP) BoJ Gov Kuroda: Reiterates BOJ's easing has contributed to growth – parliament

(JP) BoJ Kataoka: Still 'quite distant' from mulling shift from easy policy, must ease more to achieve price goal quickly ; 2019 GDP likely to fall to 0.5-1.0%

(JP) Japan PM Abe: BOJ Gov Kuroda's policies have not been wrong to date, want him to keep working towards 2% target - parliament

(JP) Nikkei looks at how BOJ Gov Kuroda may not serve a full term after being reappointed

(JP) Japan MoF sells ¥2.3T v ¥2.3T indicated in 0.1% (prior 0.1%) 10-yr JGB; avg yield 0.062% v 0.088% prior; bid to cover 4.53x v 4.58x prior

Looking Ahead: Japan Jan Unemployment rate due for release on Friday, along with the Tokyo Feb CPI data

Fast Retailing [9983.JP] is scheduled to report Feb sales on Friday (prior figures came after the market close)

Korea

Kospi closed for holiday

SK Telecom, 017670.KR CEO Jung-ho: Working on wearable technology called “The Sleeve” that will be enabled by the fifth-generation telecom network with Nokia Bell Labs - Korean press

(KR) South Korea has submitted a document rebutting US trade group representing its pharmaceutical industry that Korea’s drug pricing policies favor its domestic industry - Korean press

(KR) South Korea Feb Trade Balance: $3.31B v $2.39Be; Exports y/y: 4.0% v 0.5%e; Imports y/y: 14.8% v 12.0%e

According to KDB GM Korea may have FY17 Net loss of KRW900B (4th consecutive year of losses) - Korean press

China/Hong Kong

Hang Seng opened -0.3%, Shanghai Composite +0.1%

Hang Seng Info Tech Index +2%, Energy -0.9%

Shanghai Composite Property index has moved between gains and losses

ASM Pacific Technology [522.HK] rises over 3% after reporting Q4 earnings

(CN) China National People’s Congress to start on March 5th, will set economic targets for the coming year; Expected to keep GDP growth near or above 6.5%; Proactive fiscal policy is expected to be maintained - Xinhua

(CN) China PBoC Open Market Operation (OMO): injects CNY150B in 7-day, 28-day and 63-day reverse repos v skipped prior; Net drains CNY10B

USD/CNY (CN) PBOC SETS YUAN REFERENCE RATE AT 6.3352 V 6.3294 PRIOR

(CN) CHINA FEB CAIXIN PMI MANUFACTURING: 51.6 V 51.3E (6-month high)

(CN) China Securities Regulator (CSRC) said to have asked some funds to avoid net selling during National People's Congress, which may account for the selling seen this week - press

(HK) Macau Feb Casino Rev (MOP) 24.3B v 26.3B prior; Y/Y: +5.7% v 9.0%e

Australia/New Zealand

ASX 200 opened -0.4%; closed -0.7%

ASX 200 Energy Index -2.2%, Utilities -1.6%, Resources -1.6%, Consumer Discretionary -0.8%, Financials -0.5%

(NZ) New Zealand Q4 Terms of Trade Index Q/Q: 0.8% v 0.5%e

(AU) Australia Feb AiG Perf of Manufacturing Index: 57.5 v 58.7 prior

(AU) AUSTRALIA Q4 PRIVATE CAPITAL EXPENDITURE (CAPEX) Q/Q: -0.2% V 1.0%E; Equipment, plant, machinery investment +2.2% q/q; Buildings, structures investment -2.1% q/q; Sees 2017/18 Capex estimate +2.5% y/y; Australia companies plan to spend A$114.6B; Sees 2018/19 Capex estimate +3.5% y/y; Australia companies plan to spend A$84B

(NZ) New Zealand sells NZ$100M in 2.5% 2040 inflation indexed bonds; avg yield 2.1987%

(AU) Australia Prudential Regulatory Authority (APRA) Chairman Byres: 10% cap on bank lending to residential property investors was probably reaching the end of its useful life

(AU) Australia ACCC exec general manager of specialized enforcement Bezzi: As a general matter we are concerned about potential collusion in forex markets and we do have some investigations, that I am not able to go into in any detail, that touch on some of these issues - AFR

(AU) Australia Feb Commodity Index (AUD): 139.8 v 135.3 prior; Commodity Index SDR Y/Y: -1.0% v -0.6% prior

Other Asia

(TW) Taiwan Central Bank Gov Yang: NT$ gains help ease import driven inflation pressures; will take appropriate monetary policy to keep inflation stable

North America

US equity markets ended broadly lower: Dow -1.5%, S&P500 -1.1%, Nasdaq -0.8%, Russell 2000 -1.6%

S&P500 Energy -2.3%, Materials -1.8%

(VE) US Trump Administration Official: Does not rule out complete US oil embargo on Venezuela, says it would cause fairly strong shock to the oil market in the short-term

(US) US said to plan announcement on Thursday, Mar 1st related to steel and aluminum imports - US press

(US) SEC launches investigation into cryptocurrency, issued subpoenas and information requests to technology companies and advisers - financial press

(US) DOE CRUDE: +3.0M V +2ME

Looking Ahead: US Feb ISM Manufacturing PMI to be released

Europe

Carrefour [CA.FR]: Reports FY net -€531M v +€746M, Rev €88.2B v €85.7B y/y

Looking Ahead: UK Feb Manufacturing PMI due to be released

Levels as of 01:00ET

Nikkei225 -1.6%, Hang Seng -0.4%; Shanghai Composite +0.0%; ASX200 -0.7%, Kospi -1.2%

Equity Futures: S&P500 -0.3%; Nasdaq100 -0.2%, Dax -0.6%; FTSE100 -0.5%

EUR 1.2199-1.2184; JPY 106.87-106.55; AUD 0.7766-0.7717;NZD 0.7211-0.7187

Apr Gold -0.2% at $1,315/oz; Apr Crude Oil +0.0% at $61.66/brl; May Copper +0.3% at $3.14/lb

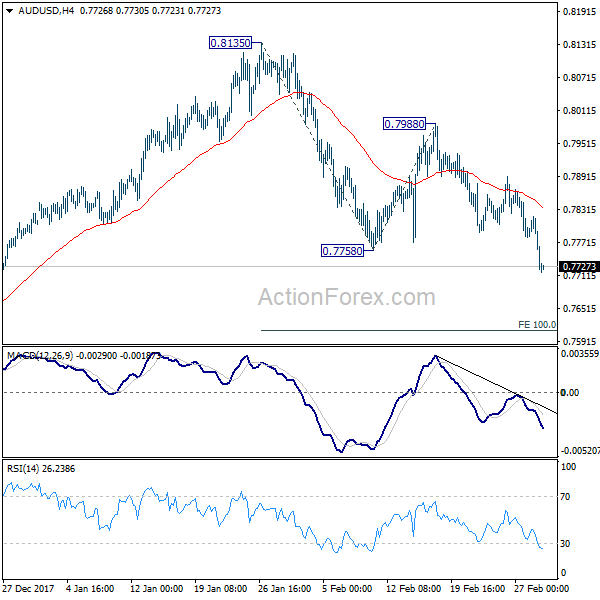

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7741; (P) 0.7780; (R1) 0.7799; More...

AUD/USD's strong break of 0.7758 confirm resumption of fall from 0.8135. Intraday bias back on the downside. Current fall should target 100% projection of 0.8135 to 0.7758 from 0.7988 at 0.7611. On the upside, break of 0.7988 resistance is needed to confirm completion of the fall. Otherwise, near term outlook will be mildly bearish even in case of recovery.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed.