Sample Category Title

USDJPY Continues Sell-Off With Weak Momentum

USDJPY has been trading considerably lower since roughly the beginning of November, hitting a 15-month low of 105.50 on February 16.

Price action is developing below the 23.6% Fibonacci retracement level near 107.70 of the downleg with the high of 114.70 and the low of 105.50. The aforementioned obstacle overlaps with the 20-day simple moving average and is following the downward movement of the price. The short-term technical indicators are neutral to bearish and point to more weakness in the market.

From the technical point of view, in the daily timeframe, the RSI indicator is moving between the 30 and 50 levels with weak momentum, while the stochastic oscillator is approaching the 20 level. Both are avoiding showing clear signals.

If price action remains below the 23.6% Fibonacci mark, there is scope to test 105.50 strong support level. Clearing this key level could see additional gains towards the 101.00 psychological barrier. This is considered to be a significant area which has been rejected a few times in the past, taken from the low in November 2016.

In case of a jump above the 23.6% Fibonacci, then the focus could shift to the upside towards the 108.20 resistance level. If this level is breached, it could increase the upside pressure and bring about a small reversal of the trend. From here, USDJPY could be on the path towards the 38.2% Fibonacci level near the 109.00 handle.

NZDUSD Holds In Narrow Range, Bearish Correction In Progress

NZDUSD is edging sharply lower over the last sessions after it created a double top at the 5-month high of 0.7435 on February 16. The double top reversal is a bearish pattern indicating further losses on the price action. When looking at the bigger picture the pair lacks a clear trend since it has been developing within a narrow range of 0.7175 – 0.7435 after its rally from 0.6780 stalled at 0.7435.

In the 4-hour chart, momentum indicators are also pointing to a continuation of the bearish bias. The MACD oscillator is standing below the trigger line and near the zero line, suggesting a further downward correction. Also, the RSI indicator dropped below the 50 level and is flattening in the negative territory.

If the price extends its losses below the lower Bollinger band and the 38.2% Fibonacci retracement level near 0.7175 of the upleg from 0.6780 to 0.7435 could open the door for the 50.0% Fibonacci mark near 0.7100. Below that, the price could hit the 0.7070 support.

On the flip side, in the event of an upside reversal, the next level to watch is the 23.6% Fibonacci level at 0.7280. A break above this level could see a re-test of the aforementioned 5-month high obstacle.

Dollar Up Gold Lower | Oil Pushed Lower | Bitcoin Losing Momentum

Dollar still on the move to the upside

Glod under pressure thanks to new Fed chairman

US Crude Oil inventory data pushed the WTI lower

Forex

The dollar index extends its bullish gains making five week highs, boosted by an upbeat assessment of the US economy from the FED’s new chairman. The lower than expected second estimate of US GDP for the fourth quarter was not enough to dent the dollar’s rally, indicating that traders may be speculating four FED interest rate rises this year instead of three. Further helping the dollar was a weaker euro that fell to 6-week lows after inflation slowed to its lowest level in 14 months. Having said this, perhaps political developments and Sunday’s Italian election may be the reason behind traders’ scepticism of the euro. GBP sell of worsened following lower than anticipated GDP figures.

Gold

Despite another red day for US equities, a stronger dollar was yet again the dominant force in determining price action for the precious metal. Gold continues to slide as traders speculate that the FED’s new chairman may be more hawkish than Yellen.

Oil

Oil dives 2.2% after US crude stockpiles rise by 3 million barrels compared with analyst expectations for a build of 2.1 million barrels. However, if producers abide to further OPEC output cuts and with the upcoming Aramco IPO, there may still be more ground for the bulls to play with in the oil market.

Cryptocurrencies

Cryptocurrencies lose some of the gains made yesterday with Bitcoin steady around $10700. However, the case for cryptocurrencies is still bullish as adoption increases with Taiwan’s new central bank brief considering using block chain for payments. This dip is likely just the markets taking a breath after what has been a bullish few weeks.

Chinese Official PMIs Fell In February

China's official PMIs surprised to the downside in February. Manufacturing PMI dropped -1 point to 50.3 in February, while non-manufacturing PMI slipped -0.9 point to 54.4. The readings came in weaker than expectations of 52.1 and 55 respectively. The Caixin manufacturing index released earlier today, however, increased to 51.6 from January's 51.5. This beat consensus of 54. Chinese economic data in the first two months of the year are usually volatile due to the week-long Lunar New Year holiday. Yet, the fact that the average of January and February manufacturing PMI (official) remains weaker than that in 4Q17 suggests caution to China's growth outlook this year.

Consider the official manufacturing PMI, the disappointment was mainly driven by the 'production' sub-index which slumped to 50.7 from January's 53.5, and the 'new order' sub-index which fell to 51 in February from 52.6 in January. Concerning other sub-indices, employment dropped -0.2 point to 48.1 in February, while imports and new exports orders sub-indices declined to 49.8 and 49, respectively. Raw materials inventory sub-index added +0.5 point to 49.3 while suppliers' delivery times dropped -0.8 point to 48.4. On inflation, the input prices sub- index plunged -6.3 point while output prices sub-index lost -2.6 points to 49.2.

The official non-manufacturing PMI covers both the services and construction sectors, roughly in 80%-20% weight. While the February services PMI also came in weaker than the January one, their average was higher than the fourth quarter's. This suggests that the growth in services activities should help offset the possible moderation in manufacturing activities.

Separately, Caixin manufacturing PMI, which focuses on small and medium firms, climbed +0.1 point to 51.6 in February. Concerning the five major sub-indices, the new orders and raw materials inventory sub-indices rose while production, employment and suppliers' delivery times eased for the month. For the average of January and February, the headline reading came in at 51.5, compared with 51.1 in 4Q17 with averages of both production and new orders sub-indices higher than those in 4Q17.

More Chinese macroeconomic data would be released later this month. Next week comes the FX reserve and trade balance. The latter would be of focus as the US is about to accelerate restrictions against China to reduce trade deficit. In response, Liu He, Chinese President Xi Jinping's top economic adviser, has arrived the US in attempt to defuse the trade tensions.

Forex Analysis: High Volume Of Data Releases And Fed Chairman Powell’s Speech Put US In Focus

German Gfk Consumer Confidence Survey (Mar) was 10.8 v an expected 10.9, from a prior number of 11.0.

French Consumer Price Index (EU norm) (YoY) (Feb) was 1.4% v an expected 1.5%, from a prior number of 1.5%. EURUSD moved lower from 1.22370 to a low of 1.22000.

Swiss KOF Leading Indicator (Feb) was 108.0 v an expected 106.1, from 106.9 previously.

German Unemployment Change (Feb) was -22K v an expected -15K, from -25K previously. Unemployment Rate s.a. (Feb) was as expected, unchanged at 5.4. EURUSD moved higher from 1.21983 to 1.22250 after this data was released.

Swiss ZEW Survey – Expectations (Feb) data was released at 25.8 from 34.5 previously.

Eurozone Consumer Price Index – Core (YoY) (Feb) was 1.0% v an expected 1.1%, from 1.0% prior. Consumer Price Index (YoY) (Feb) was as expected at 1.2%, from 1.3% previously.

US Gross Domestic Product Annualized (Q4) was as expected at 2.5%, from 2.6% previously. Gross Domestic Product Price Index (Q4) was 2.3% v an expected 2.4%, from 2.4% previously. Personal Consumption Expenditures Prices (QoQ) (Q4) was 2.7% v an expected 2.8%, from 1.5% previously, which was revised up to 2.8%. Core Personal Consumption Expenditures Prices (QoQ) (Q4) was as expected at 1.9%, from 1.3% previously, which was revised up to 1.9%. EURUSD fell to a low of 1.22021 before moving higher to 1.22278 as a result of this data.

US Chicago Purchasing Managers' Index (Feb) was 61.9 v an expected 64.2, from a prior reading of 65.7.

US Pending Home Sales (YoY) (Jan) was -1.7% v an expected -1.8%, from a prior reading of -1.8%. Pending Home Sales (MoM) (Dec) was -4.7% v an expected 0.3%, from a prior reading of 0.5%.

Australian AIG Manufacturing Index was released, coming in at 57.5 against 58.7 previously. AUDNZD moved up from 1.07594 to 1.07748 as a result of this data.

Foreign Investment in Japanese Stocks (Feb 23) was ¥-53.6B from a previous number of ¥-127.1B, which was revised up to ¥-127.2B. Foreign Bond Investment (Feb 23) was ¥-201.3B from ¥-553.1B previously. The report is released by the Ministry of Finance, detailing the flows from the public sector excluding the Bank of Japan. The net data shows the difference of capital inflow and outflow. A positive difference indicates net sales of foreign securities by residents (capital inflow), and a negative difference indicates net purchases of foreign securities by residents (capital outflow).

EURUSD is up 0.10% overnight, trading around 1.22055.

USDJPY is up 0.08% in early session trading at around 106.744.

GBPUSD is up 0.06% this morning, trading around 1.37681.

Gold is down -0.30% in early morning trading at around $1,314.10.

WTI is up 0.23% this morning, trading around $61.65.

Major data releases for today:

At 08:00 GMT, Polish Purchasing Manager Index (Feb) is expected to be 54.1 from 54.6 previously.

At 08:15 GMT, Swiss Real Retail Sales (Jan) is expected to be 1.1% from 0.6% previously.

At 08:55 GMT, German Markit Manufacturing PMI (Feb) is expected to be unchanged at 60.3. EUR crosses could be affected by this data.

At 09:00 GMT, Italian Unemployment (Jan) data will be released and is expected to be unchanged at 10.8%.

At 09:00 GMT, Eurozone Markit Manufacturing PMI (Feb) is expected to be unchanged at 58.5. EUR crosses could be moved by this data.

At 09:30 GMT, UK Markit Manufacturing PMI (Feb) is expected to be 55.0 from 55.3 previously. Consumer Credit (Jan) is expected to be £1.40B against a prior £1.52B. Mortgage Approvals (Jan) is expected to be 62.000K from a previous 61.039K. GBP pairs may be moved by this release.

At 10:00 GMT, Eurozone Unemployment Rate (Jan) data will be released, with an expected reading of 8.6% from 8.7% previously.

At 13:30 GMT, US Personal Consumption Expenditures – Price Index (YoY) (Jan) is expected to be 1.6% from 1.7% previously. Core Personal Consumption Expenditures – Price Index (MoM) (Jan) is expected to be 0.3% from 0.2% previously. Personal Consumption Expenditures – Price Index (MoM) (Jan) is expected to come in at 0.0% from 0.1% previously. Personal Income (MoM) (Jan) is expected at 0.3% v 0.4% previously. Personal Spending (Jan) is expected at 0.2% v 0.4% previously. Core Personal Consumption Expenditures – Price Index (YoY) (Jan) is expected to be unchanged at 1.5%. Continuing Jobless Claims (Feb16) is expected to be 1.930M from 1.875M previously. Initial Jobless Claims (Feb 23) is expected to come in at 226K from 222K previously. USD crosses may be heavily traded as a result of this data.

At 13:30 GMT, Canadian Current Account (Q4) is expected to be -17.80B from -19.35B prior. CAD pairs may be moved by this release.

At 14:30 GMT, Canadian Markit Manufacturing PMI (Feb) is expected to be 55.8 from 55.9 prior.

At 14:45 GMT, US Markit Manufacturing PMI (Feb) is expected to be unchanged 55.9.

At 15:00 GMT, US Fed Chairman Powell is again due to testify on the Semi-annual Monetary Policy Report before the House Financial Services Committee, in Washington DC.

At 15:00 GMT, US ISM Prices Paid (Feb) is due out with a consensus of 70.5 expected. The previous reading was 72.7. ISM Manufacturing PMI (Feb) is also out at this time, with an expectation for a number of 58.7 v 59.1 prior. Finally, Construction Spending (MoM) (Jan) is expected at 0.3% from the previous reading of 0.7%. USD crosses could be impacted by the volume of data releases at this time and turbulent price action may result.

At 16:00 GMT, US Fed's Dudley is due to give a speech with his comments having the potential to impact USD and USD assets.

At 21:45 GMT, New Zealand Building Permits s.a. (MoM) (Jan) will be released, with a previous reading of -9.6%. NZD crosses may experience volatility during this time.

At 23.30 GMT, Japanese Job/Applications Ratio (Jan) is expected at 1.60 from 1.59 previously. Unemployment Rate (Jan) is expected at 2.7% from 2.8% previously. Overall Household Spending (YoY) (Jan) is expected at -0.3% from -0.1% prior. National CPI Ex Food, Energy (YoY) (Jan) is expected at 0.9% from 0.3% prior. JPY pairs may be moved by this data release

Technical Outlook: EURUSD – Narrow Consolidation To Precede Final Push Towards Strong Fibo Support At 1.2173

The Euro was marginally higher in early European trading, probing above 1.22 handle after hitting new low at 1.2183 in Asia.

Near-term sentiment remains negative as dollar continues to firm, boosted by optimistic tone from Fed's Powell, which fueled hopes for stronger pace of US rate hikes in 2018.

Wednesday's close below 1.2205 (09 Feb low) was bearish signal for extension and test of next key supports at 1.2173/76 (Fibo 38.2% of 1.1553/1.2555 ascend / rising 55SMA).

Bears are expected to attack these supports, as firm break here would generate next strong bearish signal for fresh acceleration towards 1.2089 (04 Jan former high) and 1.2054 (Fibo 50% of 1.1553/1.2555 rise), with psychological 1.20 support expected to come in focus on stronger weakness.

Very limited upside action was seen so far, with stronger upticks to be capped by falling thick hourly cloud (cloud base lies at 1.2246).

German and EU Manufacturing PMI data are the highlights of the European session today (Feb forecasts show unchanged values from the previous month), with a batch of US data being in focus in American session.

Res: 1.2213, 1.2246, 1.2265, 1.2284

Sup: 1.2183, 1.2173, 1.2156, 1.2089

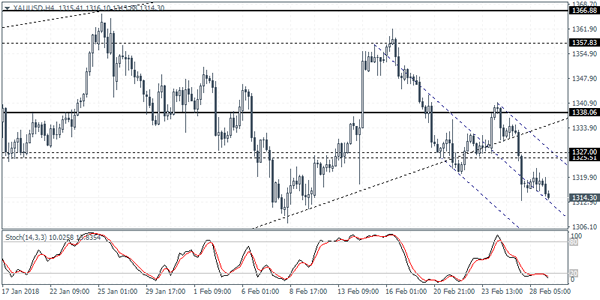

XAUUSD Intraday Analysis

XAUUSD (1314.30): Gold prices closed flat yesterday following the previous day's strong declines. This could potentially signal a turnaround in prices on a bullish close today. To the downside, the initial support at 1303 remains in view as price action could be seen extending the declines to this support. A rebound off this support could offer some short term retracement, but the overall bias remains to the downside. Watch for any rebound that could see gold prices retracing back to the 1327 - 1325 level where there is a possibility for prices to establish resistance

GBPUSD Intraday Analysis

GBPUSD (1.3748): The British pound fell sharply on the day with most of the declines coming from the Brexit negotiations and the comments from the relevant officials. On the 4-hour chart, price action extended the declines following the breakdown of the support level at 1.3902. This potentially puts the downside target in GBPUSD towards 1.2617 - 1.3600 level of support. A retest of support at this level could see GBPUSD establishing a new range, trading sideways within the support and the resistance levels. Any near-term reversals could be seen pushing the currency pair back towards 1.3902 where resistance could be established.

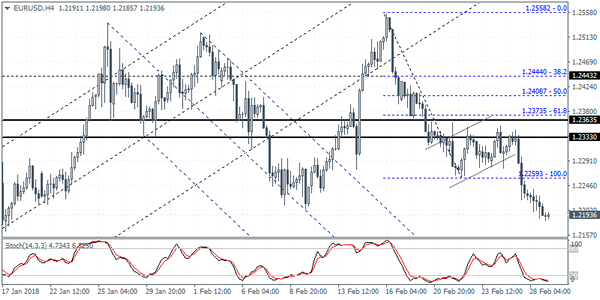

EURUSD Intraday Analysis

EURUSD (1.2193): The EURUSD continues to extend the declines with price closing at a one month low yesterday. The declines following the breakdown below 1.2260 level saw price drifting lower. The downside target remains at 1.2090 which could be tested sometime over the next week and closer to the ECB meeting. In the near term, we expect to see any short term rebound in prices stalling near 1.2260 where resistance could be established. The bias remains to the downside unless we see a reversal above 1.2260. In this case, EURUSD could be seen testing the major resistance level near 1.2230 level.

GBP Edges Lower On Barnier’s Comments

The British pound was seen trading weaker on the day after Brexit comments from the EU's chief negotiator Michel Barnier. Barnier said that the pace of the Brexit negotiations had to pick up after the EU published a draft Brexit withdrawal agreement. This included no hard border between Ireland and Northern Ireland. The British PM Theresa May is expected to give a speech on Friday.

The U.S. dollar was also on the back foot on Wednesday as the revised GDP estimates for the fourth quarter showed that the U.S. economy grew at a pace of 2.5%, compared to the initial estimates of 2.6%. The decline in the GDP came on account of higher imports and reduced investment in private inventory.

Pending home sales report was also weaker after data from NAR showed a 4.7% decline on the month. This was the largest decline in nearly four years.

Looking ahead, the markets look to a new trading month. The economic calendar is busy as investors look to the ISM's manufacturing PMI that stands out today. Forecasts point to a modest decline to 58.7, down from January's 59.1. The UK manufacturing PMI is also expected today but the index is forecast to fall slightly to 55.1 from 55.3 in the previous month.

The Fed Chair, Jerome Powell will be giving his testimony once again to the U.S. Congress later today.