Sample Category Title

GBPUSD Intraday Analysis

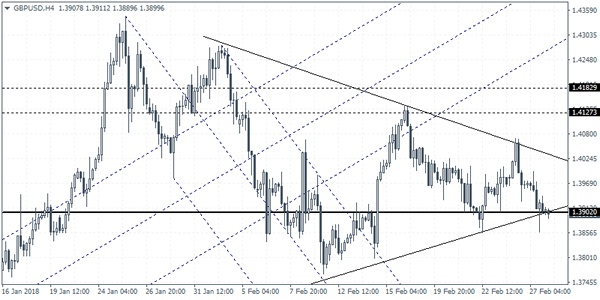

GBPUSD (1.3899): The British pound was seen extending the declines back to the support level near 1.3902. The declines came after the previous retest to the upper trend line of the triangle pattern holding out as resistance. Price action still remains flat and a breakdown below 1.3902 will signal further declines in the near term. We expect GBPUSD to target the next support level at 1.3611 - 1.3590 region. To the upside, any gains are likely to be capped by the trend line. However, in the event that GBPUSD manages to breakout above the trend line, we expect further gains towards 1.4127.

EURUSD Intraday Analysis

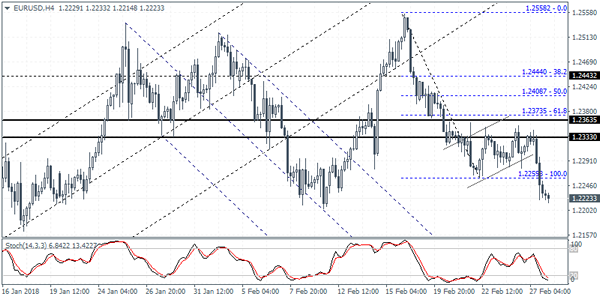

EURUSD (1.2223): The EURUSD was seen closing on a bearish note yesterday as price action closed below 1.2260 level of support. The break down below this level marks the validation of the bearish flag pattern. We expect to see a measured move to the downside, targeting the lower support at 1.2090 region. In the near term, any rebound in prices will see a retest of the breached support at 12260 where resistance could be established. A move above this level will see EURUSD retesting the major resistance level at 1.2330 region.

USD Bumps Higher On Powell’s Testimony

The U.S. dollar was seen strengthening yesterday after the markets remained fairly flat for the most part. Investors were waiting to hear the newly appointed Fed Chairman Jerome Powell, give his testimony to the U.S. Congress.

As expected, Powell gave an upbeat view of the U.S. economy which the markets translated to as a potential signal for a rate hike in March. However, Powell did not make any references to the number of times the Fed could hike rates and did not give any indicators about a potential rate hike in March.

Looking ahead, the economic calendar today will see the flash inflation estimates from the Eurozone for the month of February. Economists polled expect to see a slight decline in the headline CPI which is expected to rise at a slower pace of 1.2%, compared to 1.3% increase registered in January. Core inflation rate is expected to remain steady, rising at a pace of 1.0% for the month of February.

Later in the day, the U.S. second revised GDP estimates will be coming out. Economists expect to see the U.S. GDP rising 2.5% in the fourth quarter of 2017. This marks a slight decline from the 2.6% increase that was registered in the preliminary report. Last but not the least, the pending home sales data is also on the tap later in the day with expectations showing a 0.4% increase which is slightly down from the 0.5% increase registered in the previous month.

Technical Outlook: USDJPY – Scope For Fresh Attack At 108 Zone In Play While Key Supports 107.00/106.90 Hold

The pair eases on Wednesday after fresh strength on Tuesday spiked at 107.67, approaching key barriers at 108 zone (21 Feb recovery top / falling daily Kijun-sen).

Hawkish stance from Fed Chair Powell keeps the greenback at the front foot and showing scope for eventual attack at 108 zone, break of which is needed to generate stronger bullish signal from extension of recovery rally from 105.54 (16 Feb low).

However, caution is required as overall picture is bearish and profit-taking on recent dollar longs could put the greenback under fresh pressure.

Significant supports lay at 107.00/106.90 zone (Fibo 38.2% of 105.54/107.90 / 10SMA) and bullish outlook is expected to remain in play while the latter supports hold.

Otherwise, fresh bearish signal would be generated on firm break lower.

USDJPY's weekly performance is shaped in long legged Doji candle which signals strong indecision, while the pair is on track to complete the second straight month in red, which is seen as negative signal.

Res: 107.52, 107.67, 107.90, 108.00

Sup: 107.00, 106.90, 106.72, 106.44

Technical Outlook: GBPUSD – Fresh Bears Pressure Higher Base At 1.3856, Near-Term Outlook Is Negative

Cable maintains bearish bias on Wednesday, holding in red for the third consecutive day and pressures higher base at 1.3856 (lows of 22/27 Feb).

Fresh strength of the greenback after Powell keeps pound under pressure, with Tuesday’s eventual close below 1.3909 (Fibo 61.8% of 1.3764/1.4144 upleg) after several failures, generating bearish signal.

Support at 1.3856 is reinforced by the top of rising daily cloud (1.3841) and sustained break here will be another strong signal for further weakness towards key short-term support at 1.3764 (09 Feb trough / rising 55SMA).

Daily MA’s (10/20/30) are in full bearish setup and formed multiple bear crosses, while 14-d momentum is entering negative territory and maintaining bearish pressure for triggering stronger negative scenario on break below the lower boundary of 1.3764/1.4144 range.

Meanwhile, corrective upticks will be seen as selling opportunities and are expected to hold below psychological 1.40 barrier, reinforced by daily Tenkan-sen.

Res: 1.3916, 1.3966, 1.4000, 1.4054

Sup: 1.3856, 1.3841, 1.3800, 1.3764

Eurozone Inflation, US GDP The Talk Of The Town Wednesay

Investors won't get any reprieve from the economic calendar on Wednesday, as governments in Europe and the United States unleash a fresh wave of economic data.

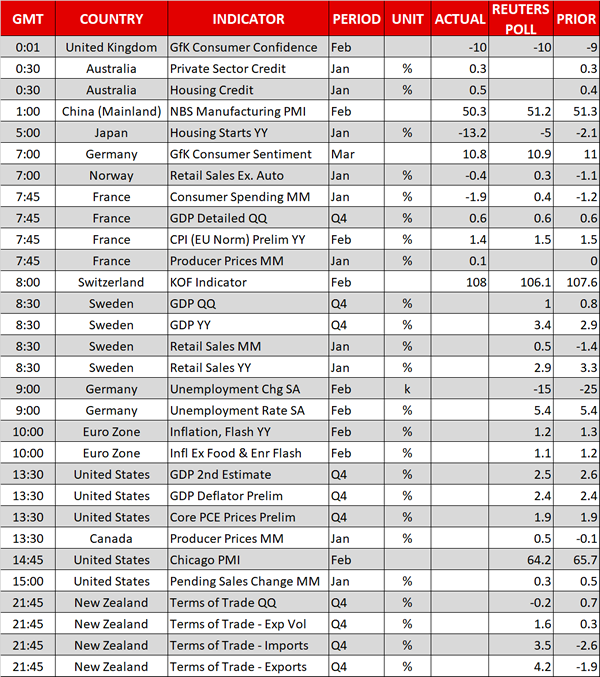

Action begins at 07:00 GMT with a report on German consumer confidence courtesy of the GfK research institute. The monthly reading is expected to dip slightly to 10.9 in March from 11.0 the month before.

Over the next two hours, investors can expect a deluge of economic reports that include French and Portuguese GDP, German unemployment, Italian consumer inflation and Swiss business confidence.

The French economy is expected to grow 0.6% in the fourth quarter. Meanwhile, Germany's employment report is expected to show a jobless rate of 5.4%, unchanged from the previous month.

At 10:00 GMT, the European Commission's statistical agency will report on the consumer price index (CPI) for February. The preliminary reading is expected to show annualized inflation at 1.2% for February, down from 1.3% the month before. So-called core consumer prices, which strip away volatile goods such as food and energy, are expected to rise to 1.1% from 1% in January.

Shifting gears to North America, the US Department of Commerce will unveil its second estimate of fourth quarter GDP at 13:30 GMT. The report is expected to show annualized growth of 2.4% in the final three months of 2017. The report will also contain the latest quarterly reading of the core personal consumption expenditure index, which is the Federal Reserve's preferred measure of inflation.

Later in the session, ISM-Chicago will release the February purchasing managers' index (PMI), which tracks business conditions in the US Midwest. The National Association of Realtors (NAR) will also release the latest pending home sales index for January.

On the monetary policy front, Federal Reserve Chairman Jerome Powell will testify before the House Financial Services Committee at 15:00 GMT.

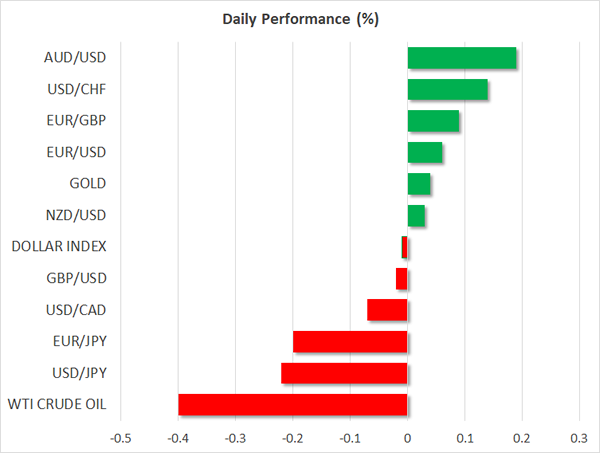

EUR/USD

Europe's common currency nosedived on Tuesday, as the US dollar regained its momentum. The EUR/USD fell from a high of 1.2343 all the way down to 1.2222. It was last seen trading at 1.2217, where it was on track for fresh two-week lows.

GBP/USD

Cable also fell sharply on Tuesday, hitting a session low of 1.3831. After a failed rally attempt, the GBP/USD found itself closing below the 1.3900 threshold. Cable now faces immediate support at 1.3825.

USD/CAD

The USD/CAD was among the better performing crosses on Tuesday, as the pair shot up more than 100 pips to close at 1.2770. The USD/CAD is currently trading at yearly highs and could be poised for further gains now that investors are beginning to speculate about four US interest rate hikes this year. The Federal Reserve is widely expected to raise rates at its forthcoming meeting 20-21 March.

Powell’s Comments Breathe Life Back Into The Dollar, Eurozone Inflation Eyed

Here are the latest developments in global markets:

FOREX: The dollar index – which tracks the greenback's performance against a basket of six major currencies – traded almost unchanged on Wednesday, after posting significant gains earlier on Tuesday as the new Fed Chair Jerome Powell appeared quite optimistic on the US' growth outlook in his testimony before Congress.

STOCKS: US markets posted notable losses yesterday, as the upbeat remarks of the new Fed chief enhanced expectations for higher interest rates. The S&P 500 led the decline, falling by 1.3%, while both the Dow Jones and the Nasdaq Composite tumbled 1.2%. Futures of the S&P, Dow, and Nasdaq 100 were all in the red today, albeit marginally so. The negative sentiment rolled over into Asian trading today as well. In Japan, the Nikkei 225 and the Topix fell 1.4% and 1.2% respectively, while in Hong Kong, the Hang Seng traded 1.6% lower. Futures tracking the major European indices were also a sea of red, signaling that these benchmarks could open lower today.

COMMODITIES: In energy markets, oil prices were lower today, with WTI and Brent crude falling 0.4% and 0.3% accordingly, as the dollar's rebound decreased the appeal of the dollar-denominated precious liquid, while the IEA warned about rising US shale production. In terms of upcoming oil market events, traders will keep their gaze locked on the weekly EIA inventory data, which will be released later today (1530 GMT). In precious metals, gold tumbled yesterday as the US dollar recovered. The yellow metal fell as low as $1313/ounce, before it managed to stabilize and recover somewhat, last trading near the $1317 handle.

Major movers: Dollar regains ground as new Fed Chair appears hawkish

Speaking before the House Finance Services Committee yesterday, Fed Chair Jerome Powell appeared quite hawkish, sending US Treasury yields and the dollar higher, while stocks moved lower. He appeared upbeat on the broader economy, and also hinted at the prospect of faster rate hikes this year than what the Fed penciled in back in December. Asked whether the recent fiscal stimulus could spur more than the projected 3 rate hikes in 2018, he replied that his own personal outlook has indeed strengthened since December. Although indirectly, Powell's confident remarks add credibility to expectations that the FOMC is shifting towards a more optimistic bias.

In the aftermath of these hawkish signals, markets have fully priced in 3 quarter-point rate increases by the Fed in 2018, helping the dollar index to reach a two-and-a-half week high. However, it remains to be seen whether this was the beginning of a sustained recovery in the greenback, or whether the rebound will turn out to be short-lived. The dollar has had a difficult time holding onto gains recently. Not only have markets grown increasingly more concerned about the health of US public finances, but foreign central banks have also moved to tighten their own policies, increasing the appeal of other currencies.

It will be interesting to see if USD bulls can remain in charge. In this environment, technical levels and patterns are worth keeping a very close eye on. The dollar index has almost completed a double bottom formation on the daily chart, and if it manages to break decisively above the 90.50 barrier, that could be a signal for larger upside extensions.

Elsewhere, there was relatively little movement in the FX market. Dollar/yen gave back its Powell-related gains during the Asian session Wednesday, as the declines in stock markets likely led investors to seek the safety of havens like the yen.

In politics, the British pound barely reacted to some downbeat comments by the EU's chief negotiator Michel Barnier yesterday. The official said that there are still significant differences between the two sides on the Brexit transition deal, echoing comments he made earlier in the year.

Day ahead: Eurozone inflation in focus; US updated Q4 GDP figures due; Brexit developments eyed

Krona pairs will be attracting interest as Sweden releases Q4 2014 GDP figures as well as retail sales numbers at 0830 GMT.

Eurozone flash inflation figures for the month of February are scheduled for release at 1000 GMT. Both headline and core CPI – that excludes volatile food and energy items from its calculations – are anticipated to ease on an annual basis. The numbers will constitute the last inflation input ahead of the ECB meeting concluding on March 8 and thus their perceived importance might be amplified by market participants, with a deviation from expectations potentially leading to sharp movements in euro pairs; of course, the extent of any such deviation is also of importance.

Earlier on Wednesday (at 0900 GMT), Germany will see the release of unemployment data for the month of February. The unemployment rate is projected to remain at 5.4%, its lowest since German reunification in 1990. The eurozone's respective rate will be made public on Thursday.

Out of the US, updated – the second reading – Q4 2017 GDP numbers are scheduled for release at 1330 GMT. Analysts project a slight downward revision from the advance estimate of 2.6% on an annualized basis, to 2.5%. Preliminary Q4 GDP deflator (this gauges the level of prices of all new, domestically produced, final goods and services) and core PCE price data will be made public at the same time. February's Chicago PMI (1445 GMT) and pending home sales for the month of January (1500 GMT) will be also be generating some interest.

Canadian producer prices for the month of January are due at 1330 GMT.

New Zealand terms of trade data for Q4 2017 will be made public at 2145 GMT.

Brexit developments to which sterling has proved highly sensitive in the past are again on the forefront. The European Union will be publishing a draft Brexit treaty later on Wednesday. Also in politics, the seventh round of NAFTA negotiations is attracting interest.

In energy markets, the Energy Information Administration's (EIA) report including information on US crude and gasoline inventories for the week ending February 23 is scheduled for release at 1530 GMT. Crude inventories are anticipated to increase by 2.4 million barrels in the period of coverage after unexpectedly falling by around 1.6m barrels during the previously tracked week.

In equities, companies continue to report earnings as some investors are repositioning in response to rising expectations for a higher interest rate environment.

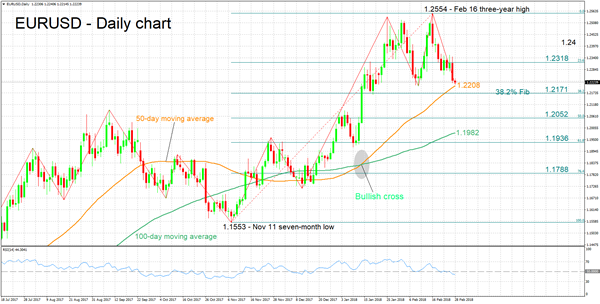

Technical Analysis: EURUSD looking bearish in the short-term

EURUSD has lost ground after reaching a three-year high of 1.2554 roughly two weeks ago. Earlier on Wednesday, it recorded a near three-week low of 1.2215. The RSI continues to fall after crossing below the 50 neutral-perceived level, projecting a negative picture in the short-term.

Stronger-than-anticipated inflation figures out of the eurozone though can definitely change the pair's short-term direction, pushing it higher. Resistance to price advancing might come around the 23.6% Fibonacci level of the November 11 to February 16 upleg at 1.2318.

On the downside and in case of a CPI miss, EURUSD is anticipated to decline. Support could come around the current level of the 50-day moving average at 1.2208. The area around this level also encapsulates the 38.2% Fibonacci mark at 1.2171. Price action is at the moment taking place not far above this area. Should it be violated, the 50% Fibonacci level at 1.2052 would be eyed next.

Lastly, it should be mentioned that US releases later on Wednesday also have the capacity to push the pair in either direction.

GBPUSD Strongly Bearish Below 1.3897 Level

The British pound has continued to move lower against the greenback, as the U.S dollar index strengthened across the board following Fed Chair Jerome Powell’s Congressional Testimony on Tuesday. The GBPUSD currently trades around the 1.3890 level, after earlier finding strong support from the former weekly price-low around the 1.3850 level. Price-action is currently testing the pairs key fifty-day moving average, at 1.3897, as it remains a pivotal technical level for traders.

The GBPUSD pair is strongly bearish whilst trading below the key 1.3897 level, further losses towards the 1.3858 and 1.3765 levels remains likely.

Should GBPUSD price-action move back above the 1.3897 level, buyers may test towards the 1.3938 and 1.4008 resistance levels.

EURUSD Strongly Bearish Below 1.2273 Level

The euro has fallen sharply lower against the U.S dollar, following bullish comments on the U.S economy and future U.S rate hikes from the new Federal Reserve Chairman Jerome Powell. The EURUSD pair has so far found technical support just above the February price-low, located at 1.2203, with price-action now trading around the 1.2220 region. EURUSD traders now look towards the release of the Eurozone February Consumer Price Index, and U.S fourth quarter GDP and CORE PCE data later today.

The EURUSD pair is strongly intraday bearish whilst trading below the 1.2273 level, further losses towards the 1.2203 and 1.2161 levels seems possible.

Should EURUSD price-action move back above the 1.2273 level, buyers may test back towards the 1.2292 and 1.2350 resistance level.

Ethereum Struggles To Pass The $900 Mark

Ethereum has moved up by more than 50% since February, 6 when it reached a multi-month low of $560.

In the past two weeks, however, the price has remained within the $800 and $900 channel, meaning that traders are slightly cautious. The currency often runs out of steam whenever it approaches the psychological $1,000 mark.

Part of the reason for the range trade is that there has been no major news in the cryptocurrencies market. Yesterday, it was reported that a hacker who had stolen 20,000 ethers from the Coindash ICO returned them. This was the second time that hackers had returned back stolen coins.

Technically, the ETH/USD pair is on an ascending trend, with its price slightly above the 50-day and 100-day moving average. The pair is showing a weak trend as shown by the Average Directional Index (ADX). Nonetheless, the pair should continue moving higher unless there is negative news with the next short-term price target being $910.