Sample Category Title

Technical Outlook: EURUSD Holds In Red After Powell, Pressures Key Supports At 1.2205/1.2173

The Euro holds in red in early Wednesday's trading and pressures key support at 1.2205 (09 Feb low), maintaining bearish near-term bias. The pair fell on Tuesday after weaker than expected German inflation numbers and testimony of Fed Chairman Powell, which inflated dollar. After markets digested the comments, the Fed looks more hawkish than initially estimated, which prompted investors into fresh dollar longs, putting the single currency under increased pressure. Bearish acceleration on Wednesday broke below four-day congestion and generated bearish signal. Wednesday's long red daily candle weighs for further weakness and attack at key supports at 1.2205 and 1.2173 (Fibo 38.2% of 1.1553/1.2555 rally, reinforced by rising 55SMA), violation of which would also trigger a number of stops parked below and spark fresh bearish acceleration, which could extend towards psychological 1.20 support (reinforced by rising 100SMA). Bearish setup of daily studies supports the notion, however, the pair may show stronger hesitation at 1.2205/1.2173 support zone, as daily slow stochastic broke into oversold territory. Upticks are expected to provide better selling opportunities and should remain below 1.2330/40 zone where daily MA's formed double bear-cross (10/20 and 10/30). Today's calendar is full, with German jobs data, EU CPI and US Q4 GDP eyed for fresh signal. German labor sector remains stable with unemployment expected to stay unchanged at 5.4% in Feb, but forecasts show significant fall in a number of unemployed people in Feb. Inflation in the Eurozone is expected to tick lower in Feb (1.2% f/ vs 1.3% in Jan).

Res: 1.2241, 1.2260, 1.2285, 1.2340

Sup: 1.2205, 1.2173, 1.2148, 1.2088

AUDUSD Risk Tilted To The Downside, Holds Below 23.6% Fibonacci Mark

AUDUSD retreats over the last couple of sessions and risk is still to a bearish correction as price continues to drift lower from the 0.7990 resistance level. The price posted a pullback on the 20-day simple moving average on Monday and slipped below the 23.6% Fibonacci retracement at 0.7826 level of the upleg from 0.6820 to 0.8135. Price action is at the moment taking place not far below this area.

Momentum indicators are pointing to a negative bias in the short-term with the MACD just below the zero line and the stochastic oscillator deep in bearish territory. However, the stochastic is ready to reach the oversold area and the %K line is attempting a bearish cross with the %D line, suggesting further downside pressure to come.

Further losses should see the 0.7730 – 0.7755 area, which is acting as a major support. If prices fell below the aforementioned zone, it would reinforce the bearish structure in the medium-term and open the way towards the next key support level of 38.2% Fibonacci mark at 0.7635.

In the event of an upside reversal, the 23.6% Fibonacci level could act as a barrier before being able to re-challenge the 40-day SMA near 0.7917 at the time of writing. A break above this level could shift the outlook to a more bullish one as it could take the pair towards the 0.7990 resistance level.

It is worth mentioning that AUDUSD has been holding within an ascending move since January 2016 and tested several times the uptrend line.

Forex Analysis: Bundesbank Are Prepared For The End Of Negative Rates Says Board Member Thiele

German Buba President Weidmann spoke about the Bundesbank’s Annual Report, in Frankfurt, with the following comments made: policy normalisation will take a long time and if the economic upswing continues and prices rise, there is no reason to not end QE this year. He said it is important to “gradually and dependably” reduce ECB stimulus. Rapid Eurozone growth confirms that inflation will move towards the target. There is evidence that FX movements are having a smaller impact on inflation than in the past. Germany’s and the Eurozone’s growth was “very satisfactory”. He also said that bigger QE reduction or a clearer end date would be justifiable. Finally, he said that an ECB rate hike in 2019 is ‘not completely unrealistic’.

Eurozone Industrial Confidence (Feb) was as expected at 8.0, from a prior number of 8.8, which was revised up to 9.0. Economic Sentiment Indicator (Feb) was 114.1 v an expected 114.0, from 114.7 previously, which was revised up to 114.9. Business Climate (Feb) was as expected at 1.48, from 1.54 previously, which was revised up to 1.56. Consumer Confidence (Feb) was as expected at 0.1, from 0.1 prior, which was revised up to 1.4. Services Sentiment (Feb) was 17.5 v an expected 16.3, from 16.7 prior, which was revised up to 16.8. EURUSD traded between 1.23374 and 1.23245 after the release of this data.

German Harmonised Index of Consumer Prices (YoY) (Feb) was 1.2% v an expected 1.3%, from 1.4% previously.

The US Fed’s Powell testified on the Semi-annual Monetary Policy Report before the House Financial Services Committee, in Washington DC, in his new capacity as Chairman. Some of his comments were: He sees further gradual rate hikes and the outlook remains strong. Some headwinds facing the US economy are now tailwinds. Financial conditions are accommodative despite volatility and the Fed must strike a balance to avoid overheating and to lift inflation. The FOMC sees risks roughly balanced and is monitoring inflation. Wages should increase at a faster pace and the US economic outlook is strong, with inflation to rise to 2%. The recent wage increases likely have been dampened by weak productivity growth. Last year’s business investments should begin to lift productivity. A robust jobs market is expected to support income and spending.

US Durable Goods Orders Ex-Transportation was -0.3% v an expected 0.4%, from -0.7% previously, which was revised up from 0.6%. Durable Goods Orders (Dec) was -3.7% v an expected -2.2%, from 2.6% previously, which was revised down from 2.9%. USDCAD traded between 1.27320 and 1.27072 after the release of this data.

US S&P/Case-Shiller Home Price Indices (YoY) (Dec) was as expected at 6.3, from 6.4% previously. House Price Index (MoM) (Dec) was 0.3% v an expected 0.4%, from 0.4% previously, which was revised up to 0.5%.

Japanese Large Retailer’s Sales (Jan) was 0.5% v an expected 0.4%, from 1.1% prior. Retail Trade s.a. (MoM) (Jan) was -1.8% v an expected -0.6%, from 0.9% prior. Retail Trade (YoY) (Jan) was 1.6% v an expected 2.1%, from 3.6% previously. Upon the release of this data, USDJPY moved to a high of 107.521 from 107.418 but then retraced the move within 30 minutes.

UK Gfk Consumer Confidence (Feb) was released earlier this morning, coming out at -10, in line with the consensus, and down from the prior reading of -9.

Chinese Non-manufacturing PMI (Feb) was released at 54.4 against a consensus of 55.0, from 55.3 previously.

EURUSD is up 0.04% overnight, trading around 1.23369.

USDJPY is down -0.27% in early session trading at around 107.035.

GBPUSD is up 0.07% this morning, trading around 1.39139.

Gold is unchanged in early morning trading at around $1,318.82.

WTI is down -0.22% this morning, trading around $62.68.

Major data releases for today:

At 08:00 GMT, Swiss KOF Leading Indicator (Feb) is expected to be 106.1 against 106.9 previously.

At 09:00 GMT, German Unemployment Change (Feb) is expected to be -15K from -25K previously. Unemployment Rate s.a. (Feb) is expected to be unchanged at 5.4%. EUR crosses could be affected by this data.

At 09:00 GMT, Swiss ZEW Survey – Expectations (Feb) data will be released with a previous value of 34.5.

At 10:00 GMT, Eurozone Consumer Price Index – Core (YoY) (Feb) is expected to be 1.1% from 1.0% prior. Consumer Price Index (YoY) (Feb) is expected to be 1.2% against 1.3% previously. EUR pairs may be moved by this release.

At 13:30 GMT, US Gross Domestic Product Annualized (Q4) is expected to be 2.5% from 2.6% previously. Gross Domestic Product Price Index (Q4) is expected to be unchanged at 2.4%. Personal Consumption Expenditures Prices (QoQ) (Q4) is expected to come in at 2.8% from 1.5% previously. Core Personal Consumption Expenditures Prices (QoQ) (Q4) is expected to be 1.9% from 1.3% previously. USD crosses may be heavily traded as a result of this data.

At 14:45 GMT, US Chicago Purchasing Managers’ Index (Feb) is expected to be 64.2 against a prior read of 65.7.

At 15:00 GMT, Pending Home Sales (YoY) (Jan) is expected to be -0.2% against a prior reading of -1.8%. Pending Home Sales (MoM) (Dec) is expected to be 0.3% against a prior reading of 0.5%.

At 15:00 GMT, US Fed’s Powell is due to testify on the Semi-annual Monetary Policy Report before the House Financial Services Committee, in Washington DC, in his new capacity as Chairman.

At 13:30 GMT, US Durable Goods Orders Ex-Transportation is expected to come in at 0.4% from -0.7% previously, which was revised up from 0.6%. Durable Goods Orders (Dec) is expected at -2.2% v 2.8% previously, which was revised down from 2.9%. USD crosses may be heavily traded as a result of this data.

At 22:30 GMT, Australian AIG Manufacturing Index is expected to be released with a previous value of 58.7. AUD crosses may be heavily traded as a result of this data.

At 23:50 GMT, Foreign Investment in Japanese Stocks (Feb 23) is expected to be in the region of the previous number of ¥-127.1B. Foreign Bond Investment (Feb 23) was ¥-553.1B previously. The report is released by the Ministry of Finance, detailing the flows from the public sector excluding the Bank of Japan. The net data shows the difference of capital inflow and outflow. A positive difference indicates net sales of foreign securities by residents (capital inflow), and a negative difference indicates net purchases of foreign securities by residents (capital outflow).

USDCHF – Targets Further Upside Pressure On Correction

USDCHF - With the pair retaining its upside pressure, more strength is likely in the days ahead. On the downside, support lies at the 0.9350 level. A turn below here will open the door for more weakness towards the 0.9300 level and then the 0.9250 level. On the upside, resistance resides at the 0.9400 level where a break will clear the way for more strength to occur towards the 0.9450 level. Further out, resistance comes in at the 0.9500 level. Above here if seen will turn attention to 0.9550. Its daily RSI is bullish and pointing higher suggesting more strength. All in all, USDCHF faces further upside pressure.

Daily Wave Analysis: US Dollar Bullish Momentum Faces Final Resistance Zone

Currency pair EUR/USD

The EUR/USD broke below the support trend line (dotted blue) and is now testing the previous bottom (green). The support zone is a key decision level for a bullish bounce or bearish breakout and will decide whether USD strength or weakness will prevail.A bearish break makes a wave 4 (purple) pattern less likely.

The EUR/USD needs to break above the resistance trend lines (orange) beforea bullish breakout is likely. A bearish breakout would need to show strong bearish price action before continuation lower is possible.

Currency pair GBP/USD

The GBP/USD is in a triangle chart pattern with multiple support and resistance trend lines near it. Price will need to break the S&R to start a new trend.

The GBP/USD indeed completed a bearish ABC (orange) zigzag yesterday, which is probably part of a larger WXY correction (grey).Price could show bullish reversal if price manages to break above resistance (orange). A break below the 100% Fib shows bearishness.

Currency pair USD/JPY

The USD/JPY is probably in a wave 4 (blue) as long as price stays below resistance (red).

The USD/JPY could be building an ABC (green) correction within wave 4.

Dollar Finds A Friend In Powell As Global Stocks Slip

Dollar bulls were injected with a renewed sense of confidence on Tuesday after Federal Reserve Chairman Jerome Powell struck a careful but fairly upbeat tone during his congressional testimony.

Powell expressed optimism over the health of the US economy withinflation pushing towards the 2% target, while downplaying concerns of market volatility. He deftly maintained a safe distance when quizzed on whether the central bank would raise rates more than three times this year – ultimately preventing market fireworks. A key takeaway from the testimony was Powell’s statement that the US economic outlook “remains strong despite the recent stock market turbulence”. These hawkish remarks have not only reinforced market expectations over a rate hike in March, but stimulated speculation that the Fedmay raise interest rates four times this year.

Today’s main risk event for the Dollar will be the second estimate of the fourth quarter US GDP, which is expected to show that the US economy expanded 2.5%. A growth figure matching or exceeding market expectations could support the prospects of higher rates, consequently boosting the Dollar further.

Focusing on the technical picture, the Dollar bounced back to life against a basket of major currencies on Tuesday, with prices venturing towards the 90.40 region. A decisive breakout and daily close above the 90.55 lower high could signal the end of the downtrend on the daily charts, ultimately bringing bulls back into the game. The level of interest above 90.55 will be the 91.00 resistance level.

Equity bears inspired by Powell

Asian equities were depressed during early trading on Wednesday following Wall Street’s steep decline overnight.

Hawkish comments from Jerome Powell have rekindled interest rate hike fears and as such continues to pressure stock markets. European shares could edge lower as investors adopt a guarded approach with the caution potentially trickling back down into Wall Street later in the day. It is becoming increasingly clear that global stocks still remain highly sensitive to the prospects of rising inflation and interest rate fears. With Powell’s testimony fuelling market speculation of higher US interest rates this year, stock markets remain exposed to downside risks as equity bears lurk in the background.

Gold melts on Fed hike expectations

Gold found itself under severe selling pressure on Wednesday thanks to an aggressively appreciating US Dollar.

The yellow metal’s downside was fuelled by hawkish remarks from Federal Reserve Chairman Jerome Powell, which heightened speculations of higher US interest rates this year. Gold, which is zero-yielding, is likely to receive further punishment in a high interest rate environment. From a technical standpoint, Gold is bearish on the daily charts. Prices are trading below the 50 Simple Moving Average while the MACD has crossed to the downside. Previous support at $1324.15 could transform into a dynamic resistance that encourages a decline to $1310 and $1300, respectively. For bulls to jump back into the game, Gold prices need to break back above $1324.15.

Stock Markets Sold Off, Bond Yields Rose

Market movers today

Today, we publish the third paper in our series on inflat ion and what it means for markets. In t oday's piece we dive int o t he inflat ion development in t he Scandinavian count ries.

Today's main event is t he release of euro area HICP inflation at 11:00 CET . With Spanish HICP surprising slightly on the upside this morning and German HICP slight y lower than expected, we see risks for the euro area print tomorrow as balanced and stick to our forecast of 1.24% for headline and 1.05% for core.

Tier 2 releases today include German unemployment rate and the second release of US GDP growth for Q4.

More interesting is the EU's Chief Brexit negotiat or Michel Barnier, who is due to brief the permanent EU representatives on Brexit today. They are expected to adopt the withdrawal text , which will be published.

We have a lot on the plate in the Scandies today. In Norway, retail sales in January and the quarterly wage statistics for Q4 are due out today. In Sweden, we have Q4 GDP, retail sales and Sweden's National Housing Board is due to publish a report on the Swedish housing market . In Denmark, the second release of GDP will give more detail on what drove growth in Q4.

Selected market news

Stock markets sold off, bond yields rose and the USD strengthened on the back of the new Fed Chairman Jerome Powell's first testimony. Powell gave a positive view on the economy and said his personal out look for the US had strengthened since the December meeting. It opens up for the Fed eyeing four hikes instead of three in 2018. See Flash Comment US: Powell says 'personal outlook has strengthened', 27 February 2018.

Chinese official PMI manufacturing for February fell more strongly than expected, pointing to a slowdown in the Chinese economy, see chart. The index fell to 50.3 (consensus 51.1) from 51.3. It is the lowest level since July 2016. While the drop is bigger than expected it is broadly in line with our out look for a slowdown in the Chinese economy this year, which is engineered by financial tightening to reduce leverage and cool the housing market . The months around the Chinese New Year always create some distortion so the weakness of the data should be taken with a grain of salt . Tomorrow, private Caixin PMI data is due out .

In Japan, preliminary industrial production for January also disappointed. The numbers showed a decline of 6.6% m/m (consensus -4.0% m/m) after a rise in December of 2.9% m/m. It was the biggest monthly drop since 2011. Japanese retail trade also fell more than expected.

While the data out of Asia probably exaggerates the weakness, it is more evidence that the global business cycle reached a peak in early 2018 and is set to lose a bit of steam during the year after finishing 2017 on a very strong note. We still expect global growth to be robust , though and underpin decent profit growth.

Market Update – Asian Session: US And China Exchange Barbs On Trade

Headlines/Economic Data

General Trend:

Asian equity markets and financials generally track declines in the US

Real Estate stocks decline after rise in US Treasury yields

Hong Kong Exchanges [388.HK] FY17 results beat ests

Asian currencies trade generally weaker after Tuesday’s gains in the US dollar

China says Feb PMIs weighed down by Lunar New Year Holiday: Manufacturing PMI hits lowest since July 2016 and has biggest m/m drop in 6-years

Japan Jan prelim industrial production has largest m/m decline since 2011

BoJ trims purchases of over 25-year JGBs in daily operation

Hong Kong issues initial 2018 GDP growth and inflation forecasts

Q4 Capex data due out of Japan and Australia on Thursday

Japan

Nikkei 225 opened -0.4%; closed -1.4%

TOPIX Iron & Steel Index -2.3%, Real Estate -1.5%, Securities -1%

Japanese mega banks trade broadly lower, track earlier declines in US financial sector

Fast Retailing [9983.JP] Declines over 1% (scheduled to report Feb sales on Friday, March 2nd)

(JP) JAPAN JAN PRELIM INDUSTRIAL PRODUCTION M/M: -6.6% V -4.0%E; Y/Y: 2.7% V 5.3%E

(JP) JAPAN JAN RETAIL SALES M/M: -1.8% V -0.6%E;RETAIL TRADE Y/Y: 1.6% V 2.5%E

(JP) Japan Jan Housing Starts Y/Y: -13.2% v -4.7%e; Construction Orders Y/Y: +0.9% v -8.1% prior

(JP) BOJ announcement related to daily bond buying operation: Reduces buying in over 25-year JGBs

(JP) Japan FY18 general budget bill is expected to pass the lower house as early as today, which would secure legislation by the end of the current fiscal year ending March

(JP) Bank of Japan (BOJ) Gov Kuroda: Reiterates BOJ easing is to reach price target

Looking Ahead: Japan Q4 Capex data due for release on Thursday

(JP) BoJ Gov Kuroda said to give speech in the lower house on Friday March 2nd, which is expected to focus on his reappointment –Japanese Press

Korea

Kospi opened -0.4%

(KR) South Korea Mar Business Manufacturing Survey: 82 v 77 prior; Non-Manufacturing Survey: 82 v 78 prior

(KR) According to analysts Bank of Korea (BOK) is expected to raise rates in May or July - Korean press

China/Hong Kong

Hang Seng opened -0.7%, Shanghai Composite -0.9%

Hang Seng Energy Index -2.9%, Information Tech -2.5%, Financials-1.7%, Services -1.5%, Property/Construction -1.6%

Shanghai Composite Property index moves between gains and losses

(CN) US President Trump:China and others take advantage of US in trade - China Daily

(CN) China Commerce Ministry (MOFCOM): China will take necessary measures to protect legal (trade) rights

(CN) China planning to reduce itsannual budget-deficit target to 2.9% of GDP, compared to the 3% set in the pasttwo years - financial press

(CN) CHINA FEB GOVT OFFICIAL MANUFACTURING PMI:50.3 V 51.1E (lowest level since July 2016); NON-MANUFACTURING PMI: 54.4 V 55.0E (4-month low),Composite PMI: 52.9 v 54.6 prior

(CN) China PBoC Open Market Operation (OMO): Skips v skips prior injection of reverse repo operations (2nd consecutive skip)

USD/CNY (CN) PBOC SETS YUAN REFERENCE RATE AT 6.3294 V 6.3146 PRIOR

(CN) China said to cut gasoline and diesel prices for March

(HK) Hong Kong Q4 GDP q/q: 0.8% v 0.7%e; 2017 GDP Y/Y: 3.8% v 3.7%e

(HK) Hong Kong Financial Sec Chan: Gives initial 2018 outlook: GDP 3-4%; CPI 2.2%, underlying CPI 2.5% - budget address

(CN) China Finance Ministry (MOF) sells 5-year bonds: avg yield 3.6566% v 3.69%e; bid to cover 3.13x

China electric vehicle (EV) firm Nio said to hire bankers for planned 2018 IPO in the US, to raise up to $2.0B - financial press

Looking ahead: China Feb Caixin Manufacturing PMI due for release on Thursday

Australia/New Zealand

ASX 200 opened -0.2%; closed -0.7%

ASX 200 REIT Index -1.5%, Telecom -2.6%, Consumer Discretionary -1%, Resources -1.1%, Financials -0.6%

Retailer Harvey Norman [HVN.AU] declines over 12% as H1 profits declined and revenues missed ests

Virgin Australia, VAH.AU Reports H1 (A$) underlyingpretax 102.5M v 107Me; Rev 2.79B v 2.8Be; Confirms that there is no intentionto privatize the company, announces share buyback priced at A$0.30/share

(AU) Australia Treasury Sec Fraser: Wage growth is starting to lift, a sharpcorrection in housing is not likely

(NZ) RBNZ Deputy Gov Bascand: RBNZ initiatives will strengthen disclosureregime; insurance sector can improve disclosure performance (update)

(AU) Australia sells A$1.0B v A$1.0B indicated in 2.25% Nov 21, 2022 bonds, avgyield 2.3582% v 2.2218% prior, bid to cover 4.10x v 3.53x prior

(AU) Australia Jan Private Sector Credit M/M:+0.3% v 0.4%e; Private Sector Credit Y/Y: 4.9% v 5.0%e

Pilbara Minerals, PLS.AU Enters into broad-based strategic relationship POSCO; includes long-term offtake and A$79.6M equity investment in Pilbara at A$0.97/shr

(AU) NAB now sees RBA raising rates one time by 25bps in Q4 2018 (prior view of 2 rate hikes)

Looking Ahead: New Zealand Q4 Terms of Trade due for release on Thursday, along with Australia Q4 Capex

Other Asia

(TH) Bank of Thailand Feb Policy Meeting Minutes: Reiterates policy should remain accommodative; Volatile movements are expected for Baht currency (THB)

(ID) Indonesia Central Bank (BI): Have been intervening in the market since this morning; Rupiah has weakened on Fed Powell's hawkish comments

(IN) India Feb PMI Manufacturing: 52.1 v 52.4 prior (7th month of expansion)

State Bank of India [SBIN.IN]: Raises interest rates on term deposits below INR10M by 10-50bps; for bulk deposits+25-75bps

Looking ahead: India Q4 GDP due later today

North America

US equity markets ended broadly lower: Dow -1.2%, S&P500 -1.3%, Nasdaq -1.2%, Russell 2000 -1.5%

S&P500 Real Estate -2.1%, Consumer Discretionary -2.1%

(US) Fed Chair Powell: Developments since the Dec meeting have increased his confidence that inflation is moving towards target; Further gradual increases in the federal funds rate will best promote attainment of both of our objectives;policy will remain data dependent

(CA) Canada Fin Min Morneau: Have budget room for all eventualities, interest rates in Canada are still accommodative

(US) OPEC reportedly schedules meeting with US shale producers in Houston next Monday – press

(US) Weekly API Oil Inventories: Crude: +0.9M v-0.9M prior

Looking Ahead: US Q4 GDP revision due for release , along with Q4 Consumer Spending and Feb Chicago PMI, Weekly DoE Crude Oil Inventories

Europe

(UK) Feb Lloyds BusinessBarometer: 33 v 35 prior

(UK) Feb BRC Shop Price Index Y/Y: -0.8% v -0.6%e

Looking Ahead: Euro Zone Prelim Feb CPI due for release

Levels as of 01:00ET

Nikkei225 -1.4%, Hang Seng -1.4%; Shanghai Composite -0.7%; ASX200 -0.7%, Kospi -1.1%

Equity Futures: S&P500 -0.1%; Nasdaq100 -0.1%,Dax -0.1%; FTSE100 -0.2%

EUR 1.2215-1.2239; JPY107.53-107.07; AUD 0.7799-0.7781;NZD 0.7242-0.7220

Apr Gold 0.0% at $1,318/oz; Apr Crude Oil -0.6% at $62.66/brl; May Copper -0.3% at $3.17/lb

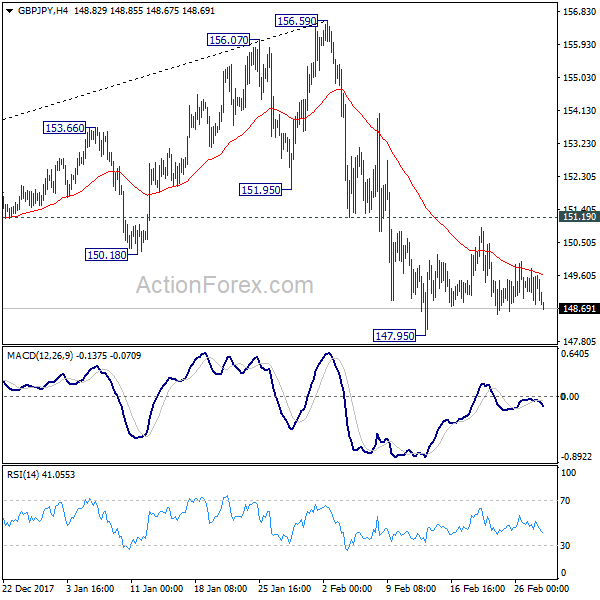

GBP/JPY Daily Outlook

Daily Pivots: (S1) 148.80; (P) 149.30; (R1) 149.78; More...

GBP/JPY weakens mildly today but it's staying in range above 147.95. Intraday bias remains neutral as consolidation could extend. But with 151.90 resistance intact, deeper decline is expected. Below 147.95 will resume the fall from 156.59 and target 146.96 support next. Considering bearish divergence condition in daily MACD, firm break of 146.96 will be another sign of medium term trend reversal. On the upside, break of 151.19 will indicate short term bottoming and turn bias back to the upside for rebound.

In the bigger picture, the case for medium term reversal continues to build up on loss of medium term momentum as seen in weekly MACD. Also, firm break of 146.96 will indicate rejection by 55 month EMA (now at 154.60) and add to that case of reversal. In that case, deeper fall would be seen to 38.2% retracement of 122.36 to 156.59 at 143.51 and then 61.8% retracement at 135.43. Meanwhile, break of 156.59 will extend the rise from 122.36 to 61.8% retracement of 195.86 to 122.36 at 167.78.

Aussie Trading A Tad Lower In The Asian Session

For the 24 hours to 23:00 GMT, the AUD declined 0.73% against the USD and closed at 0.7793.

LME Copper prices declined 1.2% or $83.0/MT to $7028.0/MT. Aluminium prices declined 0.7% or $16.0/MT to $2172.5/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7792, with the AUD trading marginally lower against the USD from yesterday’s close.

Data released overnight indicated that Australia’s private sector credit climbed less-than-anticipated 0.3% on a monthly basis in January, compared to market expectations for a gain of 0.4%. The private sector credit had registered a similar rise in the previous month.

Elsewhere in China, Australia’s largest trading partner, the NBS manufacturing PMI declined to a 19-month low level of 50.3 in February, more than market expectations of a fall to a level of 51.1. In the previous month, the NBS manufacturing PMI had recorded a reading of 51.3. Moreover, the nation’s NBS non-manufacturing PMI fell more-than-expected to a level of 54.4 in February, hitting its lowest level since October 2017. The PMI had registered a reading of 55.3 in the prior month, while markets were anticipating it to ease to a level of 55.0.

The pair is expected to find support at 0.7764, and a fall through could take it to the next support level of 0.7735. The pair is expected to find its first resistance at 0.7838, and a rise through could take it to the next resistance level of 0.7883.

Moving ahead, Australia’s AiG performance of manufacturing index for February, slated to release overnight, will garner a lot of market attention.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.