Sample Category Title

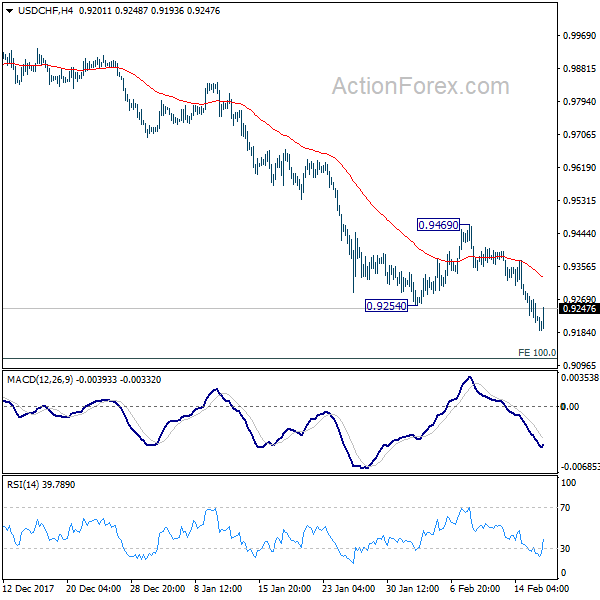

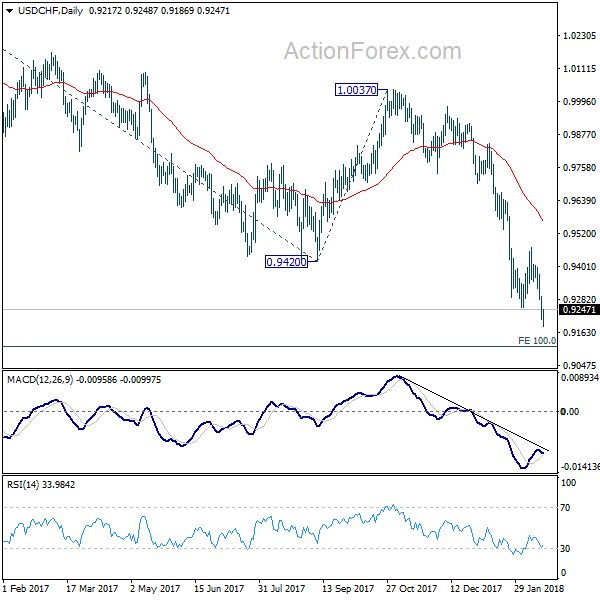

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9188; (P) 0.9240; (R1) 0.9271; More...

USD/CHF recovers mildly in early US session. But intraday bias stays on the downside. Current down trend should target 0.9115 medium term projection level next. On the upside, break of 0.9469 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, fall from 1.0342 is developing into a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 105.78; (P) 106.39; (R1) 106.74; More...

USD/JPY recovers mildly after dipping to 105.54. Still intraday bias remains on the downside for deeper fall. Current fall is part of the pattern from 118.65 and should target 118.65 to 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. On the upside, break of 107.89 minor resistance is needed to be the first sign of short term bottoming. Otherwise, outlook will stay bearish.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48. now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

Dollar Recovers on Profit Taking, Stays the Weakest for the Week

After initial selloff, dollar regains some growth in early US session. Nonetheless, that's more about pre-weekend profit taking. The greenback is still trading as the weakest one for the week, followed by the Loonie. Yen continues to trade as the strongest one and is picking up some momentum against Europeans. Released from US, housing starts rose to 1.33m annualized rate in January, building permits rose to 1.40m. Import price index rose 1.0% mom in January. Canada manufacturing sales dropped -0.3% mom in December. International securities transactions dropped CAD -1.97b in December. Released earlier, UK retail sales dropped -0.3% mom in December.

ECB Coeure: Market volatility contained to stocks only

ECB Governing Council member Benoit Coeure commented on recent market volatility. It said "so far what we see is that the adjustment has been orderly in markets and the spillover to the euro zone, the impact on the euro zone, has been largely contained to the equity market." Regarding forward guidance, Coeure reiterated the stance that our communication on monetary policy will change and we said it will be discussed in early 2018." He added "so far we have not discussed it." Meanwhile, the central bank will not raise interest rate before ending the asset purchase program.

Kuroda nomination finally confirmed

In Japan, it's finally confirmed that Haruhiko Kuroda is nominated by the government to server a rare second term as BoJ Governor. BoJ executive director Masayoshi Amamiya and Waseda University professor Masazumi Wakatabe are nominated as the to deputies. Hiroshi Nakaso and Kikuo Iwata will be replaced as deputies when their terms expire in mid-March. With the ruling coalition holding a majority, the nominations will be easily approved by both houses.

RBA Lowe: No strong case for near term hike

RBA Governor Philip Lowe told the parliament today that the timing of any change in interest rate will "depend upon the extent and pace of progress that we make in reducing the unemployment rate and having inflation return to target." And, "as things currently stand, we expect that progress to be steady, but to be only gradual." Therefore, "the reserve bank board does not see a strong case for a near-term adjustment of monetary policy."

NZ manufacturing expands at faster pace

Business NZ manufacturing PMI rose to 55.6 in January, up from 51.2, indicating faster expansion. BNZ Senior Economist Craig Ebert noted that "while the NZ PMI has led the world for the last five years, the global PMI has now pretty much caught up. This suggests the international investment cycle is clicking into place and promises to self-sustain the global economic expansion. This should be good for manufacturing industries, New Zealand included."

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 105.78; (P) 106.39; (R1) 106.74; More...

USD/JPY recovers mildly after dipping to 105.54. Still intraday bias remains on the downside for deeper fall. Current fall is part of the pattern from 118.65 and should target 118.65 to 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. On the upside, break of 107.89 minor resistance is needed to be the first sign of short term bottoming. Otherwise, outlook will stay bearish.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48. now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ Manufacturing PMI Jan | 55.6 | 51.2 | ||

| 09:30 | GBP | Retail Sales M/M Jan | 0.10% | 0.60% | -1.50% | -1.40% |

| 13:30 | CAD | Manufacturing Sales M/M Dec | -0.30% | 0.30% | 3.40% | |

| 13:30 | CAD | International Securities Transactions (CAD) Dec | -1.97B | 19.18B | 19.56B | 19.2B |

| 13:30 | USD | Import Price Index M/M Jan | 1.00% | 0.60% | 0.10% | 0.20% |

| 13:30 | USD | Housing Starts Jan | 1.33M | 1.23M | 1.19M | 1.21M |

| 13:30 | USD | Building Permits Jan | 1.40M | 1.31M | 1.30M | |

| 15:00 | USD | U. of Mich. Sentiment Feb P | 95.5 | 95.7 |

Dollar Trapped in Negative Sentiment; European Stocks Set for Weekly Gains

Here are the latest developments in global markets:

FOREX: Despite rising US Treasury yields, the dollar was under pressure against its major peers, with traders attributing the phenomenon to concerns surrounding a potential ballooning US debt and the expectations that other central banks could start raising rates amid higher inflation prospects. Dollar/yen tumbled to a fresh one-year low of 105.54 during the Asian session before it inched up to 106.17 (-0.04%) in early European trading. The dollar index was struggling to deviate above three-year lows, moving slightly up to 88.70 (+0.12%) after reaching a low of 88.25. Pound/dollar failed to gain ground on the back of the dollar's weakness, breaking below 1.41 towards 1.4070 as readings on the UK's retail sales disappointed analysts, while the EU Brexit negotiator reiterated today in a speech at the Munich Security Conference that Britain's stance on trade and regulation was putting EU-UK trade relations at risk. Euro/dollar weakened to 1.2483 (-0.18%), while euro/pound was flat at 0.8874. Aussie/dollar and kiwi/dollar were set to achieve weekly gains for the first time in two weeks, last seen at 0.7955 (+0.16%) and 0.7410 (+0.07%).

STOCKS: European stocks headed for a positive weekly close following sharp declines the past two week as worries on inflation somewhat eased, while earnings releases continued to provide support to equity markets. The pan-European STOXX 600 was up by 0.91% at 1030 GMT, underpinned by positive earnings outcomes delivered by large multinationals including ENI, Renault, and Schneider. The blue-chip Euro STOXX 50 was trading 0.93% higher, driven by utilities and consumer cyclicals. The Italian FTSE MIB and the Spanish IBEX 35 jumped by 1.0%, the French CAC 40 and the German DAX 30 rose by 0.73%. The UK FTSE 100 increased by 0.71%, while the US stock futures were in the green, pointing to a positive open.

COMMODITIES: Oil prices were rising for the third day in a row, lifted by a falling dollar and a recovering stock market. However, concerns around rising US oil production were looming in the background, restricting steeper increases. WTI crude and Brent were fluctuating near one-week highs, last seen at $61.60 (+0.35%) and $64.62 (+0.45%) respectively. In precious metals, gold stretched up towards a fresh 3-week high of $1361.61/ounce (+0.38%).

Day ahead: US housing data and University of Michigan consumer sentiment pending

The US will finish the week publishing further details on the economy and potentially ahead of a relatively quiet week in terms of US data releases.

At 1330 GMT, investors will keep a close eye on the US housing stats, with analysts predicting that the number of building permits might have remained unchanged at 1.300 million in January, while they see housing starts rebounding by 3.6% m/m in the aforementioned period to reach an annualized number of 1.234 million due to a milder cold weather in January. January's import prices will be also published along with the above data, giving additional evidence on inflationary pressures. Expectations are for the import price index to rise by 0.5 percentage points to 0.6% on a monthly basis.

At 1500 GMT, the University of Michigan will deliver initial estimates on the US consumer sentiment, forecasting that the index might inch down to 95.5 in February compared to 95.7 in the previous month.

Later in the day, Baker Hughes will report on the US oil rig counts for the week ending February 9. Note that the measure was showing increasing production the past three weeks, giving some boost to oil prices.

Meanwhile in Canada, growth in manufacturing sales is anticipated to slow down significantly to 0.2% in December after surging by 3.4% m/m in November, posting the largest expansion seen since March 2011.

In politics, US Secretary of State Rex Tillerson will be meeting Turkish Foreign Minister Mevlüt Çavuşoğlu. The meeting could be interesting given the rising tensions between the two countries. Also of interest - amid Brexit negotiations - might be a meeting between UK PM Theresa May and German Chancellor Angela Merkel in Berlin.

Turning to stock markets, earnings releases will continue to attract attention, with Coca-Cola Co and Kraft Heinz Company being among companies to reveal quarterly reports. Both multinationals are expected to report higher profits for the fourth quarter.

USDJPY: Vulnerable But With Caution Of Correction

USDJPY - The pair may still be hold on to its broader downside pressure but faces risk of a correction higher. On the downside, support lies at the 105.50 level where a break if seen will aim at the 105.00 level. A cut through here will turn focus to the 104.50 level and possibly lower towards the 104.00 level. Its daily RSI is bearish and pointing lower suggesting further weakness. On the upside, resistance resides at the 106.50 level. Further out, we envisage a possible move towards the 107.00 level. Further out, resistance resides at the 107.50 level with a turn above here aiming at the 108.00 level. On the whole, USDJPY faces further downside pressure.

Dollar Collapse Likely to Remain in Place

It has been a painful week of trading for the Dollar. The Greenback has essentially reversed its recovery from the previous two trading weeks, to return back towards levels not seen since December 2014.

This means that the Dollar has not been valued this low since traders began to price in the normalization of US interest rate policy from the Federal Reserve that began in 2015. It might sound strange on headline, considering that expectations are high for the Federal Reserve to raise US interest rates multiple times this year, but US interest rate policy is no longer a "pull" for investors to purchase the USD.

Investors are instead focusing on the development of economies that are within the remit of other central banks. The news earlier this week that EU economic growth has printed its best performance since the 2007 global financial crisis began to unfold, has reiterated the ever-increasing optimism over the global economy. The distance in economic recovery between the United States and developed economies has been narrowing for some time, but it has now come to the attention of traders that it is only a matter of time before other major central banks prepare the financial markets for their own adjustments to increased interest rates.

This eventuality poses a significant risk of weakening investor attraction towards the Dollar. It will also play a pivotal role towards the USD being at risk to hitting further multi-year lows over the months to come, and it is still possible that the Dollar Index will extend its decline to 85 over the current quarter. This would further extend the advancements in major currencies that have already strengthened by approximately 4% year-to-date. Such a move would risk the Euro trading around 1.27/1.28 for the first time since approximately October 2014 and would further accelerate the strength in the Japanese Yen that has already climbed above 6% this year.

The other currencies that would be likely to benefit heavily from a further round of selling in the USD are those in the emerging markets. Higher-yielding currencies like the South African Rand is already 6.5% higher in 2018. However, the impact this is having in emerging market currencies across Asia shouldn't be discounted away either. Both the Thai Baht and Malaysian Ringgit have strengthened by around 4% year-to-date, but it is the Chinese Yuan that I am keeping a firm eye on.

There is going to be an argument from some that the People's Bank of China (PBoC) might intervene in the market to prevent Yuan strength, although the Chinese Renminbi and offshore Yuan are currently only showing gains in 2018 of 2.6 and 3.5%, respectively. This means that the Yuan is actually lagging behind many of its counterparts, and I personally still see the potential for the USD/CNY to decline towards 6 in 2018.

This means that there is at least another 2-3% that the Yuan can potentially gain this year, beyond what it has already advanced.

Spot Gold – Bulls are Looking for Final Push through Key $1366 Barrier

Spot Gold is holding just under new three-week high at $1361, maintaining strong bullish sentiment and focusing key near-term barrier at $1366 (25 Jan peak, the highest since early Aug 2016). The yellow metal is strongly supported by weak dollar which came under increased pressure on mounting concerns about deficit US budget and current account. Projections for current account deficit are for nearly $1 trillion in 2019 which could have further strong negative impact on the greenback. Gold could extend its broader uptrend towards targets at $1375 (early July 2016 peak) and $1391 (mid-March 2014 high) on firm break above $1366 pivot. The metal is on track for strong bullish weekly close (the biggest one-week gains since Feb 2016), which would provide further boost to existing bullish structure. However, bulls may show hesitation and enter consolidation phase ahead of $1366 pivot as slow stochastic turned sideways in deeply overbought territory and could produce bearish signal on reversal. Former lower top at $1351 (also Fri session low) marks initial support, with deeper dips expected to find support at $1343 (broken Fibo 61.8% of $1366/$1307 pullback).

Res: 1361; 1366; 1375; 1380

Sup: 1351; 1346; 1343; 1336

Canadian Dollar Trading Sideways, US Housing Reports Next

The Canadian dollar is showing little movement in the Friday session, continuing the trend we saw on Thursday. Currently, USD/CAD is trading at 1.2493, up 0.10% on the day. On the release front, Canada releases Manufacturing Production, which is expected to slow to 0.2% in December, after a strong 3.4% gain in November. In the US, Building Permits is expected to inch lower to 1.30 million, and Housing Starts are projected to improve to 1.23 million. As well, UoM Consumer Sentiment is expected to rise to 95.4 points.

The US dollar has been under pressure from rival currencies throughout the week, and the Canadian dollar has jumped on the bandwagon. On Wednesday, the Canadian currency posted its best one-day performance in 2018, gaining close to 1 percent against the greenback. The US dollar sagged as investors focused on poor retail sales reports in January. Retail Sales was flat at 0.0%, short of the estimate of 0.5%. Core Retail Sales declined 0.3%, well off the forecast of +0.2%. Last week's market sell-off, which sent the US dollar higher against other currencies, was triggered by fears of higher inflation. The US has posted strong inflation numbers this week, and this has raised concerns that investors could again lose their risk appetite and send the Canadian dollar lower.

The recent volatility in the stock markets could affect US interest rate policy. Currently, the Fed has projected three hikes this year, but that could change to four or even five hikes, if inflation continues to head upwards and the robust US economy maintains its strong expansion. The new head of the Federal Reserve, Jerome Powell, received a rude welcome from the stock markets, when he started his new position last week. Powell sought to send a reassuring message earlier this week, declaring that the Fed is on alert to any risks to financial stability. However, it is clear that the Fed's hand is limited when it comes to stock markets moves, and the volatility which we saw last week could resume at any time.

DAX Gains Ground As Dollar Under Pressure

The DAX index has posted considerable gains in the Friday session. Currently, the index is trading at 12,418.30, up 0.58% since the Wednesday close. On the release front, the sole release was the German Wholesale Price Index, which rebounded with a strong gain of 0.9%, crushing the estimate of 0.2%.

It's been a dismal February for the DAX, which has shed 6.1%. However, the index has steadied, and appears headed towards its first winning week since January. The catalyst for the turnaround after the recent sell-off is strong corporate earnings in Europe. European stock markets have taken their cue from US markets, which have posted gains this week at the expense of the weaker US dollar.

The recent stock market turbulence has triggered volatility in the currency markets, and this is causing concern at the ECB. Last week, ECB President Mario Draghi said that he is more confident that eurozone inflation is moving closer to the Bank's target of just below 2 percent, due to improving economic growth. However, Draghi listed currency market volatility as an obstacle to the inflation target, and added that the ECB would carefully monitor the euro's exchange rates. The ECB tapered its massive stimulus program from EUR 60 billion to 30 billion/mth in January, and the markets are on the lookout for hints as to whether the ECB will normalize policy and wind up stimulus in September.

Technical Outlook: Spot Gold – Bulls Are Looking For Final Push Through Key $1366 Barrier

Spot Gold is holding just under new three-week high at $1361, maintaining strong bullish sentiment and focusing key near-term barrier at $1366 (25 Jan peak, the highest since early Aug 2016). The yellow metal is strongly supported by weak dollar which came under increased pressure on mounting concerns about deficit US budget and current account. Projections for current account deficit are for nearly $1 trillion in 2019 which could have further strong negative impact on the greenback. Gold could extend its broader uptrend towards targets at $1375 (early July 2016 peak) and $1391 (mid-March 2014 high) on firm break above $1366 pivot. The metal is on track for strong bullish weekly close (the biggest one-week gains since Feb 2016), which would provide further boost to existing bullish structure. However, bulls may show hesitation and enter consolidation phase ahead of $1366 pivot as slow stochastic turned sideways in deeply overbought territory and could produce bearish signal on reversal. Former lower top at $1351 (also Fri session low) marks initial support, with deeper dips expected to find support at $1343 (broken Fibo 61.8% of $1366/$1307 pullback).

Res: 1361, 1366, 1375, 1380

Sup: 1351, 1346, 1343, 1336