Sample Category Title

Week Ahead – FOMC and ECB Minutes May Rattle Markets in Quiet Data Week

Monetary policy meeting minutes from the US Federal Reserve and the European Central Bank may attract more attention than usual in the coming seven days in a relatively subdued week for economic indicators. The Reserve Bank of Australia will also be publishing the minutes of its last policy meeting. In terms of data, flash Eurozone PMIs, UK labour market report and inflation numbers out of Japan and Canada will be the main highlights.

Japan reports inflation data

The week will start with monthly trade figures from Japan on Monday. After a strong performance in 2017, Monday's data will reveal whether exports kept pace at the beginning of 2018. Exports are forecast to rise by an annual rate of 10.3% in January, while imports are expected to increase by 8.3%. The Nikkei manufacturing PMI will follow on Wednesday. It will be interesting to see whether the preliminary February report shows any evidence of a loss in business confidence from the recent turmoil in the markets as well as any impact from a stronger yen. On Friday, inflation will come into focus as the January CPI figures are released. The annual rate of core CPI (the Bank of Japan's targeted measure) is expected to ease back 0.1 percentage points to 0.8% year-on-year in January, showing the BoJ still has some way to go in achieving its 2% target.

Aussie wage growth to be eyed

The Australian and New Zealand dollars have been heading higher during the past week even though both nations' yield premium with the United States on 10-year government bonds has been wiped out, with the Australian-US spread now having turned negative. With the moves being mostly driven by US dollar weakness and risk sentiment, which the aussie and the kiwi are both very sensitive to, economic data out of Australia and New Zealand next week may struggle to make a mark in forex markets.

Nevertheless, any surprises would still have the potential to move the markets, particularly Australian pay figures. The wage price index is forecast to edge up to an annual rate of 2.2% in the final quarter of 2017 from the prior 2.0%. The RBA's Assistant Governor Luci Ellis said this week that wages are expected to pick up "but not immediately and then only gradually". A weaker than anticipated number could dampen the aussie's recent gains. Investors will get to hear more views from the RBA next week as the central bank publishes the minutes of its February policy meeting on Tuesday.

In New Zealand, retail sales numbers on Thursday will be important to watch as they will be an indication as to whether consumer spending bounced back in the fourth quarter following the slowdown in the previous quarter as a result of the uncertainty created by last September's inconclusive election.

Eurozone growth to cool slightly in February

The flash PMI readings for the Eurozone from IHS Markit are due on Wednesday and are expected to show economic activity moderating slightly in February. The composite PMI is forecast to fall from 58.8 in January to 58.5 in February with both of the index' constituents, the manufacturing and services PMIs declining too. Germany's closely watched Ifo and ZEW business confidence surveys are also forecast to display a dip in February, with the protracted CDU-SPD coalition talks possibly weighing on sentiment. The ZEW economic sentiment index is out on Tuesday and the Ifo business climate will follow on Thursday.

The euro area's final CPI print will round up the week on Friday. No revision is expected to January's preliminary reading of 1.3%. The figure remains below the ECB's target of close but below 2% and the central bank will likely stress this in its accounts of the January policy meeting, which are due on Thursday. While the minutes are unlikely to disclose anything new, they could still surprise and move the euro given the varying views among policymakers about the timing and pace of stimulus withdrawal. The single currency's recent sharp appreciation could also prompt some fresh opinions on the exchange rate.

UK employment report in focus

After this week's stronger-than-expected inflation data in the UK, all eyes will be on Wednesday's labour market report, which will contain the latest wage growth estimates. The UK's unemployment rate is forecast to stay unchanged at 4.3% in the three months to December, while average weekly earnings are also expected to hold steady, at 2.5% y/y in the same period. Another buoyant set of figures would further fuel expectations of a May rate hike by the Bank of England, while the BoE's governor, Mark Carney, may use the inflation report hearing before Parliament on Tuesday to reiterate the Bank's hawkish views.

All of this could push the pound even higher, which this week scaled back above the $1.41 level. However, a possible downward revision to UK GDP growth on Thursday could dent the current upside momentum, though the consensus forecast is that the second estimate of fourth quarter growth will remain unrevised at 0.5% quarter-on quarter.

Attention on Canadian inflation and retail sales figures

Unlike the aussie and the kiwi, the Canadian dollar took a much heavier beating from the recent market turbulence, falling to a 6-week low of C$1.2683 on February 9. Recent data has also been weighing on the loonie as it has been somewhat disappointing. But retail sales and inflation numbers due on Thursday and Friday respectively could help the currency recover further if they come in on the positive side. Retail sales are expected to rebound from 0.2% to 0.7% month-on-month, while inflation is anticipated to remain unchanged at 1.9% y/y.

South of the border, it will be a muted week in the United States, with the only major releases being the IHS Markit manufacturing and services PMIs for February and existing home sales for January, all due on Wednesday. A bigger highlight for the markets will probably be the FOMC minutes of the Fed's January meeting, which will be published on Wednesday. The Fed sounded a fairly confident tone on the economy in its press statement after the January meeting, signalling that a March rate hike is on the way. The minutes are not likely to deviate much from the statement, but investors will be sifting through them to assess the balance of views of the new 2018 voting members of the committee for possible clues on their voting bias.

Weekly Focus: The Storm Calmed Down Despite US Inflation Shock

Market movers ahead

- The main news out of the US will be the minutes from the January FOMC meeting; discussions on inflation and fiscal stimulus will be particularly interesting.

- In the euro area the focus turns to PMI and German ifo expectations – both for January. We believe the business surveys have peaked and will move slightly lower from here.

- Other global data to watch will be UK labour market report, Japanese PMI and Chinese house prices.

- In Scandi look out for Swedish inflation data and the oil investment survey and unemployment in Norway.

Global macro and market themes

- There was more fuel for the inflation scare from US core inflation…

- …but stock markets shrugged it off this time, suggesting the sell-off is over. We look for more upside in equities as fundamentals still look robust.

- We see tentative signs of a peak in the global business cycle, but growth is expected to remain solid.

- We expect the rise in bond yields to slow down, but see upside risk on a 12M horizon.

Sunset Market Commentary

Markets:

Core bonds markets fell prey to a short term short squeeze ahead of the long weekend in the US despite a third straight day of higher price pressures in the US and despite comments from ECB Coeuré who said that the debate on changing the ECB's forward guidance will start soon. The correction occurs as both the German Bund and US Note future re-entered oversold conditions. The US yield curve bull flattens with yields 1.1 bp (2-yr) to 5.6 bps (30-yr) lower. Changes on the German yield curve range between -1.4 bps (2-yr) and -4.8 bps (10-yr). 10-yr yield spread changes versus Germany are nearly unchanged with Greece outperforming (-9 bps) ahead of a potential rating upgrade by Fitch tonight (currently B-, positive outlook).

Red alert on currency markets this morning where dollar weakness prevailed. USD/JPY gave away 106.50 support despite dovish changes in the BoJ board and intervention talk from Japanese FM Aso. The trade-weighted dollar tested 88.40 support (62% retracement from 2014-2016 rally) and EUR/USD tested the cycle high (1.2537). The 62% retracement (1.2598) remained without reach. Tests failed without significant news on the economic, political, or monetary front and ahead of the long weekend in the US. Markets are closed on Monday for US President's Day. Around European noon, profit taking on dollar shorts really started to kick in. Between now and the end of February, there will be some kind of trading void with an uneventful eco calendar. Those circumstances suggest that the dollar could get some more breathing space. The failed tests of key levels also suggest a slightly firmer bottom below the greenback though we wouldn't call for a change in market sentiment yet. Therefore EUR/USD would have to break below 1.2206. Today's US eco data perhaps slightly added to the intraday momentum with strong housing data and more signs of building inflationary pressures. EUR/USD currently trades below 1.2450, USD/JPY is back above 106 and tries to regain 106.50. The trade weighted dollar moved above 89.

EUR/GBP was a beacon of stability today, trading sideways between 0.8870 and 0.8890. January retail sales disappointed and provide more evidence of reduced consumption as UK households' disposable income gets squeezed. UK PM May meets with German Chancellor Merkel later today to discuss Brexit.

News Headlines:

UK retail sales barely grew in January (0.1% M/M vs 0.6% M/M expected), providing more evidence that consumers are reluctant to spend amid a squeeze from rising prices. Retail sales rose 1.5% on a yearly basis.

US eco data beat consensus. For a third straight day, price indicators rose more than forecast. January import (1% M/M vs 0.6% M/M expected) and export prices (0.8% M/M vs 0.3% M/M expected) provided more evidence of inflation pressure following CPI on Wednesday and PPI on Thursday. US homebuilding increased to more than a one-year high in January, boosted by a rebound in the construction of single-family housing units, and further gains are likely as building permits soared to their highest level since 2007.

The last polls published by Italy's main newspapers before a blackout period starting Feb. 17 show that none of the parties or coalitions will be able to form a parliamentary majority.

ECB Coeuré signaled that officials are close to starting talks on altering their policy language as they prepare for the eventual end of bond purchases.

Elliott Wave Analysis: GOLD Can See More Upside

Gold turned up quite significantly this week which looks like an impulsive price action in progress that is expected to continue higher after broken corrective and base channel line. What we are tracking from 1306 is a five wave move in play, currently in sub-wave 4) which may look for a support at 1345-1348 area after minor three wave set-back when uptrend will be expected resume, ideally next week.

Gold, 1h

US: Homebuilders Back in Action to Start the Year

U.S. homebuilding perked back up in January, after a December lull. Homebuilders broke ground on 1,326k new homes, slightly ahead of market expectations, with the figure coming atop an upward revision in December's tally. Permits also posted a slightly better than expected result, rising 7.4% on the month.

Both single and multifamily starts posted gains. The more volatile multifamily segment saw building tick up by 24% to 449k, the highest level since December 2016. At the same time, homebuilding in the single family segment was up 3.7% to 877k, after a 10.6% drop in December.

Building permits rose a healthy 7.4% in January to 1,396k, reaching a new post-recession high. The jump was driven entirely by the multi-family segment (+26.5%). Single family permits were down slightly (-1.7%), after a period of strength in the last four months of 2017. Regionally, the strength in permits was concentrated in the South (+21.9%) and West (+5.3%), both regions attaining a post-recession high.

All regions except for the Midwest saw increased to start the year. Starts in the Northeast rose 45%, the West was up 10.7% and the South rose 9.4%. Starts in the Midwest were weak (-10.2%), and have been on a softening trend over the past year.

Key Implications

We had thought the December drop in starts was likely a blip, and that has proven to be the case. January's housing starts tally is the highest level in more than a year. And indications are that there is still momentum building, as the number of housing starts authorized, but not yet started, reached a post-crisis high.

Still, there are a few clouds over the near-term housing outlook. The changes to the mortgage interest deduction and the state and local tax deduction as part of the Tax Cuts and Jobs Act in December will impact demand housing in higher-priced and higher-taxed regions. The additional uncertainty may have led to a slight pullback in builder confidence in January, which held during February. That uncertainty adds to the challenge of a shrinking pool of construction workers, and rising mortgage rates. All these factors are expected to put downward pressure on homebuilding.

Nonetheless, optimism in the housing market remains within reach of the 18-year high hit in December. And, positive fundamentals such as a healthy labor market and accelerating wages will support demand, while tight inventories and rising prices will incentivize new homebuilding. As such, we expect residential investment to edge higher this year, albeit only modestly, led by particular strength in the single family segment.

Canadian Manufacturing Sector Ends Year on a ‘Meh’ Note

Canadian manufacturing sales dipped 0.3% lower in December - the opposite of the 0.3% gain expected by markets. After accounting for price changes the volume of sales was down by a less severe 0.1% on the month. Revisions were mixed. The prior month was revised up, with nominal sales now reported as 3.8% gain (prev. 3.4%) and real sales up 3.0% (prev. 2.5%), but earlier months figures saw downward revisions.

Durable goods were up 0.7%/0.9% in nominal/real terms respectively with strong gains in electronics, machinery, electrical equipment, and transport equipment - with the latter seeing broad based gains across motor vehicles, aerospace, as well as railroad stock and shipbuilding. However, the gain was more than offset by a decline in nondurables, down 1.3% in both nominal and real terms, led by petroleum, food, non-metallic minerals, and chemicals.

Regionally, manufacturing sales were down in all provinces but for Manitoba (+3.2%), Ontario (+1.2%) and Alberta (+1.3%). Declines were particularly pronounced in energy producing Newfoundland (-20.2%), Saskatchewan (-7.4%), but New Brunswick (-9.2%) and Quebec (-1.1%) also saw sizeable declines.

Inventories were up 0.1% on the month, with the inventory-to-sales ratio up slightly to 1.36. Forward looking indicators were mixed with new orders up 0.3% while unfilled orders pulled back 0.7%.

Key Implications

The surge in November, related to a rebound in automotive shipments after the October shutdowns, was not expected to continue through the year-end. Having said that, the performance was still somewhat disappointing, with the value and volumes of shipments down a touch and nearly half of all industries reporting declines. As a result of the weaker-than-expected performance, and downward revisions (on net) we've reduced our GDP tracking for Q4 by about 0.2 percentage points to 2%.

Still, there is some bright spots in the report. The decline was heavily concentrated in just two industries: food manufacturing and petroleum, with the weakness unlikely to be repeated. In fact, shipments in these industries should trend higher going forward, positioning the headline for a good start to 2018 despite the flat reading on U.S. industrial production to start the year. What's more, the outsized declines in Newfoundland and New Brunswick (which were responsible for double the overall pullback), are likely to be temporary.

On the whole, we remain cautiously optimistic for the Canadian manufacturing sector. On the one hand, rising global demand alongside a U.S. economy that's about to get a dose of fiscal stimulus bode well for the export-oriented sector, with the relatively inexpensive loonie also providing support. On the other hand, rising protectionist sentiment, including the resurgence of "Buy American" pose a downside risk for the sector, with the ongoing NAFTA negotiations hanging like a storm cloud over the outlook.

USDCAD Rallies on Upbeat US and Weak Canada’s Data

The US dollar rallied against its Canadian counterpart on Friday, boosted by upbeat US housing data, while loonie came under pressure on weaker than expected Canada's data. US building permits rose by 7.4% in January, compared to -0.2% in December while housing starts rose by 9.7% in January, beating forecast for 3.4% increase and vs upward-revised December's figure to -6.9%. Housing starts hit the highest since Jan 2017 and building permits rose to Nov 2017 level after showing negative results in Dec/Jan. On the other side, Canada's Manufacturing sales fell into negative territory (-0.3%) in December after huge jump previous month (3.8%). Fresh bullish acceleration is forming higher low at 1.2450 (today's spike low) where bear-leg from 1.2687 high was contained by converged 20/30SMA's. Recovery rally cracked 1.2540 barrier (Fibo 38.2% of 1.2687/1.2450 pullback) and pressures next strong barrier at 1.2555 (daily cloud base). Daily close above these barriers would generate stronger reversal signal and shift focus towards 1.2596 (Fibo 61.8% of 1.2687/1.2450) and 1.2637 (daily cloud top).

Res: 1.2555; 1.2568; 1.2596; 1.2637

Sup: 1.2506; 1.2450; 1.2416; 1.2352

Slight Dip in December Barely Dents a Solid Year for Canadian Manufacturers

Highlights:

- Manufacturing sales edged down 0.3% in December following an upwardly revised 3.8% jump in the previous month. Sales volumes were down just 0.1% in December.

- The pullback was in nondurable goods production as petroleum & coal and food manufacturing both reversed some of their earlier gains. Durable goods sales rose in the month to provide some offset.

- Overall, sales were down in 11 of 21 manufacturing sectors in December.

Our Take:

Manufacturing sales fell slightly in December after jumping higher in the previous month when a number of transitory shutdowns ended. Higher manufacturing output was a factor in November's above-trend 0.4% GDP growth. Given today's numbers we don't expect that gain will be repeated in December. Even so, we think the data continues to track annualized GDP growth of 1.9% in Q4/17, slightly softer than the Bank of Canada's 2.5% projection but still an 'above-potential' rate.

December's data closes the book on a solid year for Canadian manufacturers. Sales volumes rose 3.3% in 2017, marking the sector's best gain since 2010's post-recession rebound. 16 of 21 subsectors posted higher volumes last year, led by a double digit gain in machinery manufacturing. That sector, and a number of others, should continue to be supported in 2018 by rising business investment in Canada and the US. However, Nafta renegotiations remain a major risk to the manufacturing industry as a whole and competitiveness challenges are only being exacerbated by US corporate tax cuts. With manufacturing capacity utilization running at its highest rate since 2000, the industry will need to see some investment in order to maintain the positive growth trend that emerged last year.

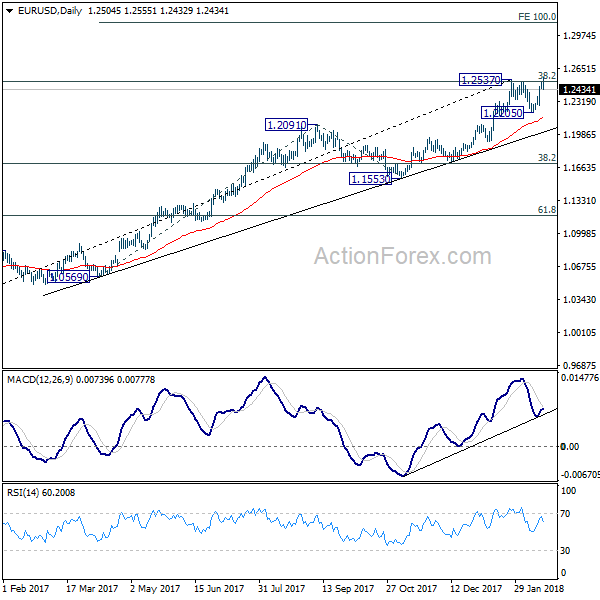

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2464; (P) 1.2487 (R1) 1.2529; More....

EUR/USD failed to sustain above 1.2537 and retreated. Break of 1.2456 minor support argues that EUR/USD could be rejected by 1.2537 resistance. Intraday bias is turned back to the downside for 1.2205 near term support. On the upside, break of 1.2555 will revive the bullish case and extend larger up trend to o 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

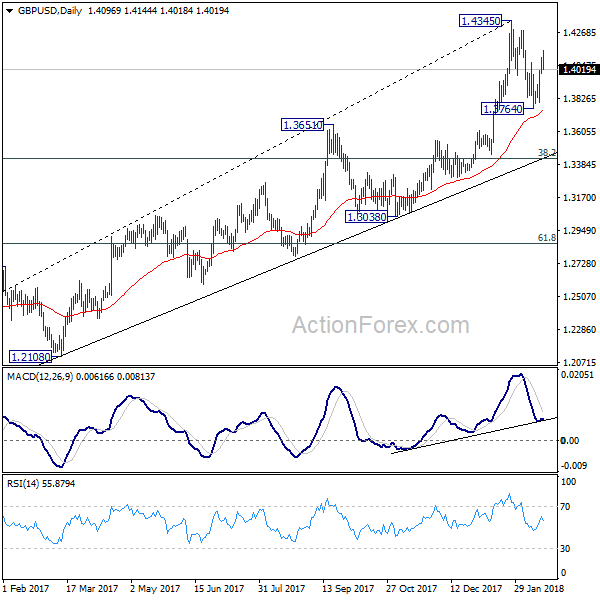

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4027; (P) 1.4065; (R1) 1.4139; More.....

Further rise is mildly in favor in GBP/USD. Pull back from 1.4345 should have completed at 1.3764 already. Retest of 1.4345 should be seen next. Break there will resume larger up trend and target long term trend line resistance (now at 1.5105). On the downside, below 1.3764 will extend the correction to 1.3651 resistance turned support instead.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279) so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.