Sample Category Title

Technical Outlook: EURUSD – Extended Recovery Pressures 1.24 Fibo Barrier, EU And US Data Expected To Provide Stronger Signals

The Euro remains firm and extends recovery rally near 1.2400 barrier (Fibo 61.8% of 1.2522/1.2205 bear-leg) on Wednesday, following Tuesday's close above 20SMA which was fresh bullish signal.

Bounce from 1.2205 correction low (09 Feb) extends for the third straight day, improving picture on daily chart as techs are returning into full bullish setup. Converged 10/20SMA's (1.2345) mark initial support and underpin for further recovery extension.

Close above 1.24 Fibo barrier will be bullish signal for renewed attacks at 1.25 zone, while close below 10/20SMA's would soften near-term tone and delay bulls.

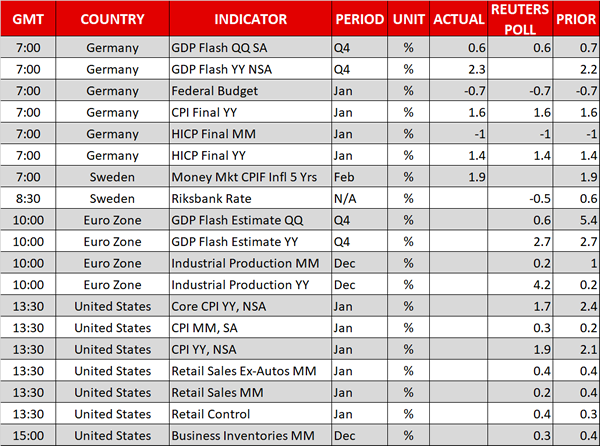

EU GDP and IP data are key releases from the Eurozone today, while US inflation data are in focus in the American session.

Bloc economy's growth is expected to stay at unchanged pace in Q4 according to the forecasts (Q4 GDP m/m 0.6% f/c vs 0.6% in Q3 and GDP q/q 2.7% f/c vs 2.7% in Q3).

On the other side, industrial production in EU is expected to increase by 0.1% in December, well below previous month's 1.0% release.

US CPI is expected to be a key driver today. Lower than expected US inflation numbers would deflate dollar and push the single currency above 1.2400.

Res: 1.2400, 1.2447, 1.2500, 1.2522

Sup: 1.2345, 1.2326, 1.2284, 1.2259

Dollar And Stocks Await Directional Clues From US Inflation

Here are the latest developments in global markets:

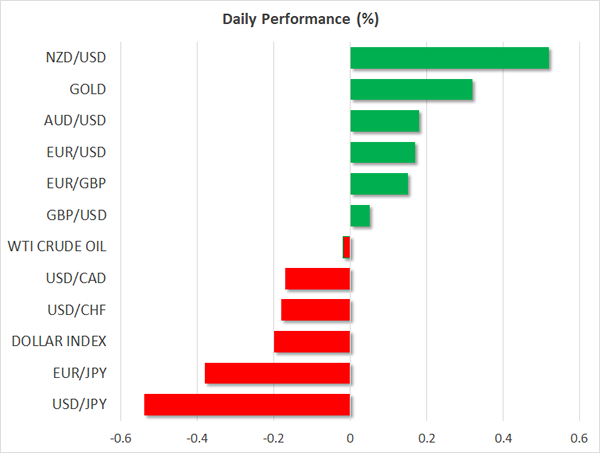

FOREX: The dollar index traded 0.2% lower on Wednesday, ahead of key US inflation and retail sales data releases that could determine the currency's short-term direction.

STOCKS: US markets closed with modest gains on Tuesday, with investors appearing hesitant to take up large positions ahead of the US inflation data today, which could determine whether the recent turmoil will intensify or subside. The Nasdaq Composite was the leader of the pack, rising by almost 0.5%. The S&P 500 and the Dow Jones gained nearly 0.3% and 0.2% respectively. At the time of writing, futures tracking the S&P, Dow, and the Nasdaq 100 are all in the green. In Asia, Japan's Nikkei 225 and Topix fell by 0.4% and 0.8% respectively – the latter recording a four-month low – but in Hong Kong, the Hang Seng was up by a remarkable 1.8%. Turning to Europe, futures tracking all the major equity indices are in positive territory, signaling they could open higher today.

COMMODITIES: Oil prices were nearly unchanged on Wednesday, after posting modest losses yesterday. The sentiment surrounding the energy market remains quite fragile. While the tentative recovery in stocks is supporting risk appetite and energy prices, the fundamentals of the oil market are showing signs of deterioration, as US production is increasing at a very rapid pace. In this respect, oil traders will look to the release of the weekly EIA inventory data today at 1530 GMT for fresh clues as to whether US oil output continued to surge in the previous week. In precious metals, gold is 0.3% higher today, boosted by the fall in the US dollar and perhaps the broader aversion to risk.

Major movers: Dollar drops ahead of critical inflation data; kiwi jumps

The US dollar came under renewed selling interest yesterday, with dollar/yen sinking to touch the 106.80 zone before rebounding, a low last seen in November 2016. While there was no clear catalyst behind the dollar's drop, the move may be owed to positioning shifts (i.e. trimming long USD positions) ahead of today's all-important US inflation figures for January. It is safe to say that these prints – and particularly the core CPI – will probably determine the near-term direction of both the dollar and US equity indices.

Let's not forget that the narrative behind this broader equity turmoil is that a surge in US inflation is just around the corner, and that the Fed may have to respond by raising rates aggressively. Investors will be looking at the CPI data to either confirm or disprove that.

In a sense, it's all about the bond market and yields today. Stronger-than-anticipated CPIs would probably push the yields on US Treasuries higher, which would be good news for the dollar, but bad news for equities, which see their demand diminish as yields move higher and higher. On the contrary, a softer inflation report than what is projected would mean that the Fed does not need to accelerate its normalization pace, something likely to push yields and the dollar lower, but provide some much-needed relief to stock indices.

In the UK, CPI data for January released yesterday showed that core inflation accelerated by more than expected, raising bets that the Bank of England (BoE) may have to respond with faster rates hikes. The pound surged on the news, but gave back its gains in the following minutes. Following the hawkish signals at last week's BoE meeting and this set of data, markets have priced in a 65% probability for a rate hike in May, according to the UK overnight index swaps.

Overnight, kiwi/dollar surged following the release of the RBNZ's updated 2-year inflation expectations print, which rose to 2.11% from 2.02% previously. This is a particularly encouraging sign for the RBNZ, which pays close attention to this indicator (in fact, a drop in this print was the key reason for the rate cuts back in early 2016). The fact that inflation expectations rose even though the actual CPI rate fell in the fourth quarter signifies that expectations remain well-anchored near the 2% mark, and increases the likelihood for a more optimistic tone by the Bank moving forward.

Day ahead: Riksbank, eurozone GDP and US inflation & retail sales on the horizon

The Riksbank will be completing it two-day meeting on monetary policy later today, with the decision on interest rates being made public at 0830 GMT; the Riksbank rate is anticipated to be maintained at -0.50%. The Governor of the Swedish central bank, Stefan Ingves, and the head of the Bank's monetary policy department, Jesper Hansson, will be holding a press conference at 1000 GMT. Krona pairs will be in focus.

At 1000 GMT, the eurozone will see the second release of Q4 2017 GDP growth. Quarter-on-quarter, the pace of expansion is anticipated at 0.6%, the same as in the first release and below Q3's respective figure of 0.7%, while annualized growth is projected to come in at 2.7%, in line with the first release and again below Q3's respective figure of 2.8%, a rate of growth last achieved in Q1 2011. Data on eurozone industrial production for the month of December will be released at the same time.

The much-talked about inflation figures out of the US are due at 1330 GMT. There are rising inflation expectations as of late in the US, and today's CPI figures could show – a least to an extent – whether those are justified. January's headline CPI is projected to grow at a stronger pace on a monthly basis, while on an annual basis it is expected at 1.9%, below December's 2.1%. Annually, core inflation is also anticipated to tick lower, with analysts projecting it at 1.7% versus December's 1.8%. The Federal Reserve's preferred inflation measure is the core personal consumption expenditure (PCE) index, but still forex market participants will be paying attention to the data as they can give insights on the speed with which the US central bank will continue to tighten its policy.

January's retail sales, released alongside CPI numbers (1330 GMT) will also be attracting interest in the US. Those exhibited positive momentum in the few previous months and are expected to have increased for the fifth consecutive month in January. Other releases out of the world's largest economy include data on December business inventories due at 1500 GMT.

Oil traders will be paying attention to the Energy Information Administration's (EIA) report including information on US crude and gasoline stocks for the week ending February 9 at 1530 GMT. Crude inventories are projected to rise for the third straight week after declining in the 10 that preceded. Specifically, analysts anticipate an increase by around 2.8 million barrels. This compares to a rise by around 1.9m barrels during the previously tracked week.

TripAdvisor will be among companies releasing quarterly results on Wednesday.

Technical Analysis: WTI oil futures trade close to 2-month low; looking bearish to neutral in short-term

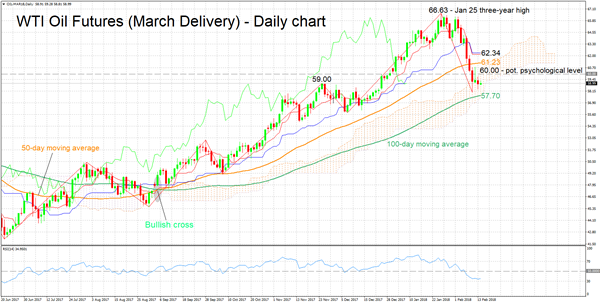

WTI oil futures for March delivery are currently trading not far above the two-month low of 58.05 hit last Friday. The short-term bias is looking bearish to neutral: The Tenkan-sen line is below the Kijun-sen, though the two lines have flatlined, suggesting that downside pressure has eased. Adding to this, the RSI has halted its decline and has been moving sideways in recent days.

If the Energy Information Administration's weekly report shows a smaller-than-anticipated increase in US crude oil inventories, oil prices could head higher. In this case, resistance could come around the 60 handle, this being a level of potential psychological significance. Prices could be meeting a barrier around the 59.00 level at the moment; the area around this point encapsulates a peak from the recent past.

On the other hand, should crude inventories rise by more than projected, then prices could weaken. In this scenario, the area around the current level of the 100-day moving average at 57.70 might provide support. The range around this point includes last week's low of 58.05, as well as the Ichimoku cloud bottom at 57.67.

Technical Outlook: USDJPY Hits New 15-Month Low Ahead Of Key US Data

The pair posted new 15-month low at 106.83 in Asian session on Wednesday, on eventual break through key med-term support at 107.31 (08 Sep low).

Fresh strength of yen was driven by overnight’s fall of Nikkei for over 1% as well as growing speculations that the Bank of Japan would follow world’s major central banks in attempts for normalizing monetary policy, despite the BoJ did not confirm such scenario.

Profit-taking caused quick bounce to 107.50, but move could be seen as positioning ahead of fresh push lower as bears remain firmly in play and eye next target at 106.51 (Fibo 61.8% of 98.99/118.66, Jun/Dec 2016 rally).

Firm break here would generate another strong bearish signal and would open way fur stronger bearish acceleration as there are no significant obstacles for bears until 103.60 zone.

Traders are focusing today’s key event, release of US inflation data, due later today. Stubbornly low inflation is one of main obstacles for Federal Reserve in attempts to increase the pace of interest rates hikes, as US economy shows solid growth and labor sector is also strong.

Inflation report would provide more clues about the pace of Fed’s raise of interest rates this year. Inflation in the US is forecasted to rise by 0.3% in January, compared to 0.1% increase previous month, while core CPI which excludes food and energy is forecasted at 0.2% in January, compared to 0.3% in

December, which marks the highest level which hasn’t been broken since 2005.

Overall, forecasts are benign and signal no significant changes which could further weigh on the greenback.

However, stronger than expected inflation numbers in January would inflate dollar for stronger bounce from new lows.

Another important event today is release of US Retail Sales, which are, according to the forecast, expected to dip to 0.2% in January, compared to 0.4% in December 2017.

Weak retail sales would also add on dollar’s bears and influence interest rates outlook.

Res: 107.50, 108.00, 108.28, 108.88

Sup: 107.00, 106.83, 106.51, 106.00

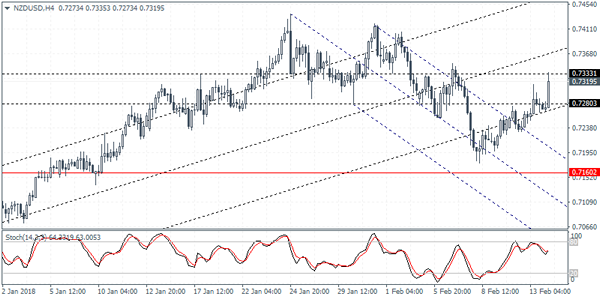

NZDUSD Intraday Analysis

NZDUSD (0.7319): The New Zealand dollar was seen rallying back to the resistance area of 0.7333 0.7280 in early trading today. The kiwi dollar was supported by the stronger inflation expectations data. We expect that the currency pair could turn flat as it trades within this resistance level. The bias remains to the downside with NZDUSD likely to test the lower support around 0.7160. In the event that NZDUSD breaks past the 0.7333 level, we can expect further gains that could be established.

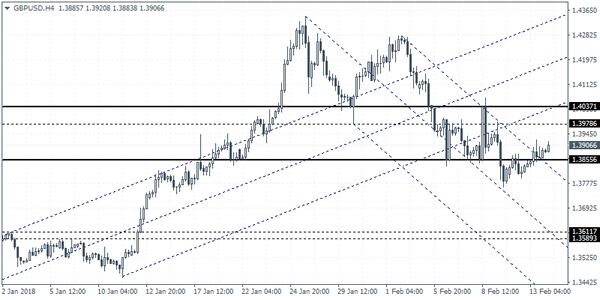

GBPUSD Intraday Analysis

GBPUSD (1.3906): The British pound continues to trade with last Friday's range with price advancing to the upside. A breakout from Friday's range could determine the near term bias in the GBPUSD. The British pound gained momentum as the inflation data showed consumer prices edging back to the 3% threshold. This sparked speculation of a faster than expected rate hike from the BoE as previously communicated by the central bank. On the 4-hour time frame, GBPUSD has close above the 1.3855 level of support which has failed to act as resistance. We expect GBPUSD to move sideways with the 1.4037 1.3855 range in the near term.

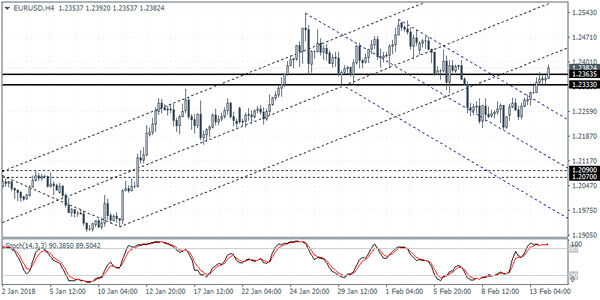

EURUSD Intraday Analysis

EURUSD (1.2382): The U.S. dollar weakened which helped to keep the euro posting gains for two consecutive days. The EURUSD was seen advancing back to the resistance level of 1.2363 - 1.2333 level in the overnight trading session. A reversal at this resistance level could signal a near term dip with the potential for the common currency to advance the declines towards the 1.2090 - 1.2070 level of support to the downside. Alternately, if price action manages to break past the resistance level, we could expect to see a new leg to the rally. This will be validated on a breakout above the previous highs posted near 1.2500.

USD Weakens As Investors Await Inflation Data

The U.S. dollar was seen falling against its peers on Tuesday amid a lack of any clear market catalysts. In the UK, data showed that consumer prices edged higher once again in January. Headline CPI was seen rising 3.0% on an annual basis while core CPI was also seen higher at 2.7%.

In Japan, the quarterly GDP data showed that the economy advanced only 0.1% on the quarter, missing estimates of a 0.2% increase. The previous quarter's GDP was however revised higher to 0.6%.

Earlier in the day, New Zealand's inflation expectations showed that inflation expectations were seen at 1.86% in one year and 2.1% in two years. The data gave a short term bump to the Kiwi dollar. The RBNZ had previously expected inflation to reach 2% band only around 2019. Looking ahead, the Eurozone quarterly GDP data will be coming out.

No changes are expected as the GDP is expected to remain steady at 0.6%. In the U.S. session, inflation data is expected to show a 0.3% increase on the month while core CPI is forecast to rise 0.2%. Retail sales figures will also be coming out at the same time.

Elliott Wave View: USDJPY Calling For More Downside

USDJPY Short-term Elliott Wave view suggests that the rally to 110.48 high ended Intermediate wave (4) bounce on February 02.2018 peak. Below from there, the decline is unfolding as an Ending Diagonal Structure within Intermediate wave (5) lower. Where Minor wave 1 ended at 108.44 low as Zigzag structure, Minor wave 2 bounce ended at 109.77 in a Double three correction. Currently, Minor wave 3 remain in progress in a Double three correction, where internals of each leg is unfolding as Elliott Wave Zigzag pattern.

Where Minutte wave ((w)) ended at 108.03 low, Minute wave ((x)) ended at 108.87. Below from there Minute ((y)) of wave 3 remains in progress as zigzag structure. When Minutte wave (a) ended in 5 waves at 107.39 low and Minutte wave (b) ended at 107.89. Near-term cycle from 2/08 high (109.77) is mature already in Minor wave 3 lower after reaching blue box area (as shown on Chart). And pair can now start the Minor wave 4 bounce anytime soon in 3, 7 or 11 swings. However within the shorter-term cycles pair could extend lower towards 106.39-105.47 100%-161.8% Fibonacci extension area of (a)-(b) within ((y)) of 3 lower before a bounce in Minor wave 4 takes place. We don’t like buying the pair and as far as a pivot from 2/08 high 109.77 holds the wave 4 bounce should get rejected in 3, 7 or 11 swings for further downside extension in Minor 5 of (5) lower.

USDJPY 1 Hour Elliott Wave Chart

GBPUSD Looking For Gains Above 1.3892 Pivot

The British pound continues to hold above the key 1.3892 pivot level against the U.S dollar, although buyers remain cautious ahead of today’s key CPI inflation release from the American economy. The GBPUSD pair currently trades around the 1.3900 handle, although buyers again failed to take-out Tuesday’s high overnight, with price failing around the 1.3320 level. Going forward, sterling traders look to ongoing weakness in the U.S dollar index and a clear breakout from the current 1.3292 to 1.3320 price-range.

The GBPUSD pair remains intraday bullish whilst clearly trading above the 1.3892 level, further buying towards the 1.3939 and 1.4000 levels still seems possible.

Should GBPUSD price-action slip back below the 1.3892 level for an extended period, we may see sellers test back towards the 1.3855 and 1.3832 levels.

EURUSD Intraday Bullish ABove 1.2332 Level

The euro has continued to press higher against the U.S dollar overnight, hitting 1.2392, as broad-based weakness in the greenback persists. The EURUSD currently trades around the 1.2370 region, with bullish intraday momentum largely intact whilst the pair trades well above the 1.2332 technical support level. Traders now look to a slew of economic data this morning, with key German January CPI Inflation figures and fourth fiscal quarter Gross Domestic Product numbers from the eurozone.

The EURUSD pair remains intraday bullish whilst trading above the 1.2332 level, further upside towards 1.2400 and 1.2432 seems likely.

Should EURUSD price-action slip back below the 1.2332 level, we may see sellers start to target the1.2290 and 1.2255 support levels.