Sample Category Title

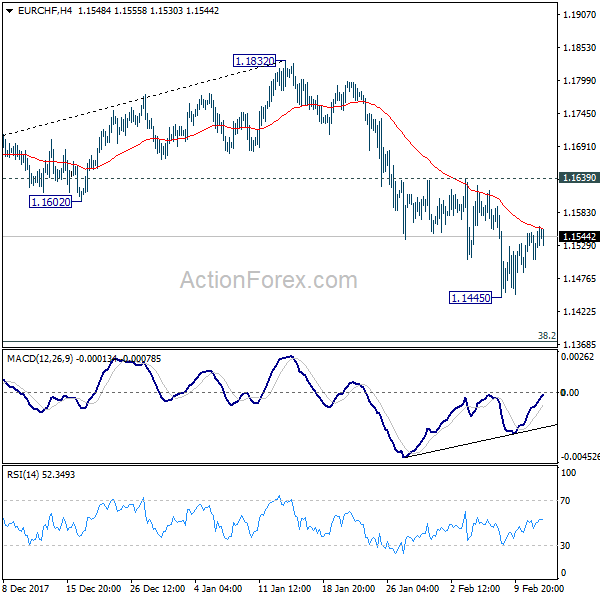

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1516; (P) 1.1539; (R1) 1.1571; More...

EUR/CHF is staying in consolidation above 1.1445 and intraday bias remains neutral With 1.1639 resistance intact, further decline is expected. Below 1.1445 will extend the corrective fall from 1.1832 to 1.1355 cluster support (38.2% retracement of 1.0629 to 1.1832 at 1.1372.) At this point, we'd expect strong support from there to contain downside and bring rebound.

In the bigger picture, a medium term top should be in place at 1.1832 on bearish divergence condition in daily MACD. But there is no indication of long term reversal yet. As long as 1.1198 resistance turned support holds, we'd still expect another rise through prior SNB imposed floor at 1.2000.

Market Morning Briefing: Euro Has Risen 100 Pips

STOCKS

Overall major stock indices are mixed. While Dow looks bullish, Dax may trade sideways. Nikkei is trading near crucial support which may either hold or break on the downside. Shanghai has recovered from deep lows and may now be on the recovery mode. No strong trend visible for the week.

Very sharp recovery seen in Dow (24640.45, +0.16%) from levels near 24190. While support near 23200 on the 3-day candles hold, we may see an attempt to rise towards 25000-25200 levels in the near term before again coming off towards 24000 or lower.

Dax (12196.50, -0.70%) has an immediate resistance near 12400 and higher at 12600. While these hold, some sideways range-trade is possible in the 12400-12100 region with a possible extension to 12600 in the medium term.

Nikkei (21109.29, -0.64%) is holding above the support near 21000 on the 3-day candles. While the support holds, an attempt to rise towards 22200 is possible in the coming sessions. A break below 21000, if seen could be vulnerable for the index taking it towards 20500 or even lower in the medium term. But for now we may expect 21000 to hold.

Shanghai (3176.95, -0.25%) has recovered from levels near 3060. A possible test of the earlier support turned resistance near 3250-3260 could be again seen in the coming sessions. Immediate support is seen in the 3060-3100 region which is likely to hold in the near to medium term.

Nifty (10539.75, +0.81%) and Sensex (34300.47, +0.87%) have recovered from the previous lows seen last week. The indices may trade in the green for a few more sessions before coming off to lower levels. Immediate targets for Nifty and Sensex is seen at 10600-10800 and 35000 respectively.

COMMODITIES

Brent (62.80) has support in the 61-62 region and while that holds, a bounce back towards 65 Is preferred just now. WTI (59.17) has similar support near 57.30-58.00 region which may push the price upwards to levels near 60-62 in the coming sessions. Near term likely to be bullish.

Gold (1337.20) is gradually moving up. A re-test of 1340-1345 is possible in the near term. View is bullish for this week.

Copper (3.1560) has managed to move back above 3.0750 and while that holds, the price may continue to move up towards 3.20-3.25 in the coming sessions. Near term looks bullish.

FOREX

The Dollar has weakened considerably against major currencies, thereby bringing the Dollar Index (89.51) down to levels near 89.50 from levels near 90.5 prevailing till Monday. The US CPI data release today is being looked at very closely for cues on inflation trends. Higher than expected inflation numbers for Jan’18 could lead to some near term selloff in both equity and debt markets, weakening the Dollar further in the next 1-2 weeks. On the 3 day candle and weekly candles,support near 88.5 could be tested.

Euro (1.2382) has risen 100 pips as the Dollar Index fell by approximately 1 point over the last 2 days. If the Dollar Index falls by 1 more point towards 88.5 by next week, the likelihood of which is projected above, Euro could again test resistance on the weekly line chart near 1.245-1.248.

Contrary to our expectation, Dollar Yen (107.09) didn’t see the strong support zone near 108.0-108.5 hold up and has broken below it. This downmove has also broken long term support on the weekly line charts (which was seen on a trend line coming from 2012). This could signal the onset of bearishness for Dollar Yen in the medium term. The next target on the downside could be 106.5 – seen as supports on both 3 day and weekly candles.

Our expectation for Euro Yen (132.51) to move up has also not surfaced due to renewed Yen strength. It could again test horizontal support near 132 on the 3 day candles by next week as Euro moves towards 1.24 and Dollar Yen towards 106.5.

The Pound (1.3913) might have just found support near 1.380-1.385 on the daily and 3 day candles which negates our view of seeing it drop till 1.37. We will have to wait and watch for the same to be confirmed in the coming sessions.

Dollar Rupee (64.135) – is trading at much lower levels compared to Monday in the morning session. There is a possibility of testing 64 soon if the Dollar weakens further against majors.

INTEREST RATES

US 10 Year Yield (2.81), US 30 year Yield (3.09), US 5 year yield (2.527), US 2 year yield (2.094) : US longer term yields have been consolidating ahead of the important inflation data release . However, the 10 Year had tested highs near 2.89% on Monday and has come down from there, thereby lending some validation to our view that yields will respect their long term resistance levels. We repeat that our expectation is for the 4 yields to respect their long term resistance levels (2.85-2.90 -earlier mentioned as 2.85, 3.20 , 2.7 and 2.2 respectively) in this month.

US 10-5 Year Yield Spread (0.28) as expected has come down a bit after touching 0.31 on Monday. It could slowly move towards 0.35 by Mar’18.

German 10 Year bond yield (0.75) is continuing its ranging between 0.7 and 0.76 as predicted.

Japan 10 year bond yield (0.067) has broken important support on short term chart near 0.07. It is dips further, we might see further strengthening of Yen against the Dollar.

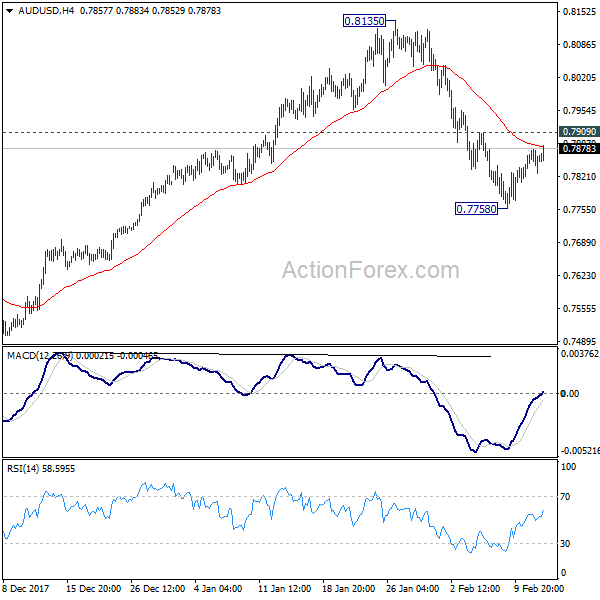

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7831; (P) 0.7854; (R1) 0.7880; More...

Intraday bias in AUD/USD remains neutral with 0.7909 minor resistance intact, and deeper fall is in favor. Break of 0.7758 will extend the fall from 0.8135 to 0.7500 key support. At this point, there is no clearly sign of larger trend reversal yet. Hence, we'd look for strong support from 0.7500 to contain downside and bring rebound. On the upside, above 0.7909 minor resistance will turn bias back to the upside for retesting 0.8135 high.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed.

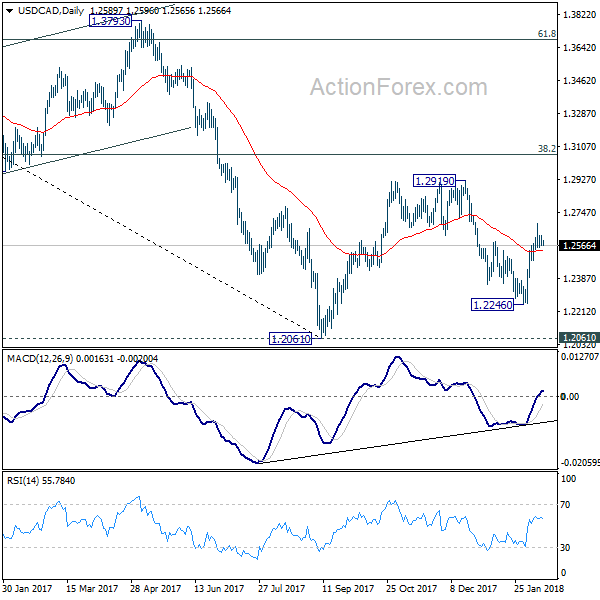

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2564; (P) 1.2594; (R1) 1.2624; More....

Intraday bias in USD/CAD stays neutral for consolidation below 1.2687 temporary top. Further rise is in favor as long as 1.2489 minor support holds. Above 1.2687 will extend the rise from 1.2246 to 1.2919 resistance next. However, below 1.2489 will turn bias back to the downside for 1.2246 again.

In the bigger picture, the rebound from 1.2246 is mixing up the medium term outlook. Nonetheless, USD/CAD is staying below falling 55 day EMA, hence, the bearish case is in favor. That is, fall from 1.4689 is not completed yet. Sustained break of 1.2061 key support will carry larger bearish implication and target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. However, firm break of 1.2919 will revive the case of medium term reversal and turn outlook bullish.

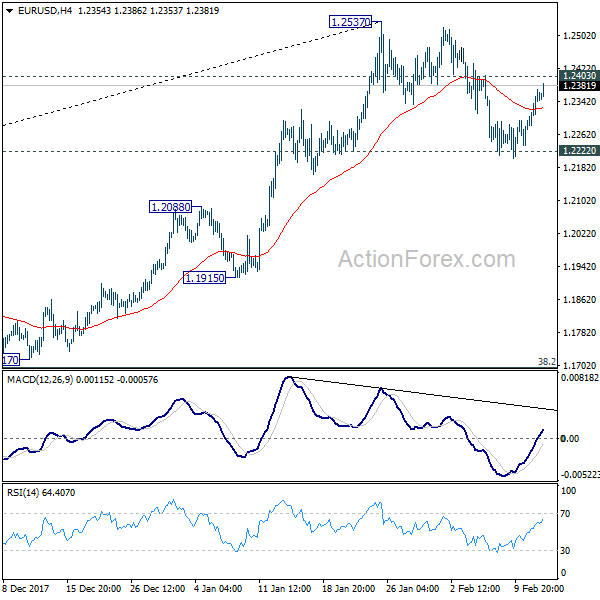

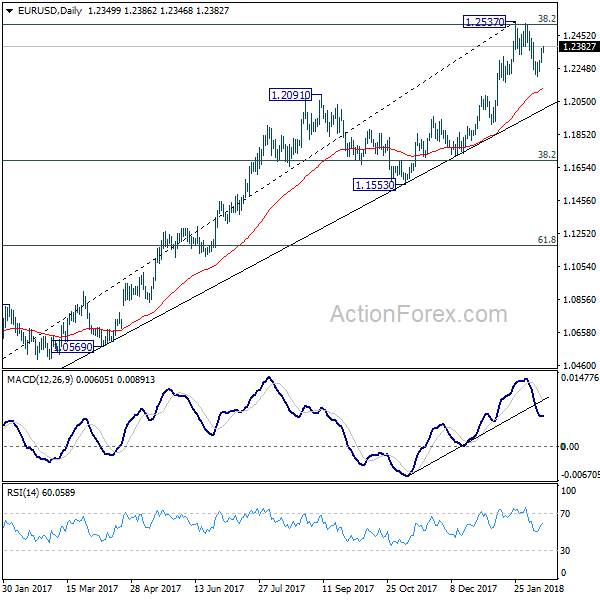

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2300; (P) 1.2335 (R1) 1.2387; More....

At this point, EUR/USD is staying below 1.2403 minor resistance and intraday bias stays neutral. On the downside, sustained break of 1.2222 key support should confirm rejection from 1.2516 key fibonacci level, as well as near term reversal, on bearish divergence condition in 4 hour MACD. That could also signal completion of medium term up trend from 1.0339. In that case, near term outlook will be turned bearish for 38.2% retracement of 1.0339 to 1.2537 at 1.1697. On the upside, though, above 1.2403 minor resistance will revive bullishness and turn focus back to 1.2537.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

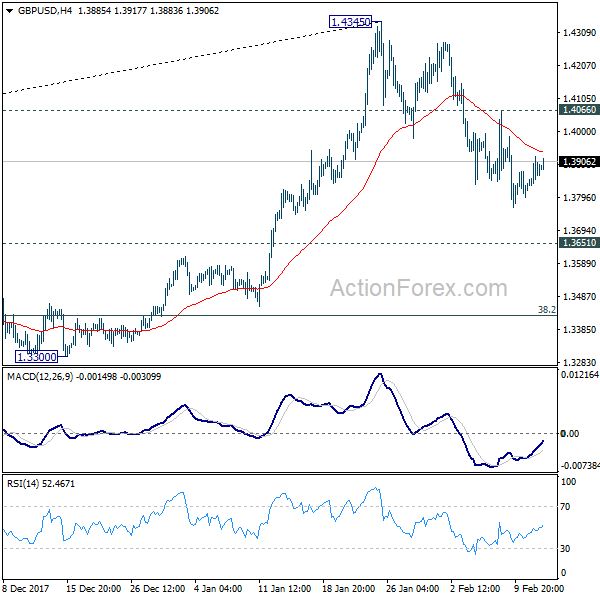

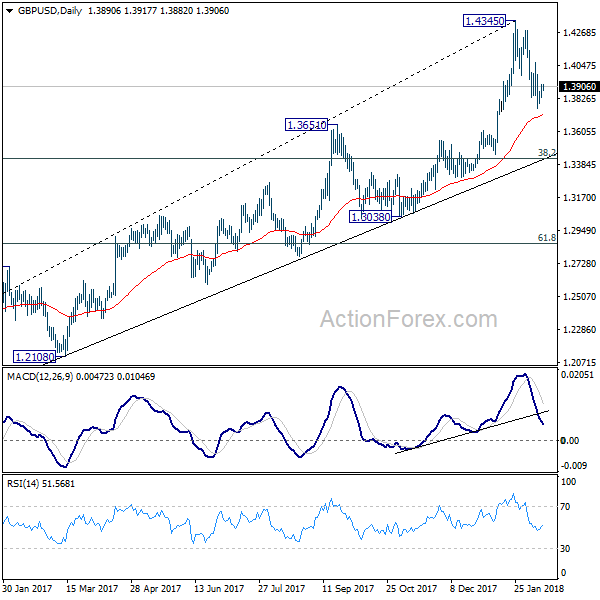

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3841; (P) 1.3882; (R1) 1.3932; More.....

No change in GBP/USD's outlook, with 1.4066 minor resistance intact, deeper fall is expected in GBP/USD for 1.3651 resistance turned support. It's still unsure whether decline from 1.4345 is correcting rise from 1.3038, or that from 1.1946, or it's reversing the trend. Break of 1.3651 will turn focus to key fibonacci level at 1.3429. On the upside, break of 1.4066 will turn bias back to the upside for retesting 1.4345 instead.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279 so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

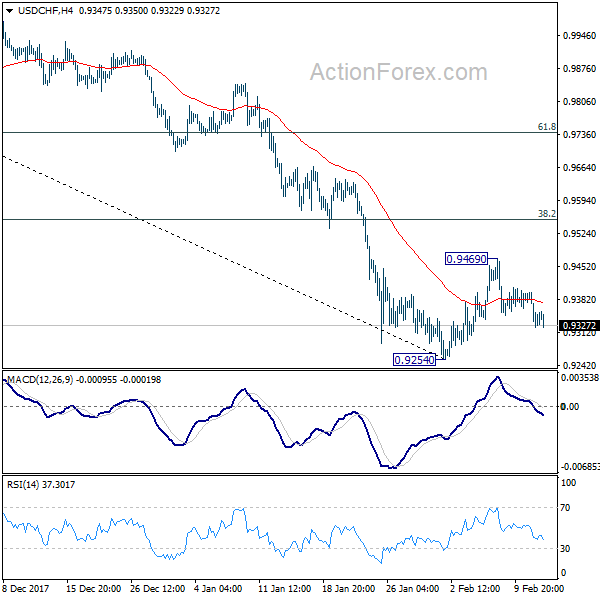

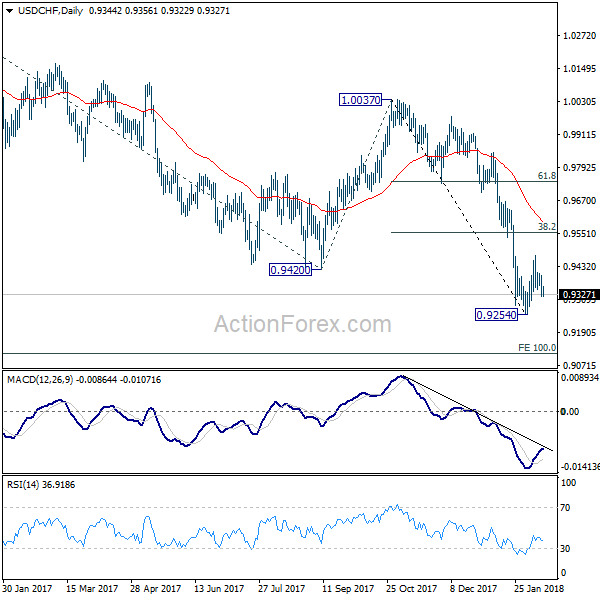

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9315; (P) 0.9356; (R1) 0.9391; More...

Intraday bias in USD/CHDF remains on the downside for 0.9254 low. Break will resume larger down trend to next projection level at 0.9115. Also, note again that there is no sign of trend reversal yet. Therefore, in case of another rise, we'd be cautious on strong resistance from 38.2% retracement of 1.0037 to 0.9254 at 0.9553 to limit upside and bring down trend resumption.

In the bigger picture, fall from 1.0342 is developing into a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

The Day Of Reckoning

The markets were reasonably busy overnight in preparation for this evening US CPI, and with some G-10 traders arguing this is the most significant economic release in the past three years, and at a minimum, the consensus is that that the US CPI release on will provide the next directional signal for markets. The announcement should generate an outsized volume of noise.

There is little to fret about the forecasted number in itself, but traders will be keying the divergence, direction and delta of the miss. Most certainly a higher CPI will be initially interpreted through USD strength, higher yields and lower equities bolstering the market views post-AHE narrative that inflation scare could push Treasury yields much higher and send equities spiralling lower.

It certainly feels like the proverbial calm before the storm and rightly so as there plenty of reasons to be cautious, but whether it warrants the present sense of foreboding in the markets or not, equity investors seem undeterred by the possibility of higher yields. US equities finished in the green for the 3rd consecutive day ahead of the critical inflation print despite the fresh memories of last weeks market carnage in the wake of an inflationary uptick in wage growth.

While there remains the concern that investors are shifting from growth to inflation narrative.A spike in CPI will reinforce that moving storyline and will draw much attention to the bond markets. However, the more significant risk for Bond Traders may be a tepid CPI reading given the staggering bearish short positions in 10 year US bonds that would likely unwind.

However, given the complexities of current market conditions straightforward outcomes are seldom honest so buckle up for a bumpy ride.

Ultimately the Fed still holds the cards, and with the markets teasing the idea of Powell fluttering, I defer to my usual stance of expecting the unexpected when it comes to essential data readings these days.

Oil markets

The mood is very bearish!

The oil landscape is looking a bit precarious given the rebounding the S&P and the weaker dollar, oil prices are struggling dearly to find solid footing. When typical market tailwinds start blinking red on the correlation matrix something is bound to snap.

If we needed further convincing that Shale Producers are rounding into form, The American Petroleum Institute (API) reported a build of 3.947 million barrels of United States crude oil inventories for the week ending February 9, But it gets even messier for oil prices when you factor in the extraordinary build in gasoline inventories.

But when regional( Singapore) physical brokers are struggling or find buyers its something that should not be overlooked and by all accounts we could be setting up for another significant oil correction towards the fundamental WTI 55 support level.

With the market shifting from growth to the inflation narrative, an oil market correction lower will add another level of complexity into the inflation storyline as it should have a significant influence on US treasury yields ( lower)

Gold Markets

The weaker US dollar and softer US bond yields certainly helped restore gold investors bravado overnight. With the US dollar once again striking a bearish chord amongst G-10 traders .the long gold set up looks favourable. However, with nearly 100 % of Gold appeal trading off the back of US dollar weakness, the US CPI reading could be a day of reckoning for Gold bulls.

Currency Markets

USD is trading weaker across the board as the market is tentatively returning to familiar themes.

The Japanese Yen

Dollar-yen quickly turned into a pain trade for dollar bulls overnight. There has been a lot of discussion on the move, but it boils down to Prime Minister Abe comment we have a blank slate for choosing next BoJ governor” which saw the market tentatively position for a possible more hawkish changing of the guard at the BoJ

But now we’ve dispatched the 108 level ahead of tonight US CPI, and with overnight vols skyrocketing, it suggests USDJPY will be the biggest mover on the release. Of course, the set up will be immensely tricky as a high inflation print could cause an equity meltdown and trigger an immediate risk aversion currency trade while a softer copy should weigh on general dollar sentiment as the macro landscape will come under question.

The massive tail risk is on the break of 107.25 which could cause panicked exporters to enter the fray not to mention funds adjusting their USDJPY hedge ratios

Certainly a busy night in store in the Yen desk

The Euro

Market is favouring the short USD position heading into the CPI, so USD dollar direction remains the key driver

The Malaysian Ringgit

The Ringgit remains precariously perched ahead of today’s Key GDP

On the contrary front, oil markets are looking increasingly bearish which is limiting MYR appeal

US Dollar Rout Continues With Inflation Data In The Horizon

Safe haven flows after the stock market collapse favour JPY and CHF

The US dollar is once again on the back foot on Tuesday. The currency is softer against major pairs ahead of key US inflation data for January. The U.S. Federal Reserve along with traders will be looking at the consumer price figures for signs of higher inflation and further validations of their plans to keep raising US interest rates in 2018. The U.S. non farm payrolls (NFP) report earlier in the month boosted the USD with a positive wage growth signal at 0.3 percent monthly gain. The market will be watching the core CPI released on Wednesday, February 14 at 8:30 am EST looking for confirmation.

- US January inflation expected to underperform

- US Oil producers putting downward pressure on prices

- US inflation trend to continue on Thursday with the release of the PPI

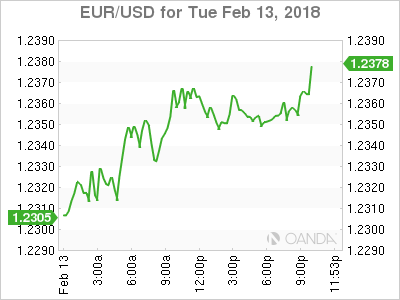

The EUR/USD gained 0.52 percent on Tuesday. The single currency is trading at 1.2355 ahead of the release of monthly inflation and retail sales data in the US. The U.S. Federal Reserve is expected to lift rates 3 or more times this year, but to do so it would need inflation in the US to pick up, as this was the biggest debate within the central bank last year. Doves within the Federal Open Market Committee (FOMC) are pushing for more patience, until inflation rises, while the hawks who lost Chair Yellen as their biggest supporter would rather raise rates sooner rather than later. The core consumer price index, the Fed pays more attention to this data point that excludes food and energy, is expected to come in at 0.2 percent. Retail sales are forecasted to have gained 0.2 percent in January, but the core reading to have advanced by 0.5 percent by removing auto sales.

The tumble in stocks prices has had a negative effect on the confidence in the US economy. The employment report released on February 2 posted higher than forecasted number of jobs and more importantly hourly wages rose by 0.3 percent. Several dollar rallies that started with a strong employment report have been cut short by disappointing inflation and retail sales data. This time around the USD has not been able to find solid footing in 2018. With a stock market correction and bond yields at four year highs inflation takes a more important role as it could solidify the case of Fed hawks and make way for a 4 rate hike scenario. The USD has been impacted by improving growth around the globe and other central banks have hiked or signalled and end to low rates cutting the lead of the U.S. Federal Reserve and reducing the attractiveness of the dollar. A higher than expected inflation figure could trigger a US currency recovery alongside a drop in the stock market as higher rates would be forthcoming. Vice versa a lower than expected consumer price gain could sink the dollar even lower as the market is already pricing in 3 rate hikes and could start reevaluating that position with weak inflationary pressures.

European politics have reached some stability with the German coalition now in place but with the upcoming Italian elections in March the boat is sure to rock. Economic fundamentals have been strong in the eurozone with Germany leading the way as usual. The gap between the U.S. Federal Reserve and the European Central Bank (ECB) is closing with regarding monetary policy. The ECB is expected to end its QE program and could even lift interest rates later this year. The week will bring minor indicator releases in Europe with the German central bank chief Jens Weidmann speaking in Frankfurt on Wednesday, February 14 at 3:00 am EST. Earlier that day the GDP figures for Germany will be released with a 0.6 percent growth expected.

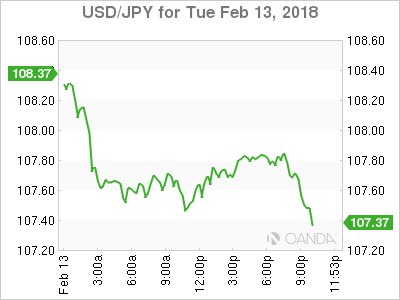

The USD/JPY lost 0.84 percent in the last 24 hours. The currency pair is trading at 107.73 as the JPY has benefited from risk aversion and risk appetite moves. Usually the USD is the main beneficiary of a risk aversion move, but given some of the global uncertainty is happening in Washington and Wall Street the greenback is not the sturdiest safe haven for investors. The USD is soft ahead of inflation and retail sales data with both having to overcome concerns.

The Japanese Prime Minister Shinzo Abe is expected to reappoint Haruhiko Kuroda as the head of the Bank of Japan (BOJ) for his second term and that in itself could be a sign the central bank is ready to start dealing back some of its massive stimulus program.

Market events to watch this week:

Wednesday, February 14

8:30am USD CPI m/m

8:30am USD Core CPI m/m

8:30am USD Core Retail Sales m/m

8:30am USD Retail Sales m/m

10:30am USD Crude Oil Inventories

7:30pm AUD Employment Change

Thursday, February 15

8:30am USD PPI m/m

Friday, February 16

4:30am GBP Retail Sales m/m

8:30am USD Building Permits

Gold Gains Ground As Weak Bonds Weigh On Dollar

Gold prices continue to move higher this week. In Tuesday’s North American trade, the spot price for an ounce of gold is $1326.90, up 0.32% on the day. There are no major events out of the US. On Wednesday, the US releases inflation and retail sales data. Traders should be prepared for some movement from XAU/USD during the North American session.

Gold headed lower last week, as the US dollar received a boost from a tumultuous week on global stock markets. Is the correction over? It’s too early too tell, but gold has posted gains in the Monday and Tuesday session, erasing most of last week’s losses. It’s no exaggeration to say that Wednesday’s inflation reports will be among the most important in recent memory, coming on the heels of the stock market meltdown. Much of the sell-off has been attributed to investor concerns over higher inflation, which could lead to a faster pace of rate hikes. If Wednesday’s inflation indicators are higher than expected, we can expect some volatility in gold prices and further sell-offs in the stock markets. The new head of the Federal Reserve, Jerome Powell, sought to send a reassuring message on Tuesday, saying that the Fed is on alert to any risks to financial stability. However, it’s clear that the Fed’s hand is limited when it comes to the volatile market movement which marked last week and could resume at any time.