Sample Category Title

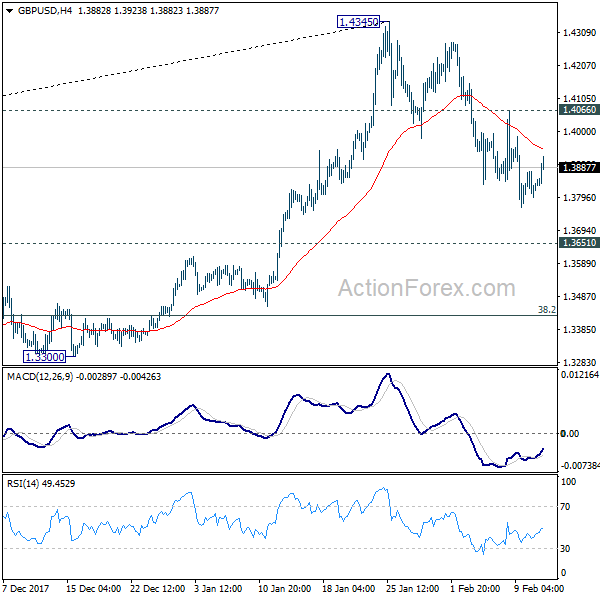

GBPUSD Intraday Bullish Above 1.3892 Level

The British pound has moved sharply higher against the U.S dollar during the European trading session, following the release of better than expected Core CPI inflation figures from the United Kingdom Economy. The GBPUSD pair has so far found intraday resistance around the 1.3920 level, with price-action testing back towards the 1.3900 region. Sterling traders will now look towards the pivotal 1.3892 level for direction and the U.S dollar index, which is currently suffering heavy daily losses.

The GBPUSD pair remains intraday bullish whilst trading above the 1.3892 level, further upside towards the 1.3939 and 1.4000 resistance levels appears possible.

Should GBPUSD price-action slip back below the 1.3892 level, we may see a downside correction back towards the 1.3832 and 1.3775 support levels.

USDCAD Trend Line is Rejecting the Rally

The USD/CAD is rejecting the trend line and the POC zone 1.2580-1.2600 with a very congested move that still lacks the real bearish momentum. The weakness in oil prices weighs on CAD and that could be the reason for a consolidation without a bearish break. However if the pair keeps rejecting the POC zone we might see a drop to 1.2561, 1.2542 and 1.2512. The pair should find buyers there due to its strong weekly support (W L3) that hasn't been tested yet.

- W H3 -1.2055 should give another upside boost to the pair.

- W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

- W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

- W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

- D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

- D L3 - Daily Camarilla Pivot (Daily Support)

- D L4 - Daily H4 Camarilla (Very Strong Daily Support)

- POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

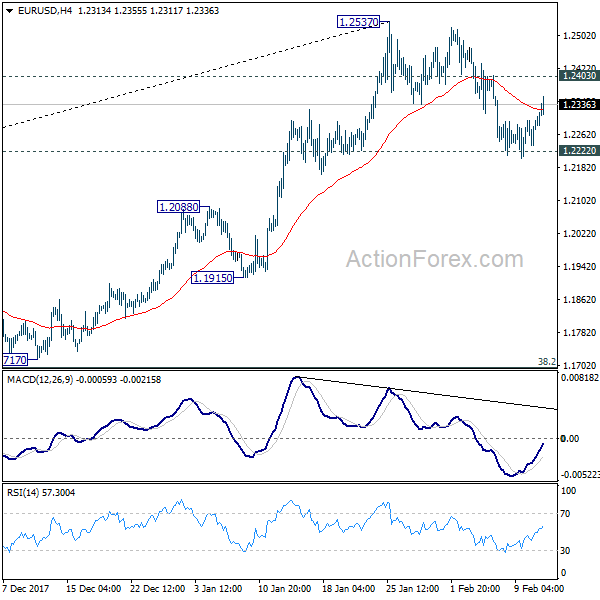

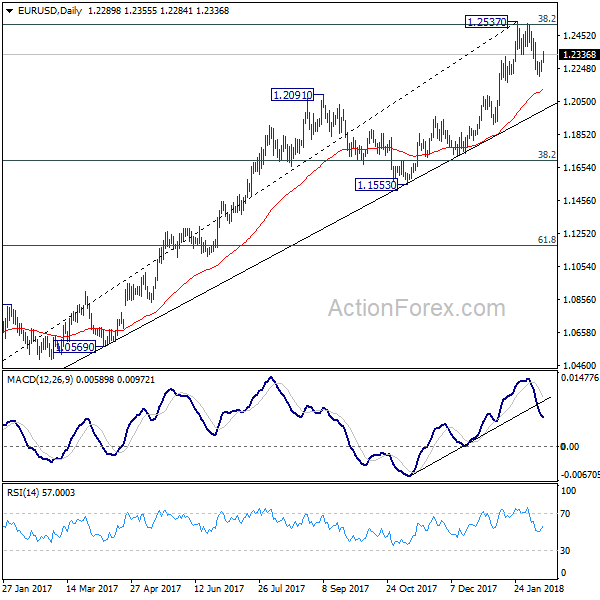

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2250; (P) 1.2274 (R1) 1.2313; More....

EUR/USD recovers further today but stays below 1.2403 minor resistance, intraday bias remains neutral first. On the downside, sustained break of 1.2222 key support should confirm rejection from 1.2516 key fibonacci level, as well as near term reversal, on bearish divergence condition in 4 hour MACD. That could also signal completion of medium term up trend from 1.0339. In that case, near term outlook will be turned bearish for 38.2% retracement of 1.0339 to 1.2537 at 1.1697. On the upside, though, above 1.2403 minor resistance will revive bullishness and turn focus back to 1.2537.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3796; (P) 1.3835; (R1) 1.3876; More.....

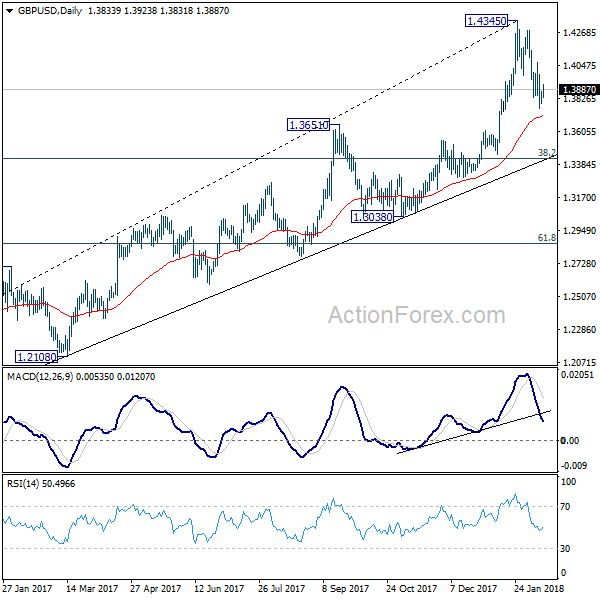

No change in GBP/USD's outlook, with 1.4066 minor resistance intact, deeper fall is expected in GBP/USD for 1.3651 resistance turned support. It's still unsure whether decline from 1.4345 is correcting rise from 1.3038, or that from 1.1946, or it's reversing the trend. Break of 1.3651 will turn focus to key fibonacci level at 1.3429. On the upside, break of 1.4066 will turn bias back to the upside for retesting 1.4345 instead.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279 so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

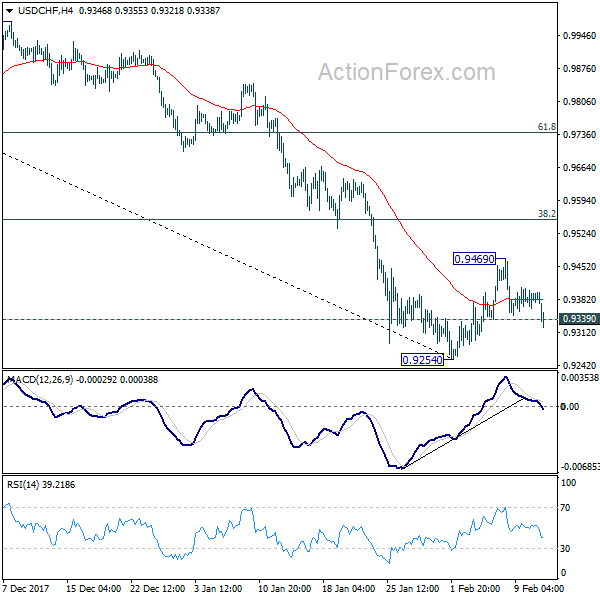

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9368; (P) 0.9386; (R1) 0.9409; More...

USD/CHF's break of 0.9339 minor support suggests that rebound form 0.9254 has completed at 0.9469 already. Intraday bias is turned back to the downside for 0.9254 first. Break will resume larger down trend to next projection level at 0.9115. Also, note again that there is no sign of trend reversal yet. Therefore, in case of another rise, we'd be cautious on strong resistance from 38.2% retracement of 1.0037 to 0.9254 at 0.9553 to limit upside and bring down trend resumption.

In the bigger picture, fall from 1.0342 is developing into a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

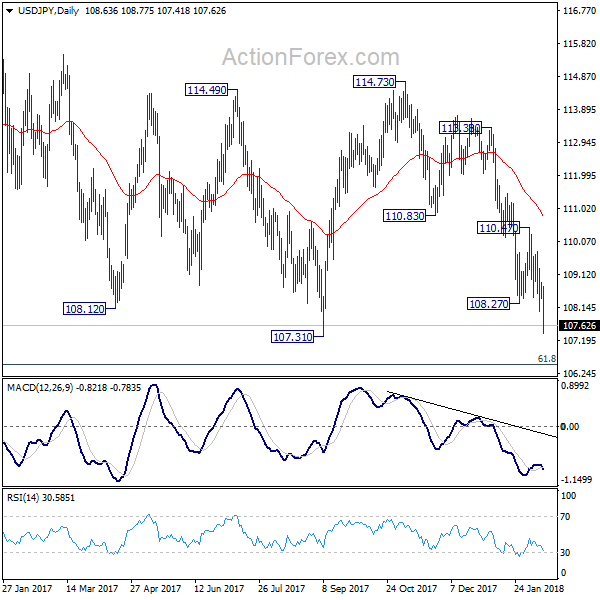

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.43; (P) 108.65; (R1) 108.88; More...

USD/JPY's decline continues today and reaches as low as 107.41 so far. Intraday bias remains on the downside and break of 107.31 will target 106.48 fibonacci level. We'd look for strong support around there to bring rebound. However, on the upside, break of 108.80 minor resistance is needed to be the first sign of short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD/JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

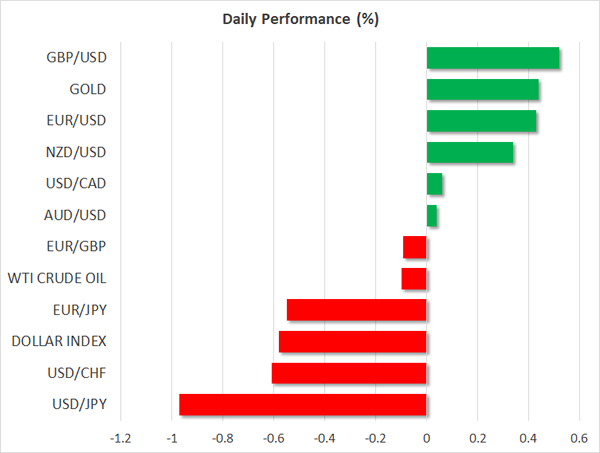

Yen and Franc Gains as Stocks Recovery Loses Momentum, Sterling Supported by CPI

Yen and Swiss Franc jump broadly today as the recovery in global stock markets lose steam again. At the time of writing, both DAX and CAC 40 are trading in red even though FTSE is mildly higher. That followed -0.65% decline in Nikkei earlier in the day. US futures also point to another day of loss. Sterling follows as the third strongest one for the day after higher than expected consumer inflation reading. On the hand, commodity currencies, and Dollar, are trading generally lower.

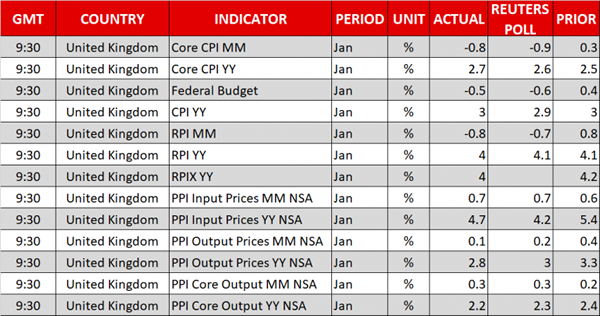

UK CPI unchanged at 3.0% yoy, beat expectation

UK headline CPI was unchanged at 3.0% yoy in January, above expectation of 2.9% yoy. Core CPI accelerated to 2.7% yoy, up from 2.5% yoy and beat expectation of 2.6% yoy. RPI slowed by 0.1% yoy to 4.0% yoy. PPI input slowed to 4.7% yoy, PPI output slowed to 2.8% yoy, PPI output core dropped to 2.2% yoy. Also from UK, house price index rose 5.2% yoy in December.

With CPI staying above 2% target level for 12 straight month, it adds to the case for BoE to pull ahead this year's rate hike to May. BoE known hawk Ian McCafferty said yesterday that the economy is "holding up well" with improvements globally too. But there are a "great deal of uncertainty around the Brexit negotiation and how that might affect both business and consumer confidence. And therefore, "we will be watching the data and making our decisions on a month by month basis."

Also from Europe, Swiss PPI was unchanged at 1.8% yoy in January.

Japan PMI Abe expects BoJ to continue with "bold steps"

In Japan, Prime Minister Shinzo Abe told the parliament that "surveys show banks' lending attitudes to small- and medium-sized companies remain healthy even after the introduction of negative rates." And he expected BoJ to "continue to take bold steps to achieve price stability in response to movements in prices and the economy." Abe also said he hasn't made the decision on whether to give Haruhiko Kuroda a second term as BoJ Governor yet. But Finance Minister Taro Aso said that fluent English is a "very important condition" to head BoJ. This is seen by some as endorsement to Kuroda. Kuroda was a former head of the Asian Development Bank and top Japanese currency diplomat.

Released from Japan, machine tool orders rose 48.8% yoy in January. Domestic CGPI rose 2.7% yoy in January.

Australia business confidence hit 9 month high

Australia NAB business confidence rose 2 points to 12 in January, hitting a 9-month high. Business condition index rose 6 points to 19. NAB chief economist Alan Oster noted in the release that "while forward orders have eased a little, they remain above average and capacity utilisation has been trending up which is a good sign for both future investment and employment."

RBA Ellis: Wage growth to be gradual

RBA Assistant Governor Luci Ellis said that wages are forecast to "pick up from here", but "not immediately and then only gradually". She added that "firms are increasingly using other creative ways to attract and keep staff without paying across-the-board wage rises." And, "they are especially reluctant to grant wage rises, because this would increase one of their most important costs." Meanwhile, Australia is still "a bit further behind" some other advanced economies and "it might take a bit longer for the turnaround in inflation to happen here than elsewhere."

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.43; (P) 108.65; (R1) 108.88; More...

USD/JPY's decline continues today and reaches as low as 107.41 so far. Intraday bias remains on the downside and break of 107.31 will target 106.48 fibonacci level. We'd look for strong support around there to bring rebound. However, on the upside, break of 108.80 minor resistance is needed to be the first sign of short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD/JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Domestic CGPI Y/Y Jan | 2.70% | 2.70% | 3.10% | 3.00% |

| 0:30 | AUD | NAB Business Conditions Jan | 10 | 12 | 13 | |

| 0:30 | AUD | NAB Business Confidence Jan | 12 | 10 | 11 | |

| 6:00 | JPY | Machine Tool Orders Y/Y Jan P | 48.80% | 48.30% | ||

| 8:15 | CHF | PPI M/M Jan | 0.30% | 0.20% | 0.20% | |

| 8:15 | CHF | PPI Y/Y Jan | 1.80% | 0.90% | 1.80% | |

| 9:30 | GBP | CPI M/M Jan | -0.50% | -0.60% | 0.40% | |

| 9:30 | GBP | CPI Y/Y Jan | 3.00% | 2.90% | 3.00% | |

| 9:30 | GBP | Core CPI Y/Y Jan | 2.70% | 2.60% | 2.50% | |

| 9:30 | GBP | RPI M/M Jan | -0.80% | -0.70% | 0.80% | |

| 9:30 | GBP | RPI Y/Y Jan | 4.00% | 4.10% | 4.10% | |

| 9:30 | GBP | PPI Input M/M Jan | 0.70% | 0.60% | 0.10% | |

| 9:30 | GBP | PPI Input Y/Y Jan | 4.70% | 4.10% | 4.90% | 5.40% |

| 9:30 | GBP | PPI Output M/M Jan | 0.10% | 0.20% | 0.40% | |

| 9:30 | GBP | PPI Output Y/Y Jan | 2.80% | 3.00% | 3.30% | |

| 9:30 | GBP | PPI Output Core M/M Jan | 0.30% | 0.20% | 0.30% | |

| 9:30 | GBP | PPI Output Core Y/Y Jan | 2.20% | 2.30% | 2.50% | 2.40% |

| 9:30 | GBP | House Price Index Y/Y Dec | 5.20% | 4.90% | 5.10% | 5.00% |

Dollar Slips On Banana Peel As Safe-Havens Cheer, European Stocks Lose Ground

Here are the latest developments in global markets:

FOREX: In currency markets, stronger-than-expected inflation figures in the UK justified the Bank of England’s potential plans to raise interest rates faster than expected, pushing pound/dollar towards a four-day high of 1.3923 (+0.49%). Pound/yen, though, recovered slightly to 149.62 but remained down on the day (-0.46%) as a rising yen weighed on the pair. Dollar/yen stretched down towards a new five-month trough of 107.41 (-0.97%) and dollar/swissie retreated to a one-week low of 0.9328 (-0.69%) as investors maintained their risk-averse mood amid recent volatility in stock markets, supporting safe-haven assets. Euro/dollar extended its uptrend towards 1.2349 (+0.44%) in the face of a falling dollar, however, a potentially fragile coalition deal in Germany and uncertainties around the upcoming Italian general elections in early March restricted further upside momentum. Dollar/loonie remained steady at 1.2577.

STOCKS: In Europe, stock markets were weaker as the two-day recovery in Wall Street equities could not convince investors that the recent turmoil in stock markets was fading. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were trading 0.10% and 0.22% lower at 1030 GMT, dragged by losses in telecommunications. The German DAX fell by 0.17%, the French CAC 40 declined by 0.22%, while the Spanish IBEX 35 and the Italian FTSE MIB retreated by 0.75%. The British FTSE 100 was flat, while US stock futures were in the red, pointing to a negative open.

COMMODITIES: Oil prices posted losses after the Paris-based International Energy Agency said in its monthly report on Tuesday that growth in the US production could outpace rises in demand in 2018. WTI crude and Brent were last seen at $58.98/barrel (-0.51%) and $62.45/barrel (-0.22%) respectively. In precious metals, gold extended upwards to touch a fresh one-week high at $1330.78/ounce (+0.42%).

Day ahead: API weekly oil report pending; Japanese flash GDP growth figures in the spotlight in Asia

The calendar will be light of economic releases during the European afternoon, with the American Petroleum Institute (API) publishing its weekly report on the US oil stocks later in the day at 2135 GMT.

However, Australian and Japanese economic releases scheduled for delivery in early Asian trading will be gathering greater attention.

At 2335 GMT, the Westpac Banking Corporation will give updates on the Australian consumer sentiment for the month of February, while a few minutes later at 2350 GMT, the Japanese Cabinet Office will release preliminary GDP growth readings for the final quarter of 2017. According to analysts, the Japanese economy is expected to expand at a slower pace in the aforementioned period, posting the lowest growth rate seen since the second quarter of 2016; though analysts expect the deceleration to be temporary. Particularly, the annualized GDP growth measure is anticipated to slow down to 0.9% after surging by 2.5% in the preceding quarter. On a quarterly basis, the gauge is said to ease by 0.4 percentage points to 0.2%, probably being dragged by a trimmed trade surplus. The consumption GDP growth component, though, is projected to positively contribute to GDP, in contrast to the preceding quarter.

Regarding today’s public appearances, the Cleveland Fed President, Loretta Mester, will be speaking on the US economic outlook at 1300 GMT. She holds voting rights within the FOMC in 2018.

In equities, the earnings season continues to gather attention, having the potential to affect market sentiment.

Sterling Flat Ahead Of UK Inflation Data

Sterling struggled for direction on Tuesday morning, as investors remained on the sidelines ahead the release of January's CPI inflation figures from the United Kingdom.

Today's pending consumer price index (CPI) readings could be a big deal, especially when considering how the British Pound remains sensitive to monetary policy speculation. Headline inflation is expected to fall for the second consecutive month to 2.9% YoY in January, from 3% in December, while core inflation is seen rising to 2.6% from 2.5% in December. Any signs of inflationary pressures easing could cool expectations of the Bank of England raising UK interest rates sooner than expected, consequently exposing Sterling to downside losses. However, an upside surprise in UK inflation figures may reinforce speculation of higher UK interest rates, ultimately supporting the Pound. While monetary policy speculation is likely to continue impacting Sterling, investors must not overlook Brexit developments and the uncertainty they present.

From a technical standpoint, the GBPUSD remains under noticeable pressure on the daily charts. Bears managed to secure a weekly close below the 1.3850 level, and as such could pave a path to further downside. Previous support at 1.3850 may transform into a dynamic resistance that encourages a decline lower towards 1.3700. Alternatively, a daily close back above 1.3850 may invite an incline towards 1.4000.

Global stocks continue to rebound

Investors seem to have entered the new trading week with a renewed appetite for risk, as global stocks rebounded from their worst week in two years on Monday.

Most Asian shares closed higher on Tuesday following Wall Street's solid rebound overnight. In Europe, equities are expected to open on a positive note, with the bullish domino effect potentially supporting Wall Street this afternoon. With global equity markets still highly sensitive to fears of rising inflationary pressures and higher interest rates, equity bears could still make an unwelcome appearance.

Commodity spotlight – Gold

Gold popped higher during Monday's trading session with prices rising towards $1329, thanks to a softening US Dollar. While Dollar weakness could in the short term offer the yellow metal further support, gains are likely to be limited by rising expectations of higher US interest rates. Focusing purely on the technical picture, the yellow metal remains under pressure on the daily charts. A failure for prices to keep above the $1324.15 level could inspire a decline towards $1300. Alternatively, if bulls are able to hold their ground above $1324.15, prices could venture towards $1340.

South African Rand weakens

The South African Rand dipped slightly lower against the Dollar, with the USDZAR up 0.09% following news overnight that President Jacob Zuma has refused to step down. It is now appearing that the ANC Party will formally request for Zuma to step down from his position, but news that he is still refusing to do so has weakened the Rand very marginally in early trade.

EURUSD – Bullish, Extends Recovery Higher

EURUSD - The pair closed higher on Monday and followed through higher on Tuesday. This has opened the door for more strength to occur. On the upside, resistance comes in at 1.2400 level with a cut through here opening the door for more upside towards the 1.2450 level. Further up, resistance lies at the 1.2500 level where a break will expose the 1.2550 level. Conversely, support lies at the 1.2300 level where a violation will aim at the 1.2250 level. A break of here will aim at the 1.2200 level. Below here will open the door for more weakness towards the 1.2150. All in all, EURUSD faces further recovery threats.