Sample Category Title

Japanese Economy Set To Extend Streak Of Expansion – Implications For BoJ?

Japanese preliminary Q4 2017 GDP growth figures will be made public on Tuesday at 2350 GMT. Economists expect the world’s third largest economy to post its eighth straight quarter of positive growth. A stronger-than-anticipated pace of growth could refuel market expectations for an exit from ultra-easy monetary policy by the Bank of Japan taking place sooner than earlier thought, boosting the yen versus other currencies.

Strong exports – foreign demand for Japanese products fueled by a recovering global economy – and domestic demand are prime contributors to the world’s third largest economy looking set to record its longest run of uninterrupted growth since a period between 1986-1989 when the economy grew for 12 consecutive quarters; though that period was linked to a bubble.

On an annualized and quarterly basis, the growth rate is projected to stand at 0.9% and 0.2% respectively, falling short of Q3’s respective figures of 2.5% and 0.6%. Analysts though, anticipate the expected slowdown to be non-persistent.

It is perhaps notable that capital expenditure is forecast to have increased for the fifth quarter in a row in Q4, supported by purchases of equipment to alleviate labor shortages as well as by robust demand from semiconductor makers. It is also perhaps interesting to mention that despite the anticipated strength in exports, forecasters project a trimmed-down trade surplus (exports minus imports) on the back of rising import costs from new-model smartphones and elevated oil prices.

In case of a data beat, dollar/yen is likely to head lower. This would especially hold true if the upside surprise delivered is large enough to incentivize forex market participants to push their expectations for policy tightening by the BoJ sooner in time. In this scenario, support could come around the 15-month low of 107.31 that was recorded on September 8. Momentum is negative at the moment for the pair (which is trading at five-month low levels), with a downside violation of the September low having the capacity to challenge the 107 handle, a level that may be of psychological importance.

On the upside and in case of a data miss, the area around 108 could act as barrier to price advancing. The range around this point encapsulated a few bottoms in the past and could be of significance. Further above, major resistance might come around the 110 handle, this being an area of congestion in the past.

Factors that have the capacity to affect Japan’s economic outlook are market fluctuations that could for example lead to a notably stronger yen and render exports relatively less attractive, a considerable deceleration in the Chinese economy, and tensions or an outright confrontation with North Korea. It should be mentioned however that the risk of conflict with North Korea has significantly eased lately (it was considered extremely low even before), with North and South Korea displaying a level unity not experienced in years as the 2018 Winter Olympics are taking place in PyeongChang, South Korea – though the two are still separated by significant differences. It remains to be seen whether positive momentum will be maintained and extended in bilateral relations between North Korea and other countries, such as Japan.

The next big release out of Japan will be December’s machinery orders, scheduled for release on Wednesday at 2350 GMT. Those are seen falling on a monthly basis, though analysts anticipate the fall to be temporary in nature.

USD Under Pressure As Traders Eye U.S Inflation

Tuesday February 13: Five things the markets are talking about

Euro equities are trading steady despite a late down swing in Asia, as investors wrestle to find direction after this month’s early collapse.

The dollar has weakened against G10 currency pairs while Treasuries have edged a tad higher along with gold. Crude is heading for its first advance in eight sessions.

Investors are looking to tomorrow’s U.S. consumer-price data for some clues on direction, given that pressure on stocks have been stemming from the outlook for inflation.

The market is expecting U.S consumer-price index to probably increase at a moderate pace last month along with U.S retail sales – both due out tomorrow.

Note: Lunar New Year celebrations for the Year of the Dog begin, affecting China, Hong Kong, Taiwan, Singapore, Malaysia and Indonesia. Chinese mainland markets are closed Feb. 15-21.

1. Stocks mixed review

In Japan, the Nikkei share average closed at a four-month low overnight as investors turned somewhat risk averse as the yen rallies outright. The Nikkei ended -0.7% lower, its lowest closing level in four months.

Down-under, Aussie shares tracked Wall St into positive territory. The S&P/ASX 200 index rose +0.6% at the close of trade, after a -0.3% yesterday. In S. Korea, the Kospi climbed +0.35%.

In Hong Kong, stocks rose overnight, tracking a global rebound, on bargain hunting. At close of trade, the Hang Seng index was up +1.29%, while the Hang Seng China Enterprises index rallied +0.88%.

In China, stocks rebounded, supported by investor sentiment aided by signs of government support and record bank lending last month. At the close, the Shanghai Composite index was up +1%, while the blue-chip CSI300 index was up +1.19%.

In Europe, regional indices trade mostly lower taking the lead from weaker U.S futures. The FTSE trades little changed following a slightly hotter CPI reading, as Gilt yields pare declines.

U.S stocks are set to open in the ‘red (-0.6%).

Indices: Stoxx600 -0.1% at 372.7, FTSE flat at 7173, DAX -0.1% at 12266, CAC-40 -0.1% at 5133, IBEX-35 -0.6% at 9708, FTSE MIB -0.5% at 22215, SMI -0.3% at 8799, S&P 500 Futures -0.6%

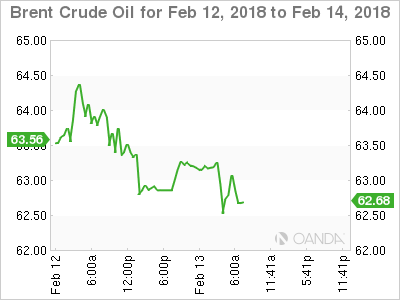

2. Oil prices firm on weaker dollar, gold higher

Oil prices are better bid, supported by a rebound in global equities, as well as by a weaker dollar, which potentially supports more fuel consumption.

Brent crude futures are at +$62.97 per barrel, up +38c, or +0.6% from Monday’s close. U.S West Texas Intermediate (WTI) crude futures are at +$59.60 a barrel, up +31c or +0.5% from yesterday’s settlement.

The stronger prices came after crude registered its biggest loss in two years last week as global stock markets slumped.

Nonetheless, rising U.S production continues to undermine the efforts led by the OPEC and Russia to tighten markets and prop up prices.

Note: U.S oil production has rallied above +10m bpd, overtaking top exporter Saudi Arabia and coming within reach of top producer Russia.

There are also strong signals the output will rally further. Data last Friday showed that U.S energy companies added 26 oilrigs looking for new production, boosting the count to +791, the highest since April 2015.

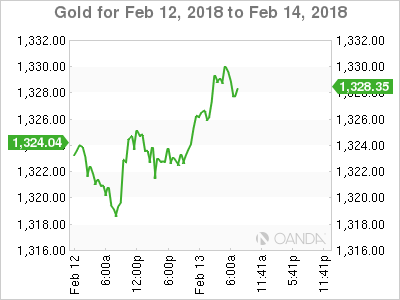

Gold prices have hit a one-week high overnight, aided by a weaker dollar and as the market awaits for tomorrow’s U.S inflation data for clues on the pace of interest rate hikes. Spot gold is up +0.4% at +$1,327.81 an ounce.

Note: Yesterday, the yellow metal rose +0.5%, its biggest single-day percentage gain in more than one week.

3. Sovereign yields fall

G7 sovereign bond yields look attractive across the curve after yields rallied on a recovering global economy and on expectations central banks will tighten policy faster than previously thought.

With the lack of economic market news the fixed income market looks attractive and reason why yields fell in the overnight session.

The yield on U.S 10-year Treasuries fell -3 bps to +2.83%, the biggest drop in more than a week. In Germany, the 10-year Bund yield declined -2 bps to +0.74%, the lowest in a week, while in the U.K the 10-year Gilt yield has dipped -1 bps to +1.601% despite the higher inflation print (see below).

4. Sterling reaction muted

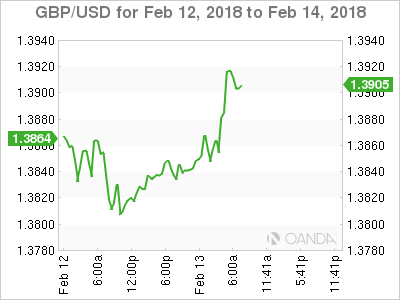

The pound (£1.3896) has edged a tad higher after U.K January annual inflation unexpectedly remained at +3% (see below) as worries about the U.K. getting a transitional deal after breaking up from the E.U persist. EUR/GBP trades down -0.1% at €0.8868. Although the high inflation number will add to expectations for another BoE hike, futures prices would suggest that the market has priced in two rate increases for the next 12-months.

Note: PM Theresa May’s government will aim to address the Brexit transition in a series of six speeches by the prime minister and other senior ministers in the next few weeks, which her office dubbed “The Road to Brexit.” May’s first speech is to be delivered at a conference in Munich next Saturday, while Foreign minister Boris Johnson will begin the series with a speech tomorrow.

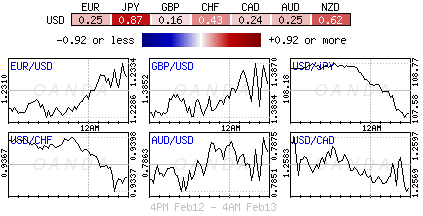

Elsewhere, the USD is modestly lower as President Trump’s proposed budget brings into focus the U.S twin deficits. The EUR/USD (€1.2337) is higher by +0.2%, while USD/JPY (¥107.55) is lower by -0.9% as fixed income dealers ponder the limits of an expansionary BoJ policy.

5. U.K inflation above target in January

Data this morning showed that U.K consumer prices rose +3% y/y in January. This headline print suggests that the Bank of England (BoE) case for higher borrowing costs is somewhat justified to bring borrowing costs back to its +2% annual goal.

The ONS said that the price gains were driven by clothing, footwear and recreational goods and services, especially tickets for zoos and gardens.

Note: Market consensus was expecting annual inflation in January to slow to +2.9%, from +3% m/m.

U.K Inflation has been above the BoE’s +2% annual target for 12-consecutive months. Last week the BoE said that they expected to raise interest rates at a swifter pace than they anticipated last year to contain growth in prices.

Note: The BoE raised its benchmark rate for the first time in a decade in November, to +0.5%. Futures prices suggest that the central bank will lift it again as soon as May.

and a willingness to intervene in currency markets.

Technical Outlook: GBPUSD – Inflation Overshoot Inflates Pound But Concerns About Brexit Persist

Cable rose to new session high at 1.3924 after data showed UK inflation unexpectedly rose in January (3.0% vs 2.9% f/c) remaining close to six-year high at 3.1%.

Near-term sentiment improves further as strong inflation numbers support hawks who advocate for BoE rate hike in May and counting one more hike in 2018.

Strong inflation data in January backed BoE’s hawkish hold last week, keeping positive interest rate outlook.

However, strong expectations that BoE will act in May could be overshadowed by persisting Brexit concerns, as BoE MPC member McCafferty pointed at Brexit in his speech on Monday, saying that central bank’s rate outlook could be tested by Brexit.

Next round of Brexit talks starts on 26 Feb and would provide more clues about monetary policy outlook.

Sterling holds positive near-term tone against the greenback and extends recovery from 1.3764 (three-week low, posted on 09 Feb), which needs close above next pivot at 1.3960 (Fibo 38.2% of 1.4277/1.3764 bear-leg) to generate fresh bullish signal and open way for recovery extension towards 1.40 zone.

Res: 1.3924, 1.3960, 1.4000, 1.4021

Sup: 1.3885, 1.3832, 1.3796, 1.3764

Recovery Continues For Equity Markets | UK CPI Under Focus

Traders supporting the markets with more buying pressure

The US bond yields have not reacted to the new spending news yet

Bank of England's policymaker Gertjan Vlieghe thinks that the UK's economy is ready for higher rates

UK's CPI number has a special importance

After suffering from it's worst week in nearly two years, traders over at Wall Street have decided that they are behind the recovery now. We have seen another stellar day for the US stock market yesterday as investors rushed to buy stocks at a better price. The message is same over in Europe, traders supporting the markets with more buying pressure and this is helping the European indices to recover from their recent heavy losses.

Overall, the European markets and US future are looking strong today with the help of a strong positive momentum and thanks to the stabilising sentiment among bond traders.

Remember the sell-off was triggered due to the qualm around higher inflation. The tax cuts which Trump administration brought in the sunlight has fuelled worries amid investors that inflation would be running hot. Ironically enough though we had no such concerns when this process started and now in a matter of weeks, inflation became the very reason for the sell-off which we experienced.

President Trump announced his massive infrastructure plans yesterday. You could argue that the Federal spending of $200 billion is not something which is going to fuel any further rout in the bond yields. But here is the fact, that the US is running a large number when it comes to the deficit and with more federal spending, it only means more bond issuance. The US bond yields have not reacted to the new spending news yet, but the odds of such an event to take place have certainly skewed to the upside in our opinion. The White House indicated over the weekend that the path of the US interest rate hike could steepen further if there is any need. This means that if the Fed sees that the market is thinking that the Fed needs to take action to tackle inflation, the bank would take all necessary steps to address that. The White House statement pushed the US 10 bond yield towards 2.9% but we are off from that level again. Perhaps, need another announcement.

Back in the UK, the Bank of England's policymaker Gertjan Vlieghe thinks that the UK's economy is ready for higher rates, not sure on what basis he thinks this or if he is looking through a different lens. Nonetheless, his comments have increased the importance of the upcoming data because any positive reading would mean that the odds are moving in Vlieghe's favour. Today's UK's CPI number has a special importance. The expectations are; we would witness the CPI number losing some of it's steam after touching its peak 3.1%. The forecast for the number is 2.9% while the previous reading was at 3.0%.

However, if the inflation number does start to tick higher again, it would increase the pressure on the BOE to tweak it's monetary policy. This means another increase in the interest rate and that would not be a welcoming sign for the UK's economy. The BOE's governor has indicated and has prepared the market to some extent that inflation could tick higher which is a big change in his earlier stance. The only safety net for the BoE could hope for is the bounciness in the wages and the wages should continue to show the same sort of resilience as they have over in the US.

GBP/CHF 4H Chart: Trading Along Channel

The Pound Sterling has been constrained by a descending channel against the Swiss Franc after hitting the weekly pivot point near 1.3515. The upper boundary of a junior channel was reached on January 25.

The Sterling's inability to make a new wave up suggests that it might breach the dominant channel in the next few hours.

Technical indicators flash bearish signals during the following trading sessions; therefore, the currency exchange rate is likely to decline further until it finds support at the monthly and weekly PPs near the 1.2888 mark.

EUR/CHF 4H Chart: Possible Reverse

After approaching the upper boundary of a dominant channel down , the Euro began depreciating against the Swiss Franc.

The EUR/CHF pair is gradually moving upwards to test the upper boundary of the junior pattern.

In general, two scenarios are likely during the following trading sessions. First, the currency pair might breach the upper boundary of the junior pattern, but this surge could be stopped by a resistance cluster near 1.1620. Second, the rate could reverse from 1.1534 to re-test the lower boundary of the dominant channel.

EUR/USD Analysis: Poised For 1.24

The Euro was driven by upside risks on Monday. Even though the norhtern side was guarded by a strong resistance cluster formed by the 55– and 100-hour SMAs and the weekly and monthly PPs, the pair managed to gather enough momentum to push through this barrier and thus move away from the bottom boundary of a four-month channel up.

The same bullish momentum is likely to prevail during the following hours, as well. It is expected that gains are capped near the 1.24 mark where the upper boundary of a short-term channel down is located. Further upward movement is unlikely, given that this area is likewise reinforced by the 200-hour SMA.

In terms of support, a possible fall should be restricted by the 55– and 100-hour moving averages cica 1.2270.

GBP/USD Analysis: Re-Tests 1.39 Area

Lack of fundamantal events on Monday resulted in the Pound moving sideways against the US Dollar. The pair tried to push higher during the day; however, the strong resistance of the 55– and 100-hour SMAs restricted any advances.

It is likely that the Pound tries to move past this resistance area once again in this session. A possible bullish push could be provided by the British CPI data to be released at 0930GMT.

In case this cluster is surpassed, the Pound is expected to appreciate up to the 1.40 mark where the 200-hour SMA and and the monthly PP are located. A further advance is unlikely, as the pair was unable to breach this psychological level last week.

Meanwhile, losses should be restricted by the weekly and monthly S1s near 1.37.

USD/JPY Analysis: Plunges Early On Tuesday

The US Dollar remained steady against the Japanese Yen on Monday, as it was trading in a narrow 108.70/50 range.

This lack of direction changed rapidly during the Asian session when the Greenback plunged 85 pips within a couple of hours down to the weekly S1 near 108.00. In case this massive fall continues, losses should be limited by the monthly S1 located at 107.20.

This strongly bearish sentiment during the first part of the day has sent technical indicators in the oversold area. Thus, it is likely that bulls use this opportunity to re-gain some of their lost positions. This expected advance should be limited by the 55– and 100-hour moving averages and the weekly PP circa 109.00.

XAU/USD Analysis: Trades Between SMAs

The yellow metal was stranded between the bounds of the 55– and 100-hour SMAs during the first part of Monday. A strong hourly surged mid-session allowed XAU/USD to breach the latter and move towards the 200-hour SMA and the upper boundary of a three-week channel down circa 1,330.00.

However, the pair's movement after breaching the line has been sideways, thus suggesting that it might not be able to overcome its nearest resistance. In addition, the formation of a minor rising wedge should result in a southern breakout. This bearish move should not be long-lived, as the rate is supported by the 55– and 100-hour SMAs at 1,320.00.

Gold should subsequently edge higher and try to re-test the 1,330.00 area. Gains should be capped at the 23.60% Fibo and the monthly PP at 1,335.60.