Sample Category Title

DAX Gains Ground On German, Eurozone Growth

The DAX index has posted losses in the Tuesday session. Currently, the index is trading at 12,277.50, up 0.67% since the Monday close. In Germany, Preliminary GDP slowed in the fourth quarter to 0.6%, but still matched the estimate. Final CPI declined 0.7%, also matching the forecast. Eurozone Flash GDP for Q4 remained steady at 0.6% for a third straight quarter, matching the estimate. In the US, the markets are expecting mixed inflation numbers. Core CPI is expected to expected to edge lower to 0.2%, while CPI is forecast to improve to 0.1%.

European markets have given a thumbs-up to German and Eurozone GDP reports. Both indicators showed respectable gains of 0.6% in the fourth quarter. On an annual basis, Eurozone GDP was up by 2.7%, underscoring the strong rebound in the eurozone economy in 2017. The DAX is marginally higher last week, after sliding 7.6% last week. In the banking sector, stocks are in green territory on Wednesday. Commerzbank has posted strong gains of 1.24%, and Deutsche Bank has gained 0.24%.

Investors across the globe, who endured a massive sell-off last week, will be keeping a close eye on US inflation indicators. Concern over higher inflation and additional rate hikes was a catalyst to the volatility in the stock markets, and any whiff of higher consumer inflation could again spook investors and send the markets into a tailspin. The new head of the Federal Reserve, Jerome Powell, sought to send a reassuring message on Tuesday, saying that the Fed is on alert to any risks to financial stability. However, it is clear that the Fed’s hand is limited when it comes to stock markets moves, and the volatility which we saw last week could resume at any time.

Will It Be A Valentines Day Massacre For The Dollar?

Wednesday February 14: Five things the markets are talking about

Are financial markets justified going from a growth story to an inflation narrative?

Today's U.S consumer price index (08:30 am) is being touted as one of the most significant economic releases in a number of years as capital markets seek to understand the recent plunges in global equities and sovereign bonds.

With investors already on edge, they are expected to renew this months convulsion on any sign that U.S inflation is exceeding expectations at a rate that may entice the Fed to quicken its plans for tightening monetary policy.

Already this month, after a stronger U.S non-farm payroll (NFP) print and wage numbers, investors have sent U.S Treasury yields aggressively higher and instigated a rout in equities that pushed them into the first correction in 18-months.

Note: Market expectations are looking for the core-CPI (ex-food and energy) to rise +1.7% in January y/y compared with the +1.8% increase in December. U.S retail sales are also out this morning and are expected to have increased for a fifth consecutive month.

A higher CPI will give the USD strength, lead to higher yields and lower equity prices, but a tepid headline print could cause more of a problem, especially with record short U.S 10-year treasury position and a market focusing on President Trump's proposed budget and the rise in U.S twin deficits.

Note: Lunar New Year celebrations for the Year of the Dog begin, affecting China, Hong Kong, Taiwan, Singapore, Malaysia and Indonesia. Chinese mainland markets are closed Feb. 15-21.

1. Stocks mixed reaction

In Japan, the Nikkei share average dropped to a fresh four-month low overnight as investor sentiment was again sapped by worries about U.S inflation data due this morning. The Nikkei ended -0.4% lower, its lowest closing since early October. The broader Topix fell -0.8%.

Down-under, the Aussie S&P/ASX 200 index fell -0.3%, following a +0.6% rise on Tuesday. In S. Korea the Kospi closed out the overnight session up +1.1%, helped by a +3% jump in Samsung.

In Hong Kong, shares rebound sharply ahead of Lunar New Year holiday. Trading will resume on Feb 20. At close of trade, the Hang Seng index was up +2.27%, while the Hang Seng China Enterprises index rose +2.14%.

In China, stocks rebounded overnight, but volumes were thin, as many traders had already left for the weeklong Lunar New Year holiday. Chinese markets will reopen on Feb. 22. At the close, the Shanghai Composite index was up + 0.46%, while the blue-chip CSI300 index was up +0.8%.

In Europe, regional indices trade higher across the board following a rebound in Wall Street yesterday and strength in U.S futures this morning.

U.S stocks are set to open in the black (+0.4%).

Indices: Stoxx600 +0.7% at 373.2, FTSE +0.7% at 7216, DAX +0.7% at 12286, CAC-40 +0.6% at 5139, IBEX-35 +0.5% at 9693, FTSE MIB +0.2% at 22071, SMI +0.9% at 8832, S&P 500 Futures -+0.4%

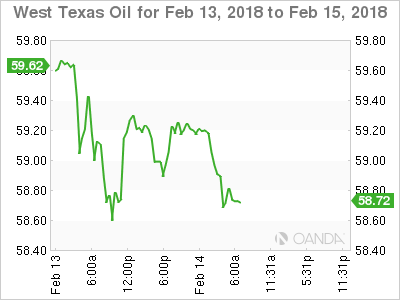

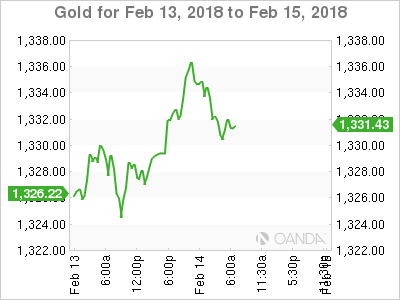

2. Oil dips on looming oversupply and weak U.S dollar, gold higher

Oil prices have dipped overnight, pressured by lingering oversupply including rising U.S inventories. However, the prospect of Saudi output dropping next month, economic growth hopes and a weaker U.S dollar all combined to limit losses.

Brent crude futures are at +$62.68 per barrel, down -4c. Brent was above +$70 a barrel earlier this month. U.S West Texas Intermediate crude futures are at +$59.06 a barrel, down -13c from yesterday's close. WTI was trading above +$65 in early February.

On Wednesday, the Saudi energy ministry said that Saudi Aramco's crude output in March would be -100k bpd below this month's level while exports would be kept below +7m bpd.

Stateside, yesterday's API report showed that U.S crude inventories rose by +3.9m barrels in the week to Feb. 9, to +422.4m.

Note: That is due to soaring U.S crude production, which has jumped by over +20% since mid-2016 to more than +10m bpd, surpassing that of top exporter Saudi Arabia and coming within reach of Russia, the world's biggest producer.

Oil traders will take their cue from today's EIA print (10:30 am EDT) and U.S inflation release.

Ahead of the U.S open, gold prices have rallied for a third consecutive session overnight to hit a one-week high, buoyed by a weaker U.S dollar, while the market awaits U.S inflation data for clues on the pace of future Fed rate increases. Spot gold is up +0.3% at +$1,332 an ounce.

3. Sovereign yields little changed

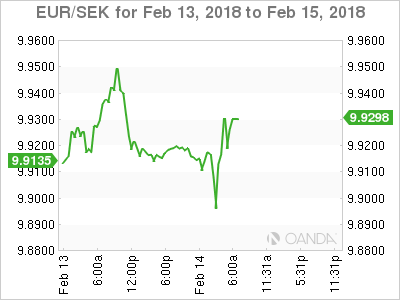

Earlier this morning, Sweden's Central Bank (Riksbank) kept their repo rate unchanged at -0.5%. Deputy governor Henry Ohlsson voted to raise rates, but the central bank's signals on inflation were more downbeat. The inflation forecast for this year was downgraded to +1.8% from +2%. The statement indicated that policy makers would start raising the rate in H2 of 2018. Policy makers stressed that was important not to raise the rate too early and was committed to stimulus to prevent inflation setbacks.

Elsewhere, fixed income seeks guidance from today's U.S CPI release. The yield on U.S 10-year Treasuries fell less than -1 bps to +2.83%. In Germany, the 10-year Bund yield declined -2 bps to +0.74%, while in the U.K, the 10-year Gilt yield dipped -1 bps to +1.618%. In Japan, the 10-year JGB yield decreased -1 bps to +0.07%, the lowest in more than five weeks.

4. Dollar on soft footing

The USD remains on soft footing ahead of key Jan CPI data for the U.S.

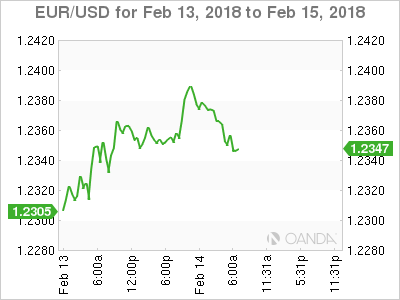

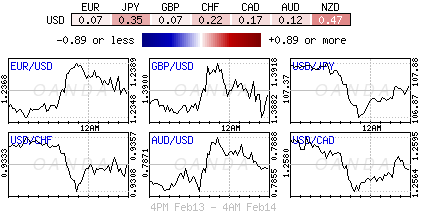

The EUR/USD is steady, trading atop of the €1.2350 area after various European GDP data highlighted better economic growth prospects (see below).

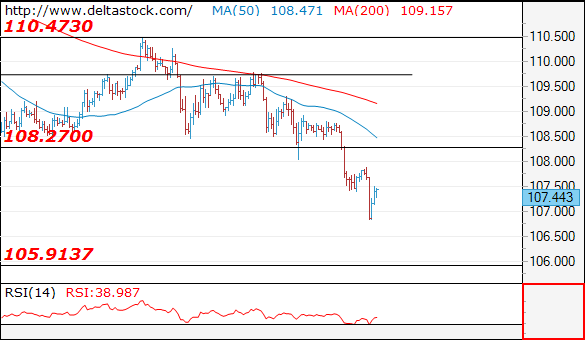

USD/JPY tested ¥106.85 overnight for 15-month lows. The pair came off its worst level to approach 107.50 just ahead of the N.Y session after Japanese officials reiterated that they had no comments on forex levels.

In S. Africa, political optimism that President Zuma would resign has sent the ZAR currency to its best level in nearly two-years outright. The South African Democratic Alliance (DA) leader Maimane (opposition) has stated that its motion to dissolve parliament was processed by Speaker. USD/ZAR is at $11.85 ahead of the open stateside.

The Swedish krona has been volatile after the Riksbank interest rate decision. The krona briefly rose soon after the announcement, but has since pared those gains EUR/SEK last trades flat on the day at €9.9163, compared with €9.8952 before the decision.

5. Euro-zone economy ends 2017 on a high note

Note: There were a number of European GDP releases in the Euro session highlighting better economic growth prospects – Germany mixed; Netherlands beat and Italy a miss.

Industry helped drive the euro-zone's +0.6% expansion in Q4. This morning's ‘flash' estimate of Q4 GDP is the second release and confirms that quarterly growth slowed a tad from Q3's +0.7% to +0.6%.

There is no breakdown until the next release; however, expenditure evidence would suggest that weaker consumer spending growth was the main driver of the slowdown, while investment expanded after Q3's contraction and net trade again made a positive contribution to growth.

Digging deeper, industry appears to have made a stronger contribution to GDP growth than in Q3. Following the consensus-beating +0.4% monthly rise in IP in December.

Euro Unchanged As German GDP, CPI Matches Forecasts

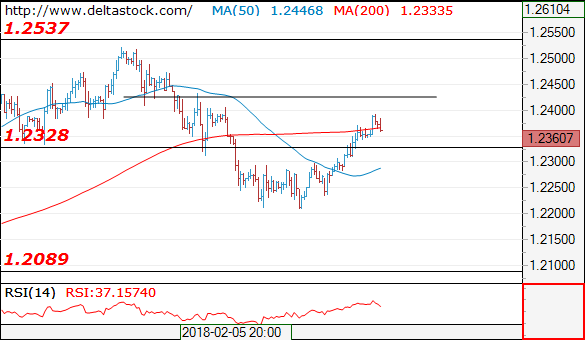

The euro has shown some movement in both directions but is unchanged in the Wednesday session. Currently, the pair is trading at 1.2356, up 0.04% on the day. It’s a busy day for fundamentals, with key releases out of the eurozone and the US. In Germany, Preliminary GDP slowed to 0.6% in the fourth quarter, matching the estimate. Final CPI declined 0.7%, also matching the forecast. Eurozone Flash GDP for Q4 remained steady at 0.6% for a third straight quarter, matching the estimate. In the US, the markets are expecting mixed inflation numbers. Core CPI is expected to expected to edge lower to 0.2%, while CPI is forecast to improve to 0.1%. The US will also release retail sales reports. Retail Sales is forecast to slow to 0.2%, while Core CPI is forecast to accelerate to 0.5%. Traders should be prepared for movement from EUR/USD during the North American session.

The stock market sell-off has triggered some volatility in the currency markets, and this is causing concern at the ECB. Last week, ECB President Mario Draghi said that he is more confident that eurozone inflation is moving closer to the Bank’s target of just below 2 percent, due to improving economic growth. However, Draghi listed currency market volatility as an obstacle to the inflation target, and added that the ECB would carefully monitor the euro’s exchange rates. Draghi’s concerns about the exchange rate are likely even stronger, after the euro fell 1.6 percent last week. The ECB tapered its massive stimulus program from EUR 60 billion to 30 billion/mth in January, and the markets are on the lookout for hints as to whether the ECB will normalize policy and wind up stimulus in September.

Global stock markets have steadied after last week’s turbulence, but investors remain wary. Wednesday’s US inflation numbers will be closely watched, as inflation fears was a key catalyst of the massive sell-off. The new head of the Federal Reserve, Jerome Powell, sought to send a reassuring message on Tuesday, saying that the Fed is on alert to any risks to financial stability. However, it is clear that the Fed’s hand is limited when it comes to stock markets moves, and the volatility which we saw last week could resume at any time.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.2360

The intraday bias is positive above 1.2330, with a risk of another leg upwards, to 1.2435 zone. The latter should cap the upside for a renewal of the general slide towards 1.2090.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2435 | 1.2540 | 1.2330 | 1.2160 |

| 1.2540 | 1.2870 | 1.2210 | 1.2090 |

USD/JPY

Current level - 107.44

Current rebound after 106.83 low is corrective in nature, thus preceding another leg downwards, to 105.90 zone. Key resistance is projected around 108.00-25.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 108.30 | 111.90 | 106.85 | 105.90 |

| 109.70 | 113.40 | 105.90 | 105.90 |

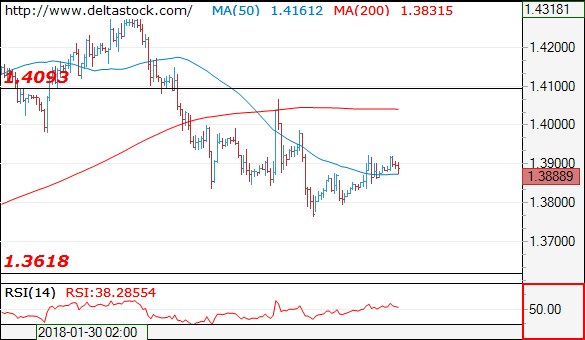

GBP/USD

Current level - 1.3889

Intraday allow a brief bounce to 1.3990 area, before drowning towards 1.3760 low, en route to 1.3620 zone.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3900 | 1.4090 | 1.3800 | 1.3730 |

| 1.3985 | 1.4174 | 1.3620 | 1.3620 |

Market Update – European Session: Focus On US CPI Data

Notes/Observations

Highly anticipated US CPI report being focal point of the week for investors and markets

Signs of stability in USTs and Bunds

Various European GDP releases in session highlighting better economic growth prospects (Germany mixed; Netherlands beat; Italy miss

Sweden Central Bank keeps policy steady and saw slow rate hikes initiated in 2nd half of 2018

Asia:

Japan Q4 Preliminary GDP data missed expectations but still registered its 8th consecutive quarter of growth (Q/Q: 0.1% v 0.2%e Annualized GDP Q/Q: 0.5% v 1.0%e)

Japan Economy Min Motegi: 'Virtuous economic cycle' starting to take hold with pick-up in private consumption (confirmed GDP grew for 8 quarters for the first time in 28 years)

New Zealand 1-Year Inflation Expectation Survey: 1.86% v 1.87% prior; 2-Year Inflation Expectations at 2.1% v 2.0% prior

China PBoC again skipped its Open Market Operation(OMO) for the 16th straight session

(SG) Monetary Authority of Singapore (MAS): Monetary policy stance remained unchanged; had not revised core or headline CPI forecasts since Oct

Europe:

Germany SPD Leader Schulz stepped down as party chairman (as speculated). Scheduled a SPD special party convention for April 22nd. Andrea Nahles nominated as SDP chair by executive board. Hamburg Mayor Scholz to take over as acting leader of Germany’s SPD party

France President Macron: in Europe's interest that Barnier remained EU's only Brexit negotiator

Israeli police said to find sufficient evidence to indict PM Netanyahu on corruption charges

Americas:

President Trump: reviewing all options over Sec 232 trade probe on steel and aluminum; looking at tariffs and/or quotas on steel and aluminum imports

Fed Chair Powell stated that Fed will remain alert to any financial stability risks

White House said to be considering nominating current head of Cleveland Fed’s Loretta Mester as Vice Chair of Federal Reserve Board

Canada NAFTA negotiator: NAFTA talks I've been a part of are 'most unusual'; had seen fairly limited progress overall but quite close to completing some chapters, including customs and telecom

Energy:

Weekly API Oil Inventories: Crude: +3.9M v -1.1M prior

Economic Data:

(SE) Sweden Jan Maklarstatistik Housing Prices Y/Y: -1.0% v -2.0% prior; Apartment Prices Y/Y: -4.0% v -3.0% prior

(DE) Germany Q4 Preliminary GDP Q/Q: 0.6% v 0.6%e; Y/Y: 2.9% v 3.0%e; GDP NSA Y/Y: 2.3% v 2.2%e

(DE) Germany Jan Final CPI M/M: -0.7% v -0.7%e; Y/Y: 1.6% v 1.6%e

(DE) Germany Jan Final CPI EU Harmonized M/M: -0.7% v -1.0%e; Y/Y: 1.4% v 1.4%e

(RO) Romania Jan CPI M/M: 0.8% v 0.5%e; Y/Y: 4.3% v 3.9%e

(RO) Romania Q4 Advance GDP Q/Q: 0.6% v 1.2%e; Y/Y: 6.9% v 7.3%e

(FI) Finland Dec GDP Indicator WDA Y/Y: 3.6% v 4.3% prior

(FI) Finland Dec Final Retail Sales Volume Y/Y: 3.0% v 3.5% prelim

(TR) Turkey Dec Current Account Balance: -$7.7B v -$7.5Be

(TH) Thailand Central Bank (BOT) left Benchmark Interest Rate unchanged at 1.50% (as expected)

(CZ) Czech Jan CPI M/M: 0.6% v 0.7%e; Y/Y: 2.2% v 2.2%e

(HU) Hungary Q4 Preliminary GDP Q/Q: 1.3% v 1.1%e; Y/Y: 4.4% v 4.3%e

(SE) Sweden Central Bank (Riksbank) left Repo Rate unchanged at -0.50% (as expected); maintained its repo rate path outlook

(NL) Netherlands Q4 Preliminary GDP Q/Q: 0.8% v 0.7%e; Y/Y: 2.9% v 3.2%e

(NL) Netherlands Dec Trade Balance: €4.1B v €5.9B prior

(IT) Italy Q4 Preliminary GDP Q/Q: 0.3% v 0.4%e; Y/Y: 1.6% v 1.7%e

(PL) Poland Q4 Preliminary GDP Q/Q: 1.0% v 1.2%e; Y/Y: 5.1% v 5.2%e

(PT) Portugal Q4 Preliminary GDP Q/Q: 0.7% v 0.6%e; Y/Y: 2.4% v 2.3%e

(EU) Euro Zone Q4 Preliminary GDP (2nd reading) Q/Q: 0.6% v 0.6%e; Y/Y: 2.7% v 2.7%e

(EU) Euro Zone Dec Industrial Production M/M: 0.4% v 0.1%e; Y/Y: 5.2% v 4.2%e

Fixed Income Issuance:

(IN) India sold total INR140B vs. INR140B indicated in 3-month, 6-month and 12-month bills

(DK) Denmark sold DKK4.0B in 3-month Bills; Yield: -0.660% v -0.690% prior; bid-to-cover: 1.73x v 1.25x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.7% at 373.2, FTSE +0.7% at 7216, DAX +0.7% at 12286, CAC-40 +0.6% at 5139 , IBEX-35 +0.5% at 9693, FTSE MIB +0.2% at 22071 , SMI +0.9% at 8832, S&P 500 Futures -+0.4%]

Market Focal Points/Key Themes: European Indices trade higher across the board following a rebound in Wallstreet overnight and strength in futures this morning. Earnings picked up this morning with large financial names Credit Agricole and Credit Suisse reporting results, the latter trades higher on improved outlook. Plus500 outperforms after strong results and raising outlook, while Rexel trades over 7% higher following earnings. To the downside Galliford Try is a sharp decliner after announcing a capital raise alongside results, while ThyssenKrupp trades lower after mixed Q1 results. Looking ahead notable earners include Bunge, Groupon and Shire Pharma.

Movers

Materials [DSM [DSM.NL] +4.1% (Earnings), Boliden [BOL.SE] +3.3% (Earnings), ThyssenKrupp [TKA.DE] -1%(Earnings), Claraint [CLN.CH} -1% (Earnings)

Technology [ Rexel [RXL.FR] +9.0%(Earnings)]

Financials [Credit Suisse [CSGN.CH] +3.2% (Earnings), Plus 500 [PLUS.UK] +6% (Earnings), Credit Agricole [ACA.FR] -2.6% (Earnings), Hargreaves Services [HSP.UK] -2.5%(Earnings), Natixis [KN.FR] +1.1% (Earnings)]

Real Estate [Galifrod Try [GFRD.UK] -19%(Earnings, Capital raise)]

Speakers

Sweden Central Bank (Riksbank) policy statement noted that the prior Dec staff forecasts for the repo rate path was unchanged and indicated that slow repo rate rises were set to be initiated during the second half of this year. Stressed that was important not to raise the rate too early and was committed to stimulus to prevent inflation setback. Inflation forecast revised down slightly, primarily for 2018. From 2019 onwards, inflation was expected to be close to 2 per cent in 2019. Dep Gov Ohlsson did advocate a 25bps rate hike to -0.25%

Sweden Central Bank (Riksbank) Jansson post rate decision press conference: Short-term inflation forecast was down a bit and needed to secure that inflation development continued

ECB: Brexit banks should have trading and hedging capacity in the EU

SNB's Zurbrugg: Not planning to issue any digital currency

Swiss govt: No additional taxes for systemically important banks

BOE Agents summary of business conditions: Growth in activity had held steady at a modest pace; pay growth had picked up

IMF: Brexit uncertainty will continue to weigh on UK growth

South Africa Parliament: Democratic Alliance (DA) leader Maimane (opposition): Motion to dissolve Parliament processed by Speaker

Israel PM Netanyahu: Coalition govt was stable; no plans for early election (***Reminder: Reports circulated that Israeli police had sufficient evidence to indict PM Netanyahu on corruption charges)

Thailand Central Bank policy statement noted that the decision to keep policy steady was unanimous. Reiterated view that monetary policy remained accommodative and ready to use policy to aid growth and stability. Inflation seen back into target in Q2 (**Note: YoY has been below the lower end of the 1.0-4.0% target range) while the growth outlook had improved further. Reiterated to closely monitor THB currency (Baht) price movements

China PBoC Q4 Monetary Policy Implementation Report reiterated pledge to maintain prudent and neutral monetary policy; to strengthening the fine-tuning of policy through the use of many tools

Currencies

USD was on soft footing ahead of key Jan CPI data for the US.

EUR/USD was steady at 1.2350 area as various European GDP data highlighted better economic growth prospects.

USD/JPY tested 106.85 overnight for 15-month lows. The pair came off its worst level to approach 107.50 just ahead of the NY session. Japanese officials reiterated that had no comments on forex levels

EUR/SEK moved off its worst levels in the after math of the Riksbank decision to keep its policy steady. The Staff forecasts cut its inflation outlook for the horizon period. Soma analyst still saw the 1st Riksbank rate hike in 2019 despite the central bank statement that hikes could occur in H2 2018. EUR/SEK at 9.9250 just ahead of the NY morning.

Political optimism that South Africa President Zuma would resign sent the ZAR currency to its best level since May 2015. South Africa: Democratic Alliance (DA) leader Maimane (opposition) stated that it motion to dissolve Parliament was processed by Speaker. USD/ZAR at 11.85 just ahead of the NY morning.

Fixed Income

Bund Futures trades up 2 ticks at 158.25 as futures gain on weak volumes. Upside targets 158.85, while a continued move lower targets the157.25 level.

Gilt futures trade at 121.07 up 9 ticks as the bearish trend remains intact. Support continues to stand at 120.75 then 120.15, with upside resistance at 122.75 then 123.25.

Wednesday's liquidity report showed Tuesday's excess liquidity rose to €1.896T from €1.891T prior. Use of the marginal lending facility unchanged at €13M from €13M prior.

Corporate issuance saw 3 issuers raise $2.3B in the primary market

Looking Ahead

(PT) Bank of Portugal Reports Jan ECB financing to Portuguese Banks: No est v €22.4B prior

(NG) Nigeria Jan CPI Y/Y: 15.1%e v 15.4% prior

(AR) Argentina Central Bank (BCRA) Interest Rate Decision: Expected to leave 7-Day Repo Reference Rate unchanged at 27.25%

05:30 (DE) Germany to sell €1.5B in 2.5% July 2044 Bunds

05:30 (PT) Portugal Debt Agency (IGCP) to sell €1.0-1.25B in 2022 and 2028 bonds

06:00 (IE) Ireland Dec Property Prices M/M: No est v 1.1% prior; Y/Y: No est v 11.6% prior

06:00 (PT) Portugal Q4 Labour Costs Y/Y: No est v -1.1% prior

06:00 (ZA) South Africa Dec Retail Sales M/M: -0.1%e v +4.0% prior; Y/Y: 4.9%e v 8.2% prior

06:00 (RU) Russia to sell combined RUB44.3B in 2024 and 2033 OFZ Bonds

06:30 (CL) Chile Central Bank Traders Survey

06:45 (US) Daily Libor Fixing

07:00 (US) MBA Mortgage Applications w/e Feb 9th: No est v 0.7% prior

07:00 (CZ) Czech Central Bank to comment on CPI data

08:00 (HU) Hungary Central Bank (NBH) Jan Minutes

08:00 (RO) Romania Central Bank (NBR) Jan Minutes

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Jan CPI M/M: 0.3%e v 0.1% prior; Y/Y: 1.9%e v 2.1% prior

08:30 (US) Jan CPI Ex Food and Energy M/M: 0.2%e v 0.3% prior; Y/Y: 1.7%e v 1.8% prior

08:30 (US) Jan CPI Index NSA: 247.599e v 246.524 prior; CPI Core Index : No est v 254.426 prior

08:30 (US) Jan Advance Retail Sales M/M: 0.2%e v 0.4% prior; Retail Sales Ex Auto M/M: 0.5%e v 0.4% prior, Retail Sales Ex Auto and Gas: 0.3%e v 0.4% prior, Retail Sales Control Group: 0.4%e v 0.3% prior

08:30 (US) Jan Real Avg Weekly Earnings Y/Y: No est v 0.9% prior (revised from 0.7%); Real Avg Hourly Earning Y/Y: No est v 0.6% prior (revised from 0.4%)

08:30 (CA) Canada Jan Teranet/National Bank HPI M/M: No est v 0.2% prior; Y/Y: No est v 9.1% prior, HPI Index: No est v 217.49 prior

09:00 (BR) Brazil Central Bank Weekly Economists Survey

10:00 (US) Dec Business Inventories: 0.3%e v 0.4% prior

10:00 (CO) Colombia Dec Trade Balance: +$0.3Be v -$0.8B prior; Total Imports: $3.8Be v $4.0B prior

10:00 (CO) Colombia Dec Industrial Production Y/Y: -2.3%e v +0.3% prior

10:00 (CO) Colombia Dec Retail Sales Y/Y: -1.6%e v -1.2% prior

10:00 (US) Treasury Sec Mnuchin before House Ways & Means Committee on budget

10:30 (US) Weekly DOE Crude Oil Inventories

12:00 (CA) Canada to sell 5-Year Bonds

14:00 (AR) Argentina Jan National CPI M/M: 1.9%e v 3.1% prior

Technical Outlook: WTI OIL – Negative Outlook On Speculations For Stronger Build Of Weekly Crude Inventories

Near-term outlook remains negative and sees risk of retesting low at $58.06 (09 Feb) after recovery attempts showed strong rejection at $60.81 on Monday (capped by 55SMA) and Tuesday’s action closed in red.

Negative tone was boosted by stronger than expected build in weekly crude inventories (stocks rose by 3.94 million barrels vs forecasted build of 2.80 million barrels and last week’s draw of 1.05 million barrels) API report showed on Tuesday.

Focus turns towards EIA US crude stocks report , due later today, which is forecasted to show build of 2.82 million barrels compared to 1.89 million barrels build last week.

Fears that US crude stocks may rise more than expected keeps oil price under pressure, along with persisting concerns about soaring US oil output which offsets OPEC-led efforts to tighten oil market by reducing global production.

Break below strong supports at $58.06 (09 Feb low) and $57.68 (rising 100SMA) would spark fresh extension of steep bear-leg from $66.28 high towards targets at $55.81 and $54.80 (07 Dec / 14 Nov troughs).

Alternative scenario requires lift above initial $60.00 barrier and $60.51 (daily cloud top) to sideline immediate downside threats.

Res: 59.29, 60.00, 60.51, 60.91

Sup: 58.58, 58.38, 58.06, 57.68

German Growth Stems Confidence | Focus On US CPI Number

German GDP and CPI data matches estimates

Investors await US CPI data and its reaction

Yen blast past 107

FTSE Futures +34

European markets and US futures are trading higher as traders get a boost from German growth. The solid german growth confirmation was enough to shake off all the negativity-at least for now. Having said that, there are still concerns about the US inflation data and this has been the primary reason (or shall we say an excuse) for the recent turmoil in the global markets. Asian markets had a mixed session ahead of the US CPI data and caution is the word which is more popular amid traders over in the European trading session. Year to date, most of the major indices are trading in a red territory, a sign that bears have overall control of the price.

Inflation and labour data have been two important factors for the Fed through which they have been gauging the health of the US economy. And today’s CPI US number has gained the most attention since the US NFP number. This number is of critical importance as it would determine the future direction of the US equity market and the Goldilocks narrative is at the stack. A strong figure would have the potential to push the dollar index higher as it will fuel the speculations that the Fed is going to adopt a lot more hawkish tone in the market. However, the forecast is for 1.9% and the retail sales data would tell us the ultimate truth about the consumer health.

Strong wage data released earlier this month has also increased the importance of CPI and retail number. In the past, the CPI number has been something which the Fed has paid the least amount of importance to gauge inflation but today is not the today to have that stance.

If the ISM prices are anything to go by, the message which could be taken from that data is that the prices are rising. They are on the steepest path which is not witnessed since 2011. The qualm is that the Fed is behind the curve and the similar message egos when you turn your focus to other central banks. Luckily, the inflation number over in the U.K. remained steady yesterday at 3.0% but the governor of the Bank of England already thinks that there are chances this number may start to move higher again.

The core inflation over in the U.K. has triggered a wake-up call for those who only pay attention to the headline number. The core inflation number over in the U.K. jumped from 2.5% to 2.7%, a primary reason for Sterling to ... , and this has increased the odds for a further reaction by the BoE as soon as May. Something, which the consumers aren’t ready for at all.

For most traders, something which is equally important is the Vix option expiry date which is today. Liquidity is an important in the market and lack of liquidity calls for feeble confidence among investors.

Here Comes CPI Wednesday

USD risk skewewd to the uupside ahead of CPI report

The last jobs report is still in everybody’s mind as it had some unexpected consequences. Indeed, the upside surprise in wage growth triggered last week equity sell-off and send equity volatility through the roof. The January CPI figures, which are due for release this afternoon at GMT 13:30 pm, will be highly scrutinized as a better-than-expected read could potentially trigger another equity sell-off.

The headline CPI is expected to rise 1.9%y/y following an increase of 2.1% in December. Market participants anticipate the core CPI to increase 1.7%y/y for January following a rise of 1.8% in the previous. It would not be surprising to see a stronger reading in headline CPI, thanks to a surge in energy prices. Regarding the core measure, it is unlikely that the cost of rental accommodation and healthcare accelerate further in January. Finally, the persistent weakness in the greenback could give an extra boost to US prices. On a trade-weighted-basis, the dollar fell more 3% just in January, following a decrease of 1.2% in November and 1.1% in December.

During the Asian session, the US dollar stayed on the back foot, as investors don’t know where to stand ahead of the release. We think that the risk is significantly skewed to the upside as investors remain mostly short USD.

Confusing JPY

Japan's 4Q 2017 real GDP rose 0.1% Q/Q and annual 0.5% Q/Q, below expectation for annualized 1.0% increase. However, the Japanese economy has now experienced two years of growth. In a marginal shift Private consumption rose 0.5% Q/Q suggesting household are becoming more confident in economic outlook. JPY continues to appreciate bit overall behavior is confusing. Historical relationship between USDJPY and yields has totally decoupled. During recent period of volatility FX traders favored haven currencies like the JPY and CHF, as well as the EUR.

Yet vol hast decreased significantly, as US interest expectations shown by 10-year breakeven has fallen. Japanese government leaders confirmed their confidence in BoJ Governor Kuroda, bolstering expectations that he will be reappointed for an uncommon second term. Kuroda dovish pedigree indicated at talk of early exit is unwarranted. Clearly, from today data growth has returned but hardly strong enough to demand investor’s attention (especial considering jpy inverse relationship between strength and exprt growth). USDJPY 107.30 “line-in-the-sand” failed to put up much of a fight.

UK inflation in line with expectations but careful with doldrums risk

UK January Consumer Price Index Y/Y ended at 3.0%, in line with expectations and confirming the view of the Bank of England to tighten monetary policy sooner than expected (probably in May 2018), largest contributors to this increase (CPIH Y/Y data) being Housing & Household Services (+0.52%), Transportation (+0.43%) and Recreation & Culture (+0.41%). Recent data are bad news for UK consumers, as wage growth remains weak, valued at 2.20 as of September 2017 in nominal value according to the Office for National Statistics and currently estimated at 2.50%. GBP/USD decrease since Brexit referendum (-3.60% since June 2016; +2.94% Year to date) also contributed to inflation increase, outbidding costs of imported goods and services. Despite this inflationary scenario, the BoE remains optimistic and maintains its prevision of an inflation rate at 2.40% for 2018, expecting an inflation slowdown for 2018 due to recent commodity prices pullback (Bloomberg Commodity Index down by 4.47% since the end of January).

No clear reactions were noticed following the announcement. The FTSE 100 and FTSE 250 closed at 7’168 (-0.16%) and 19’320 (-0.31%) points while GBP/USD and GBP/EUR pairs were maintained at 1.3894 and 1.1246.

We expect Brexit negotiations to be the main factor as to determine whether the BoE will be able to maintain price stability for the coming year, as a weaker GBP would cause further harm to UK purchasing power (UK consumer spending gives first signs of weakness according to a recent payment processing company published data on UK payment processing). In any case a sudden rate hike would cause further harm by exposing households holding consumer credits or real-estate loan to higher interest rates, coupled with strong inflation.

CRUDE OIL Weakness Confirmed

Crude oil slowly continues its fall, trading below 59. Hourly resistance at 64.77 (11/01/2017) keeps being distanced while supports stand at 55.82 (07/12/2017 low) and 53.89 (01/11/2017). The technical structure suggests further downside moves.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness is very likely. For the time being, the pair lies in an upside trend since June 2017. Support lies at 42.20 (16/11/2016) while resistance is located at 77.83 (20/11/2014). Crude oil is trading largely above its 200 DMA.

SILVER Slowing Down

Silver increase weakens, though reversing pattern pattern is maintained and points toward a rise around 16.75. Silver currently trades between hourly resistance at 17.07 (09/11/2017 high) and support at 16.03 (05/12/2017 low). The technical structure suggests further short-term increase.

In the long-term, the trend remains negative/ sideways. Further downside is very likely. The pair is trading below its 200 DMA. Resistance is located at 21.58 (10/07/2014 high). Strong support can be found at 11.75 (20/04/2009).