Sample Category Title

US January Consumer Price Inflation Moves Higher in the Month

Highlights:

- All items CPI rose 0.5% month-over-month which was up from a 0.2% gain in December and compared to market expectations of a 0.3% monthly increase. A 5.7% expected jump in gasoline prices was a main contributor to the sizeable monthly increase.

- A stronger-than-expected 0.3% increase in core prices was also a key factor sending the overall monthly increase higher. The January gain followed a 0.2% increase in December with expectations of that monthly increase being maintained in January.

- The stronger-than-expected monthly gain contributed to the overall year-over-year rate remaining unchanged at 2.1%.

- The annual increase in core prices remained unchanged as well at 1.8%.

Our Take:

The January CPI report indicated consumer prices rose a stronger than expected 0.5% in the month. This report will likely abet financial market concerns about rising inflation pressures that emerged last week with wage inflation rising at a pace not seen since 2009. Indications of incipient wage pressures reinforced the view that labour markets are operating beyond capacity with a current unemployment rate of 4.1%. Confirmation of tightening labour markets made an even stronger case for the Fed to continue to tighten policy which weighed on financial markets. Today's inflation report will raise concerns that this wage pressure is starting to seep into consumer prices. It is the case that the year-over-year rate for core prices remained unchanged at 1.8% and thus below the Fed's inflation objective of 2%. However, the 6-month average price gain for core consumer prices has jumped to 2.6% from 2.2% in December. This pressure in conjunction with indications of potential wage pressures emerging are expected to keep the Fed tightening. Our forecast assumes that the central bank will raise the fed funds range by 25 basis points at the March FOMC meeting to 1.50% to 1.75%. The tightening is expected to continue through the forecast with similar-sized hikes expected each quarter through the end of 2019 resulting in the fed funds range finishing next year at 3.25% to 3.50%.

USDJPY – Limited Reaction on Upbeat US Inflation Numbers Keeps Bearish Bias Intact

The pair showed limited reaction on upbeat US inflation data today, as the dollar jumped to 107.53 but quickly fell back, erasing all post-data gains. Unlike from other major currency pairs where the greenback advanced strongly, USDJPY's reaction was mild. Better than expected inflation numbers in January and underlying inflation showing the biggest gains in a year, would further boost expectations for Fed's more aggressive approach towards the monetary policy this year and likely prompt the central bank for more rate hikes than planned. Stronger dollar after release of key data pushed stocks lower, which boosted yen and limited dollar's rally, while Japanese currency also advanced against other major counterparts, registering fresh gains against the Euro and British Pound. USDJPY's near-term outlook did not change significantly after strong US data, maintaining bearish bias after rather mild 106.83/107.50 correction (106.83 is new 15-month low posted overnight while 107.50 is the highest traded after release of US CPI data). Fresh easing cracked 107.00 figure and pressured support at 106.83, eyeing target at 106.51 (Fibo 61.8% of 98.99/118.66, Jun/Dec 2016 rally). Initial resistance lies at 107.53 (post data/European session high), followed by session high at 107.90 which guards former low and key support at 108.28, where stronger upticks should be capped.

Res: 107.53; 107.90; 108.28; 108.87

Sup: 106.99; 106.83; 106.51; 106.00

Price Determination: A Web of Interactions

One of the fascinations about economics and finance is the matrix of interactions among prices. For some time now, we have focused on the interaction of prices for goods, capital and exchange rates.

Growth and Goods Inflation: One Way Link

When we first examine the pattern of goods prices, one driver is the growth of GDP. GDP has a one-way causal link to the PCE deflator (top graph). As would be expected in the short-run, stronger economic growth tends to raise the rate of inflation as resource utilization increases, thus driving prices higher.

However, there is a problem: the PCE deflator is a mean reverting series but has an autocorrelation problem. That is, the process of the series returning to its long-run mean is painfully slow. The autocorrelation problem suggests that if the PCE deflator series deviates from the long-run mean, then the series will take an extended period of time to return to the mean. Unfortunately, the same conclusion is true for the core PCE deflator series as well. In fact, both series have, to some extent, shifted downward in the last decade. The average for the 2009-2017 period is just 1.3 percent for the PCE deflator and 1.5 percent for the core PCE deflator.

Domestic Demand and the Price of Capital

A second critical price in the economy is the cost of capital, i.e., interest rates. Consider the relationship in the middle graph between real final sales and the two-year Treasury rate. Here, real final sales have a one-way causality link to the two-year benchmark Treasury rate. This may not be surprising in recent months as the rise in economic strength has been accompanied by a rise in the two-year rate. However, this relationship is based upon data over the entire 1982-2017 period—not upon a short/one-time phenomenon.

The real final sales series underwent a downward break in October 2008 so that the period of "low" interest rates since then is perfectly consistent with the downward shift in its driver—real final sales.

Completing the Web: Dollar, Rates and Inflation

Interrelationships between economic and financial factors are fascinating. Consider that both the US dollar and the two-year Treasury rate have oneway causality link to inflation. That is, both the dollar and the two-year Treasury rate influence the behavior of the PCE deflator but the deflator does not drive the behavior of the dollar nor the two-year rate. Yes, there is some influence as you might expect but the link is not statistically significant and thereby unreliable in the forecasting sense.

For the PCE, growth in GDP is the main driver. For our work, the link from the dollar and the two-year Treasury to inflation reinforces our imperative to focus on a broader model of economic behavior than the linear nonrecursive behavior that so dominates popular commentary. Moreover, these statistical results remind us to focus on the significant links and not be distracted by the myriad of minor forces in the economy.

USD/JPY Mid-Day Outlook

Intraday bias in USD/JPY remains on the downside for the moment. Current fall should extend to 106.48 fibonacci level. We'd look for strong support around there to bring rebound. However, on the upside, break of 108.80 minor resistance is needed to be the first sign of short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

Daily Pivots: (S1) 107.22; (P) 107.99; (R1) 108.59; More...

Intraday bias in USD/JPY remains on the downside for the moment. Current fall should extend to 106.48 fibonacci level. We'd look for strong support around there to bring rebound. However, on the upside, break of 108.80 minor resistance is needed to be the first sign of short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD/JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

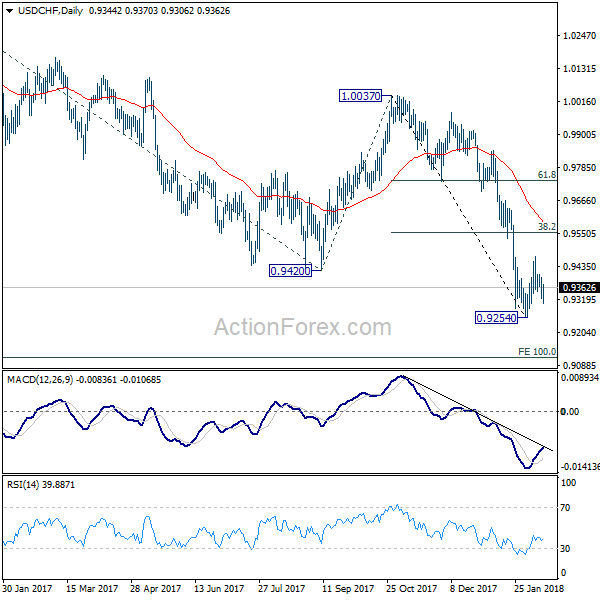

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9315; (P) 0.9356; (R1) 0.9391; More...

With 0.9408 minor resistance intact, fall from 0.9469 is in favor to extend to retest 0.9254 low. Break will resume larger down trend to next projection level at 0.9115. Above 0.9408 would bring stronger rise through 0.9469. However, note again that there is no sign of trend reversal yet. We'd be cautious on strong resistance from 38.2% retracement of 1.0037 to 0.9254 at 0.9553 to limit upside and bring down trend resumption.

In the bigger picture, fall from 1.0342 is developing into a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

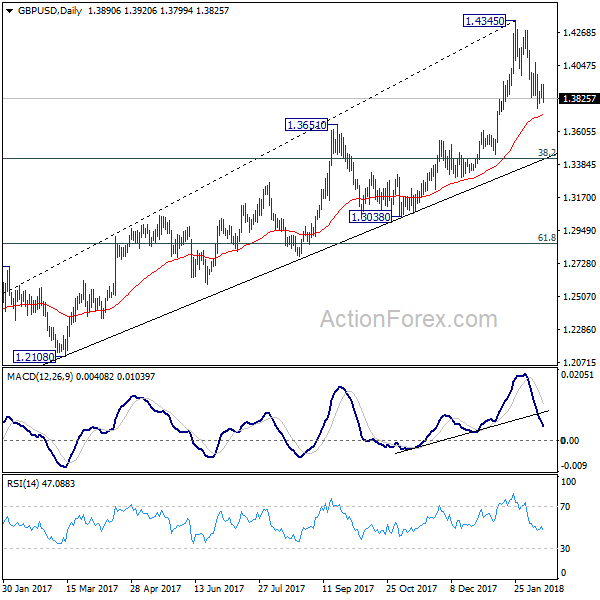

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3841; (P) 1.3882; (R1) 1.3932; More.....

GBP/USD failed to take out 4 hour 55 EMA and weakens again in early US session. Outlook in GBP/USD remains unchanged as fall from 1.4345 is expected to extend to 1.3651 resistance turned support. It's still unsure whether decline from 1.4345 is correcting rise from 1.3038, or that from 1.1946, or it's reversing the trend. Break of 1.3651 will turn focus to key fibonacci level at 1.3429. On the upside, break of 1.4066 will turn bias back to the upside for retesting 1.4345 instead.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279 so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

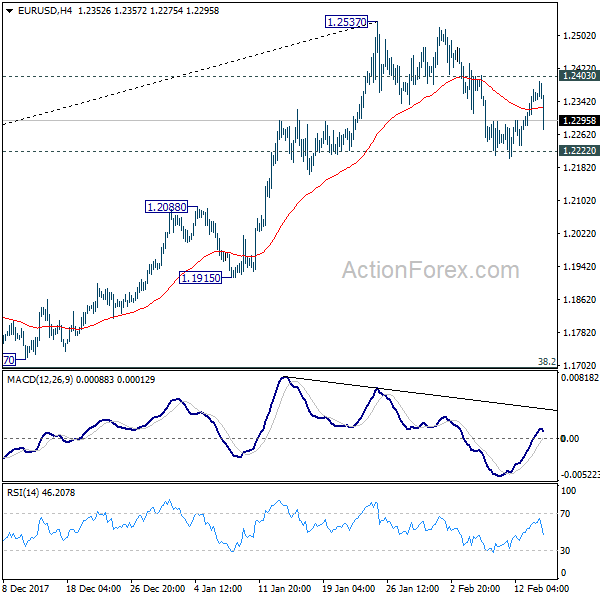

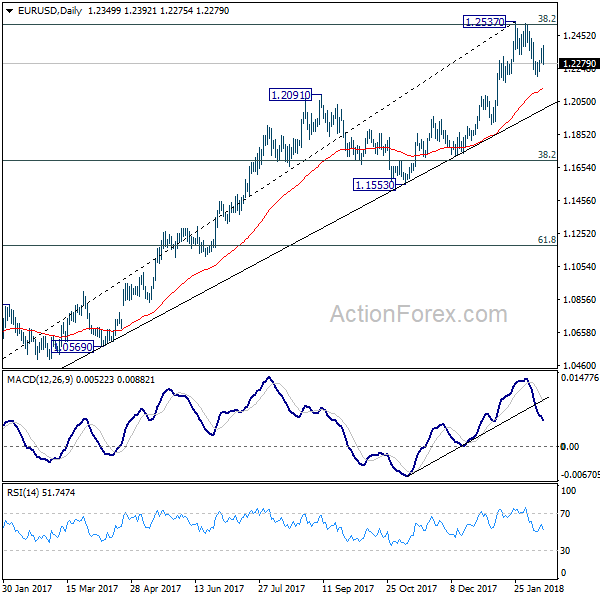

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2300; (P) 1.2335 (R1) 1.2387; More....

EUR/USD's recovery was limited well below 1.2403 minor resistance and weakens sharply. Intraday bias stays neutral with focus back of 1.2222. On the downside, sustained break of 1.2222 key support should confirm rejection from 1.2516 key fibonacci level, as well as near term reversal, on bearish divergence condition in 4 hour MACD. That could also signal completion of medium term up trend from 1.0339. In that case, near term outlook will be turned bearish for 38.2% retracement of 1.0339 to 1.2537 at 1.1697. On the upside, though, above 1.2403 minor resistance will revive bullishness and turn focus back to 1.2537.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Dollar Jumps on Resilient Consumer Inflation, Stock Futures Tumble

Dollar jumps notably in early US session after stronger than expected inflation data. Headline CPI jumped 0.5% mom in January, above expectation of 0.3% mom. Annual rate of CPI was unchanged at 2.1% yoy, above expectation of 1.9% yoy. Core CPI rose 0.3% mom, above expectation of 0.2% mom. Annually, core CPI was unchanged at 1.8%, above expectation of 1.7%. The set of inflation does nothing to alter expectation of a Fed hike in March. More importantly, the resilience in annual reading is raising the chance of three or four hikes this year. Retail sales were disappointing but markets paid little attention. Headline sales dropped -0.3% while ex0auto sales was flat in January.

Technically, Dollar's rebounds against Euro, Sterling, Aussie and Loonie are apparent. However, it looks quite unsure against Yen and Swiss Franc. The latter could be explained by risk aversion as stock futures tumble after the CPI release.

ECB: Bitcoin is not a currency

ECB President Mario Draghi is clear with his position on Bitcoin. He said it's "not the ECB's responsibility" to regulate Bitcoins. He acknowledge the blockchain technology as "quite promising" that could bring "many benefits". But he warned that "it's still not secure for central banking and therefore we need to look through it and investigate it more." And when asked by the public on whether he should buy Bitcoin, Draghi said "frankly i would think it carefully".

At the same time, ECB published a short article explaining "what is bitcoin?" It short, it's a "speculative asset". And, ECB explained that Bitcoin is not a currency by the following chart.

Released from Eurozone, GDP grew 0.6% qoq in Q4, same as prior quarter and met expectations. Industrial production rose 0.4% mom in December, above expectation of 0.1% mom. German GDP grew 0.6% qoq in Q4, slowed from 0.8% qoq but met expectation. German CPI was finalized at -0.7% mom, 1.6% yoy in January.

IMF: UK investment growth constrained by Brexit uncertainty

The International Monetary Fund warned in a report that UK "business investment growth has been constrained by continued uncertainty about the future trade regime." It pointed out that "UK growth moderated in 2017 despite significant monetary policy accommodation and strong trading partner growth, and is expected to remain subdued in the near term."

IMF emphasized that "early agreement on a transition period would avoid a cliff edge exit in March 2019 and reduce the uncertainty now facing firms and households." Also, "continued steady fiscal consolidation, with an emphasis on pro-growth spending and tax reforms, remains critical to rebuild fiscal buffers and maintain investor confidence." In additional, IMF urged BoE to continue to withdrawal stimulus at as "gradual pace".

Elsewhere

Japan GDP rose 0.1% qoq in Q4, below expectation of 0.2% qoq. GDP deflator rose 0.01% yoy. Australia Westpac consumer confidence dropped -2.3% in February. RBNZ 2 year inflation expectation rose 2.1% in Q1.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2300; (P) 1.2335 (R1) 1.2387; More....

EUR/USD's recovery was limited well below 1.2403 minor resistance and weakens sharply. Intraday bias stays neutral with focus back of 1.2222. On the downside, sustained break of 1.2222 key support should confirm rejection from 1.2516 key fibonacci level, as well as near term reversal, on bearish divergence condition in 4 hour MACD. That could also signal completion of medium term up trend from 1.0339. In that case, near term outlook will be turned bearish for 38.2% retracement of 1.0339 to 1.2537 at 1.1697. On the upside, though, above 1.2403 minor resistance will revive bullishness and turn focus back to 1.2537.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Feb | -2.30% | 1.80% | ||

| 23:50 | JPY | GDP Q/Q Q4 P | 0.10% | 0.20% | 0.60% | |

| 23:50 | JPY | GDP Deflator Y/Y Q4 P | 0.00% | 0.00% | 0.10% | 0.20% |

| 02:00 | NZD | RBNZ 2-Year Inflation Expectation Q1 | 2.10% | 2.00% | ||

| 07:00 | EUR | German GDP Q/Q Q4 P | 0.60% | 0.60% | 0.80% | |

| 07:00 | EUR | German CPI M/M Jan F | -0.70% | -0.70% | -0.70% | |

| 07:00 | EUR | German CPI Y/Y Jan F | 1.60% | 1.60% | 1.60% | |

| 10:00 | EUR | Eurozone Industrial Production M/M Dec | 0.40% | 0.10% | 1.00% | 1.30% |

| 10:00 | EUR | Eurozone GDP Q/Q Q4 P | 0.60% | 0.60% | 0.60% | |

| 13:30 | USD | CPI M/M Jan | 0.50% | 0.30% | 0.10% | 0.20% |

| 13:30 | USD | CPI Y/Y Jan | 2.10% | 1.90% | 2.10% | |

| 13:30 | USD | CPI Core M/M Jan | 0.30% | 0.20% | 0.30% | 0.20% |

| 13:30 | USD | CPI Core Y/Y Jan | 1.80% | 1.70% | 1.80% | |

| 13:30 | USD | Retail Sales Advance M/M Jan | -0.30% | 0.20% | 0.40% | |

| 13:30 | USD | Retail Sales Ex Auto M/M Jan | 0.00% | 0.50% | 0.40% | |

| 15:00 | USD | Business Inventories Dec | 0.30% | 0.40% | ||

| 15:30 | USD | Crude Oil Inventories | 2.8M | 1.9M |

USDJPY Strongly Bearish Below 107.29 Level

The USDJPY pair remains strongly bearish while price-action trades below the 107.29 level, further downside towards 106.89 and 106.60 appears likely.

Should the USDJPY pair start to hold above the key 107.29 level for an extended period, we may see a upside correction back towards the 107.84 and 108.40 resistance areas.

EURUSD Retracing Towards Key 1.2332 Level

The euro has moved marginally lower against the greenback during the European trading session, following weaker than expected German economic data and a rebound in the U.S dollar index. The EURUSD pair currently trades around the 1.2350 region, with bullish momentum largely intact while price-action remains above the key 1.2332 support level. Traders now look to the release of the U.S Consumer Price Index for the month of January, with any major upticks in U.S inflation likely to further pressure the EURUSD lower.

The EURUSD pairs bullish trading sentiment remains intact whilst price-action trades above the 1.2332 level, key upside resistance is now found at 1.2393 and 1.2432.

Should EURUSD price-action move below the 1.2332 level, the intraday sentiment will turn bearish, encouraging further selling towards the 1.2290 and 1.2255 levels.