Sample Category Title

Japan’s Industrial Production Revised Higher In December

For the 24 hours to 23:00 GMT, the USD declined 0.15% against the JPY and closed at 106.93.

In the Asian session, at GMT0400, the pair is trading at 106.50, with the USD trading 0.4% lower against the JPY from yesterday's close.

Overnight data showed that Japan's machinery orders slid 11.9% MoM in December, more than market expectations for a drop of 2.0%. In the previous month, machinery orders had climbed 5.7%.

Earlier today, data indicated that the nation's final industrial production grew more than initially estimated by 2.9% on a monthly basis in December, while the preliminary figures had recorded an advance of 2.7%. In the prior month, industrial production had risen 0.5%.

The pair is expected to find support at 106.03, and a fall through could take it to the next support level of 105.55. The pair is expected to find its first resistance at 107.26, and a rise through could take it to the next resistance level of 108.01.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading Higher In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.38% against the CHF and closed at 0.9291.

In the Asian session, at GMT0400, the pair is trading at 0.9275, with the USD trading 0.17% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9239, and a fall through could take it to the next support level of 0.9203. The pair is expected to find its first resistance at 0.9343, and a rise through could take it to the next resistance level of 0.9411.

Amid no macroeconomic releases in Switzerland today, investors would focus on global macroeconomic releases for further direction.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Loonie Trading A Tad Higher, Ahead Of Canada’s Existing Home Sales Data

For the 24 hours to 23:00 GMT, the USD declined 0.57% against the CAD and closed at 1.2496.

On the macro front, Canada's Teranet/National Bank house price index climbed 0.3% on a monthly basis in January. In the previous month, the index had risen 0.2%.

In the Asian session, at GMT0400, the pair is trading at 1.249, with the USD trading slightly lower against the CAD from yesterday's close.

The pair is expected to find support at 1.2430, and a fall through could take it to the next support level of 1.2371. The pair is expected to find its first resistance at 1.2599, and a rise through could take it to the next resistance level of 1.2709.

Ahead in the day, investors would await the release of Canada's existing home sales data for January.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

ECB’s Praet Speaks At 11:45 CET

Market movers today

In Norway, Norges Bank's governor Olsen is making his annual address at 18.00 CET, which will be interesting, not least as Norges Bank has made a U-turn from signalling further rate cuts to indicating a rate increase within a year (page 2).

In the US, we get PPI inflation data for January, which might attract more attention than usual after the higher-than-expected CPI inflation print released yesterday.

Also in the US today, we get production data for January and Empire and Philly regional manufacturing PMIs for February.

The Chinese financial markets are closed from today and until 22 February for the Lunar New Year.

ECB's Praet speak s at 11:45 CET.

Selected market news

The US CPI was the highlight of data points yesterday. Overall the strong CPI core 1.8% yoy (close to 3% annualised in the last three months), supports the case for the Fed to move forward with further rate hikes. Albeit , retail sales were weaker than expected. Over the day as a whole, risk sentiment was supported despite an initial knee-jerk on the US CPI. Global equities rose across the board. Asian equities followed the pattern by rising 1-2% in the overnight session. S&P 500 rose 1.4% as eurostoxx rose 0.9%, while the volatility index VIX fell rapidly after the knee-jerk reaction to the US data and ended around 19.3. The yen strengthened again yesterday. The treasury yields ended the day 7bp higher at 2.90%.

South African now former president resigned yesterday with immediate effect . ANC leader Cyril Ramaphosa will replace Zuma.

Euro area Q4 growth was confirmed at 0.6% q/q as expected. The flash release of Germany and Italy were also released. German Q4 17 growth came in as expected at 0.6% q/q, mainly due to strong foreign demand and a pick-up in exports. This leaves annual growth in 2017 at 2.5% and we expect the German economy to continue running on all engines. The Italian Q4 growth disappointing slightly at 0.3% q/q after 0.4% q/q in the previous quarter, despite the high manufacturing PMIs. This leaves annual growth in 2017 at 1.5%.

Yesterday, the Riksbank chose to reduce inflation (in part icular CPIF ex energy due to lowerthanexpected wage increases) and GDP forecasts (now recognising that housing construction activity will decrease more than expected previously) while keeping the reporate unchanged. We have elaborated with a base Riksbank scenario (no rate hikes this year) and a not improbable alternative scenario (one or possibly two hikes then a pause for a year or so). Admittedly, it looks like a close call. That the Riksbank is sticking to the rate path despite lowering the inflation forecast could be taken as hawkish but , in our view this is not really vindicated by the policy report . This suggests that the Riksbank was close to delaying the first hike. For now, we stick to our base case as the most probable but the minutes published on Friday next week will be of the essence just like the coming inflation data.

Market Update – Asian Session: Aso Says No Intervention Needed On Yen At Current Levels

Headlines/Economic Data

General Trend: Asian equities generally track US gains amid holidays in China, Taiwan, South Korea and Vietnam

Hang Seng gains 1.8% in shortened session

Banks in Japan outperform after gains in S&P500 Financials sector and rise in Treasury yields

With the Shanghai markets closed, China equity futures gain in Singapore

Nasdaq and S&P500 Futures rise

US dollar (USD) trades broadly weaker in Asia, in the aftermath of the US inflation and retail sales data

USD/JPY declines: Japan Fin Min Aso said Yen strength is not abrupt enough to intervene

Japan Dec Core Machinery Orders see largest m/m decline since May 2014 (follows recent weaker than expected prelim Q4 GDP)

New Zealand sells 2025 bonds at higher yield and lower bid to cover

In Jan, Australia adds jobs for a record 16th straight month, but full-time employment declines

Indonesia reports second straight monthly trade deficit

Australia's largest gold miner Newcrest reports declines in H1 profits and revenues amid impact of seismic event at Cadia operations and decline in gold/copper sales volumes.

US 10-year Treasury yield extends gains in Asian trading, hits 4-year high

Japan

Nikkei 225 opened +1.1%; closed +1.5%

TOPIX Electronic Devices Index +1.9%, Securities +1.8%, Iron &Steel +1.5%, Real Estate +1%

Financials track outperformance seen during US session, Japanese mega banks gain more than 1%

Japan Display [6740.JP]: Declines over 4% after 9M net loss widened

(JP) JAPAN DEC CORE MACHINE ORDERS M/M: -11.9% V -2.0%E; Y/Y: -5.0% (largest fall since June 2017) V +1.8%E

(JP) Japan Fin Min Aso: Yen (JPY) strength NOT strong enough to require intervention: No comment on yen level - parliament

(JP) Japan Govt to urge companies to adopt a more transparent decision-making process through measures such as allocating at least one-third of board seats to outsiders - Nikkei

(JP) Japan Ruling Coalition Partner Yamaguchi: No word from PM Abe on BOJ Gvo nominee

(JP) Japan MoF sells ¥4.4T in 3-month bonds; avg yield -0.1607%

(JP) JAPAN DEC FINAL INDUSTRIAL PRODUCTION M/M: 2.9% V 2.7% PRELIM; Y/Y: 4.4% V 4.2% PRELIM, Capacity Utilization m/m: 2.8% v 0.0% prior

Korea

Kospi closed

(KR) South Korea President Moon coming under some criticism for slow regulatory reform, in light of his repeated pledges to push for drastic deregulation - Korean press

Lotte, LOTZ.KR Chairman Shin Dong-bin jail term will reigniting a succession battlebetween Shin and his older brother, Shin Dong-joo - Korean press

China/Hong Kong

Hang Seng opened +1.5%, Shanghai Composite closed for holiday

Hang Seng Materials Index +3.3%, Info Tech +2.9%, Energy +2.7%, Financials +2.3%,Property/Construction +1.7%

(CN) China cuts manufacturer subsidies for many electric cars and plug-in hybrids by ~30%, with the centralgovt planning to re-evaluate this aid again around mid-year - press

(CN) China Ambassador to US Tiankai: It's dangerous to advocate for confrontation against China - financial press

Australia/New Zealand

ASX 200 opened +0.6%; closed %

ASX 200 Materials Index +2.1%, Energy +1.9%, Utilities+1.2%, Telecom +1.2%, Financials +0.7%; REIT -0.1%

Origin Energy [ORG.AU] rises over 6% after raising guidance

Telstra [TLS.AU] gains over 1% after reporting in line H1 earnings

(NZ) New Zealand Rev Min:To extend test on residential sales (bright line test) to 5 years

(AU) Australia Jan Consumer Inflation Expectation: 3.6% v 3.7% prior

(AU) AUSTRALIA JAN EMPLOYMENT CHANGE: +16K V +15.0KE (16TH CONSECUTIVE MONTHLY GAIN); UNEMPLOYMENT RATE: 5.5% V 5.5%E

(AU) Australia Jan RBA Govt FX Transactions (A$): -634M v -1.36B prior

(NZ) New Zealand sells NZ$200M in 2.75% 2025 bonds; avg yield 2.7719%; bid to cover 2.78x

FCG.NZ Raises 12-month forecast auction volumes by 2.0K MT

(NZ) Fitch affirms New Zealand Sovereign Rating at AA; Outlook Stable

Looking ahead: RBA Gov Lowe expected to speak on Friday’s session (follows his remarks on Feb 8th)

Other Asia

(SG) Singapore Jan Non-OilDomestic Exports M/M: -0.3% v 4.2%e; Y/Y: +13.0% v 8.9%e; Electronic ExportsY/Y: -3.9% v -5.3% prior

North America

US equity markets ended higher: Dow +1%, S&P500 +1.3%, Nasdaq +1.9%, Russell 2000+1.8%

S&P500 Financials +2.4%, Technology +1.8%

(US) Treasury Sec Mnuchin: reiterates he expects wage growth in the US this year

(US) Pres Trump reportedly supports a 25-cent gas tax hike to pay for infrastructure - Axios

(US) DOE CRUDE: +1.8M V +3ME

Europe

(DE) Bundesbank study says about 90% of euro (EUR) bank notes issued in Germany are never used for payments, but instead hoarded – FT

(DE) German Chancellor Merkel: will make sure Germany maintains a balanced budget; CDU Party remains opposed to debt mutualization in the Euro Zone

(GR) Greece Deputy PM Dragasakis: Greece wants a closer relationship with China, it is also keen to build stronger ties with Japan, India and other Asian countries - press

Levels as of 01:00ET

Nikkei225 +1.5%, Hang Seng +1.8%; Shanghai Composite closed; ASX200 +1.2%, Kospi closed

Equity Futures: S&P500 +0.4%; Nasdaq100 +0.5%,Dax +0.4%; FTSE100 +0.2%

EUR 1.2473-1.2448; JPY107.01-106.30; AUD 0.7946-0.7905;NZD 0.7395-0.7363

Apr Gold -0.1% at $1,357/oz; Mar Crude Oil +1.3% at $61.41/brl; Mar Copper +0.3% at $3.24/lb

GOLD – Threatening Further Upside Pressure

GOLD - The commodity saw price rally on Wednesday leaving risk higher. On the downside, support comes in at the 1,340.00 level where a break will turn attention to the 1,330.00 level. Further down, a cut through here will open the door for a move lower towards the 1,320.00 level. Below here if seen could trigger further downside pressure towards the 1,210.00 level. Conversely, resistance resides at the 1,360.00 level where a break will aim at the 1,370.00 level. A turn above there will expose the 1,380.00 level. Further out, resistance stands at the 1,390.00 level. All in all, GOLD looks to strengthen further.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 148.95; (P) 149.78; (R1) 150.59; More...

Intraday bias in GBP/JPY remains on the downside as fall from 156.59 is in progress for 146.96 support. Considering bearish divergence condition in daily MACD, firm break of 146.96 will be another sign of medium term trend reversal. On the upside, break of 151.19 is needed to be the first sign of short term bottoming. Otherwise, outlook will remain cautiously bearish even in case of recovery.

In the bigger picture, as long as 146.96 key support holds, medium term outlook remains bullish. Rise from 122.36 is in favor to extend to 61.8% retracement of 195.86 to 122.36 at 167.78. However, break of 146.96 support will indicate trend reversal after rejection by 55 month EMA. In that case, deeper fall would be seen to 38.2% retracement of 122.36 to 156.59 at 143.51 and then 61.8% retracement at 135.43.

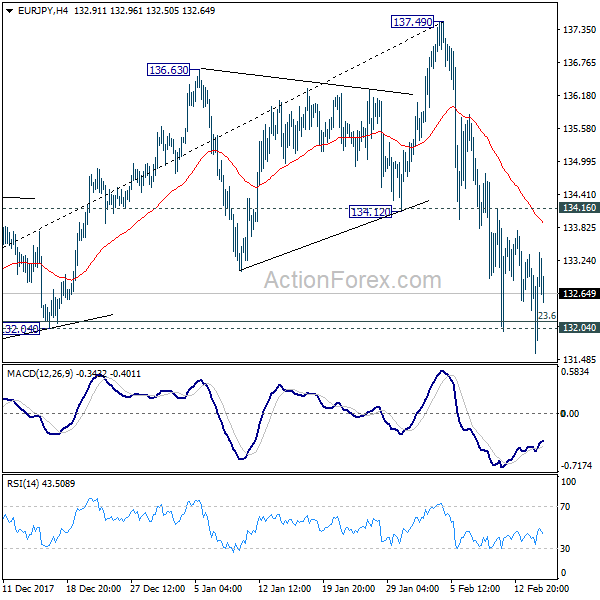

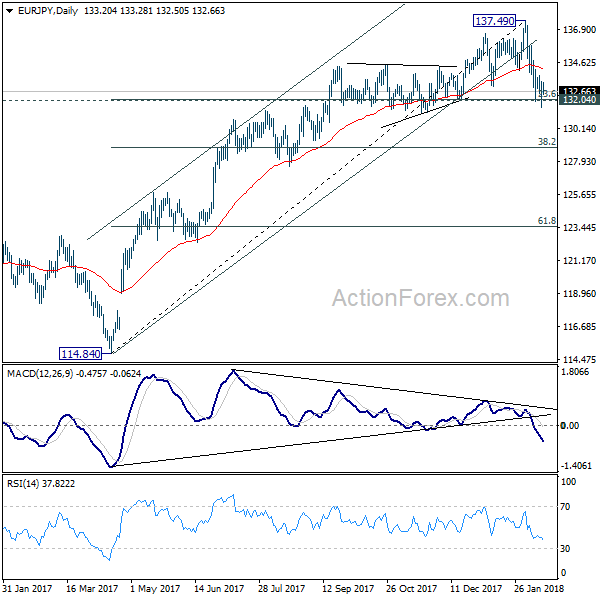

EUR/JPY Daily Outlook

Daily Pivots: (S1) 132.52; (P) 133.15; (R1) 133.79; More....

At this point, EUR/JPY cannot sustain below 132.04 cluster support (23.6% retracement of 114.84 to 137.49 at 132.14) yet. Intraday bias remains neutral first. Deeper fall is still expected with 134.16 resistance intact. Decisive break of 132.04/14 will indicate larger trend reversal on bearish divergence condition in daily MACD. In such case, outlook will be turned bearish for 38.2% retracement at 128.38 first. Nonetheless, rebound from 132.04 will retain near term bullishness. Break of 134.16 minor resistance will bring retest of 137.49 high instead.

In the bigger picture, bearish divergence condition in week EMA indicates lost up medium term up trend momentum. But there is no clear sign of completion of up trend from 109.03 yet. Break of 137.49 will target 141.04/149.76 resistance zone. However, sustained break of 132.04 will be the early sign of long term reversal and should bring deeper fall back to retest 124.08 key support level.

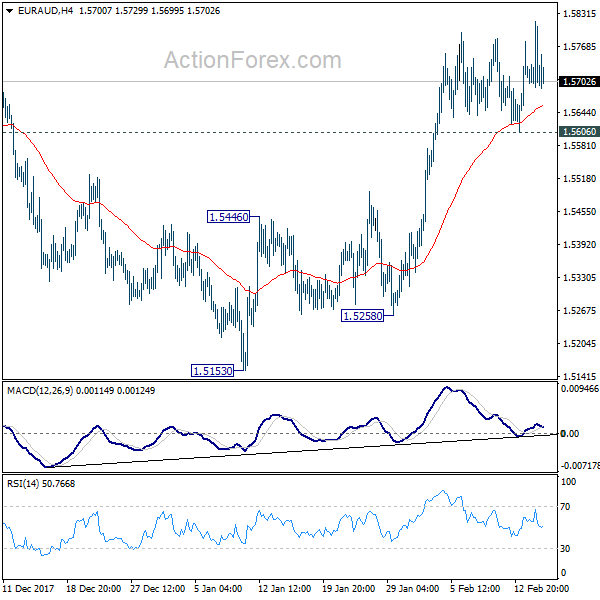

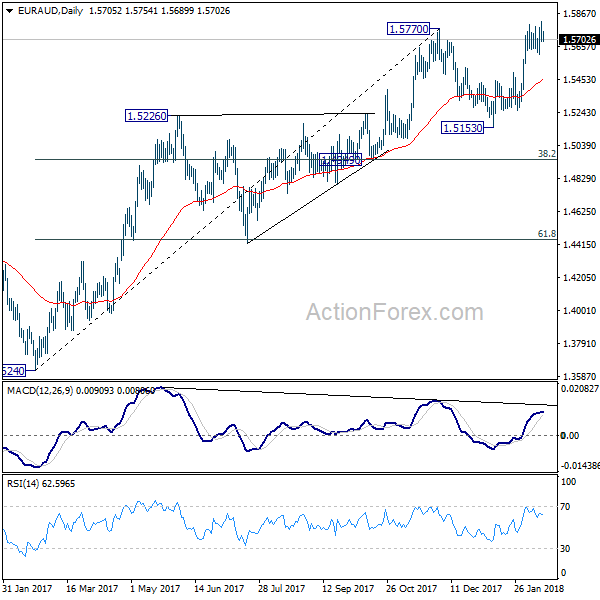

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5660; (P) 1.5738; (R1) 1.5785; More....

EUR/AUD edged higher to 1.5816 but quickly retreated. But after all, as long as 1.5606 support holds, further rally is expected. Sustained break of 1.5770 resistance will confirm resumption of medium term rise from 1.3264. In that case, EUR/AUD should target 1.6587 key long term resistance. However, below 1.5606 minor support minor support will dampen this bullish case and turn bias to the downside.

In the bigger picture, medium term rise from 1.3624 is not completed yet. Break of 1.5770 will extend the rise to retest 1.6587 (2015 high). However, considering bearish divergence condition in daily MACD, sustained break of 1.4949 cluster support (38.2% retracement of 1.3624 to 1.5770 at 1.4950) will indicate medium term reversal. And there is prospect of retesting 1.3624 low in that bearish case.

Gold Price Back In Bullish Zone Post US CPI

Key Highlights

- Gold price traded higher recently and succeeded in breaking the $1,335 resistance against the US Dollar.

- A crucial bearish trend line with resistance at $1,330 was breached on the 4-hours chart of XAU/USD.

- The US Consumer Price Index increased 0.5% in Jan 2018, more than the forecast of 0.3% (MoM).

- The US Retail Sales declined 0.3% in Jan 2018, compared with the forecast of +0.2% (MoM).

Gold Price Technical Analysis

There was a bullish price action in Gold price earlier this week above $1,325 against the US Dollar. Later, the price gained upside momentum and broke a major resistance at $1,335.

More importantly, there was a break above a crucial bearish trend line with resistance at $1,330 on the 4-hours chart of XAU/USD. The trend line resistance was also near the 100 simple moving average (red, 4-hours).

Therefore, the $1,335 level break holds a lot of significance. The price traded as high as $1,355 recently. On the downside, an initial support is around the 23.6% Fib retracement level of the last wave from the $1,307 low to $1,355 high.

However, the most important support is near $1,335 (previous resistance). It is also near the 38.2% Fib retracement level of the last wave from the $1,307 low to $1,355 high.

In the short term, the price may consolidate above $1,345, with supports at $1,340 and $1,335. On the upside, a break above $1,355 could push the price towards $1,365.

US CPI and Retail Sales

Recently, the US saw two important releases. First, the Consumer Price Index for Jan 2018 by the US Bureau of Labor Statistics. The market was looking for a rise of 0.3% in the CPI compared with the previous month.

The actual result was better, as there was a 0.5% rise in the CPI (MoM). The yearly change came in at 2.1%, more than the forecast of 1.9%, but similar to the last. The report added that:

The seasonally adjusted increase in the all items index was broad-based, with increases in the indexes for gasoline, shelter, apparel, medical care, and food all contributing. The energy index rose 3.0 percent in January, with the increase in the gasoline index more than offsetting declines in other energy component indexes. The food index rose 0.2 percent with the indexes for food at home and food away from home both rising.

The second release was the Retail Sales for Jan 2018 by the US Census Bureau. The result was disappointing, as there was a 0.3% decline in sales compared with the previous month, whereas the market was looking for a 0.2% rise.

The US Dollar gained initially after the release, but it later declined heavily. EUR/USD jumped from 1.2280 to 1.2450 and GBP/USD moved above 1.4000. However, there was a no relief for the USD/JPY buyers, as the pair tumbled to a new 15-month low and traded below 107.00.