Sample Category Title

Dollar Slides While Stocks Climb, Jobless Claims And IP Gathering Attention In The US

Here are the latest developments in global markets:

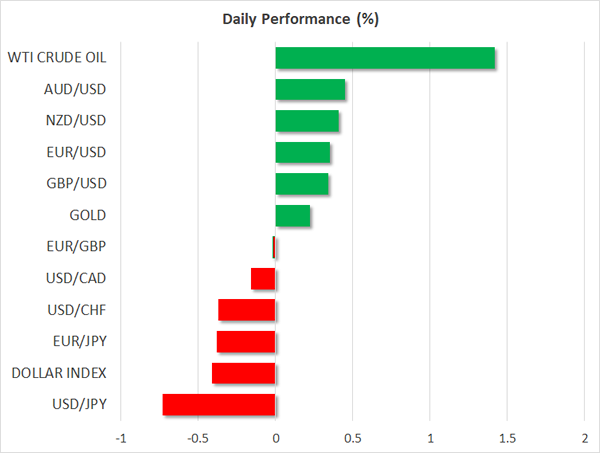

FOREX: The dollar index fell 0.4% on Thursday, extending the significant losses it posted on Wednesday in the aftermath of the US CPI and retail sales data.

STOCKS: US markets finished the day notably higher yesterday, erasing earlier losses, despite the stronger-than-anticipated US inflation prints for January. The Nasdaq Composite led the charge, gaining almost 1.9%, while the S&P 500 followed in its tracks, closing 1.3% higher. The Dow Jones climbed 1.0%. Moreover, futures tracking the Dow, S&P, and Nasdaq 100, are all in positive territory, suggesting these indices could open higher today. The positive sentiment spilled over into Asian trading as well. In Japan, the Nikkei 225 rose 1.5% while the Topix climbed by 1.0%, both indices recovering some of their latest losses even despite the surge in the yen, which typically weighs on Japanese equities. In Hong Kong, the Hang Seng added 2.0% in shortened trading ahead of the Lunar New Year holidays, while in Europe, futures tracking all of the major indices are in the green as well.

COMMODITIES: Oil prices surged today, with WTI and Brent crude being up 1.4% and 0.8% respectively, both benchmarks adding to the massive gains they posted yesterday on the back of a weaker dollar, the recovery in risk sentiment, and a smaller-than-anticipated build in US inventories. Some comments from the Saudi Energy Minister Khalid al-Falih probably helped as well. He noted that his nation is willing to stick to the OPEC and non-OPEC supply cuts throughout 2018, even if the market rebalances itself in the meantime, alleviating some fears of over-supply amid recent reports that US production continues to soar. In precious metals, gold was 0.2% higher today, after skyrocketing yesterday in the aftermath of the US data to break above the $1350/ounce barrier, currently trading near $1354. Technically, the $1366 level will be key to watch, as a potential upside break of that area would mark a forthcoming higher high on the daily chart.

Major movers: Dollar tanks while US stocks close higher, even despite CPI beat

To say that markets moved sharply after the US data releases yesterday is an understatement. In terms of inflation, both the headline and the core CPI rates remained unchanged at 2.1% and 1.8% respectively in yearly terms, beating their forecasts for modest declines. However, retail sales disappointed notably, with the headline rate dropping instead of rising as anticipated, while last month’s prints were also revised lower.

The market response was fierce. Initially, the knee-jerk reaction was a stronger dollar as the yields on 10-year Treasury bills surged to reach 4-year highs. The opposite was true for US equity indices, which dropped on speculation that the Fed may raise rates more aggressively due to robust inflation, and the prospect of softer corporate earnings amid signs that consumption may be waning.

However, this all reversed within the following minutes. The dollar quickly gave back all its gains to trade much lower against its major counterparts, while US stocks recovered to finish the day even higher. There was no clear catalyst for the reversal. A plausible explanation is that despite the signs of strong inflation, the FOMC may not pick up the pace of normalization, amid signs of slowing consumption in the economy. Indeed, in the aftermath of the data, the Atlanta Fed GDPNow model revised down its GDP forecast for the first quarter to 3.2%, from 4.0% previously. Some large option expiries at that time (especially in euro/dollar) may have helped to initiate the reversal in the dollar, and once it was underway, the break of some key technical levels likely aided as well.

Overall, the reaction to this data set confirms that despite some consolidation in recent days, the negative sentiment surrounding the dollar remains in full force, amid concerns over rising budget deficits and the sustainability of the US debt trajectory, among others. Judging by yesterday’s moves, dollar/yen appears to be a good proxy for further dollar weakness. Besides the dollar tanking, the yen is enjoying safe haven inflows amid all of this havoc, causing the pair to break below key technical barriers. Moreover, Japanese officials do not appear to be particularly worried with the currency’s appreciation, so far at least, with Finance Minister Taro Aso noting overnight that the yen’s strength is not abrupt enough to warrant intervention. Another key pair to watch is euro/dollar, which is now hovering very close to its recent highs around 1.2530. Should the bulls manage to overcome that barrier, it would be a bullish signal that may carry larger upside extensions.

Day ahead: US initial jobless claims & industrial production on the agenda

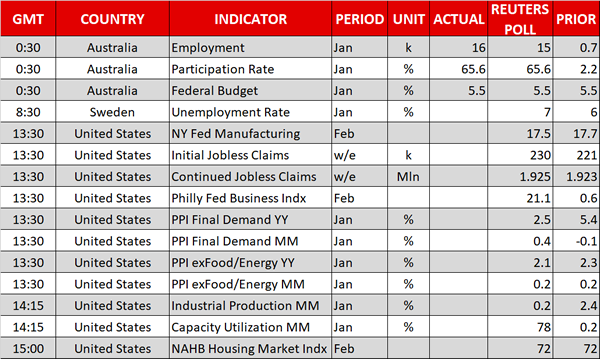

The US will be on the receiving end of relatively important data during Thursday’s trading. Initial and continued jobless claims for the week ending February 10 will be made public at 1330 GMT. First-time benefit claimants are expected to stand at 230k, this being higher by 9k relative to the week that preceded, though yet again below the 300k threshold that’s linked to a healthy labor market. Other data released at the same time include February’s New York Fed manufacturing survey and the Philly Fed business index for the same month, as well as data on producer prices for the month of January.

US industrial production data for January are also of significance. Those are scheduled for release at 1415 GMT. Industrial production is expected to ease, growing by 0.2% on a monthly basis, after beating expectations in December to expand by 0.9% m/m. Manufacturing output, a subset of industrial output, will also be watched, while figures on capacity utilization are also due at the same time. Lastly, February’s National Association of Home Builders Housing Market index will be made public at 1500 GMT.

Out of Canada, the ADP’s nonfarm employment change due at 1330 GMT might attract some interest.

ECB executive board member and chief economist Peter Praet will be participating in a discussion at a conference organized by the French Treasury and the IMF at 1045 GMT. Sabine Lautenschlager, herself an ECB board member, is scheduled to give a speech at Dutch Banking Day 2018 at 1200 GMT. Norway’s central bank governor, Oystein Olsen, will be giving a keynote speech at 1700 GMT. Lastly, Bank of Canada Deputy Governor Lawrence Schembri will be talking at 1830 GMT.

In equities, companies releasing quarterly results will be attracting attention.

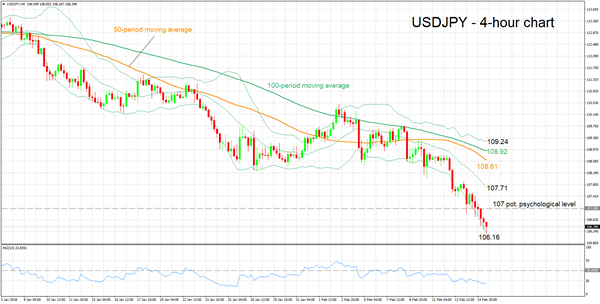

Technical Analysis: USDJPY hits fresh 15-month low; RSI oversold

USDJPY recorded a fresh 15-month low of 106.17 during Thursday’s trading after losing significant ground in previous sessions.

The short-term bias is clearly negative. The RSI is well into bearish territory below 50 on the four-hour chart and is heading lower. Notice though that it has entered oversold territory below 30.

Should Thursday’s data out of the US come in stronger than expected, then the pair might receive a boost. In this case, the area around the 107 handle – a level of potential psychological significance – could act as a barrier to the upside. Stronger bullish movement would shift the focus to the middle Bollinger line – a 20-period moving average line – at 107.71.

Weaker US data could see USDJPY extending its losses. Support could be taking place at the moment around the lower Bollinger band at 106.16 (including the 106 handle that might hold psychological importance). A violation of this area would turn the attention to the range around 105.

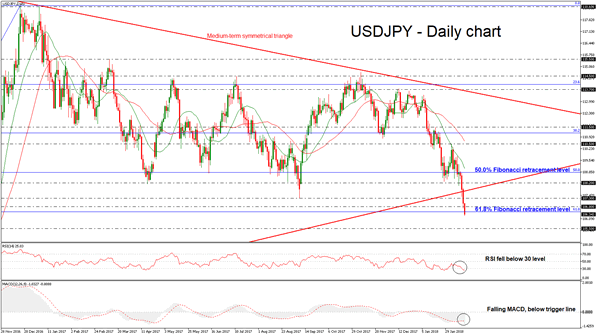

USDJPY Edges Sharply Lower Below Symmetrical Triangle, Records Fresh 15-Month Low

USDJPY dipped sharply lower on Wednesday, while it posted the third red day in a row and created a new 15-month low of 106.29 during today’s Asian session. The aggressive bearish rally started after the fall below the 50.0% Fibonacci retracement level near 108.80 of the up-leg with the low of 98.96 and the high of 118.60 and drove the price below the symmetrical triangle, which has been holding since May 2015. A weekly close below the triangle could reinforce the downside pressure.

Short-term momentum indicators in the daily timeframe are also pointing to a continuation of the bearish bias. The Relative Strength Index (RSI) slipped below the 30 level and is challenging the oversold zone. Also, the MACD oscillator recorded a downside crossover with its trigger line with strong momentum, suggesting further losses.

If prices continue the sharp sell-off, immediate support could come at 105.50, which is taken from the high in October 2016. It is worth mentioning that the price has just hit the 61.8% Fibonacci retracement level near 106.50 and is ready to break it to the downside.

Conversely, in case of an upward correction, the pair needs to go through the medium-term ascending trend line and the 108.20 resistance level. A jump above the aforementioned levels, the price could open the door for the 110.50 obstacle.

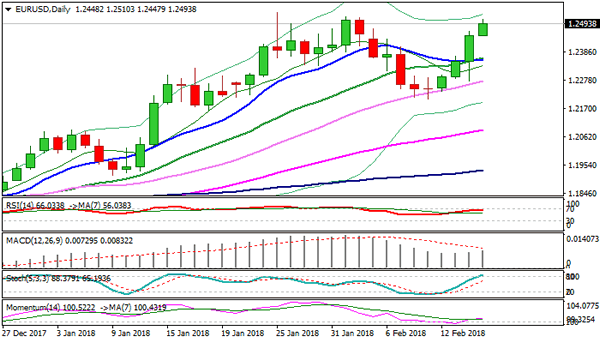

Technical Outlook: EURUSD – Bulls Probe Above 1.25 Barrier, Targets At 1.2537/97 In Focus

The Euro probed above 1.25 barrier in early European session trading on Thursday, extending strong rally from 1.2205 (09 Feb) into fourth straight day.

Euro's bulls were interrupted on Wednesday after stronger than expected US inflation data sent the dollar higher across the board, but rally proved to be short-lived.

Post-data dip to 1.2275 and subsequent swift recovery offered good opportunity to renew existing longs for extension towards targets at 1.2537 (25 Jan new over three-year high) and 1.2597 (Fibo 61.8% of 1.3992/1.0340, May 2014 / Dec 2016 fall).

Rally may show hesitation before breaking through 1.2500/37 zone, however, bulls remain firmly in play and gaining bullish momentum for further advance.

Broken Fibo barrier at 1.2400 now acts as solid support and is expected to keep the downside protected.

Res: 1.2522, 1.2537, 1.2567, 1.2597

Sup: 1.2474, 1.2447, 1.2400, 1.2358

Currencies: Risk Rebound Hammers Dollar

Sunrise Market Commentary

- Rates: Higher CPI sends US 10-yr yield to new cycle high

The global core bond sell-off accelerated yesterday on higher-than-expected US CPI data. US yields set new cycle highs for tenors up to 10-yr. The 10-yr yield closes in on key resistance around 3.05% (2014 high). Today's heavy US eco calendar might set the stage for more losses. Not that much good news is probably needed to do so. - Currencies: Risk rebound hammers dollar

The dollar showed remarkable swings. Higher US CPI and disappointing retail sales attracted bottom fishers in the equities. This equity rebound caused sharp USD selling across the board, even in USD/JPY. The move continues this morning. For now, this repositioning develops independent from the data. For now, the dollar is a falling knife…

The Sunrise Headlines

- Traditional market correlations disappeared after yesterday's combination of higher US inflation and disappointing retail sales. US yields added up to 9 bps, the dollar fainted and US equities skyrocketed (>+1%). Several Asian markets are closed this morning for lunar New Year; the others gain ground as well.

- Oil prices extended gains, pushed up by a weak dollar and by comments from Saudi Arabia that it would rather see an undersupplied market than end a deal with OPEC and Russia to withhold production.

- Japan's Finance Minister Aso says the yen isn't rising or falling abruptly enough for us to intervene now. He couldn't change recent yen strength. USD/JPY dropped towards 106.50.

- Australian employment data printed very close to expectations with a 16k net job creation and a stabilization of the unemployment rate 5.5%. Underlying figures disappointed somewhat as full time jobs were shed (-49.8k).

- Jacob Zuma resigned as President of South Africa, reluctantly heeding orders by the ruling ANC to bring an end to his nine scandal-plagued years in power.

- A bipartisan Senate plan to protect young illegal immigrants from deportation and pour billions of dollars into border security appeared headed toward a Senate showdown on Thursday.

- Today's eco calendar heats up in the US with empire manufacturing, weekly jobless claims, PPI inflation, Philly Fed business outlook and industrial production. Spain and France tap the bond market

Currencies: Risk Rebound Hammers Dollar

Risk-rally hammers USD, despite higher US yields

The dollar made some wild and very remarkable swings yesterday. US CPI printed higher than expected, but retail sales posted at big miss. US yields and the dollar jumped higher immediately after the release. US yields held their gains setting new cycle peaks, but the dollar reversed course soon. An initial decline in equities attracted bottom fishers and kick-started an impressive risk-rebound, despite poor retail sales. This risk rally also hammered the dollar. EUR/USD jumped from the high 1.22 area to close the session at 1.2451. Even USD/JPY remained under pressure despite higher core yields and the equity rally! USD/JPY finished the session at 107.01. The ‘usual correlations' didn't work at all.

Positive risk sentiment and the dollar decline remain at play overnight. Several markets (China, Korea) are closed for the Lunar New year. Japanese equities remarkably joined the global risk rally despite a further decline of USD/JPY and poor December machine orders (-11.9% M/M). USD/JPY is trading in the mid 106 area. EUR/USD trades in the 1.2465 area holding near the overnight peak. The risk rally at least eased the decline of EUR/JPY. The pair hovers in the mid 132 area.

The US eco calendar is again well filled today with Empire manufacturing, Philly Fed business outlook, jobless claims, industrial production and, last but not least the PPI data. Sentiment indicators and activity data are expected to confirm decent growth. PPI is expected to rise 0.4% M/M, but decline from 2.6% to 2.5% on a yearly basis. Good eco data and/or an upward surprise in PPI might reinforce the rise in US yields. However, considering yesterday's price action, it is unlikely to change fortunes for the dollar. The repositioning on equity markets and technical considerations are probably more important. At least for now, risk sentiment correlates with a further decline of the dollar. In this move we also keep an eye at the technicals. EUR/USD is nearing the 1.2537 correction top. A break above this level would signal more trouble for the dollar. We don't see a fundamental reason for EUR/USD to already break this level, but this is not a good enough reason to row against the tide. The dollar is a falling knife. A return below 1.2206 would be a first sign, that the USD sell-off easing.

UK retail sales are expected to rebound 0.6% M/M and 2.4% Y/Y after a sharp setback in January. We doubt that even better than expected data will be a big help for sterling. EUR/GBP holds the 0.8690/0.9033 range, with intermediate resistance at 0.8930. We hold our view that the 0.8690 support won't be easy to break without big progress on Brexit.

EUR/USD nears ST range top

USD Weakens Following US Inflation

US Inflation data was released yesterday, with the initial reaction seeing USD pairs strengthen and Equities selloff. However, once the first 15 minutes had passed, post data, the trend reversed and the USD weakened further while Equities were short squeezed and bid higher. The US 500 Index dropped from 2672.90 to a low of 2627.7 but has since rebounded to highs of 2706.50. Gold sold off from 1330.70 to a low of 1317.20 but rebounded to currently trade around its highs of 1354.00. USDCAD moved higher after the data from 1.25763 to 1.26480 but is now trading at its lows near 1.24808.

German Harmonised Index of Consumer Prices (YoY) (Jan) was released coming in unchanged at 1.4%, as expected. Gross Domestic Product (QoQ) (Q4) was also as expected at 0.6%, from 0.8% previously. Gross Domestic Product (YoY) (Q4) was 2.3% v an expected 2.2%, from 2.3% previously. Gross Domestic Product w.d.a. (YoY) (Q4) was 2.9% v an expected 3.0%, from 2.8% previously.

SNB Governing Board Member Zurbrugg delivered a speech titled “Cash – a means of payment yesterday, today, and tomorrow” at the Bundesbank Cash Symposium in Frankfurt. His comments were: that the central bank is not planning to issue digital currency. He said that digital currencies won't displace cash anytime soon and they do not pose a problem for central banks currently. USDCHF moved higher from 0.93183 to 0.93582 after the comments.

Italian Gross Domestic Product (QoQ) (Q4) was as expected at 1.6%, from 1.7% previously. Gross Domestic Product (YoY) (Q4) was 0.3% v an expected 0.4%, from 0.4% previously.

Eurozone Gross Domestic Product s.a. (QoQ) (Q4) was as expected, unchanged at 0.6%. Gross Domestic Product s.a. (YoY) (Q4) was also as expected at 2.7%, from 2.6% previously, which was revised up to 2.7%. Industrial Production w.d.a. (YoY) (Dec) was released at 5.2% v a consensus of 4.2% and a prior of 3.2%, which was revised up to 3.7%. Industrial Production s.a. (MoM) (Dec) was 0.4% v an expected 0.2%, from 1.0% previously, which was revised up to 1.3%. The EURUSD pair moved lower to 1.23455 after this data.

US Retail Sales (MoM) (Jan) was released coming in at -0.3% against an expected 0.2%, from 0.4% previously. Retail Sales ex Autos (MoM) (Jan) was 0.0% v an expected 0.4%, from 0.4% prior, which was revised down to 0.1%. Retail Sales Control Group (Jan) was 0.0% v an expected 0.4%, from 0.3% prior. Consumer Price Index (MoM) (Jan) was 0.5% v an expected 0.3%, from 0.1% previously, which was revised up to 0.2%. Consumer Price Index (YoY) (Jan) was 2.1% v an expected 1.9%, from 2.1% previously. Consumer Price Index Ex Food & Energy (YoY) (Jan) was 1.8% v an expected 1.7%, from 1.8% prior. Consumer Price Index Ex Food & Energy (MoM) (Jan) was 0.3% v an expected 0.2%, from 0.3% previously, which was revised down to 0.2%. USDJPY went to a high of 107.541 before dropping back to 107.122. EURUSD dropped to 1.22757 from a high of 1.23508. GBPUSD dropped from 1.38874 to a low of 1.37996.

Japanese Machinery Orders (YoY) (Dec) were released at -5.0% with a consensus of 2.2% expected, from 4.1% prior. Machinery Orders (MoM) (Dec) were released at -11.9% with a consensus of -2.3% expected, from 5.7% previously.

At 01:30 GMT, Australian Unemployment Rate s.a. (Jan) came in as expected at 5.5%, from 5.5% previously, which was revised up to 5.6%. The Employment Change s.a. (Jan) was 16.0K v an expected 15.0K, from a previous 34.7K, which was revised down to 33.5K. The Participation Rate (Jan) was as expected at 65.6%, from a previous number of 65.7%. Consumer Inflation Expectation (Feb) was 3.6% from a reading of 3.7% previously.

EURUSD is up 0.14% overnight, trading around 1.24662.

USDJPY is down -0.50% in early session trading at around 106.469.

GBPUSD is up 0.08% to trade around 1.40089.

AUDUSD is up 0.22% overnight, trading around 0.79415.

Gold is up 0.16% in early morning trading at around $1,352.50.

WTI is up 1.10% this morning, trading around $61.36.

Major data releases for today:

At 08:15 GMT, ECB's Mersch will speak and this may impact on moves in EUR crosses.

At 10:45 GMT, ECB's Praet will speak. Comments from the speech may impact EUR crosses.

At 12:00 GMT, ECB's Lautenschlager will speak and any comments made could move EUR pairs.

At 13:30 GMT, US Continuing Jobless Claims (Feb 2) expected at 1.925M from a previous number of 1.923M. Initial Jobless Claims (Feb 9) is expected to come in at 230K with a prior reading of 221K. Philadelphia Fed Manufacturing Survey (Feb) is expected at 21.1 against a prior 22.2. USD crosses could see increased volatility around this data release.

At 14:15 GMT, US Industrial Production (MoM) (Jan) will be released. The consensus is for 0.2% from 0.9% previously. Capacity Utilization (Jan) is also released at this time, with an expectation for 78.0% v 77.9% prior. USD crosses may be impacted by this release.

At 15:00 GMT, US NAHB Housing Market Index (Feb) will be released and is expected to be unchanged at 72. This release may affect USD pairs.

At 18:30 GMT, Canadian BOC Governing Council Member will speak at the Manitoba Association for Business Economics in Winnipeg. Comments may affect CAD crosses.

At 21:30 GMT, New Zealand Business NZ PMI (Jan) is due to be released. The prior number was 51.2. NZD could see an increase in volatility due to this event.

At 22:30 GMT, Australian RBA Governor Lowe will testify before the House of Representatives' Standing Committee on Economics in Sydney. Volatility in AUD crosses is often experienced during his speeches.

At 23:50 GMT, Japanese Foreign Investment in Japan stocks (Jan 5) will be released with a previous number of ¥-126.7B. Foreign Bond Investment (Jan 5) had a prior number of ¥-866.6B.

Investors Shrug Off Inflation Fears

The U.S. inflation figures for January have been anxiously awaited by investors after wage growth sparked a sharp selloff in equity and treasury markets last week over fears of an overheating economy.

Wednesday's data confirmed that inflation in the world's largest economy is on the rise. Headline inflation hit 2.1%, beating the forecast of 1.9%. More importantly, the core CPI, which excludes volatile components like food and energy, rose 0.35% MoM, the biggest monthly rise since 2005, to stay unchanged for the year at 1.8%.

Higher prices are frequently accompanied by an increase in aggregate demand when the economy is at full employment. Making things more interesting, retail sales contracted 0.3% in January. This should become a complex situation for both investors and monetary policymakers if higher inflation accompanies lower spending.

So far, I still see three rate hikes in 2018 as the base case scenario and, in my opinion, this had already been baked into equity prices after last week's selloff. However, the risks are skewed to further monetary tightening and this will be problematic for the still overstretched valuations.

In such an environment, some investors might change their strategy to selling the rallies instead of buying the dips, which wasfollowed throughout last year. This requires a further rally in bond yields, and a significant break of 3% on the 10-year Treasuries will likely drive it.

Yesterday's reversal was quite surprising. Wall Street equities dipped immediately after the release of the data and the S&P 500 opened 0.5% lower to reverse losses within 30 minutes and ended the day 1.35% higher. A similar reaction was seen in European equities which turned to red, but managed to end the trading session in green.

The heightened expectations for rate increases and higher U.S. bond yields should be bullish for the U.S. dollar, particularly against the Yen. What we currently see is exactly the opposite. The Yen is sitting at a 15-month high against the dollar and showing no signs of giving up gains. This suggests investors are still nervous and unwilling to continue with the carry trade where they borrow the Yen at low interest rates in order to invest in higher-yielding currencies.

The dollar did not just decline against the Yen –it fell against a basket of currencies with the DXY falling 1.4% from yesterday's peak. This might be harder to explain when rate differentials widen. Markets seem to be expecting the rate differentials to narrow in the next couple of months, as other central banks begin with the tightening process. However, another spike in U.S. bond yields should start attracting more interest to the greenback.

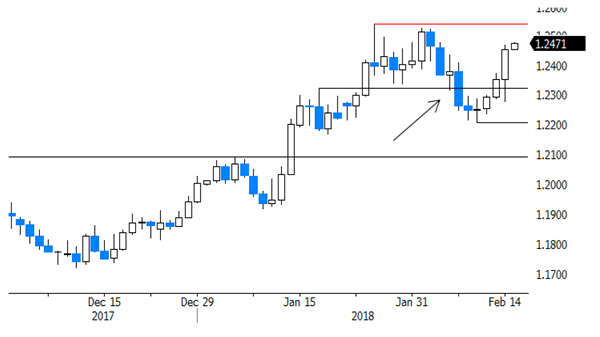

Daily Wave Analysis: EUR/USD Bullish Bounce Retests 1.25 Resistance Zone

Currency pair EUR/USD

The EUR/USD bullish momentum is now approaching the previous top and resistance trend line (red). A break above the resistance could indicate an uptrend continuation within wave 5 (purple).A bull flag pattern or other chart pattern could indicate a pause before the breakout.

The EUR/USD strong pullback is probably a wave 2 (blue) but the bullish reversal is indicating that this is a potential wave 3 (blue).For price to confirm the wave 3 though, there will need to be a bullish break above the resistance trend line and a move towards the 161.8% Fib target.

Currency pair GBP/USD

The GBP/USD made a bullish breakout above the previous tops (dotted orange) and resistance trend line (dotted red) which could indicate the start of wave 5 (green). A break above the next resistance (red) trend line could confirm a bullish breakout.

The GBP/USD bullish break is slow and corrective, which could indicate an ABC pattern rather than a 123. If price manages to stay above support (green/blue), then a 123 is more likely. Otherwise, if the support levels should break, then an ABC is more likely.

Currency pair USD/JPY

The USD/JPYused thesupportzone (dotted green) as resistance and broke below the -27.2% Fibonacci target. Price now has potential space to the next target which is the -61.8% Fib.

The USD/JPYis at the bottom ofa falling wedge pattern which could indicate a potential bullish retracement.

Australia’s Unemployment Rate Ticked Lower In January

For the 24 hours to 23:00 GMT, the AUD rose 0.48% against the USD and closed at 0.7919.

LME Copper prices rose 0.8% or $54.0/MT to $6962.0/MT. Aluminium prices rose 0.7% or $14.5/MT to $2138.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7936, with the AUD trading 0.21% higher against the USD from yesterday's close, after Australia's seasonally adjusted unemployment rate fell to 5.5% in January, at par with market expectations. Unemployment rate had registered a revised reading of 5.6% in the preceding month.

On the other hand, the nation's consumer inflation expectations eased to 3.6% in February, compared to a reading of 3.7% in the prior month.

The pair is expected to find support at 0.7824, and a fall through could take it to the next support level of 0.7712. The pair is expected to find its first resistance at 0.7997, and a rise through could take it to the next resistance level of 0.8058.

Going ahead, traders would keep a close watch on a speech by the Reserve Bank of Australia's (RBA) Governor, Philip Lowe, due overnight.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Economy Grew As Initially Estimated In 4Q 2017, Industrial Production Zoomed In December

For the 24 hours to 23:00 GMT, the EUR rose 0.55% against the USD and closed at 1.2451, after the seasonally adjusted second estimate of the Euro-zone's gross domestic product (GDP) climbed 0.6% on a quarterly basis in the fourth quarter of 2017, confirming the preliminary print, thus suggesting that the region continued to witness strong growth in the final months of last year. In the prior quarter, GDP had registered a revised rise of 0.7%.

Additionally, the region's seasonally adjusted industrial production registered a rise of 0.4% on a monthly basis in December, higher than market expectations for a rise of 0.1%, amid a rise in the output of durable goods and intermediate goods. In the previous month, industrial production had risen by a revised 1.3%.

Separately, preliminary data revealed that economic activity in Germany expanded 0.6% on a quarterly basis in the three months to December 2017, meeting market expectations, owing to a strong pick-up in exports. In the prior quarter, GDP had climbed 0.8%. Moreover, the nation's final consumer price index (CPI) rose 1.6% on an annual basis in January, in line with the flash estimate. The CPI had registered a rise of 1.7% in the previous month.

The US Dollar declined against a basket of major currencies, after latest US economic releases painted a mixed picture of the health of the nation's economy.

Data indicated that consumer price inflation in the US jumped more-than-anticipated by 0.5% on a monthly basis in January, marking its sharpest increase in 5 months, thus offering signs of firming inflation that could force the Federal Reserve (Fed) to move aggressively in raising interest rates. In the prior month, the CPI had registered a revised rise of 0.2%, while markets were anticipating for a gain of 0.3%.

On the other hand, the nation's advance retail sales recorded an unexpected drop of 0.3% in January, dipping to its lowest in nearly a year. Retail sales had registered a revised flat reading in the previous month, while investors had envisaged for a rise of 0.2%. Also, the nation's MBA mortgage applications retreated 4.1% in the week ended 09 February, after recording an increase of 0.7% in the previous week.

In other economic news, business inventories in the US grew 0.4% on a monthly basis in December, topping market expectations for a gain of 0.3%. In the prior month, business inventories had registered a similar rise.

In the Asian session, at GMT0400, the pair is trading at 1.2460, with the EUR trading 0.07% higher against the USD from yesterday's close.

The pair is expected to find support at 1.2333, and a fall through could take it to the next support level of 1.2206. The pair is expected to find its first resistance at 1.2530, and a rise through could take it to the next resistance level of 1.2600.

Looking ahead, traders would keep a close watch on the Euro-zone's trade balance data for December, slated to release in a few hours. Moreover, the US initial jobless claims followed by the industrial and manufacturing production data for January as well as the NAHB housing market index for February, all scheduled to release later in the day, will keep investors on their toes.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

UK Should Address Weak Productivity: IMF

For the 24 hours to 23:00 GMT, the GBP rose 0.62% against the USD and closed at 1.4002.

Yesterday, the International Monetary Fund (IMF) warned that Britain must focus on improving its productivity and international competitiveness in order to weather the shock of Brexit. Further, the Fund noted that weak domestic demand owing to rising inflation has asserted downward pressure on the nation’s economic growth.

In the Asian session, at GMT0400, the pair is trading at 1.4016, with the GBP trading 0.1% higher against the USD from yesterday’s close.

The pair is expected to find support at 1.3870, and a fall through could take it to the next support level of 1.3724. The pair is expected to find its first resistance at 1.4092, and a rise through could take it to the next resistance level of 1.4168.

With no macroeconomic releases in UK today, investor sentiment would be determined by global macroeconomic news.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.