Sample Category Title

UK’s Industrial Production Sank By The Most In Over 5 Years In December

For the 24 hours to 23:00 GMT, the GBP declined 0.98% against the USD and closed at 1.3806 on Friday, after comments from the European Union’s (EU) chief negotiator sparked a fresh wave of uncertainty over Britain’s exit from the EU.

The EU’s chief negotiator, Michel Barnier, warned that a Brexit transition deal may not be in reach for the moment.

Losses in the Pound were extended, after data revealed that UK’s industrial production retreated more-than-anticipated by 1.3% on a monthly basis in December, dropping by the most since September 2012, amid a temporary closure of Britain’s most important pipeline. Industrial production had posted a revised rise of 0.3% in the previous month, while markets were expecting for a fall of 0.9%. Further, the nation’s total trade deficit surprisingly widened to £4.90 billion in December, following a revised deficit of £3.65 billion in the previous month. Markets were anticipating the nation to register a total trade deficit of £2.40 billion.

On the contrary, the nation’s manufacturing production grew 0.3% on a monthly basis in December, meeting market expectations. In the previous month, manufacturing production had risen by a revised 0.2%. Moreover, the nation’s construction output recorded an unexpected rise of 1.6% MoM in December, driven by an upturn in infrastructure projects. Construction output had registered a revised rise of 0.1% in the prior month, while investors had envisaged for a fall of 0.1%.

In other economic news, leading think tanker, NIESR estimated that UK’s gross domestic product (GDP) advanced 0.5% in the three months to January, at par with market expectations and compared to a rise of 0.6% in the October-December 2017 period.

In the Asian session, at GMT0400, the pair is trading at 1.3861, with the GBP trading 0.4% higher against the USD from Friday’s close.

The pair is expected to find support at 1.3755, and a fall through could take it to the next support level of 1.3649. The pair is expected to find its first resistance at 1.3977, and a rise through could take it to the next resistance level of 1.4093.

With no macroeconomic releases in Britain today, investor sentiment would be governed by global macroeconomic events.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Japanese Yen Reverses Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.36% against the JPY and closed at 108.49 on Friday.

In the Asian session, at GMT0400, the pair is trading at 108.71, with the USD trading 0.2% higher against the JPY from Friday’s close.

The pair is expected to find support at 108.07, and a fall through could take it to the next support level of 107.43. The pair is expected to find its first resistance at 109.33, and a rise through could take it to the next resistance level of 109.95.

Going ahead, traders would focus on Japan’s flash machine tool orders data for January, due to release tomorrow.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Swiss Franc Trading Higher, Ahead Of Swiss Inflation Data

For the 24 hours to 23:00 GMT, the USD rose 0.17% against the CHF and closed at 0.9387 on Friday.

Macroeconomic data revealed that Switzerland’s seasonally adjusted unemployment rate remained unchanged at 3.0% in January, in line with market expectations.

In the Asian session, at GMT0400, the pair is trading at 0.9380, with the USD trading 0.07% lower against the CHF from Friday’s close.

The pair is expected to find support at 0.9356, and a fall through could take it to the next support level of 0.9331. The pair is expected to find its first resistance at 0.9407, and a rise through could take it to the next resistance level of 0.9433.

Ahead in the day, market participants would keep a close watch on Switzerland’s inflation numbers for January.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Canada’s Unemployment Rate Unexpectedly Rose In January, Number Of People Employed Dipped To A 9-Year Low In The Same...

For the 24 hours to 23:00 GMT, the USD rose 0.15% against the CAD and closed at 1.2615 on Friday.

The Canadian Dollar declined against the USD on Friday, following downbeat Canadian labour market report.

Data revealed that Canada's unemployment rate surprisingly advanced to a level of 5.9% in January, while investors had envisaged it to remain steady at a revised level of 5.8%. Additionally, net number of people employed in the nation recorded an unexpected drop of 88.0K in January, posting its steepest drop since January 2009. The net number of people employed had increased by a revised 64.8K in the prior month, while markets had anticipated for an advance of 10.0K.

In the Asian session, at GMT0400, the pair is trading at 1.2559, with the USD trading 0.44% lower against the CAD from Friday's close.

The pair is expected to find support at 1.2517, and a fall through could take it to the next support level of 1.2475. The pair is expected to find its first resistance at 1.2643, and a rise through could take it to the next resistance level of 1.2727.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Market Update – Asian Session: Markets Stabilize Mostly Higher After Last Weeks Volatility

Headlines/Economic Data

General Trend:

USD/JPY volatility muted amid Japanese holiday

Singapore exchange falls most since Nov 2008, as exchanges in India announced plans to end licensing of data

Hong Kong property developer (Shui On Land) M&A canceled on recent ‘turbulence’ and volatility in the capital and debt markets

Energy company CNOOC to be added to Hang Seng China Enterprises Index

WTI Crude Oil Futures gain over 1% after falling below $60/bbl on Friday

Chinese airlines higher on stronger yuan

Taiwan, China, Hong Kong and South Korea will start to wind down ahead of Lunar New year holiday, starting mid-week: China’s Lunar New Year begins on Friday, Feb 16th

(CN) Moody’s Report: Says the impact of intensified regulation [in China] is no longer limited to the de-risking of the financial sector, but now starting to impact supply of credit to the real economy

Key data due later this week: US Jan CPI and Retail Sales data due to be released on Wed, Feb 14th

Australia Jan Employment Change due for release on Thursday, Feb 15th

Japan

Nikkei 225 closed for holiday

(JP) Reportedly Japan govt set to reappoint Kuroda as Gov of BOJ to a new 5-year term (as expected) - Kyodo News

(JP) Japan government said to consider promoting current BoJ Exec Dir Amamiya to the position of Deputy Gov – Japanese Media

JR East [9020.JP] union said to consider strike related to pay levels - Japan Press

Korea

Kospi opened +0.7%

Financials trade generally higher: Hana Financial, KB Financial and Industrial Bank of Korea all gain by more than 1%

Samsung Electronics gains over 1.5%

(KR) South Korea sells KRW850B 5-year bonds:pre-issuance yield 2.55%

(KR) Bank of Korea (BoK) sells KRW910B in 1-year monetary stabilization bonds(MSBs): yield 1.90%

Samsung, 005935.KR More funds of Chairman Lee Kun-hee found in borrowed name accounts -Korean press

(KR) According to the Korea Automobile Manufacturers Association rising costs have become a growing source of concern for carmakers operating in South Korea

(KR) South Korea Trade Ministry: will seek ways to better protect investor rights from arbitrary regulations when holding talks with China to expand the scope of the two countries' free trade agreement to the service and investment sector - Korean press

China/Hong Kong

Hang Seng opened +0.7%, Shanghai Composite +0.1%

Hang Seng Information Tech Index +2%, Services +1.6%, Consumer Goods +1.5%, Materials +1.2%; Energy -0.8%, Property/Construction -0.2%

Shanghai Property Sub-index has moved between gains and losses after dropping over 6% on Friday

(CN) China Banking Regulatory Commission (CBRC) official: Tighter financial regulations have prompted Chinese banks to apportion greater resources to the real economy and improve the overall quality of financial services while keeping risks at controllable levels – CD

(CN) Asset manager under the State Council, China Chengtong Holdings Group Ltd Official: Planning to bring in more private capital to finance the mixed-ownership reform of the country's State-owned enterprises

(CN) China Banking Regulatory Commission (CBRC) reports 2017 Commercial Non-performing Loan Ratio (NPL) 1.74%

(CN) China to allow states to keep electric car subsidies and cap local subsidies at 50% of central govt level

(CN) China National Development and Reform Commission (NDRC) pledges there willbe an adequate supply of coal throughout the Spring Festival holiday season,after four top coal producers recently struggled to keep up with demand and raised prices

(CN) China National and Development Reform Commission (NDRC) spokeswoman: To create millions of new jobs under "employment first" policies

(CN) China PBoC: Skips Open Market Operation (OMO) for the 13th straight session

USD/CNY (CN) PBOC SETS YUAN REFERENCE RATE AT 6.3001 V 6.3194 PRIOR

(CN) China National Development and Reform Commission (NDRC): Releases list of sensitive areas where it intends to restrict overseas investments, putting a specific curb on deals related to real estate, hotels, cinema, entertainment, sports clubs

Looking Ahead: China Jan New Loans data may be released during Monday’s European session

Australia/New Zealand

ASX 200 opened flat; closed %

ASX 200 Utilities Index -2%, Telecom -1%, Consumer Discretionary -0.8%, Energy -0.7%, Financials -0.6%; Resources +0.8%

(NZ) New Zealand Jan CardSpending Retail M/M: 1.4% v 0.5%e; Card Spending Total M/M: 0.6% v 0.2% prior

JPHi-FI, JBH.AU Reports H1 (A$) net 151.7M v148Me; Rev 3.69B v 3.6Be

Ansell, ANN.AU Reports H1 Net $428.2M* v$69.8M y/y, Rev $722.2M v $664M y/y

(AU) Australia starts commission to examine its banks' misconduct - press

AUD/USD CBA sees A$ close to A$0.83 by the end of 2018

Looking Ahead: RBA Assistant Gov Ellis may speak on Tuesday

North America

(US) OMB Head Mulvaney comments ahead of US budget release: Budget to seek $3.0T cut in deficit over 10 years [**Note:President Trump is expected to release his 2019 budget proposal on Monday, Feb12th]

(US) White House: 2019 budget plan will project 3% growth; Projects 3.2% growth to 2020, 3% to 2025, and 2.8% to 2029

(US) Said that the White House is sticking with its calls for sharp cuts to non-defense programs, even after the Congress budget deal lifted spending caps on domestic spending by $300B over the next 2-yrs – Politico

(US) US budget is said to not project a balance in 10-years, according to a Washington Post report.

CDK Global [CDK]: Reportedly Carlyle Group/Silver Lake consortium are near agreement to acquire CDK Global; could be valued at over $10B – press

Fox [FOXA]: Comcast said to consider restarting approach of Fox - US financial press

Broadcom said to receive up to $100B in debt financing for bid for Qualcomm - US financial press

Europe

Ryanair [RYA.UK] CEO O'Leary warns British investors will be forced to sell stock in hard Brexit - UK press; To keep its planes flying in EU, Ryanair must demonstrate to European regulators that a majority of investors are EU citizens. Currently, 56% of shareholders are European, and within that about 20% are from the UK.

(UK) BoE Chief Economist Haldane reiterated BoE is in ‘no rush’ to raise rates– financial press

(UK) George Soros said to pledge an additional £100K for anti-Brexit group – UK Press

(DE) German Central Bank (Bundesbank): Decision to hold some currency reserves in Chinese yuan is part of a long-term strategy, and the investment will be effected as long as the preparations have been completed - Xinhua interview

(DE) Fitch affirms Germany AAA; outlook stable (from Feb 9th)

(EU) ECB's Nowotny (Austria): Concerned about attempts by the US to politically influence the exchange rate, his was a theme addressed at Davos and will be discussed again at the upcoming G20 summit

(EU) ECB’s Visco (Italy): ECB will be patient in pursuit of its inflation target; its been difficult to push up inflation expectations; FX volatility is a major risk to the inflation outlook(from Feb 10th)

(IE) Ireland Jan Consumer Confidence Index: 110.4 v 103.2 prior

(IE) Ireland Jan Construction PMI: 61.4 v 58 prior

GKN [GKN.UK]: Expected to announce cash payout plans to shareholders this week, as it works to stave off Melrose's £7B hostile takeover bid - FT

Looking Ahead: OPEC Monthly Report may be released during Monday’s European session

Levels as of 01:00ET

Nikkei225 closed, Hang Seng +0.6%; Shanghai Composite +0.7%; ASX200 -0.3%, Kospi +1.2%

Equity Futures: S&P500 +0.7%; Nasdaq100 +0.5%,Dax +0.6%; FTSE100 +0.5%

EUR 1.2297-1.2243; JPY108.93-108.56; AUD 0.7839-0.7804;NZD 0.7277-0.7239

Apr Gold +0.8% at $1,325/oz; Mar Crude Oil +1%at $59.80/brl; Mar Copper +1.1% at $3.08/lb

GBP/JPY Daily Outlook

Daily Pivots: (S1) 148.57; (P) 150.66; (R1) 152.42; More...

Intraday bias in GBP/JPY remains on the downside for the moment. Current fall from 156.59 short term top should target 146.96 support. Considering bearish divergence condition in daily MACD, firm break of 146.96 will be another sign of medium term trend reversal. On the upside, break of 154.03 resistance is needed to confirm completion of the fall. Otherwise, outlook will remain cautiously bearish even in case of recovery.

In the bigger picture, as long as 146.96 key support holds, medium term outlook remains bullish. Rise from 122.36 is in favor to extend to 61.8% retracement of 195.86 to 122.36 at 167.78. However, break of 146.96 support will indicate trend reversal after rejection by 55 month EMA. In that case, deeper fall would be seen to 38.2% retracement of 122.36 to 156.59 at 143.51 and then 61.8% retracement at 135.43.

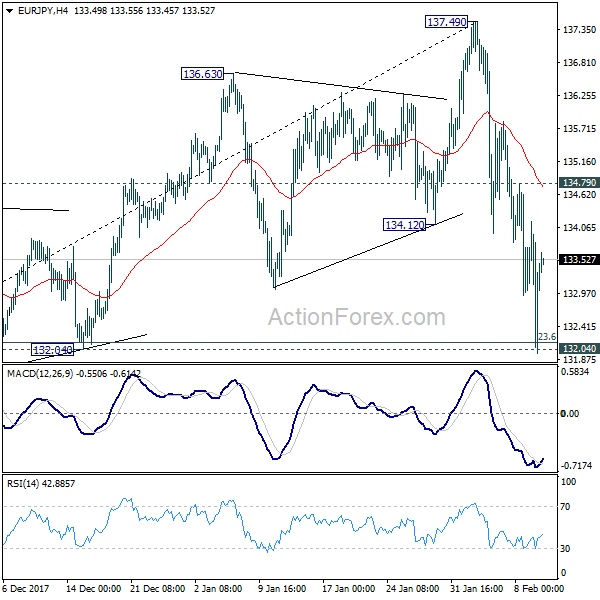

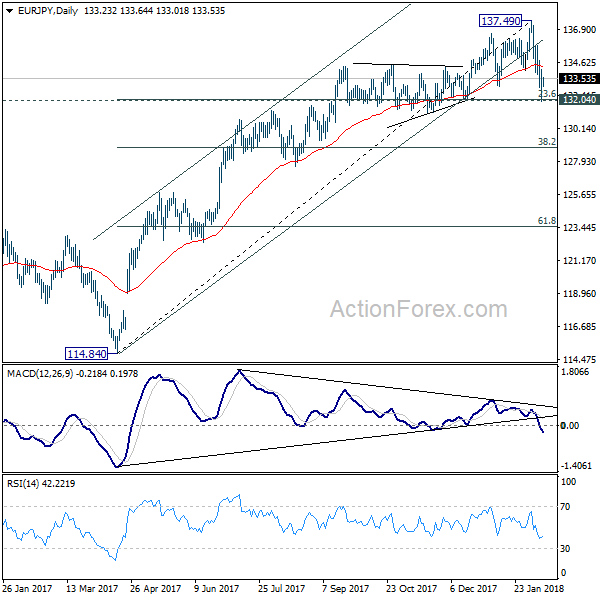

EUR/JPY Daily Outlook

Daily Pivots: (S1) 132.11; (P) 133.13; (R1) 134.29; More....

Intraday bias in EUR/JPY is turned neutral with 4 hour MACD crossed above signal line. At this point, deeper decline is expected as long as 134.79 resistance holds Decisive break of 132.04 cluster support (23.6% retracement of 114.84 to 137.49 at 132.14) will indicate larger trend reversal on bearish divergence condition in daily MACD. In such case, outlook will be turned bearish for 38.2% retracement at 128.38 first. Nonetheless, rebound from 132.04 will retain near term bullishness. Break of 134.79 minor resistance will bring retest of 137.49 high instead.

In the bigger picture, bearish divergence condition in week EMA indicates lost up medium term up trend momentum. But there is no clear sign of completion of up trend from 109.03 yet. Break of 137.49 will target 141.04/149.76 resistance zone. However, sustained break of 132.04 will be the early sign of long term reversal and should bring deeper fall back to retest 124.08 key support level.

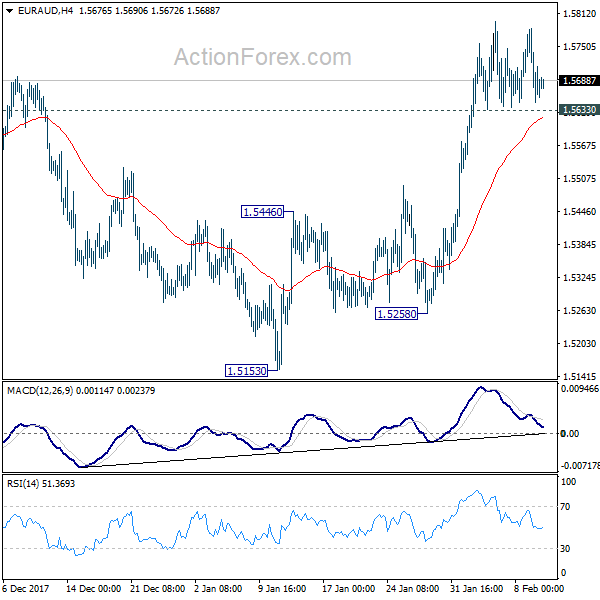

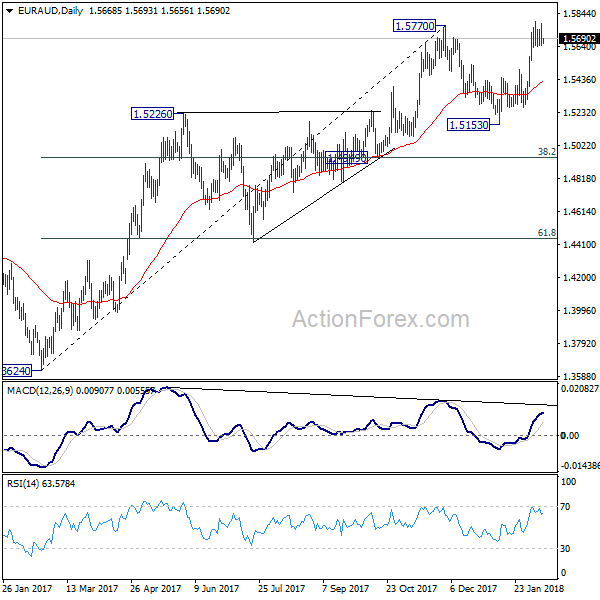

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5619; (P) 1.5701; (R1) 1.5756; More....

No change in EUR/AUD's outlook. Further rise is expected as long as 1.5633 minor support holds. Sustained trading above 1.5770 will confirm resumption of medium term rise from 1.3264. In that case, EUR/AUD should target 1.6587 key long term resistance. However, below 1.5633 minor support minor support will dampen this bullish case and turn bias to the downside.

In the bigger picture, medium term rise from 1.3624 is not completed yet. Break of 1.5770 will extend the rise to retest 1.6587 (2015 high). However, considering bearish divergence condition in daily MACD, sustained break of 1.4949 cluster support (38.2% retracement of 1.3624 to 1.5770 at 1.4950) will indicate medium term reversal. And there is prospect of retesting 1.3624 low in that bearish case.

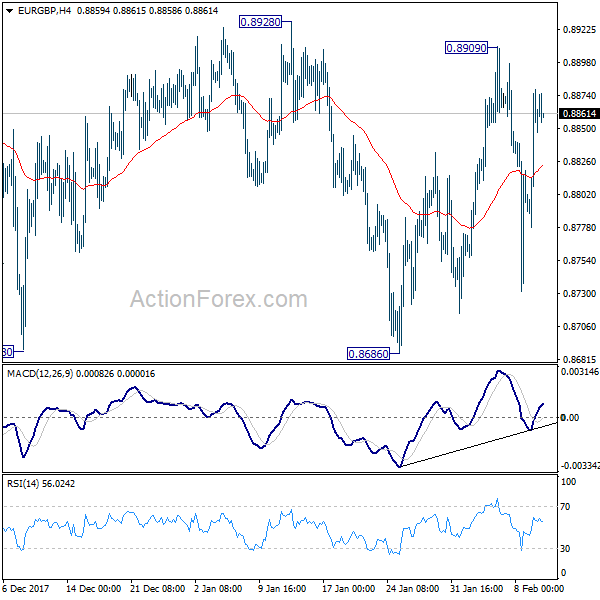

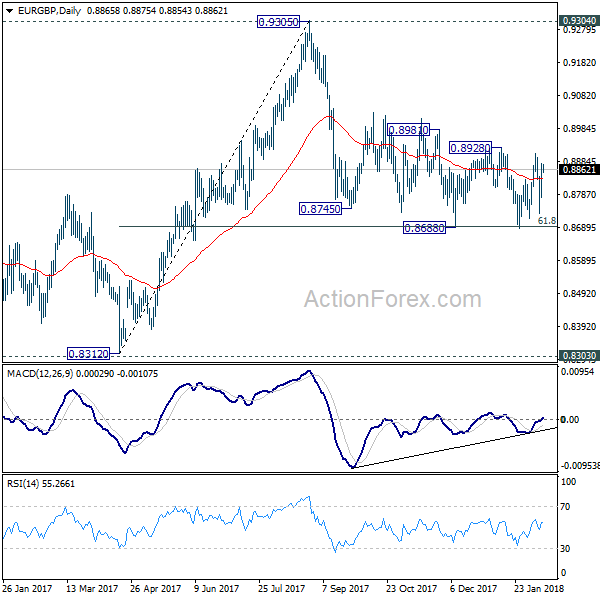

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8798; (P) 0.8838; (R1) 0.8899; More...

Intraday bias in EUR/GBP remains neutral as range trading continues. Near term outlook will remain mildly bearish as long as 0.8928 resistance holds. On the downside, firm break of 0.8686 will resume whole decline from 0.9305. As 61.8% retracement of 0.8312 to 0.9305 should then be taken out too. Deeper decline would be seen to retest 0.8303/8312 support zone. Nonetheless, on the upside, break of 0.8928 will indicate near term reversal and turn outlook bullish for 0.9304 resistance.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

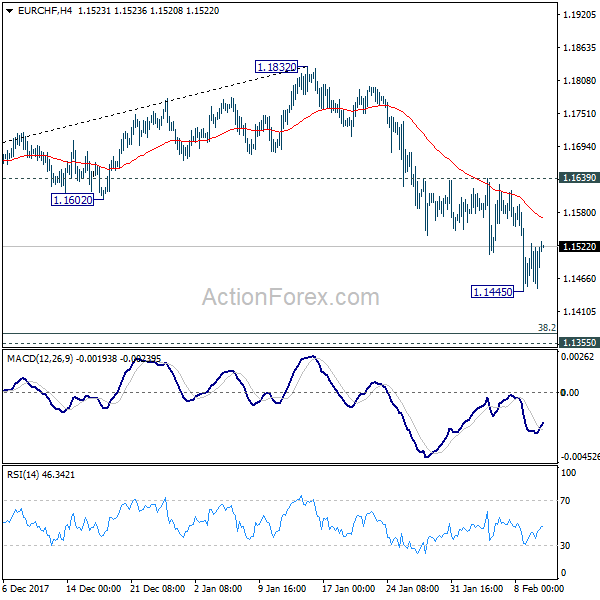

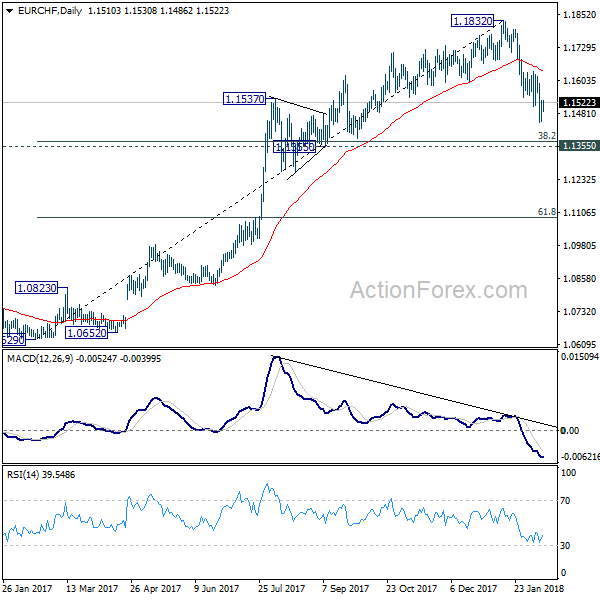

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1460; (P) 1.1493; (R1) 1.1538; More...

Intraday bias in EUR/CHF is turned neutral with a temporary low in place at 1.1445. Deeper decline is expected as long as 1.1639 resistance holds. Below 1.1445 will extend the corrective fall from 1.1832 to 1.1355 cluster support (38.2% retracement of 1.0629 to 1.1832 at 1.1372.) At this point, we'd expect strong support from there to contain downside and bring rebound.

In the bigger picture, a medium term top should be in place at 1.1832 on bearish divergence condition in daily MACD. But there is no indication of long term reversal yet. As long as 1.1198 resistance turned support holds, we'd still expect another rise through prior SNB imposed floor at 1.2000.