Sample Category Title

Summary 2/12 – 2/16

Monday, Feb 12, 2018

[php_everywhere] [/php_everywhere]

Tuesday, Feb 13, 2018

[php_everywhere] [/php_everywhere]

Wednesday, Feb 14, 2018

[php_everywhere] [/php_everywhere]

Thursday, Feb 15, 2018

[php_everywhere] [/php_everywhere]

Friday, Feb 16, 2018

[php_everywhere] [/php_everywhere].

Why Has Gold Remained Indifferent to Stock Market Volatility?

The classic narrative that safe havens rally when stocks plunge is on shaky legs right now. While major US equity indices have dropped roughly 10% in a matter of days, gold has actually moved lower over the same period, leaving most investors puzzled. Why has gold's response been so muted, and what do the cards hold for the precious metal moving forward?

A variety of factors can be blamed for gold's indifference to the market turbulence. First and foremost is the recovery in the US dollar. Gold is traded in dollars, which implies that when the dollar gains in value, the yellow metal becomes more expensive for investors using other currencies, thereby decreasing its appeal. Moreover, expectations of higher inflation and higher interest rates have probably hurt demand for the precious metal. While gold has traditionally been considered a hedge against inflation, speculation that the Fed will raise interest rates faster as a result of higher inflation is weighing on gold. Since gold pays no interest to hold, it becomes less attractive in an environment of rapidly rising rates.

Another narrative is that investors consider the correction in stock markets as being "healthy". Even though they are piling out of equities, the selloff doesn't reflect a lack of optimism about the economy's prospects, but rather the reality of stretched valuations in equities (or in other words, equities being "expensive"). Thus, they have little need to increase their exposure to safe havens like gold, as they may expect the selloff to remain contained in stocks, and perhaps end relatively soon.

Having said all of the above, gold is not necessarily headed lower from current levels. While market participants may largely view this as a "stocks crisis" and have thus not moved into safe havens, that could change very quickly in case the equity turmoil develops into "panic". Moreover, continued market volatility may see the Fed become more conservative about raising rates, for fear of amplifying the selloff further. A more cautious Fed could work against the dollar, and by extent in favor of gold prices.

On another note, concerns regarding the ballooning US budget deficit and long-term debt sustainability have become increasingly more evident recently, as US Treasury yields surged. It thus appears that money is flowing out of both the bond and the equity markets (the two largest markets by far), with investors potentially increasing their cash reserves and waiting for new opportunities. In such an environment, gold and other precious metals could attract some inflows, as an alternative to cash.

In terms of technical levels to watch, the $1300 – $1305 territory will probably serve as the proverbial "line in the sand" regarding further declines or a rebound. Should prices move below the psychological $1300 mark, that would be a negative sign, which could raise the probability for further declines in the metal. On the other hand, a potential rebound from that area would confirm its validity as a support, and may increase the likelihood for a recovery.

Summing up, in the scenario that the equity selloff intensifies, or that the US dollar resumes its downtrend, then gold prices could rebound. A break above $1320 could target the $1350 level as a resistance. A move above that hurdle as well is likely to pave the way for a test of gold's recent high, at $1366.

Conversely, should the market turbulence subside, or if the greenback continues to recover, gold could break below $1300 and potentially test the $1289 zone. Further downside may see scope for extensions towards the $1270 territory, identified by the lows of mid-November.

Weekly Economic and Financial Commentary: Economic Data Stay the Course

U.S. Review

The Economic Calendar Was Quiet this Week

- It was a light week in terms of new economic data, but the main indicators we got all came in above expectations and point to a strong underlying domestic economy.

- The ISM non-manufacturing index hit a cycle high in January, signaling a strong start to 2018 for businesses. The headline was helped by a bump in new orders, suggesting current business optimism has legs for the next few months.

- The United States' trade deficit widened further in December, as import growth outweighed growth in exports. Domestic and global demand have strengthened.

Economic Data Stay the Course

The few readings on the economy this week continued the string of positive news about underlying economic fundamentals. The ISM non-manufacturing index posted a solid rebound in January after service sector activity took a breather in November and December. The headline rose to hit a new cycle high of 59.9. The improvement in new orders was the main driver of the recovery, but the breadth of positive responses across industries was also notable. The new orders index rose 8.2 points to a reading of 62.7 in January, which is the strongest since 2011. Business activity was up, measured by the business activity index and the tone of the comments in the press release. Many noted optimism stemming from the tax changes, and also that prices were picking up. Indeed, the nonmanufacturing prices paid index rose on the month, following the manufacturing survey in pointing to a stronger price pressure environment. January is often when businesses test pricing power, so we will follow this closely in months ahead to see if it holds.

The ISM non-manufacturing employment component hit a fresh series high of 61.6 in January, which is a very promising sign for hiring. The Department of Labor also released the Job Openings and Labor Turnover Survey (JOLTS) for December. The number of available jobs open at the end of the year declined on the month, drifting further from its likely high-water mark posted in October. The hiring rate has yet to reflect much of a shift in trend. Turnover as measured by total separations rose despite a drop off in the number of layoffs. The number of workers that left their jobs voluntarily during the month was at its cycle high. That suggests a rising sense of optimism about job prospects elsewhere, which should also come with pay increases. The number of quitters jumped solidly but resulted in only a slight increase in the quit rate, or quits share of total employment, which remained bound in the 2.1-2.2 percent range for the 12th month in December. We expect this rate will break out to the upside in 2018 as the available labor supply shrinks further, prompting hiring managers to offer higher wages that entice those already employed to leave for more lucrative pastures. This underpins our call that inflation will firm this year, prompting the Fed to raise interest rates three times.

The global economy is currently experiencing synchronous growth, as most nations are seeing rising demand. The upswing in demand overseas along with the weakening of the U.S. dollar has been a boon for U.S. exports, which rose 1.8 percent in December to their highest point on record. American demand propelled a 2.5 percent monthly rise in imports, which resulted in a larger than expected widening of the U.S. trade deficit. The larger widening of the deficit in Q4 may result in trade taking a larger chunk off Q4 GDP than the 1.13 percentage points estimated in the advance GDP report. Still, the larger volume of trade between the U.S. and the rest of the world is a positive for both domestic and foreign economies, even if it results in a slight drag from trade in the GDP calculations. The consumer credit report was also released this week. It showed a slight cool down in December following November's cycle-record increase, when Americans racked up credit card balances for the holidays.

U.S. Outlook

CPI • Wednesday

The Consumer Price Index (CPI) increased 0.2 percent in December, following November's stronger 0.4 percent gain. Contributing to relatively slower growth on the month was a 0.8 percent decline in gasoline prices. Core inflation, which excludes the volatile food and energy prices, increased in December by 0.2 percent. Core goods prices increased 0.2 percent, helped by increases in vehicle and prescription drug prices. Services also helped core inflation, with shelter costs growing by a larger-than-usual 0.3 percent.

Low levels of inflation have been the primary concern in the Fed's move to raise interest rates. However, inflation has shown a stronger trend recently, at a 2.5 percent three-month annualized pace, with core inflation at 2.3 percent. We expect consumer prices to jump to a stronger pace as we move into the spring. Should inflation pick up as we expect it to, the Fed's concern of low inflation should dissipate and continued rate hikes should follow.

Previous: 0.2% Wells Fargo: 0.3% Consensus: 0.3% (Month-over-Month)

PPI • Thursday

The Producer Price Index (PPI) declined 0.1 percent in December to close 2017. This marks the first contraction in producer prices since August 2016 and follows five consecutive monthly gains. The drop was driven by the first decline in services prices in 10 months. Food prices fell 0.7 percent, trade services declined 0.6 percent and energy prices were unchanged on the month. Excluding these three components, the PPI recorded a slight 0.1 percent gain in December and is up 2.3 percent over the year.

Despite December's headline decline, the PPI exhibited strong growth in 2017. Commodity prices have trended higher overall, and the economy is showing signs of promise behind more job gains and historically high levels of confidence among both consumers and businesses. For these reasons, we believe producer prices should continue their upward momentum into this year.

Previous: -0.1% Wells Fargo: 0.4% Consensus: 0.4% (Month-over-Month)

Housing Starts • Friday

Housing starts fell drastically in December by 8.2 percent. However, this appears to be due to winter volatility, as November's starts were exaggerated to the upside due to unseasonably warm weather. The December slowdown was fully driven by single-family starts that fell 11.8 percent, while multifamily starts rose 1.4 percent. For the whole of 2017, starts rose 2.4 percent thanks to an 8.4 percent increase in single-family starts.

Housing permits were stronger than starts to close the year, indicating a likely ramp-up in homebuilding to start 2018. We expect tax reform and rising construction input costs to lead to a shift away from higher-priced homes in 2018. We call for single-family starts to rise 10.8 percent in 2018, and we have also boosted our multifamily forecast as tax reform should bolster apartment demand further.

Previous: 1,192K Wells Fargo: 1,234K Consensus: 1,228K (SAAR)

Global Review

Balancing Growth & Inflation: Central Bank Challenges

- The Bank of England kept its main policy rate steady at its meeting this week, but still above-target inflation and diminishing slack led policymakers to adopt a hawkish tilt.

- The Reserve Bank of India also kept monetary policy unchanged, though stronger inflation has accompanied the turnaround in economic growth that took place at the end of last year.

- Canadian employment growth came crashing back down to Earth in January after two strong previous months. Encouragingly, full-time employment rose by 49,000, although part-time employment fell by 137,000.

Balancing Growth & Inflation: Central Bank Challenges

Across the pond, the Bank of England held its main policy rate steady at its meeting this week, but upward revisions to the central bank's growth forecast and hawkish commentary caused sovereign bond yields to jump. The policy statement noted that the U.K. economy "has only a very limited degree of slack" amid an increasingly broad-based recovery. Robust foreign demand and a weak currency have aided economic growth; data on manufacturing output released this morning showed production rising for the eighth consecutive month, the longest streak in three decades. Additional data released today showed U.K. exports climbing a strong 11 percent in 2017.

Inflation continues to run above the 2 percent target, mostly due to sterling's depreciation post-Brexit (top chart). This combination of diminishing slack and above-target inflation has "diminished the trade-off that the MPC is required to make," an implicit nod to tighter monetary policy on the horizon. For more on the MPC and our international rate outlook, see this week's Interest Rate Watch on page 6.

The Reserve Bank of India (RBI) also held its main policy rate steady at 6.0 percent this week. A slowdown in both economic growth and inflation brought on roughly 200 bps in policy rate easing over the past few years. More recently, however, inflation has strengthened across a broad range of categories, and economic growth in Q3-2017 reversed a slowdown that had stretched for five consecutive quarters (middle chart).

The fading effects from demonetization and a solid global growth backdrop should bode well for the Indian economy, though the RBI notes that rising commodity prices could act as a drag on aggregate demand if sustained. The policy statement finished by noting that "the Committee is of the view that the nascent recovery needs to be carefully nurtured and growth put on a sustainably higher path" suggesting the RBI is in a wait-and-see mode in regards to monetary policy.

Elsewhere, Canadian employment came crashing back down to Earth, falling by 88,000 jobs in January. As we noted in last week's international outlook, November-December saw the second-strongest two-month period of job growth, so some payback this month was likely inevitable. That said, the decline far outstripped even the most pessimistic of forecasters, with the monthly contraction in payrolls resembling the declines seen during the throes of the Great Recession (bottom chart).

Part-time employment declined 137,000 in January, the largest decline in part-time employment on record. The run-up and subsequent collapse in part-time employment growth over the past few months suggests some seasonal/timing quirks around the turn of the year. Encouragingly, full-time employment actually rose 49,000 in January, higher than December (23,200) or November (35,500). Smoothing through the monthly volatility, total monthly employment growth has averaged about 19,000 over the past three months, more or less in-line with the 21,000 averaged over the previous three-month period from August-October.

Global Outlook

Japanese GDP • Wednesday

Real GDP in Japan has risen on a sequential basis for seven consecutive quarters, the longest unbroken string in 16 years. Although it appears that real GDP growth slowed in the fourth quarter, we estimate that the economy continued to expand for an eighth consecutive quarter. Although real GDP was up only 2.1 percent on a year-ago basis in Q3-2017, the expansion has generally been broad based across spending categories, which makes it more sustainable. Indeed, we look for the expansion to continue through 2018 and 2019.

Private non-residential fixed investment spending was up 4.0 percent on a year-ago basis in Q3. On Thursday, December data on core machinery orders, which are a good leading indicator of fixed investment spending, will be released. The outturn will give analysts some insights into the current state of capital spending.

Previous: 2.5% Wells Fargo: 2.1% Consensus: 1.0% (SAAR)

Eurozone Industrial Production • Wed

Industrial production (IP) in the Eurozone accelerated in 2017. Indeed, IP in the October-November period was up 3.5 percent on a year-ago basis. Data slated for release on Wednesday will show how IP in the euro area ended the year. Although we already have preliminary GDP data for the fourth quarter—real GDP grew 2.7 percent (year-over-year) in Q4-2017—the IP data will give analysts some insights into the momentum the industrial sector had coming into 2018.

Speaking of GDP growth, the first disaggregation of Eurozone GDP into its demand-side components will be available on Wednesday, and many individual economies in the Euro area will release their own GDP data as well. France will print its labor market report for the fourth quarter on Thursday.

Previous: 1.0% Consensus: 0.0% (Month-over-Month)

U.K. Retail Sales • Friday

Consumer spending in the United Kingdom decelerated markedly last year. The sharp depreciation of the British pound in the aftermath of the Brexit referendum in June 2016 lifted inflation and eroded consumer purchasing power. As growth in real income slowed, so too did growth in consumer spending. Data on retail spending in January that are on the docket on Friday will offer some insights into the state of consumer spending early in 2018.

The value of sterling has stabilized over the past year, and the impulse to inflation from exchange rate depreciation is fading. Consequently, we expect CPI inflation to recede in coming months from its current rate of 3.0 percent. CPI data for January that are slated for release on Tuesday will show if this process has started yet. Producer price data for January, which will also print on Tuesday, will offer further insights into the current inflation dynamics in the British economy.

Previous: -1.5% Consensus: 0.6% (Month-over-Month)

Point of View

Interest Rate Watch

Bank of England Turns Hawkish

The Monetary Policy Committee (MPC) at the Bank of England held a policy meeting on February 8 and, as widely expected, the MPC voted unanimously to keep policy unchanged. Specifically, the MPC voted 9-0 to keep the Bank's main policy rate (i.e., Bank Rate) unchanged at 0.50 percent, where it has been maintained since November (top chart).

However, the MPC sounded hawkish in the statement that it released after the meeting. The MPC said that "the U.K. economy has only a very limited degree of slack" and that "domestic inflationary pressures are expected to rise." Therefore, the MPC projects that monetary policy will need to be tightened "somewhat earlier" and "by a somewhat greater extent" than it deemed appropriate three months ago.

Accordingly, we have made some changes to our U.K. interest rate outlook. We had thought that the MPC would wait until Q4 of this year before hiking rates again, but we have moved up the next rate hike to Q3. In addition, we now see the Bank Rate at 1.50 percent at the end of 2019 rather than at 1.25 percent. The 10-year government bond yield in the United Kingdom has followed comparable yields in the United States and Germany higher over concerns of higher inflation (middle chart), and we have made some adjustments to our forecast for gilt yields.

We have not made any changes to our outlook for ECB policy, at least not at this time. The Governing Council has said that it intends to buy €30 billion worth of bonds per month, and we take ECB policymakers at their word (bottom chart). But we believe the Governing Council will decide to wrap up its quantitative easing program rather quickly, and look for it to cease buying bonds by year-end 2018. We also think the ECB will not waste much time in hiking rates. We look for the Governing Council to raise its deposit rate from 0.40 percent to, say, -0.20 percent in the first half of 2019 and then to hike all three of its policy rates not too long thereafter. Expectations of rising rates in foreign economies should lead to further U.S. dollar depreciation going forward.

Credit Market Insights

Consumer Lending Remains Solid

The January Senior Loan Officer Opinion Survey (SLOOS) on bank lending practices affirmed generally solid consumer lending standards seen through the end of 2017. Banks reported that consumer lending standards were basically unchanged in Q4, while a modest number of banks reported tighter standards for credit card loans.

The January lending survey data come amid soaring levels of consumer credit. November's print was upwardly revised to a cycle-high $31.0 billion, followed by a stillhealthy $18.4 billion increase in December. Generally easy lending standards likely contributed to the up-tick in consumer credit over the past few months. Solid consumer spending data also show that consumers are likely taking advantage of low interest rates and borrowing costs to help fuel consumption, especially given the only recent acceleration in income growth and a low saving rate.

That said, the most recent SLOOS report also included a special section on the 2018 outlook, and banks reported mixed expectations on the quality of different loan types over the coming year. Notably, a significant share of banks expect the asset quality of credit card loans to worsen in 2018, and a modest share expect tighter credit card lending standards. However, in the near term, positive consumer finances should support the current levels of consumer credit and the solid lending environment. But, if rates rise too quickly, consumers could feel the squeeze amid a low saving rate and tighter lending standards.

Topic of the Week

Is the U.S. Consumer Running on Fumes?

Personal consumption expenditure (PCE) growth continues to remain at elevated levels despite lackluster gains in real disposable personal income (DPI). Increased consumption yet muted income growth leads to an intriguing question: is the U.S. consumer running on fumes?

Americans reacted to the Great Recession by increasing the saving rate and by deleveraging. However, as the elevated level of the consumer confidence index suggests that consumers are feeling very confident regarding the current and future state of the economy, this increased confidence has led consumers to decrease the amount they save to keep pace with their current consumption habits.

With the savings rate currently sitting at 2.4 percent (top graph), markets are starting to get concerned that this reduction in the rate of saving is not sustainable, and that the risks for PCE during 2018, and for the economy as a whole, have increased considerably.

It is clear that the growth rate of real DPI has not kept pace with the increase in real PCE during the past several years (bottom graph). However, the good news is that income growth has been strengthening lately, and any divergence seen in these series tends to disappear over time. Today's deviation between growth in real PCE and growth in real DPI seems to have not only been compensated for by a lowering of the saving rate, but as well as growth in credit.

Increased confidence, backed by the feeling of increased financial security, has fostered a condition where individuals are more confident to decrease the amount they save, or even utilize part of their accumulated wealth (housing and financial wealth) to fund their consumption habits.

In our full analysis on this subject, we discuss the sustainability and effects on PCE from consumers drawing from their accumulated wealth, rather than from growth in DPI, to fund consumption.

The Weekly Bottom Line: Stocks Correct but Fundamentals Remain Solid

U.S. Highlights

- Major U.S. stock indices entered correction territory on Thursday but remain elevated relative to where they were a year ago. The sell-off was spurred by fears of higher interest rates, as the 10-year government bond yield hit a four-year high.

- The $300 billion increase in the spending cap over two years, laid out in the federal budget deal, could add to inflationary pressures at a time when the economy is already operating at close to full capacity, pressuring yields up further.

- Next week, investors will turn their attention to hard data, with advanced January retail sales providing an indication of whether or not first quarter growth will be affected by the residual seasonality.

Canadian Highlights

- It was a sea of red in Canadian financial markets this week, with the S&P TSX, oil prices and the Canadian dollar all losing ground.

- Canada's trade deficit widened in December, suggesting that net trade will be a drag on growth in the fourth quarter.

- Employment started the year off on a soft note, shedding 88k jobs in January. Losses were concentrated in part-time positions. The unemployment rate ticked up a point to 5.9%.

- Housing starts topped 200k units for an 8th straight month in January, despite some unfavourable weather conditions.

U.S. - Stocks Correct but Fundamentals Remain Solid

Major U.S. stock indices entered correction territory on Thursday but remain elevated relative to where they were a year ago. Despite falling about 10% from highs reached in the final days of January, the S&P 500, Dow Jones Industrial Average and the NASDAQ Composite remain 13-20% higher on a year-on-year basis. The sell-off was likely spurred by fears of higher real interest rates, as last week's strong January jobs report showed robust wage growth, lifting both market expectations for inflation and fed rate hikes. At 2.85%, the ten-year government bond yield hit a four-year high this week.

What's important to note is that this sell-off was not triggered by weak economic data either for the U.S. or global economy. Indeed, we learned this week that the ISM non-manufacturing index showed an improvement in the services sector at the start of 2018, with rising price pressures mirroring its manufacturing counterpart (Chart 1).

With tax cut stimulus already expected to keep U.S. growth above trend, there is little need for more stimulus. Yet, that's effectively what the federal government budget deal signed into law this morning delivers. The $300 billion increase in the spending cap over two years could foster additional inflationary pressures at a time when the economy is already operating at close to full capacity. And, higher issuance of Treasuries could put further upward pressure on yields. Moreover, the plan could have a more material effect on growth than tax cuts, since consumers are likely to save a share of the disposable income accrued from tax reform. Growth in 2019 will likely be augmented the most, assuming that spending gets underway in the second half of this year. But, the increase in the deficit would limit the government's ability to respond to any large scale downturn in the future (Chart 2). Chart 2: Spending Deal Amplifies Tax Reform Fiscal WoesAll told, any increase in investment would be a positive for future trend growth, providing further upside risk around our December forecast.

As market volatility surged, Fed speakers this week appeared unconcerned about financial market developments, instead choosing to reinforce their positive economic outlook. FOMC members had previously noted that equities were overvalued and therefore showed no sign of concern over the widespread sell-off. Voting members Dudley and Williams noted in speeches that wage inflation had picked up as expected and that markets are now adjusting to global monetary policy accommodation removal. This may help calm investor fears of faster rate hikes than previously expected, with the first of three hikes this year expected in March.

Next week, investors will turn their attention to hard data. Of particular interest will be advanced January retail sales data that should provide an indication of whether or not first quarter growth will be affected by the residual seasonality that has led to first quarter weakness in three of the previous four years. Although tax cuts have only started to boost pay checks in February, we anticipate that household spending has continued to be propped up by jobs and wage gains and will contribute strongly to economic activity again in the first quarter.

Canada - A Sea Of Red

It was a sea of red in Canadian financial markets this week, with the S&P TSX down 3% from last Friday's close; the WTI oil benchmark sliding 8% to a 1-month low of just under US$60 per barrel; and the Canadian dollar falling back below the 80 US cent mark. The bleeding in Canadian markets was part of a broader based selloff, driven by uncertainty surrounding the path for U.S. interest rates now that wage growth appears to be picking up - increasing inflation potential - and a new Fed Chair coming in.

A correction had been in store for a while, given the relatively straight line up that has characterized most equity and commodity markets recently. Hence, at least with respect to commodity prices, the recent pullback has helped to bring prices closer to fundaments. At US$60 per barrel, oil prices are still on the high side given expectations for growth in non-OPEC production. Already, US output has surged to a record high, with a whopping 1 million barrel per day increase expected for the year as a whole. And, given that speculative activity was - prior to this week - sitting at a record high, risks for oil prices remain tilted to the downside.

Canadian data out this week certainly didn't help markets. International trade data for December showed a further widening in the trade deficit. For Q4 as a whole, import volumes were up 1.2% while export volumes edged up by a mere 0.3%. As such, net trade will be a drag on growth during the quarter. Still, overall economic growth in Q4 is on track to come in at a healthy pace of about 2.2%. With the loonie expected to hover around current levels, and demand expected to remain healthy thanks to robust growth Stateside, Canada's trade picture should improve in 2018, actually contributing to overall growth.

Employment data was also soft. The Canadian economy shed 88k jobs in January, and the unemployment rate ticked up a point to 5.9%. The losses were concentrated in part-time positions - which were down by a massive 137k positions - and led by Ontario where 59k part-time jobs were lost. This loss in employment in the province coincided with a 23% jump in minimum wage. Surprisingly perhaps, accommodation and food services, one of the sectors most exposed to minimum wages, added jobs (+2.2k) in Ontario in January. While certainly a weak report, it follows a record-breaking string of gains and points to an economy moving back toward a more neutral pace of growth.

Housing starts were the bright spot this week, as they topped 200k units for an 8th straight month - and this came despite some unfavourable weather conditions in parts of the country. While kicking off the year on a strong note, homebuilding activity is likely to soften in the coming months, as tighter lending rules and rising mortgage rates put a dent in demand.

All told, this week's data won't alter the Bank of Canada's outlook much. Economic growth is unfolding largely as expected and the remains near full employment. With several risks on the radar - including tighter mortgage lending requirements, provincial minimum wage hikes and NAFTA renegotiations - the tightening cycle is likely to be gradual, with the next hike not expected until July.

U.S.: Upcoming Key Economic Releases

U.S. Consumer Price Index - January

Release Date: February 14, 2018

Previous Result: 0.2% m/m, core 0.2% m/m

TD Forecast: 0.3% m/m, core 0.2% m/m

Consensus: 0.3% m/m, core 0.2% m/m

We expect headline CPI inflation to moderate to 1.9% y/y in January, with prices up a seasonally adjusted 0.3% m/m. Energy prices should be a net positive, led by higher gasoline prices. We also see scope for a pickup in food prices, helped by dollar depreciation. Excluding food and energy, we expect core CPI to print a second consecutive 0.2% m/m increase. One tailwind is dollar weakness, which in addition to food could lend a boost to weak categories like apparel.

U.S. Retail Sales - January

Release Date: February 14, 2018

Previous Result: 0.4%, ex-auto 0.4%

TD Forecast: 0.1%, ex-auto 0.5%

Consensus: 0.2%, ex-auto 0.5%

We expect retail sales to rise 0.1% in January, held down by motor vehicle sales. Light weight auto and truck sales retraced to 17.0m from 17.8m, pointing to a sizeable decline in motor vehicle and parts sales. Gasoline station receipts will likely see a boost from higher gasoline prices. But aside from that, we expect a relatively modest 0.3% rise in the control group (excluding auto, gasoline station, food services and building material sales). Risks are generally to the downside amid the past collapse in the saving rate.

Canada: Upcoming Key Economic Releases

Canadian Manufacturing Sales - December

Release Date: February 16, 2018

Previous Result: 3.4% m/m

TD Forecast: 0.7% m/m

Consensus: N/A

Manufacturing sales are forecast to rise 0.7% m/m in December on the continued normalization of motor vehicle production and a positive tailwind from energy prices. Auto output rebounded by 14% m/m in November but remains well below levels from Q2, after which the industry was hit by the combined impact of a labour dispute and retooling shutdowns. Petroleum production should lend another tailwind due to a rise in gasoline prices while a strong performance in exports of metals and minerals bodes well for factory sales. Real manufacturing sales growth should come in near the nominal print due to a modest decline in factory prices, which would leave volumes up roughly 2.3% y/y and 3.3% for 2017 as a whole.

Week Ahead – US & UK CPI, Australian Employment and Japanese Growth Figures on the Horizon

On the face of it, it looks that the upcoming week will lack events of similar magnitude to the one we just experienced - for example, the Bank of England meeting and subsequent press conference by Governor Carney. Still, there are releases that have the capacity to keep investors on edge and lead to notable movements in forex markets: US and UK CPI and retail sales, Australian jobs data, and Japanese GDP figures are among the readings that will be closely watched as the week unfolds.

Australian employment report in focus

Australian data on employment (and unemployment) for the month of January will be made public on Thursday at 0030 GMT. December's net new positions added to the economy stormed past expectations, posting a record-equaling 15th consecutive month of rises along the way; the unemployment rate did rise, though that was attributed to more individuals entering the labor force. It would be interesting to see if next week's release maintains positive momentum and whether it will lend some support to the local dollar which has experienced notable losses versus the US currency after hitting a more than 2½-year high of 0.8135 in late January.

It should be mentioned however, that an upbeat report would not necessarily translate into a rising currency. In December, labor supply grew by more than labor demand, easing wage growth and consequently inflationary pressures, pushing back in time market participants' expectations for a rate hike by the Reserve Bank of Australia and leading to aussie weakness.

New Zealand will see the release of electronic card retail sales for the month of January on Sunday (Monday morning for Asian traders).

GDP estimates for Q4 2017 and machinery orders among Japanese releases

January's corporate goods prices (these being wholesale prices, i.e. what companies charge each other for their goods and services) out of Japan will be released on Monday at 2350 GMT. More importantly, the world's third largest economy will see the release of preliminary Q4 GDP growth on Tuesday at 2350 GMT. On an annualized and quarterly basis, growth is expected to stand at 0.9% and 0.2% respectively. These compare to Q3's respective figures of 2.5% and 0.6%, though most analysts anticipate the expected deceleration to be temporary. A reading showing positive growth - as projected by analysts - would translate into eight straight quarters of expansion, Japan's longest such streak since the period between 1986 and 1989 when the economy grew for 12 straight quarters; though that period was associated with the formation of a bubble. Next in line out of the nation will be December's machinery orders scheduled for release on Wednesday at 2350 GMT.

Remaining in Asia and turning to China, the world's second largest economy, data on bank lending are forecast to show that new yuan loans rose to their highest in a year in January following a big decline in December. In general, Chinese banks front-load loans every year to win market share, so one might not read much into the data than otherwise would. Attention, however, remains on government efforts to mitigate risks from rising debt levels. Beyond the yuan, it is invariably the case that markets also pay attention to the Australian dollar ahead of and in the aftermath of Chinese releases; the aussie is viewed as a liquid proxy for China's economy due to the two nations' strong economic ties. Lending data out of China are tentative however, lacking a specific date and time of release (they have a release window that spans between February 12 and 19).

Second release of Q4 2017 eurozone GDP, UK inflation & retail sales make list of European releases

Of most interest out of the eurozone will be the second release of Q4 2017 GDP growth out on Wednesday at 1000 GMT. Quarter-on-quarter, the pace of expansion is anticipated at 0.6%, the same as in the first release and below Q3's respective figure of 0.7%, while annualized growth is projected to come in at 2.7%, in line with the first release and again below Q3's respective figure of 2.8%, a rate of growth last achieved in Q1 2011. Data on eurozone industrial production for the month of December will be released at the same time. A few hours earlier (at 0700 GMT), Germany, the eurozone's and Europe's largest economy, will see the release of flash Q4 2017 GDP growth estimates and final inflation figures for the month of January.

Out of the UK, January's inflation figures and data on retail sales for the same month scheduled for release on Tuesday and Friday (both at 0930 GMT) will be drawing most attention, having the potential to lead to positioning on sterling. On a monthly basis, headline CPI is projected to contract by 0.6% and on a yearly basis to expand by 2.9%, continuing to ease after hitting a near six-year high of 3.1% in November and lending support to those saying that it will start to gradually slow, moving towards the Bank of England's target for annual inflation of 2%; though it might be early to conclusively state that a gradual slowdown is taking place. January's producer prices are also due on Tuesday at the same time as CPI numbers, while core inflation will also be attracting interest.

On the UK retail sales front, those are expected to rebound after December's contraction on a monthly basis. Last year, retailers experienced their worst year since 2013 as inflation outstripping wage growth - translating into weaker purchasing power for households - weighed on consumer spending and consequently retail sales. It will be interesting to see to what extent this would continue moving forward.

Lastly out of Europe, the Riksbank, Sweden's central bank, will be deciding on rates on Wednesday.

CPI, retail sales, industrial & manufacturing output on US agenda

In terms of US releases, Wednesday's inflation and retail sales figures (both due at 1330 GMT), Thursday's industrial production (due at 1415 GMT), and Friday's data on housing starts (due at 1330 GMT) as well as the University of Michigan's preliminary survey on consumer sentiment for the month of February (due at 1500 GMT) are expected to generate most investor interest. Barring the University of Michigan's survey, all other releases will pertain to the month of January.

There are rising inflation expectations as of late in the US, and Wednesday's CPI figures could show - a least to an extent - whether those are justified. Headline CPI is projected to grow at a stronger pace on a monthly basis, while on an annual basis it is expected at 2.0%, slightly below December's 2.1%. Annually, core inflation is also anticipated to tick slightly lower, with analysts projecting it at 1.7% versus December's 1.8%. The Federal Reserve's preferred inflation measure is the core personal consumption expenditure (PCE) index, but still forex market participants will be paying attention to the data as they can give insights on the speed with which the US central bank will continue to tighten its policy.

In terms of other data out of the US, retail sales in previous months showed positive momentum and it would be interesting to see whether that is carried through into 2018. Industrial production is expected to ease to a growth rate of 0.2% on a monthly basis, after beating expectations in December to expand by 0.9% m/m; manufacturing output, a subset of industrial output, will also be watched. Housing starts were affected by cold weather conditions in December, recording their sharpest monthly fall in around one year. As the extreme weather effects are dropping out of the data, a rebound is to be anticipated. Finally, the University of Michigan's survey is projected to show that consumer sentiment remained around the same levels as in January.

Out of Canada, manufacturing sales for the month of December due on Friday will be gathering some interest.

US Dollar Surges Amidst Volatility

BoE Signals Higher Interest Rates in the UK

The US dollar had its strongest week against major currency pairs in twelve months. Even as the United States is suffering a bout of political uncertainty the dollar became a safe haven as stocks and bonds saw massive moves this week. The signing of a federal budget by US President Donald Trump boosted the dollar ahead of the release of retail sales and inflation data next week. Central banks are moving away from record low interest rates around the globe.

- UK inflation expected at 2.9 percent

- US inflation potential rise has markets worried

- EU Brexit negotiator warns UK about transition risks

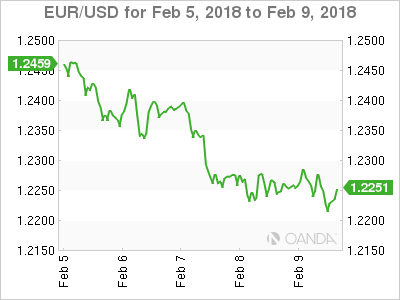

The EUR/USD lost 1.77 percent in the last five trading days. The single currency is trading at 1.2235 after heavy losses were registered by European equities to follow in line with the drop in American markets. The rise in wages in the latest U.S. non farm payrolls (NFP) report triggered a surge of the US dollar as investors are buying the currency as higher rates are in the horizon. Higher inflation is expected and will be one of the economic indicators under review this week. The US Bureau of Labor Statistics will publish the Consumer Price Index (CPI) on Tuesday, February 13 at 8:30 am EST. Core inflation is expected to have gained 0.2 percent in January with anything above could drive the US currency even higher.

European politics have reached some stability with the German coalition now in place but with the upcoming Italian elections in March the boat is sure to rock. Economic fundamentals have been strong in the eurozone with Germany leading the way as usual. The gap between the U.S. Federal Reserve and the European Central Bank (ECB) is closing with regarding monetary policy. The ECB is expected to end its QE program and could even lift interest rates later this year. The week will bring minor indicator releases in Europe with the German central bank chief Jens Weidmann speaking in Frankfurt on Wednesday, February 14 at 3:00 am EST. Earlier that day the GDP figures for Germany will be released with a 0.6 percent growth expected.

The market will be following US releases more closely after a strong week for the USD. Producer Price Index data will be released on February 15 at 8:30 am EST with a forecasted gain of 0.4 percent after the prices of goods fell last month.

Data released on Friday by the CFTC showed short positions of the US dollar shrank for the first time in six weeks signalling a change in investor sentiment towards the greenback.

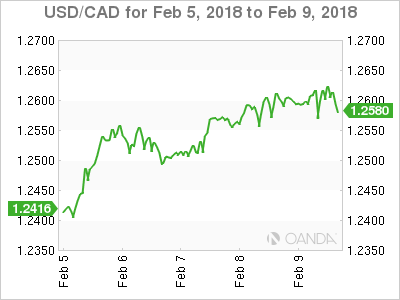

The USD/CAD gained 1.52 percent in the last five days. The currency pair is trading at 1.2613 after the start of Monday trading at 1.2416. The stock market sell off has seen a growing appetite for US dollars as well as the end of some short USD positions. Canadian data was few and far between and it overall did not help the loonie. The Trade balance grew from 2.7 billion last month to 3.2 as imports grew by 1.5 percent in December, while export only did so by 0.6 percent. Canadian employment data was released on Friday and did not paint a pretty picture. Canada lost 88,000 positions well below expectations of a 10,000 gain in January. There was a slowdown anticipated after two back to back 70,000 plus gains, but the drop surprised even the more pessimistic analysts. The fact that most of the losses came in part time positions took some of the sting from the report and could be explained in part by the rise of minimum wages in Ontario.

Next week will be quiet in the Canadian economic calendar with the relatively new ADP non farm report due out on Thursday, February 15 at 8:30 am EST. and Foreign purchases of securities on Friday, February 16 at 8:30 am EST.

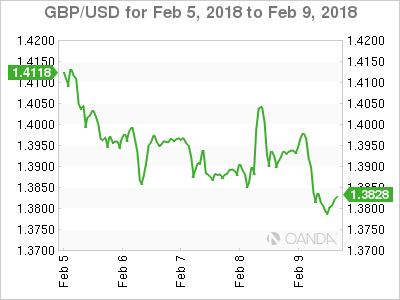

The GBP/USD lost 2.17 percent this week. The currency pair is trading at 1.3814 despite a hawkish Bank of England (BoE) singling a rate hike sooner rather than later. The biggest downwards pressure comes from comments by the EU Brexit negotiator Michel Barnier said Brussels as disagreements between the UK and the European Union remain. The words: "A transition is not a given", was a shock after the Brexit divorce appeared to be headed to a more amicable end. The fragile situation of the conservative government after their narrow triumph in the snap elections they themselves triggered has left them in a position of weakness at this stage of the negotiation.

The Bank of England (BoE) hosted its first super Thursday of the year on February 8. The central bank was openly hawkish about inflation and its willingness to hike sooner than later. The BoE could move interact rates higher as soon as May. The release of the Consumer Price Index on Tuesday, February 13 at 4:30 am could validate the strong messaging from the BoE if inflation stay above the 2 percent target.

Market events to watch this week:

Tuesday, February 13

- 4:30am GBP CPI y/y

- 9:00pm NZD Inflation Expectations q/q

Wednesday, February 14

- 8:30am USD CPI m/m

- 8:30am USD Core CPI m/m

- 8:30am USD Core Retail Sales m/m

- 8:30am USD Retail Sales m/m

- 10:30am USD Crude Oil Inventories

- 7:30pm AUD Employment Change

Thursday, February 15

- 8:30am USD PPI m/m

Friday, February 16

- 4:30am GBP Retail Sales m/m

- 8:30am USD Building Permits

*All times EDT

Weekly Focus: Stock Sell-off is Mostly Technical But Watch Inflation

Market movers ahead

- Inflation expectations are moving higher in the US but we expect CPI data for January to show that core inflation remains subdued.

- UK inflation data will also be important, as the Bank of England may increase rates as early as May.

- We expect the Swedish Riksbank to maintain its confident stance on the economy and inflation at next week's monetary meeting, even though we see major risks to both.

- Norges Bank Governor Øystein Olsen delivers his annual address, where he is likely to touch on the strengthening economy and fading risks in Norway.

Global macro and market themes

- We view the sell-off in stocks as a correction – the upward trend is supported by strong profit growth.

- Data this week adds to the picture of a robust global recovery underpinning profits.

- Bond yields are set to increase further.

- EUR/USD is in a range before the next move higher.

Sunset Market Commentary

Markets:

We can be rather brief about today's trading session on core bond markets. Both the Bund and the US Note future hovered near opening levels with US Treasuries underperforming as the US House passed a two-yr budget bill and ended a brief government shutdown. The eco calendar was empty and risk aversion on European stock markets had little spill-over effects. US yields add 1.5 bps (2-yr) to 2.9 bps (10-yr) at the time of writing. The German yield curve bull flattens with yields declining by 0.7 bps (2-yr) to 3.3 bps (30-yr). On intra-EMU bond markets, 10-yr yield spread changes versus Germany widen up to 4 bps (Italy) with Portugal (+7 bps) and Greece (+28 bps) underperforming.

The dollar developed a similar indecisive trading pattern as was the case yesterday. EUR/USD hovered up and down in the 1.22 big figure. The dollar slightly outperformed the single currency this morning as risk sentiment remained very fragile. However, it was insufficient for the dollar to make a decisive step higher. Later in the session, the dollar ceded again slightly ground as global equity selling eased, at least temporary. EUR/USD trades in the 1.2265 area. USD/JPY hovers around 109. There were no important eco data to guide USD trading. Developments on interest rate markets/interest rate differentials also failed to provide a clear directional driver for USD trading. USD traders still don't really know how to adapt USD positions in the wake of the recent spike in global volatility.

Sterling strengthened temporary yesterday as the BoE signaled that it might raise rates at a faster pace than anticipated until now. However, the gains could not be sustained. Overall risk-aversion and lingering uncertainty on Brexit kept investors cautious to add sterling long exposure. The sterling positive momentum dwindled further today. UK eco data were mixed. Production suffered from a (temporary ) shutdown in an oil pipeline. The UK trade deficit was also wider than expected. Sterling started a new gradual downleg after the data. The decline accelerated around noon as EU's Barnier warned Britain that a post-Brexit transition period is not a given. The comments are another indication that Brexit negotiations are proceeding on a bumpy road. EUR/GBP spiked higher in the 0.88 big figure (currently 0.8875). Cable tumbled temporary below 1.38, but rebounds slightly as the dollar regained some ground this afternoon (currently 1.3840 area).

News Headlines:

The US Congress ended a brief government shutdown by reaching a wide-ranging deal that is expected to push budget deficits into the $1 trillion-a-year zone. The bill passed by a wide margin in the Senate and survived a rebellion of conservative Republicans in the House of Representatives thanks to the support of some Democrats. President Donald Trump signed the measure into law on Friday morning.

Norway's economic recovery continued in the fourth quarter led by rising consumer spending and investments. Mainland economic growth, which excludes oil and shipping, expanded by 0.6% Q/Q. At the same time, January CPI was reported soft at 1.6% Y/Y. Core inflation even slowed to 1.1% Y/Y, raising questions on whether the Norges bank will raise rates this year. The Norwegian Krone came under further pressure. EUR/NOK jumped to the 9.87 area.

A post-Brexit transition period is "not a given", the European Union's Brexit negotiator Michel Barnier warned Britain, saying London had raised "substantial" issues with the plan proposed by the bloc.

British industrial output declined 1.3% M/M in December due to the temporary shutdown of a major oil pipeline, but growth in manufacturing (0.3% M/M and 1.4% Y/Y) pointed to solid growth at the end of 2017.Construction output also showed a surprise surge in December. At the same time, ONS data showed Britain's goods trade deficit widened more than expected to 13.6 billion pounds in December, due to rising crude oil prices and higher imports.

Canada’s Long Streak of Job Gains Finally Ended in January

Highlights:

- Employment fell 88k in January marking the first drop in 18 months.

- Part-time employment plunged 137k and full time jobs rose 49k.

- The unemployment rate ticked up to 5.9% but was still down 0.8% from a year ago.

- Wage growth strengthened to 3.3% on a year-over-year basis - in part because of a large minimum wage hike in Ontario.

Our Take:

Employment plunged 88k in January, bringing an end to an impressive 17-month long streak of gains - the longest such stretch in 17 years - in what is normally a very volatile measure. The monthly drop in headline employment is eye-catching but still only retraced about 60% of the 146 increase over just the last two months. Other details also weren't as bad as the headline employment drop might suggest. Part-time employment dropped a whopping 137k - the largest one-month decline on record - but full-time jobs rose 49k. The unemployment rate ticked up to 5.9% but that was still just slightly above the 5.8% in December that matched the lowest reading on record since 1976. The rate is still down almost a percent from a year ago and more than that if sources of 'hidden' unemployment like discouraged workers are included. Indeed, by our calculations, the Bank of Canada's closely-watched 'LMI' composite labour market indicator appears to have ticked modestly lower in January - consistent with further underlying labour market improvement. Permanent employee wage growth accelerated to 3.3% year-over-year in January. That was probably in part related to a big hike in the minimum wage in Ontario although wages also appeared to accelerate somewhat on balance in other provinces.

Broadly speaking, we don't expect the 36k average monthly employment gain last year to be repeated, and today's report does not change our view that labour markets will nonetheless continue to tighten.

Canada’s Labour Market Winning Streak Ends in January, as the Economy Sheds 88k Jobs

Canada shed 88.8k positions in January, ending the economy's 17-month streak of job gains.

Losses were concentrated in part-time jobs, which fell a staggering 137k. Full-time jobs, on the other hand, were up a healthy 49k.

Despite the magnitude of decline, the unemployment rate edged up just a notch to 5.9% (from 5.8%), as 73.7k people left the labour force. As a result of the exodus, the participation rate ticked down to 65.5% (from 65.8%).

Both public and private sectors shed jobs in the month, with public employment down 41.2k and private-sector jobs down 70.7k. Self-employment bucked the trend, adding 23.9k positions.

Good-producing industries shed 16.2k positions, led by construction (-14.9k). Manufacturing employment, on the other hand, edged up 0.8k. Service-producing employment fell 71.9k, with losses relatively widespread across sectors. Surprisingly perhaps, trade (wholesale and retail) were not major contributors (down just 0.8k).

Regionally, losses were relatively widespread, and gains relatively minimal. Ontario was the biggest loser in January, shedding 50.9k jobs in the month. Despite the drop, Ontario's unemployment edged down ever so slightly (to 5.5%) as 54.8k people left the labor force. In Quebec, employment fell 17.3k and the unemployment rate reversed the prior month's decline, moving back up to 5.4% (from a record-low of 5.0% in December).

Wage growth accelerated in the month to 3.3% (from 2.8% in December).

Key Implications

You win some, you lose some. After a record-breaking string of gains, Canada's job market was due for a pullback. This is a big number on the surface, but so were the gains over the previous several months.

All told, this does not change the story for the Canadian economy much. The unemployment rate is still low with the economy remaining close to full employment.

Wage growth heated up this month but did not accelerate to the pace expected given the minimum wage legislation being implemented in Ontario. Still, more gains may be on the way in the months ahead, with the metric likely to be closely watched going forward.

This report does not much change the outlook for the Bank of Canada, but suggests a more rationale pace of job growth consistent with an economy that is moving toward a more neutral pace of growth after a very robust year.