Sample Category Title

EURUSD: Remains Vulnerable On Bear Pressure

EURUSD: The pair closed lower on further weakness on Thursday leaving risk of more weakness on the cards. On the upside, resistance comes in at 1.2300 level with a cut through here opening the door for more upside towards the 1.2350 level. Further up, resistance lies at the 1.2400 level where a break will expose the 1.2450 level. Conversely, support lies at the 1.2200 level where a violation will aim at the 1.2150 level. A break of here will aim at the 1.2100 level. Below here will open the door for more weakness towards the 1.2050. Its daily RSI is bearish and pointing lower suggesting more weakness. All in all, EURUSD faces further pullback threats.

Pound Falls Below 1.39, Delated by Downbeat UK Data

Cable fell below 1.3900 handle in Europe, deflated by downbeat trade balance/IP data. Trade deficit widened to 13.5 billion pounds in Dec from forecasted 11.5 billion gap, while industrial production fell by 1.3% in Dec, falling below forecasted 0.9% fall and against downward-revised previous month's 0.3% release.

Fresh easing after recovery failed under 1.40 pivot and loss of 1.39 handle weakens near-term structure and turns near-term focus lower again, after hawkish comments from BoE on Thu/Fri showed limited and short-lived positive impact on sterling.

Temporary base at 1.3840 zone, reinforced by rising 30SMA is coming under increased pressure as risk of continuation of pullback from 1.4277 lower top is intensifying.

Thursday's strong upside rejection above 1.40 which left daily candle with long upper shadow, weighs on near-term action for renewed attack at 1.3840 base.

Firm break here would open next strong support at 1.3796 (Fibo 61.8% of 1.3457/1.4344 upleg) and could trigger stronger bearish acceleration on break lower.

Broken 1.39 point now acts as initial resistance and guarding pivotal barrier at 1.4000 (20SMA / psychological barrier).

Res: 1.3900; 1.3986; 1.4000; 1.4033

Sup: 1.3854; 1.3835; 1.3796; 1.3667

Canadian Dollar in Holding Pattern Ahead of Key Job Reports

The Canadian dollar has ticked higher in the Friday session. Currently, the pair is trading at 1.2609, up 0.05% on the day. On the release front, the focus is on Canadian employment indicators, with the release of Employment Change and the unemployment rate.

This week's market selloff has boosted the US dollar, at the expense of the Canadian dollar and most other major currencies. The Canadian dollar has dropped 1.4% this week, and is down 2.5% in February, erasing the gains we saw in January. Interestingly, the catalyst for the current turbulence has been solid economic data in the US, namely, improved payrolls and wage growth reports. This has raised concerns of inflation, which could lead to a quicker pace of rate hikes from the Federal Reserve. This sentiment has sent the bond markets higher, while weighing on global stock markets.

After some spectacular readings, Canada's economy is expected to show more modest job creation in January, with an estimate of 10.3 thousand. The unemployment rate is forecast to edge up from 5.7% to 5.8%. If these predictions are within expectations, the Canadian dollar could gain some ground on Friday, and end a tough week on a positive note.

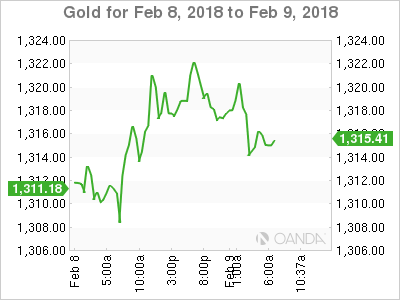

Technical Outlook: Spot Gold – Bears To Resume After A Breather, Thick Hourly Cloud Weighs Heavily

Spot Gold fell to European session low at $1313, coming under renewed pressure after recovery attempts were repeatedly rejected at $1322 (Thu/Fri).

Yesterday’s long-tailed Doji signaled a breather in broader downtrend, with fresh easing keeping near-term bias with bears.

Weaker dollar on the second US government shutdown in 2018 showed little impact to the yellow metal which keeps focus at the downside.

However, bearish continuation requires stronger signal which will be generated on close below cracked $1316 pivot (Fibo 38.2% of $1236/$1366 ascend) and would expose 55SMA ($1302) and psychological $1300 support.

Near-term action is heavily pressured by thick falling hourly cloud (spanned between $1317 and $1327) which is expected to limit stronger recovery attempts.

Thin calendar from the US on Friday signals lack of fundamentals and suggests the yellow metal’s price would be driven by technicals.

Res: 1317, 1322, 1327, 1330

Sup: 1313, 1307, 1302, 1300

US Futures Higher After Second Plunge This Week

- Indices Remain Vulnerable After Entering Correction;

- US Congress Passes Funding Bill Ending Brief Government Shutdown;

- Sterling Dips After Worrying Manufacturing Data.

Indices Remain Vulnerable After Entering Correction

US futures are trading slightly in the green ahead of the open on Friday, a day after stock markets once again tumbled leaving indices in correction territory.

As we saw on Thursday, this isn't necessarily indicative of calm returning to the markets. The Dow recorded declines of more than 1,000 points for the second time this week, having never done so before, despite futures prior to the open being relatively unchanged on the previous days close.

Clearly there remains a lot of volatility and nervousness in the markets and I don't expect this to ease up heading into the weekend. Stock markets will likely remain vulnerable to further shocks heading into today's close and possible even next week. That said, with a 10% correction having now completed, I wonder whether investors will now start looking to buy the dips as the fundamental backdrop remains strong.

US Congress Passes Funding Bill Ending Brief Government Shutdown

On a more positive note, the House and the Senate approved a new funding bill in the early hours of Friday morning that will see the government through to 23 March and increase spending limits for two years, ending a showdown that came into effect overnight.

Markets haven't been too concerned about the prospect of a shutdown since the start of the year despite two having now taken place so I don't expect to see any boost now that a deal has been reached. This is merely just another self-inflicted risk that's been temporarily averted.

Sterling Dips After Worrying Manufacturing Data

It's a slightly quieter day in terms of notable economic events. The Canadian jobs data will be of interest given that the central bank has been relatively aggressively raising interest rates over the last six months. The UK GDP estimate from NIESR will also be of interest, given that the pound has continued to rise even as the economy experiences a notable slowdown.

The manufacturing and industrial production figures from the UK this morning showed another dip in December, with the latter in particular experiencing no year on year growth. Given that these are among the areas that have benefited since the referendum, it may be a minor concern. The pound dipped after the releases having failed to hold above 1.40 against the dollar in recent days.

Equities Lose $5 Trillion As Bulls Slay Bulls

Friday February 9: Five things the markets are talking about

Stateside, the House of Representatives has approved the bill to fund the U.S government and has raised spending limits over two-years, it is now sending the measure to President Trump.**

Investors should expect market turbulence to continue this year as pullbacks and volatility become more common in the wake of rising central bank interest rates and sovereign bond yields.

The growing consensus is that increasing market volatility should not be capable of derailing the underlying economic expansion or fundamentally dent risk assets, it does however make many things less predictable.

Ahead of the U.S open, European stocks have pared their decline and U.S stock futures have gained despite an Asian session seeing red, with China's bourses tumbling the most in 24-months.

Elsewhere, Treasury yields have backed up to trade atop of their four-year highs as the 'buck' edged lower. Crude oil is heading towards its worst week in 12-months on concerns of over growing U.S supply and gold prices have temporarily stopped the bleeding.

On Tap: Canadian employment numbers are out at 08:30 am EDT. Is the market about to see a deep revision to the last two-months of massive job gain headlines?

1. Stocks Sea of red

In Japan, the Nikkei share average tumbled again overnight, mirroring Wall Street's losses, with oil-related equities leading the broad declines as crude prices slumped. The Nikkei finished down -2.3%, bringing its weekly loss to -8.1%. The broader Topix was -1.9%, down -7.1% for the week.

Down-under, Aussie shares slumped to a near four-month low overnight hammered by renewed selling on worries of higher inflation and interest rates. The S&P/ASX 200 index fell -0.9%. The benchmark has declined -4.6% on the week, its biggest loss in over 24-months. In S. Korea, the Kospi index fell -1.8%.

In Hong Kong, stocks crumble and cap the biggest weekly fall since the global financial crisis. At close of trade, the Hang Seng index was down -3.1%, the Hang Seng China Enterprises index fell -3.87%. For the week, the Hang Seng tumbled -9.5%, the biggest weekly loss since October 2008, while the HSCE posted a weekly loss of -12.01%.

In China, stocks were crushed and suffered their worst day in almost two-years, with blue-chip led carnage dragging the markets into correction territory. The benchmark Shanghai Composite Index tumbled -4.0% and the blue-chip CSI300 ended the day down -4.3%.

In Europe, regional indices trade mostly lower, but are off their session lows after a rebound in U.S futures ahead of the open stateside. Increased outlook for higher rates from the Bank of England (BoE) is weighing on the FTSE.

Indices: Stoxx600 -0.5% at 372.1, FTSE -0.4% at 7144, DAX -0.3% at 12221, CAC-40 -0.4% at 5129, IBEX-35 -0.7% at 9689, FTSE MIB -0.3% at 22407, SMI +0.1% at 8768, S&P 500 Futures +0.7%

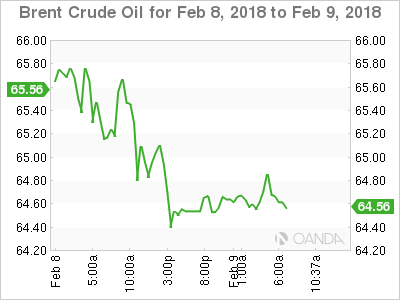

2. Oil slides towards steep weekly loss as supply fears mount, gold higher

Oil prices are on track for their biggest weekly loss in 10-months after hitting new lows overnight after data this week showed U.S crude output had reached record highs and the North Sea's largest crude pipeline reopened following an outage.

Brent futures are down -30c at +$64.51 a barrel. Yesterday, Brent fell -1.1% to its lowest close since Dec. 20. U.S West Texas Intermediate (WTI) crude is down -42c at +$60.73 a barrel, having settled down -1% Thursday, its lowest close since Jan. 2.

Note: Brent futures have lost around -9% from their four-year January high print of +$71. Futures positions suggest that investors are sitting on the largest 'bullish position in history.

Earlier this week, the U.S. Energy Information Administration (EIA) upped its 2018 average output forecast to +10.59m bpd, up +320k bpd from its last forecast 10-days ago.

Note: The output is now higher than the previous bpd record from 1970 and above that of top exporter Saudi Arabia.

Ahead of the U.S open, gold prices have edged a tad higher after hitting more than one-month lows yesterday, as the correction in equities drove investors towards safe-haven assets like gold. However, gold 'bulls' should expect a stronger U.S dollar and concerns over rising global interest rates to keep gains somewhat capped. Spot gold is up +0.1% at +$1,320.72 an ounce.

Note: On Thursday, gold prices touched their lowest since Jan. 4 at +$1,306.81 an ounce.

3. Equity pain brings relief to bonds

The Eurozone and U.S bond yields have edged a tad lower as renewed global stock selling has managed to lend some support to safe-haven debt markets.

Bond yields have been backing up aggressively all week as investors brace for an end to easy-monetary policies by G7 central banks.

Note: Yesterday's more hawkish than expected Bank of England (BoE) was the latest catalyst to cause fixed income to steepen sovereign yield curves.

The yield on U.S 10-year Treasuries has decreased less than -1 bps to +2.84%. In Germany, the 10-year Bund yield fell -1 bps to +0.76%, while in the U.K the 10-year Gilt yield declined -2 bps to +1.617%.

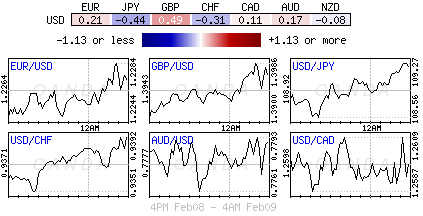

4. Dollar jives and dips

Market risk aversion sentiment remains to the fore, but the G10 forex pairs continue to stay locked within their recent ranges. The U.S dollar bull, and they are dwindling; maintain that it's the Fed who may be caught behind the curve on rates. Next week's U.S CPI may very well put the 'cat amongst the pigeons.'

Note: The greenback has caught a bid now that the House of Representatives has approved the bill to fund the U.S government.

Elsewhere, the EUR/USD (€1.2254) is little changed, the pound continues to benefit, albeit struggling after the U.S funding announcement, from the Bank of England saying on Thursday that it expected to “increase interest rates earlier and faster' than previously projected, seen by many to mean a likely May rate rise.

The Chinese currency is on track for its first weekly loss in nine-weeks as the yuan (¥6.3400) has weakened against the dollar in thin volume.

5. U.K industrial output falls on North Sea pipeline shutdown

Data this morning showed that U.K. manufacturing continued to grow in the final month of 2017, but overall industrial production fell by more than anticipated due to an emergency shutdown of a North Sea pipeline.

In monthly terms, U.K. factory output grew by +0.3%, in line with market expectations, the eighth consecutive month of growth.

However, overall industrial production, meanwhile, declined by -1.3%, +0.4% more than forecast.

Separately, the ONS said that the U.K.'s trade deficit widened in December, driven by increased oil imports and rising prices. The December goods trade deficit stood at -£13.6B – significantly wider than expected (-£11.8B e)

CAC Loses Ground As Global Sell-Off Continues

The CAC index has posted losses in the Friday session. Currently, the index is at 5124.00, down 0.54% on the day. On the release front, French Industrial Production came in at 0.5%, above the estimate of 0.1%.

It's been a tumultuous week for global stock markets, and the CAC has dropped 3.6% percent this week. February has been dismal for European markets, and the CAC has shed 6.9%. Earlier this week, the CAC dropped to its lowest level since early September. The CAC has lost ground on Friday, following losses in the North American and Asian stock markets. Ironically, the catalyst for the current sell-off has been solid economic data in the US; namely, improved payrolls and wage growth reports. This has raised concerns of inflation, which could lead to a quicker pace of rate hikes from the Federal Reserve. This sentiment has sent the bond markets higher, while weighing on global stock markets.

A rebound in the global economy has been a boon for eurozone exports, and this has boosted France's manufacturing setor. This was underscored by a solid French industrial production report, which gained 0.5% in December. We'll get a look at Eurozone Industrial Production next week. The November reading surged to 1.0%, marking a 3-month high.

After months of intense negotiations, President Angela Merkel appears to have put together a new coalition government. Earlier this week, Merkel's conservative party and the socialist SDP announced that they had finalized a coalition agreement. In the last government, the SDP was the junior partner of the conservatives, but this time around the SDP has extracted major concessions from Merkel, including the finance and foreign affairs ministries. This could present a unique opportunity for French President Macron, as the new German government will likely undergo a significant shift in its stance towards the eurozone. Under the previous government, there was a reluctance to provide large bailouts to weaker eurozone members, such as Cyprus and Greece. However, struggling members will likely find a sympathetic ear for financial help from the SDP. As well, Macron's vision of a more integrated Eurozone, complete with a budget and finance minister, may dovetail nicely with the SDP's stance towards the eurozone.

Market Update – European Session: Awaiting US House To Approve Spending Bill To Reopen Govt

Notes/Observations

Market volatility remained elevated as concern simmer that central banks were not keeping up with global economic growth.

Senate passed a two-year budget deal in the wee hours of Friday morning; after the government was forced into a technical shut down at midnight due to a political stunt by Sen. Rand Paul (R-KY); Government would reopen once the bill cleared the House in the predawn hours

Asia:

RBA Quarterly Statement on Monetary Policy (SOMP) made little resison to its growth and inflation outlook. Outlook for global growth was positive despite volatility in equity markets: Reiterated an appreciating A$ would dampen domestic growth and inflation

China Jan CPI in-line at 1.5% y/y - China PBoC again skipped its Open Market Operation (OMO) for the 12th straight session (12th straight session)

China PBoC noted that it had released Temporary liquidity worth almost CNY2.0T to help satisfy cash demand before Lunar New Year

Japan Economy Min Motegi: Economic fundamentals were strong both in the US and Japan; reiterated monitoring impact of financial markets on economy

Japan PM Abe Adviser Hamada noted that the BOJ should stick with current easy settings; recent stock declines could make BoJ cautious about raising rates

Europe:

UK Govt spokesperson: Business representatives expressed importance of time-limited implementation period in providing clarity

Labour party Jeremy Corbyn (opposition) said to have told EU’s Barnier he was open to keeping Britain in the customs union after Brexit; wlling to allow the UK to submit to ECJ rulings should he become PM

Americas:

Senate approved a far-reaching budget deal that would reopen the federal government and boost spending by hundreds of billions of dollars

Bank of Canada (BOC) Wilkins: high household debt was the largest vulnerability to the Canadian economy

Mexico Central Bank raised the Overnight Rate by 25bps to 7.50% (as expected) for its 12th hike in the current tightening cycle.

Economic Data:

(NL) Netherlands Dec Manufacturing Production M/M: 0.6% v 1.1% prior; Y/Y: 5.2% v 4.4% prior, Industrial Sales Y/Y: 0.7% v 12.9% prior

(CH) Swiss Jan Unemployment Rate: 3.3% v 3.4%e, Unemployment Rate (seasonally Adj): 3.0% v 3.0%e

(FI) Finland Dec Industrial Production M/M: 0.0% v 0.8% prior; Y/Y: 4.2% v 4.2% prior

(NO) Norway Jan CPI M/M: -0.1% v +0.1%e; Y/Y: 1.6% v 1.6%e

(NO) Norway Jan CPI Underlying M/M: -0.8% v -0.2%e; Y/Y: 1.1% v 1.5%e

(NO) Norway Q4 GDP Q/Q: -0.3%v 0.8% prior; Mainland GDP Q/Q: 0.6% v 0.6%e

(CN) Weekly Shanghai copper inventories (SHFE): 186.1K v 172.6K tons prior

(FR) France Dec Industrial Production M/M: 0.5% v 0.1%e; Y/Y: 4.5% v 3.5%e

(FR) France Dec Manufacturing Production M/M: +0.3% v -0.5%e; Y/Y: 4.7% v 3.4%e

(IT) Italy Dec Industrial Production M/M: 1.6% v 0.8%e; Y/Y: -1.3% v +2.3% prior, Industrial Production WDA Y/Y: 4.9% v 1.9%e

(UK) Dec Industrial Production M/M: -1.3% v -0.9%e; Y/Y: 0.0% v 0.3%e

(UK) Dec Manufacturing Production M/M: 0.3% v 0.3%e; Y/Y: 1.4% v 1.2%e

(UK) Dec Construction Output M/M: +1.6% v -0.1%e; Y/Y: -0.2% v -1.9%e

(UK) Dec Visible Trade: -£13.6B v -£11.6Be, Overall Trade Balance: -£4.9B v -£2.4Be, Trade Balance Non EU: -£5.2B v -£4.1Be

Fixed Income Issuance:

(IN) India sold total INR110B vs. INR110B indicated in 2024 and 2028 bonds

(ZA) South Africa sold total ZAR900M vs. ZAR900M indicated in I/L 2029, 2033 and 2050 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.5% at 372.1, FTSE -0.4% at 7144, DAX -0.3% at 12221, CAC-40 -0.4% at 5129 , IBEX-35 -0.7% at 9689, FTSE MIB -0.3% at 22407 , SMI +0.1% at 8768, S&P 500 Futures +0.7%]

Market Focal Points/Key Themes: European Indices trade mostly lower but off the session lows after a rebound in US Futures overnight after sharp falls yesterday. Increased outlook for higher rates in the UK weigh on the FTSE, as the index under performs. Ont he corporate front Maersk trades lower after Q4 results; Ceconomy also trades lower after a fall in profits. To the upside Trinity Mirror outperforms after its trading update, Flow Traders trades over 10% higher after strong y/y growth. In the M&A space Hogg Robinson trades sharply higher after receiving a bid from American Express Global, representing a 54% premium to prior close. Looking ahead earners include PG&E, Tenneco and Moody's.

Movers

Consumer Discretionary [ Hogg Robinson [HRG.UK] +49% (To be acquired for 120p/shr], Trinity Mirror [TNI.UK] +7.3% (Trading update, acquisition), Ceconomy [CEC.DE] -2.0% (Earnings), L'Oreal [OR.FR] +0.8% (Earnings), Bechtle [BC8.DE] +1.0% (Prelim earnings)]

Industrials [Maersk [MAERSKB.DK] -2.9% (Earnings), Victrex [VCT.UK] +1.2% (Prelim results)]

Technicals [Fingerprint Cards [FINGB.SE] +1.1% (Earnings)]

Financials [Flow Traders [FLOW.NL] +13.0% (Earnings)]

Speakers

BoE Deputy Gov Broadbent reiterated MPC stance that rate hikes could come sooner than expected but will remain limited and gradual

UK PM May said to be planning Brexit meeting with senior cabinet ministers in two weeks’ time. Meeting requested after trade sub-committee ended without a decision

Czech Central Bank Feb Minutes: Interest rate outlook conditional on pace of CZK currency appreciation. Slow return of ECB to normal rates could inhibit Czech rate growth

Romania Central Bank gov Isarescu: Inflation acceleration was broad-based. Reiterated view that RON currency (Leu) had no more room for appreciation

Italy's Berlusconi Forza (Italia party): Gentiloni should stay as PM if no majority achieved at the March election

Currencies

Risk aversion sentiment remained on the front burner but the major FX pairs stayed locked within recent ranges. The USD maintaining its recent strength as some analysts believe the Fed might be behind the curve on rates. One analyst noted that given how sensitive markets were to a slightly hawkish BoE yesterday, one can only imagine the turmoil on Wednesday next week if US CPI comes in ahead of expectations

EUR/USD was slightly higher by 0.2% at 1.2270

GBP/USD at 1.3920

USD/JPY at 109.03

Fixed Income

Bund Futures trades down 7 ticks at 158.07 as the bearish trend remains intact. Upside targets 159.85, while a continued move lower targets the157.25 level.

Gilt futures trade at 121.09 down 8 ticks, as the BoE turns more hawkish. Support continues to stand at 120.75 then 120.15, with upside resistance at 122.75 then 123.25.

Friday's liquidity report showed Thursday's excess liquidity rose to €1.901T from €1.895T prior. Use of the marginal lending facility rose to €70M from €50M prior.

Corporate issuance saw 5 issuers raise $8.5B in the primary market.

Looking Ahead

(MX) Mexico Jan Nominal Wages: No est v 5.2% prior

(UR) Ukraine Jan CPI M/M: No est v 1.0% prior; Y/Y: No est v 13.7% prior

05:30 (RU) Russia Central Bank (CBR) Interest Rate Decision: Expected to cuts Key 1-Week Auction Rate by 25bps to 7.50%

06:00 (BR) Brazil Dec Retail Sales M/M: -0.5%e v +0.7% prior; Y/Y: 4.6%e v 5.9% prior

06:00 (BR) Brazil Dec Broad Retail Sales M/M: -0.9% v +2.5% prior; Y/Y: 5.7%e v 8.7% prior

06:00 (UK) DMO to sell combined £3.0B in 1-month, 3-month and 6-month Bills (£0.5, £0.5B and £2.0B respectively)

06:30 (IN) India Weekly Forex Reserves

06:30 (EU) EU chief Brexit negotiator Barnier to hold press conference

06:45 (US) Daily Libor Fixing

07:00 (UK) Jan NIESR GDP Estimate: 0.5%e v 0.6% prior

08:00 (RU) Russia Dec Trade Balance: $13.0Be v $11.5B prior

08:00 (IN) India announces upcoming Bill auction (held on Wed)

08:00 (ES) Spain Debt Agency (Tesoro) announces upcoming bond auction (held on Thurs)

08:05 (UK) Baltic Dry Bulk Index

08:30 (CA) Canada Jan Net Change in Employment: +10.0Ke v +64.8K prior (revised from +78.6K); Unemployment Rate: 5.8%e v 5.8% prior (revised from 5.7%)

09:00 (MX) Mexico Dec Industrial Production M/M: +0.4%e v -0.1% prior; Y/Y: -0.7%e v -1.5% prior, Manufacturing Production Y/Y: 2.5%e v 2.4% prior

10:00 (US) Dec Final Wholesale Inventories M/M: 0.2%e v 0.2% prelim, Wholesale Trade Sales M/M: 0.4%e v 1.5% prior

11:00 (EU) Potential sovereign rating after European close (Czech and Finland Sovereign Debt to be rated by Fitch

11:45 (UK) BOE’s Cunliffe in CA

13:00 (US) Weekly Baker Hughes Rig Count data

14:00 (CO) Colombia Central Bank Jan Minutes 21:00 (US) Fed’s George (non-voter, hawk) on economy

Technical Outlook: WTI OIL In Narrow Consolidation, Broader Bears Remain Intact And Threaten For Attack At Rising Daily Cloud

WTI oil is holding within narrow consolidation above fresh five-week low at $60.26 on Friday, after suffering heavy losses during the week.

Oil remains under strong pressure on increased US oil production, with fresh pressure coming from announcement of Iran's plans to boost production.

Steep two-week fall from recovery peak at $66.64, posted on 25 Jan, threaten of further extension through key supports at $60.00 zone (psychological support / Fibo 61.8% of $55.81/$66.64 ascend) and $59.51 (top of rising daily Ichimoku cloud).

Bears may take a stronger breather as ascending daily cloud underpins and daily slow stochastic is deeply oversold, but so far lacking stronger bullish signal.

Extended consolidation could be likely scenario as weekly indicators turned south after emerging from overbought territory and show plenty of space at the downside.

In addition, oil is on track for strong weekly bearish close (the second straight week in red and the biggest one week loss since early March 2017), which heavily weighs.

Broken 30SMA marks initial resistance at $60.90, with stronger upticks to be capped under previous pivotal support at $62.50 (broken Fibo 38.2% of $55.81/$66.64 rally).

Res: 60.90, 61.23, 62.07, 62.50

Sup: 60.26, 60.00, 59.51, 59.02

DAX Slide Continues As US Markets See Red

The DAX index has posted sharp losses in the Friday session. Currently, the index is trading at 12,210.00, down 0.41% on the day. On the release front, there are no German or Eurozone indicators on the schedule.

Nervous investors continues to watch the massive sell-offs in the markets, and European markets have been following the downward trend in the North American and Asian sessions. It’s been a blue February for the DAX, which has plunged 7.8 percent. On Thursday, the DAX dropped to its lowest level since early September. Interestingly, the catalyst for the current turbulence has been solid economic data in the US, namely, improved payrolls and wage growth reports. This has raised concerns of inflation, which could lead to a quicker pace of rate hikes from the Federal Reserve. This sentiment has sent the bond markets higher, while weighing on global stock markets.

It’s been a slow process, but Germany finally is on the verge of forming a new government. On Wednesday, the socialist SDP and Angela Merkel’s conservatives announced that they had finalized a coalition agreement. In the last government, the SDP was the junior partner of the conservatives, but this time around the SDP has extracted major concessions from Merkel, including the finance and foreign affairs ministries. This will likely mark a shift in Germany’s eurozone policy, which had been marked by a conservative stance under former finance minister Wolfgang Schaeuble. The weaker members of the eurozone, such as Greece, will likely find a more sympathetic ear for financial help from the SDP than they did from Schauble. The coalition agreement still requires the consent of a majority of the 464,000 members of the SDP, but is expected to pass this final hurdle.