Sample Category Title

XAU/USD Analysis: Returns To 55-Hour SMA

As previously expected, the yellow metal was driven by upside risks on Thursday. The scope of this move, however, was not in line with the forecasts. After testing the monthly S1 at 1,309.92 for a brief period of time, the pair managed to reverse and push up to the 55-hour SMA and the weekly S1—area where it was trading early on Friday. Technical indicators are neutral about the pair’s possible direction in this session; the overall tendency, however, should remain north. If the aforementioned resistance area is breached, traders could expect a continuous appreciation towards the 23.60% Fibo and the 200-hour SMA near 1,338.00; meanwhile, losses are unlikely to exceed the 1,305.00 mark. By and large, lack of fundamentals today might result in a period of consolidation.

USD/CAD: Canada NHPI

The Loonie depreciated versus the Greenback, as the weaker-than-expected new home prices report came in. The USD/CAD currency pair rose slightly on the data, but remained in the bearish trend.

New home prices in Canada revealed no change in December for the first time in more than two years, with the annual rate falling to 3.3% from 3.4% in the reported period, Statistics Canada said. Another report showed on Thursday that housing starts in the country fell less than anticipated in January, as new groundbreaking rose on single-detached houses in urban areas. The CMHC reported that a seasonally adjusted yearly rate declined slightly to 216.2K in January, following a downwardly revised 216.3K in December.

GBP/USD: BoE Interest Rate Decision

The Sterling jumped against the US Dollar more than 100 pips or 0.76%, just after the Bank of England’s monetary policy decision was announced on Thursday, and continued to appreciate further.

The BoE stated that the interest rate needed to be increased sooner and by more than it was thought three months earlier, as the Bank raised economic growth expectations for Britain amid the solid global recovery. The Bank of England anticipated the economy to expand 1.75% year-on-year in average over the next couple of years. The sluggish outlook of the UK was attributable to weaker growth in labour force amid the UK aging population and fewer immigrants coming into the country. Meanwhile. Pay growth would rise to 3% by the end of this year, as projected.

Technical Outlook: USDJPY – Bears Remain In Play, Consolidation To Precede Fresh Downside

The dollar rose above 109 barrier in early Europe after retesting support at 108.50 zone overnight, bur recovery was so far capped by sideways-moving 10SMA (109.24).

Extended consolidation under falling 20SMA (109.74) before fresh attempts at key 108.28 support is seen as likely near-term scenario, as daily studies remain negative and building bearish momentum.

Eventual break below 108.28 (26 Jan low) would open way for test of psychological 108.00 support and final push towards key short-term support at 107.31 (09 Sep low).

Conversely, lift above 20SMA (109.74) would delay bears, but extension above 110.32/48 (Fibo 38.2% of 113.63/108.28 / 02 Feb recovery high)is needed to neutralize and turn focus higher.

Res: 109.24, 109.54, 109.74, 110.32

Sup: 108.50, 108.28, 108.00, 107.31

Technical Outlook: EURUSD – Recovery Attempts Need Break Above 1.23 Pivot To Sideline Persisting Downside Risk

The Euro moved higher on Friday, in recovery attempt after broader bears were contained by rising 30SMA at 1.2212 on Thursday.

Initial sign of basing is seen on bounce from 1.2212, but recovery is still holding below 1.2300 pivot (former strong support – Fibo 38.2% of 1.1915/1.2537 rally), weighed by thick descending hourly cloud (spanned between 1.2297 and 1.2340)

Stronger recovery needs lift above hourly cloud and 10SMA (1.2368) to generate stronger bullish signal and confirm higher low formation.

However, weak momentum studies on daily chart (14-day momentum is attempting to break into negative territory) warn about recovery stall.

Stronger bearish signal could be expected on firm break below rising 30SMA which would open support at 1.2153 (Fibo 61.% of 1.1915/1.2537).

Res: 1.2300, 1.2331, 1.2368, 1.2404

Sup: 1.2240, 1.2212, 1.2153, 1.2089

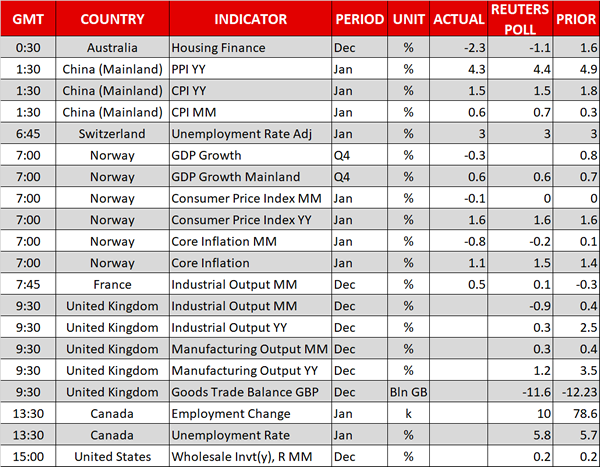

Equities Topple While US Government Shuts Down, UK Industrial Output & Canadian Jobs Report Due

Here are the latest developments in global markets:

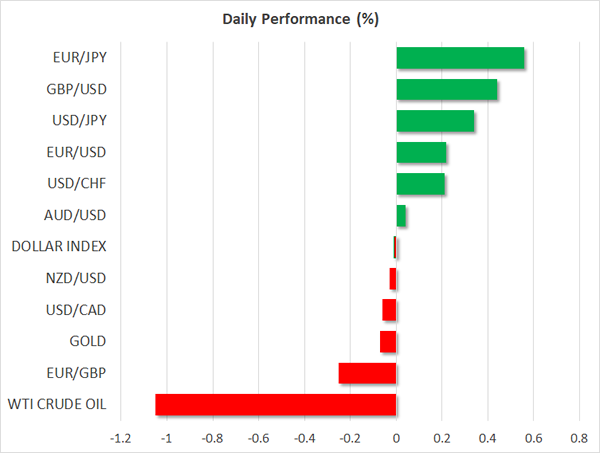

FOREX: The dollar index was practically unchanged on Friday, remaining unfazed by the shutdown of the US government. Meanwhile, sterling gave back all of the gains it posted after the Bank of England appeared more hawkish yesterday.

STOCKS: The turmoil in global equity markets got a second wind on Thursday, with US stock indices collapsing once more. The Dow Jones led the way lower, shedding 4.1% of its value, while the Nasdaq Composite and S&P 500 followed in its tracks, closing lower by 3.9% and 3.8% respectively. It is worth noting that all three indices closed below their respective 100-day moving averages. According to futures though, the Dow, S&P, and Nasdaq 100 are all anticipated to open in positive territory today. The negative sentiment rolled over into Asian trading as well, with Japan’s Nikkei 225 and Topix falling by 2.3% and 1.9% accordingly. In Hong Kong, the Hang Seng was down by 3.3%. As for Europe, futures tracking the Euro STOXX 50 are very close to neutral territory.

COMMODITIES: Oil prices drifted lower alongside energy stocks yesterday, and extended their losses on Friday, with WTI and Brent crude trading lower by 1.0% and 0.7% respectively. Besides risk sentiment, the other potential driver of prices today may be the release of the US Baker Hughes oil rig count, due at 1800 GMT. Following the latest EIA data showing that US oil output soared to record highs, any further increase in rigs could signal that production may have risen even further, and thereby keep prices under pressure. Gold traded fractionally lower, last seen near the $1,317 level. It is quite puzzling that the safe-haven metal has not responded to the turbulence in equity markets lately, drifting lower in recent days even despite the broader risk-off sentiment.

Major movers: Sterling surrenders BoE-related gains; US government shuts down; equity volatility remains in the spotlight

The Bank of England (BoE) kept its policy unchanged yesterday via a unanimous vote, as was widely anticipated. The Bank appeared quite optimistic on the economy’s outlook, noting that GDP growth is expected to be faster moving forward even despite the higher market-implied path for interest rates and the stronger exchange rate. On the inflation front, the BoE now anticipates the CPI rate to fall to 2.16% in two years’ time, just shy of its 2% target.

Moreover, the Bank vindicated those looking for faster rate hikes in the future. It noted that according to its new projections, monetary policy may now need to be tightened somewhat earlier and to a greater extent than anticipated back in November. The British pound surged on these hawkish signals, as the implied probability for a rate hike in May rose to 70%, from roughly 50% prior to the meeting. Nonetheless, sterling was unable to hold onto its BoE-related gains, retreating in the following hours to trade virtually unchanged against most of its major counterparts, and even lower against the yen.

In the US, the government has now officially shut down, as Congress missed a deadline to approve the bill that would raise spending limits over the next two years. The Senate did approve the bill, but the House still has to vote on it in order to end the shutdown, something very likely to happen today. Importantly, if approved, this bill would balloon the US deficit by another $300 billion, making the US debt outlook even more unsustainable. These concerns have begun to show up in the bond market, where yields on 10-year Treasuries rose to 2.85%. This surge in yields may be another factor weighing on US and global equities. As Treasury yields rise, bonds begin to offer a better and “safer” return, curbing demand for equities.

The volatility in equity markets is likely to remain at the forefront of attention for a while more, as investors try to gauge whether the correction is over or whether it still has more legs to run. US equity indices closed below their 100-day moving averages yesterday, with the S&P 500 now being roughly 10% lower than its peaks. The lower these indices go, the more attractive they become from a valuation perspective for investors looking to “buy the dip”, a factor that could help to stem the decline.

Elsewhere, the Australian dollar remained under pressure yesterday. Besides the broader risk-averse sentiment, the tumble may have been owed to some dovish comments from RBA Governor Philip Lowe, who noted that he doesn’t “see a strong case” for a near-term rate hike.

Day ahead: UK industrial & manufacturing output and Canadian jobs report on the agenda

Industrial and manufacturing output figures for December out of the UK are due at 0930 GMT. After the upbeat releases of previous months, the numbers are expected to ease on an annual and monthly basis, with industrial production even forecasted to contract in December relative to the month that preceded. UK data on the goods trade balance are also scheduled for release at the same time.

Canada’s jobs report for the month of January will be made public at 1330 GMT. Projections point to a “soft” report relative to the preceding month, though it could be argued that a “soft” report was forecasted in December as well, and the actual figures ended up storming past expectations. Specifically, the economy is expected to have added 10k positions (versus 78.6k in December) and the unemployment rate is expected to have risen to 5.8% from 5.7% in December, though that would be linked to more individuals entering the labor force – being optimistic that they could find a job – rather than to weakness in the jobs market. It would be interesting to see if the release alters the market’s perception as regards the speed with which the Bank of Canada will deliver additional interest rate rises moving forward.

Data on US wholesale inventories for the month of December are due at 1500 GMT.

In US politics, there was not much of a reaction after Congress missed a deadline to renew funding for the US government, triggering a partial shutdown. However, this situation might not last for long; the Senate did approve the stop gap bill and budget deal with a House vote pending.

Jon Cunliffe, the Bank of England’s Deputy Governor for Financial Stability will be speaking at 1645 GMT.

The US Baker Hughes oil rig count is due at 1800 GMT. If it shows an increase in active rigs, oil prices could come under pressure on speculation that US output may increase further.

Corporations continue to release quarterly results as the equity market turmoil continues

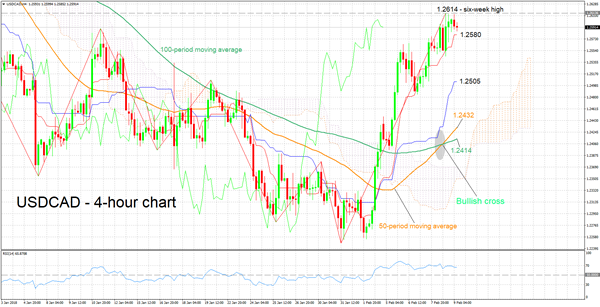

Technical Analysis: USDCAD close to 6-week high; Tenkan- and Kijun-sen positively aligned

USDCAD has posted considerable gains in recent days, reaching a six-week high of 1.2614 during Thursday’s trading. The pair is currently trading not far below this level.

The Tenkan- and Kijun-sen lines are positively aligned, pointing to bullish short-term momentum. The RSI is in bullish territory above 50, supporting the case for a positive bias, though notice that it is moving sideways. This is perhaps an indication that positive momentum is losing steam. Also, the indicator is relatively close to the 70 overbought level.

A strong jobs report out of Canada, is anticipated to lead to weakness in USDCAD, with the range around the Tenkan-sen at 1.2580 – including the 1.26 handle, a level that may be of psychological importance – potentially offering support. A violation of this area would turn the attention to the one around the Kijun-sen at 1.2505.

Weaker Canadian data on the other hand, are expected to see the pair advancing. Thursday’s high of 1.2614 could provide resistance in this case, with 1.27 being eyed next in case of an upside break from 1.2614. The area around the 1.27 handle was relatively congested in the past.

Technical Outlook: Pound Struggles To Regain 1.40 Pivot Despite Support From Hawkish Comments And Weaker Dollar

Cable holds firm tone on Friday and attempts again towards psychological 1.40 barrier, following Thursday's spike to 1.4066 after BoE rate decision and subsequent quick pullback. Sterling was boosted by hawkish hold from BoE, as the central bank kept interest rate unchanged but signaled hikes in the near future. Additional support was provided by hawkish comments from BoE deputy governor Broadbend on Friday, who said that couple of hikes in 2018 shouldn't be a great shock. Also, weaker US dollar on the second shutdown of the US government sine the beginning of the year, underpinned pound on Friday. Fresh attempts higher on Friday look for renewed probe above 1.40 trigger (Fibo 38.2% of 1.4277/1.3835 pullback/rising 20SMA), with close above here needed to generate bullish signal for extension of recovery rally from 1.3840, where higher base is forming. Technical studies send mixed signals as daily slow stochastic is attempting to emerge from oversold territory but momentum is in the negative territory. Prolonged consolidation with immediate risk shifted lower could be expected while the price stays below 1.40 pivot. Next important support lies at 1.3900 (daily Kijun-sen / near session low) and break here would generate bearish signal for retest of 1.3840 base and extension towards Fibo support at 1.3800 (61.8% of 1.3457/1.4344 rally).

Res: 1.4000, 1.4043, 1.4066, 1.4109

Sup: 1.3940, 1.3900, 1.3856, 1.3835

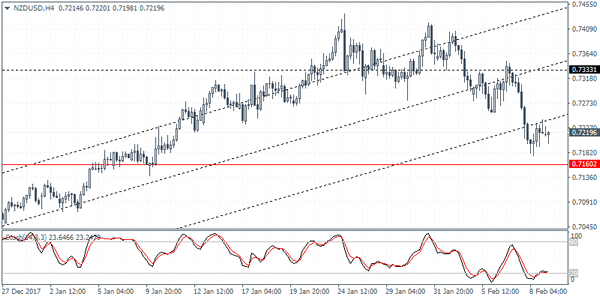

NZDUSD Intraday Analysis

NZDUSD (0.7211): The New Zealand dollar continues to extend the declines with the RBNZ's dovish statement earlier this week. The reversal off the 0.7333 support turned resistance indicates a decline to the initial support at 0.7160. NZDUSD could be seen rebounding off this level. If the support holds, we anticipate a potential inverse head and shoulders pattern being formed, visible on the daily time frame. With the neckline resistance seen at 0.7333 - 0.7350, NZDUSD could be potentially consolidating for a stronger breakout to the upside. The bias is invalidated on a break down below the 0.7160 support.

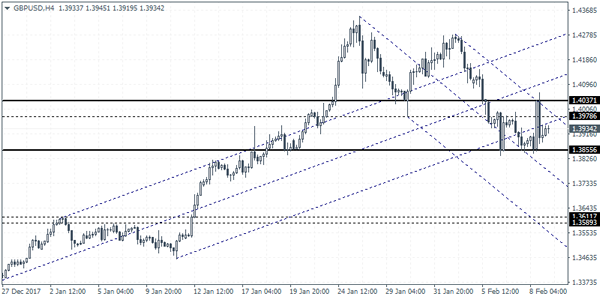

GBPUSD Intraday Analysis

GBPUSD (1.3934): The British pound was seen to be volatile yesterday on the back of the Bank of England monetary policy meeting. As noted in yesterday's commentary, GBPUSD initially rallied to 1.4037 but with the resistance holding up, price action promptly reversed gains. We expect GBPUSD to maintain a sideways range within 1.4037 and 1.3855. A breakout from this range will establish further direction in the currency pair. The bias is to the downside and we expect GBPUSD to eventually breakout below 1.3855 to fall towards 1.3611 - 1.3589 level of support.

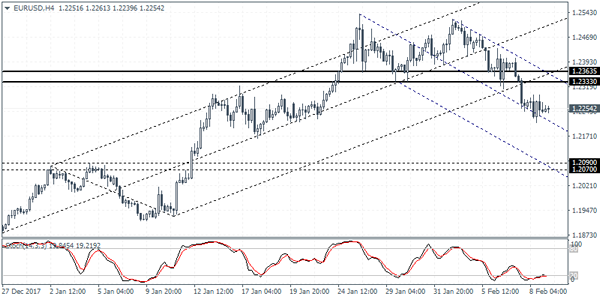

EURUSD Intraday Analysis

EURUSD (1.2254): The EURUSD extended declines as prices touched a fresh monthly low at 1.2211 before pulling back slightly. The daily session in the EURUSD ended with a spinning bottom candlestick pattern that could suggest a near term recovery in the declines. On the 4-hour time frame, EURUSD is seen consolidating near 1.2237 retesting the January 23 lows. We expect to see a pullback in prices that could see EURUSD retesting the broken support level at 1.2363 - 1.2333. If resistance is established here, then EURUSD could extend declines down to 1.2090 - 1.2070 level in the medium term. The bias shifts if price manages to breakout above 1.2363, resistance high