Sample Category Title

EUR Fixed Income Markets Fluctuated Quite A Lot

Market movers today

A very quiet day in terms of major economic data releases.

See next page for market movers in Scandi today.

Selected market news

Bank of England (BoE) sent a more hawkish message than we and markets had expected, as it is concerned about overheating the economy. This is also the reason why we now expect the BoE to hike by 25bp already in May (although admittedly it is a somewhat close call between May and August ) and launch a hiking cycle.

EUR fixed income markets fluctuated quite a lot during yesterday's trading session. On the back of BoE hawkish message yields climbed higher. However, later in the afternoon spillover from risk off sentiments in equity markets weighed in yields, e.g. with the equity volatility index VIX increasing from around 25 to above 30 yesterday after the index has been t rending lower since the major risk-off day in the financial markets on Monday. Overnight , the risk-off sentiments in equity markets continued with Asian stock markets in red.

In the US, Fed nominee Goodfriend was approved by the senate banking committee yesterday. The vote was 13-12, making it a close call whether he will be approved by the full Senate, where the Republicans only has a very slim majority 51-49.

Yesterday, Fed's William Dudley said in a Bloomberg interview, that ‘the little decline that we've had in the equity market today has virtually no implications for the economic outlook', indicating (as expected) that the Fed is seeing through the current market turmoil – it has to be more persistent for the Fed to become concerned.

The US Government entered a partial shutdown as Congress missed the midnight deadline to pass the two-year spending bi ll announced on Wednesday. The House and Senate plan votes early Friday morning. The USD300bn two-year spending bill also includes a suspension of the debt limit until March 2019, meaning Treasury can start rebuilding its cash buffer again, which will drain USD liquidity if passed.

Market Update – Asian Session: Asian Equities Track Declines In US

Headlines/Economic Data

General Trend

Shanghai Composite and Hang Seng decline over 4%

Currency volatility relativity muted vs equities

Australia/NewZealand

ASX 200 opened -0.4%: closed -0.9%%

Energy -2.4%,Telecom -1.8%, Utilities -1.8%, Consumer Discretionary -1.6%, Resources -1.2%, Financials -0.9%

(AU) RESERVE BANK OF AUSTRALIA (RBA) QUARTERLY STATEMENT ON MONETARY POLICY (SOMP): QUARTERLY INFLATION AND GROWTH FORECASTS LITTLE CHANGED

(AU) Australia Dec Home Loans M/M: -2.3% v-1.0%e; Investment Lending: -2.6% v +1.5% prior

(AU) Australia sells A$400M v A$400M indicated in July 2022 bonds, avg yield 2.2838%, bid to cover 5.79x

China/Hong Kong

Shanghai Composite opened -2.7%, Hang Seng -2.5%

Hang Seng Materials Index -4.9%, Services -4.1%

(CN) CHINA JAN CPI M/M: 0.6% V 0.3% PRIOR: Y/Y:1.5% V 1.5%E

(CN) China Jan PPI Y/Y: 4.3% v 4.3%e

(CN) China won’t face big inflationary pressure in 2018 – China Securities Journal

(CN) PBOC SETS YUAN REFERENCE RATE AT 6.3194 V 6.2822 PRIOR

(CN) China PBoC: Skips OMO (12th straight session)

(CN) PBoC: Has released Temporary liquidity worth almost CNY2.0T (under previously announced measures); measure seeks to satisfy cash demand before Lunar New Year; Previously announced targeted RRR cuts inject about CNY450B in liquidity.

(CN) China to cut gasoline by CNY170/ton - Press

Looking Ahead: China Jan Bank Lending data maybe released during the European session

Japan

Nikkei 225 opened -1.8%; closed -2.3%

TOPIX Electric Appliances Index -3.4%, Iron & Steel -3.3%, Securities -3%,Real Estate -3%

Nissan Motors [7201.JP]: Declines over 3.5%after revising FY guidance

Nexon [3659.JP]: Gains over 14% after reporting FY results and announcing stock split

Nikkei 225 Feb options said to settle at 21,190

Japan PM Abe Adviser Hamada: Recent stock declines could make BoJ cautious about raising rates

Japan Fin Min Aso: Various factors are behind stock market moves; US and global economy’s fundamentals are‘not bad’

BOJ announcement related to daily bond buying operation: leaves amounts unchanged

Korea

Kospi opened -2.5%

Samsung Electronics has declined by over 2.5%

(KR) South Korea Fin Min Official: Will take action to stabilize financial markets should uncertainties spread; to strengthen monitoring of FX market

Other Asia

(PH) Philippines Dec Trade Balance: -$4.0B(multi-year high for the deficit) v -$3.0Be

(PH) Philippines Central Bank(BSP) Gov Espenilla comments after central bank left rates unchanged on Thursday: ‘Inflation spike’does not warrant immediate tightening

North America

US equity markets ended lower: Dow -4.2%, S&P500 -3.8%, Nasdaq -3.9%, Russell 2000-2.9%

S&P500 Financials -4.4%, Technology -4.1%

(US) Fed's Dudley (dove, FOMC voter): Decline inequity markets doesn't have economic implications at this point; so far stock selloff has been 'small potatoes'; Main outlook for three rate hikes is reasonable; could do four hikes if economic outlook gains; Bond yields moving higher is putting pressure on stocks; US govt debt service costs are likely to rise a lot - TV interview

(US) Fed's George (hawk): 3 rate hikes for 2018 and 2019 would be reasonable unless economic outlook changes

(US) TREASURY'S $16B 30-YEAR BOND AUCTION DRAWS 3.121%; BID-TO-COVER RATIO: 2.26 V 2.23 PRIOR AND 2.25 AVG OVER THE LAST 4 AUCTIONS (highest yield since March 2017, lowest BTC since Nov)

(US) House GOP Leaders say next votes [related to funding] to come after 12 AM EST government funding deadline - US financial press

(US) Office of Management and Budget (OMB) said to direct agencies to prepare for possible shutdown if Congress cannot pass funding bill by the midnight deadline – Washington Post

(US) President Trump expected to propose reducing some drug costs for Medicare - US press

(US) US said to consider 'emergency' support for coal plants - US financial press

Levels as of01:00ET

Hang Seng -3.5%;Shanghai Composite -4.8%; Kospi -1.8%

Equity Futures:S&P500 +0.3%; Nasdaq100 +0.2%, Dax +0.3%; FTSE100 +0.3%

EUR 1.2240-1.2265 ;JPY 108.49-109.11; AUD 0.7758-0.7794 ;NZD 0.7198-0.7231

Feb Gold flat at $1,319/oz;Feb Crude Oil -1% at $60.53/brl; Mar Copper -0.2% at $3.067/lb

GBP/JPY Daily Outlook

Daily Pivots: (S1) 151.01; (P) 152.06; (R1) 152.79; More...

GBP/JPY's decline resumed after brief consolidation and intraday bias is back on the downside for 150.18 support. . Considering bearish divergence condition in daily MACD, the near term trend could have reversed. Break of 150.18 will affirm this case and target 146.96 key support level.

In the bigger picture, as long as 146.96 key support holds, medium term outlook remains bullish. Rise from 122.36 is in favor to extend to 61.8% retracement of 195.86 to 122.36 at 167.78. However, break of 146.96 support will indicate trend reversal. In that case, deeper fall would be seen to 38.2% retracement of 122.36 to 156.59 at 143.51 and then 61.8% retracement at 135.43.

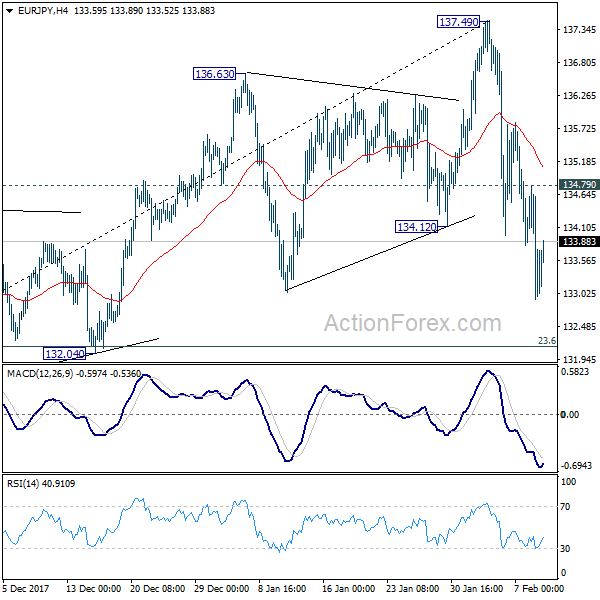

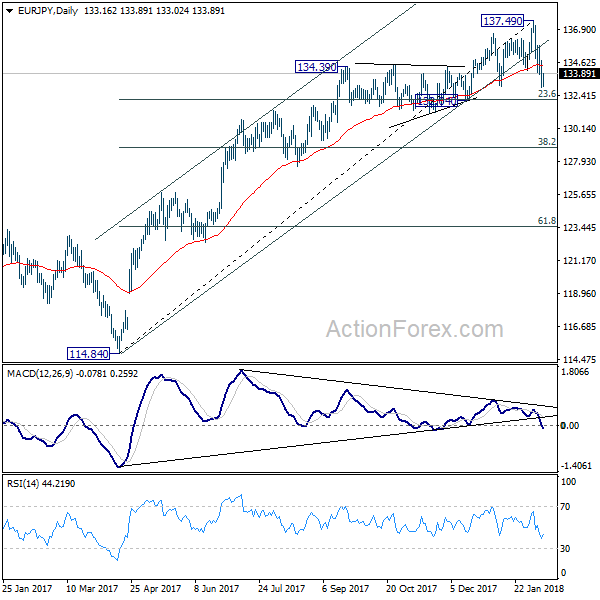

EUR/JPY Daily Outlook

Daily Pivots: (S1) 132.48; (P) 133.63; (R1) 134.34; More....

EUR/JPY's decline from 137.49 is still in progress and intraday bias remains on the downside for 132.04 cluster support first (23.6% retracement of 114.84 to 137.49 at 132.14). Decisive break there will indicate larger trend reversal on bearish divergence condition in daily MACD. On the upside, though, above 134.79 minor resistance will turn intraday bias neutral first.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). It should be targeting 141.04/149.76 resistance zone. On the downside, break of 132.04 support, however, will be an early sign of trend reversal and will bring deeper fall back to 124.08 key medium term support.

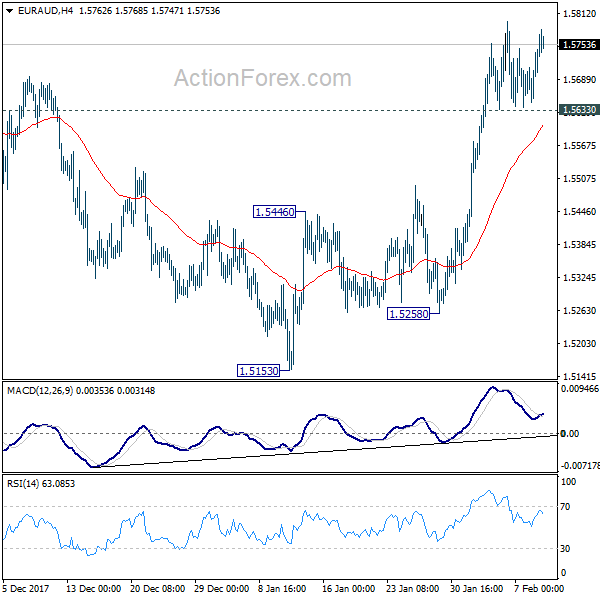

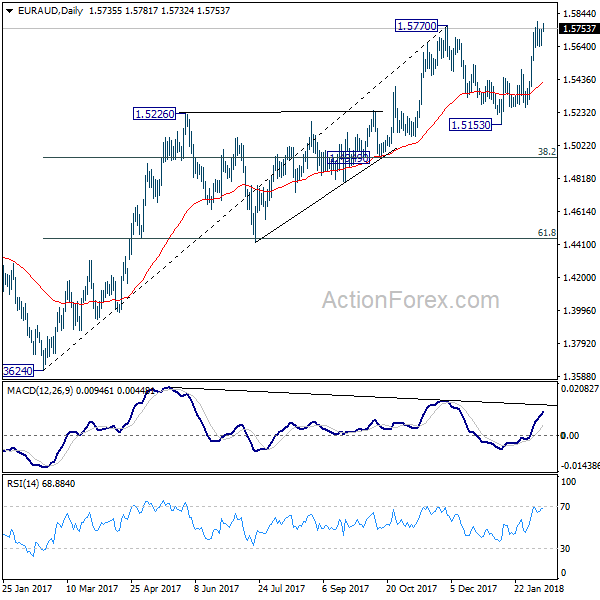

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5675; (P) 1.5709; (R1) 1.5771; More....

As long as 1.5633 minor support holds, further rise is expected in EUR/AUD. The breach of 1.5770 resistance suggests that medium term rise from 1.3264 is resuming. Sustained trading above 1.5770 will pave the way to 1.6587 key long term support. Nonetheless, below 1.5633 minor support will dampen this bullish case and turn intraday bias neutral first.

In the bigger picture, medium term rise from 1.3624 is not completed yet. Break of 1.5770 will extend the rise to retest 1.6587 (2015 high). However, considering bearish divergence condition in daily MACD, sustained break of 1.4949 cluster support (38.2% retracement of 1.3624 to 1.5770 at 1.4950) will indicate medium term reversal. And there is prospect of retesting 1.3624 low in that bearish case.

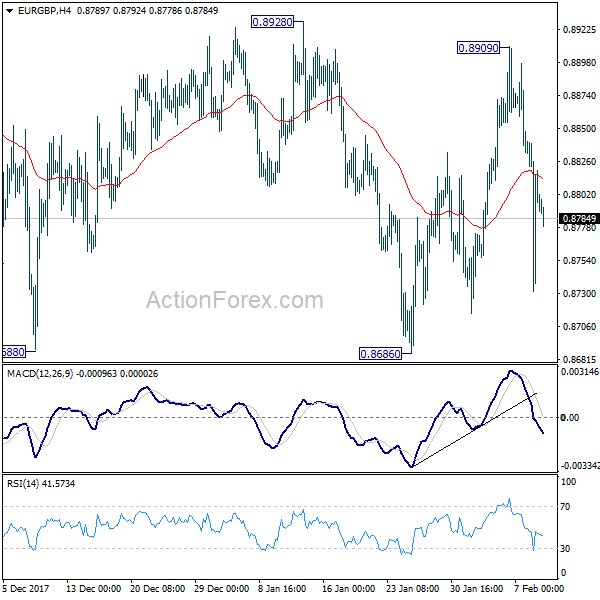

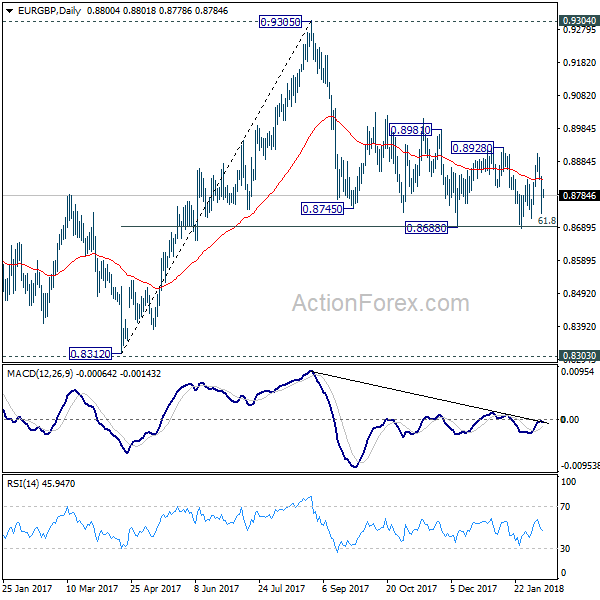

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8742; (P) 0.8791; (R1) 0.8851; More...

Despite steep fall from 0.8909, EUR/GBP is still bounded in range of 0.8686/8928. Intraday bias remains neutral for the moment. And, near term outlook will remain mildly bearish as long as 0.8928 resistance holds. On the downside, firm break of 0.8686 will resume whole decline from 0.9305. As 61.8% retracement of 0.8312 to 0.9305 should then be taken out too. Deeper decline would be seen to retest 0.8303/8312 support zone. Nonetheless, on the upside, break of 0.8928 will indicate near term reversal and turn outlook bullish for 0.9304 resistance.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

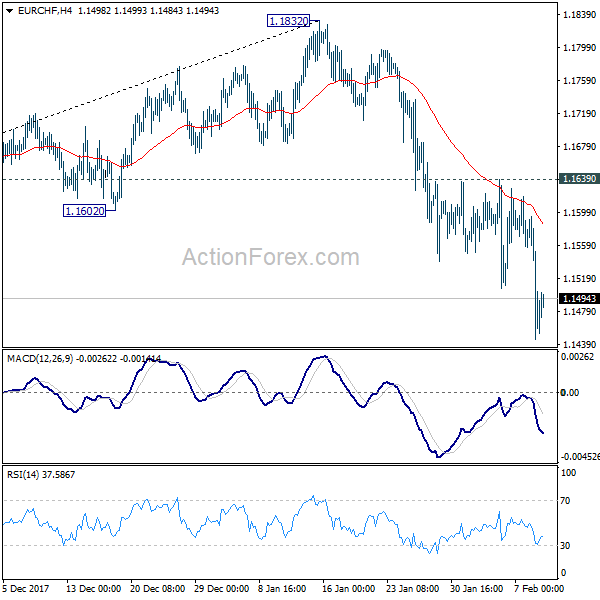

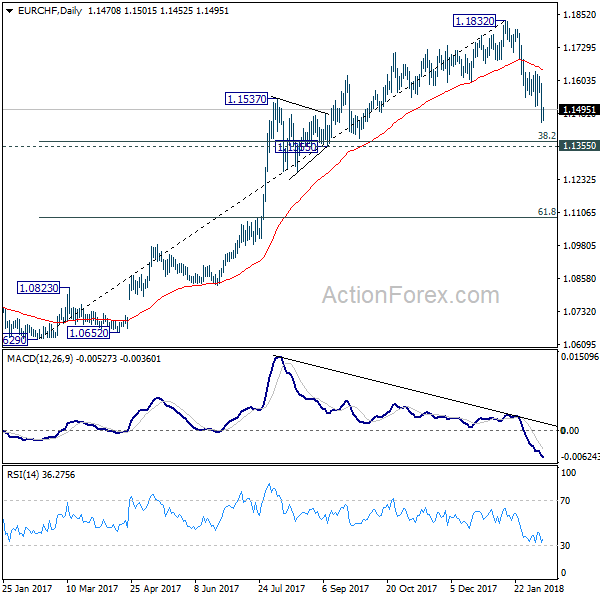

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1407; (P) 1.1500; (R1) 1.1556; More...

EUR/CHF's decline extends to as low as 1.1445 so far and intraday bias is back on the downside. Current fall from 1.1832 is correcting medium term rise from 1.0629. Next target will be 1.1355 cluster support (38.2% retracement of 1.0629 to 1.1832 at 1.1372.) On the upside, break of 1.1639 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, a medium term top should be in place at 1.1832 on bearish divergence condition in daily MACD. But there is no indication of long term reversal yet. As long as 1.1198 resistance turned support holds, we'd still expect another rise through prior SNB imposed floor at 1.2000.

RBA Upbeat On Economy, Slashed Unemployment Forecast

For the 24 hours to 23:00 GMT, the AUD declined 0.66% against the USD and closed at 0.7776, after the Reserve Bank of Australia's (RBA) Governor, Philip Lowe, diminished the odds of an imminent interest rate hike, on the backdrop of sluggish wage growth and scant inflationary pressures. Nevertheless, Lowe expressed confidence that a pick-up in economic growth would gradually fuel inflation and reduce unemployment.

LME Copper prices declined 2.4% or $168.0/MT to $6838.0/MT. Aluminium prices declined 0.6% or $13.5/MT to $2168.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7779, with the AUD trading slightly higher against the USD from yesterday's close.

Overnight, the Reserve Bank of Australia (RBA), in its quarterly statement on monetary policy, stated that it continues to anticipate Australian economic growth to slightly pick-up over the next two years. Further, the central bank added that unemployment will decline faster than expected and that inflation will remain below its 2.00%-3.00% target range until the middle of next year. Additionally, the jobless rate is estimated to slip to 5.25% by mid-2018 and remain there until 2020.

Elsewhere in China, Australia's largest trading partner, the consumer price index (CPI) rose 1.5% on an annual basis in January, at par with market expectations and rising at its weakest pace in 7 months. In the prior month, the CPI had advanced 1.8%. Further, the nation's producer price index (PPI) grew 4.3% YoY in January, meeting market anticipations. In the prior month, the PPI had gained 4.9%.

The pair is expected to find support at 0.7744, and a fall through could take it to the next support level of 0.7710. The pair is expected to find its first resistance at 0.7828, and a rise through could take it to the next resistance level of 0.7878.

Moving ahead, Australia's unemployment rate, consumer inflation expectations, NAB business confidence and Westpac consumer confidence indices, all slated to release next week, would keep investors on their toes.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Robust Growth Expected To Continue In The Near Term: ECB Economic Bulletin

For the 24 hours to 23:00 GMT, the EUR declined 0.24% against the USD and closed at 1.2249.

Yesterday, the European Central Bank (ECB), in its latest economic bulletin report, stated that the Euro-zone economy is expected to continue its robust pace of economic expansion beyond the near term. While the central bank noted that economic progress was yet to bring a self-sustaining rise in inflation, it indicated that officials grew more confident that inflation will eventually converge towards its 2.0% inflation target.

In economic news, Germany’s seasonally adjusted trade surplus narrowed more-than-estimated to €18.2 billion in December, compared to a surplus of €23.7 billion in the previous month, while markets were expecting the country’s trade surplus to drop to €21.0 billion.

Macroeconomic data revealed that the number of Americans filing for fresh jobless claims unexpectedly dipped to a level of 221.0K in the week ended 03 February, dropping to its lowest level in nearly 45 years and pointing to a rapidly diminishing slack in the labour market. Initial jobless claims had registered a level of 230.0K in the prior week, while investors had envisaged for a rise to a level of 232.0K.

In the Asian session, at GMT0400, the pair is trading at 1.2255, with the EUR trading slightly higher against the USD from yesterday’s close.

The pair is expected to find support at 1.2213, and a fall through could take it to the next support level of 1.2171. The pair is expected to find its first resistance at 1.2296, and a rise through could take it to the next resistance level of 1.2337.

With no major macroeconomic releases in the Euro-zone today, investors would focus on the US final wholesale inventories data for December, set to release later in the day.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

BoE Left The Key Interest Rate Unchanged At 0.50%, Signalled At Sooner And Sharper Rise In Interest Rates

For the 24 hours to 23:00 GMT, the GBP rose 0.19% against the USD and closed at 1.3923, after the Bank of England (BoE) lifted UK's economic growth forecasts and hinted at rapid monetary policy tightening.

The BoE, at its February monetary policy meeting, opted to keep the benchmark interest rate steady at 0.50%, as widely expected. In an accompanying statement, the central bank indicated that borrowing costs could rise sooner than expected and by a somewhat greater degree in order to prevent the Brexit-weakened economy from overheating. In its quarterly inflation report, the BoE nudged up Britain's economic growth outlook to 1.80% for this year, up from its prior estimate of 1.60%, stating that UK trade would benefit from a strong global upswing. Additionally, growth estimate for 2019 was revised up 0.10% to 1.80%. Meanwhile, the central bank projected that annual inflation rate would hit 2.40% in 2018 before slowing to 2.20% next year.

In the Asian session, at GMT0400, the pair is trading at 1.3935, with the GBP trading 0.09% higher against the USD from yesterday's close.

The pair is expected to find support at 1.3832, and a fall through could take it to the next support level of 1.3728. The pair is expected to find its first resistance at 1.4053, and a rise through could take it to the next resistance level of 1.4170.

Moving ahead, all eyes would be on UK's industrial as well as manufacturing production, total trade balance and construction output data, all for December, slated to release in a few hours. Moreover, the NIESR GDP estimate for the three months ended January 2018, set to release later today, will also be on investors' radar.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.