Sample Category Title

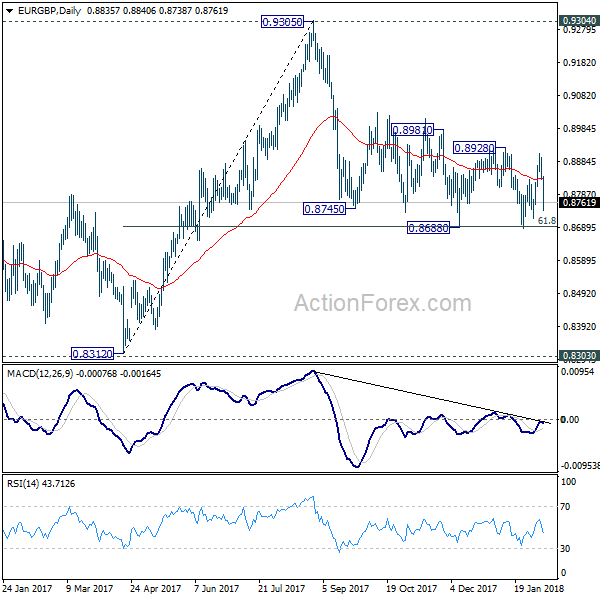

EURGBP – Bearish Acceleration on Hawkish BoE Threatens for Retest of Key S/T Supports at 0.8689/86

The cross accelerated sharply lower after hawkish stance from BoE today, being down 1.2% for the day so far, in extension fall from 0.8897 on Wednesday.

Fresh weakness turned daily techs into full bearish setup which may result in final push towards key short-term supports at 0.8686/89 (25 Jan / 08 Dec lows).

The cross hit new one-week low at 0.8732, cracking support at 0.8739 (Fibo 76.4% of 0.8686/0.8910 rally) and eyes the last obstacle en-route to 0.8686 target at 0.8716 (01 Feb trough).

However, the action on hourly chart shows that bears may take a breather on strongly oversold hourly studies, but limited upside could be expected for now, as a cluster of bearishly aligned daily MA's lies above.

Hourly Tenkan-sen (0.8786) is expected to ideally cap upticks.

Bigger picture shows the cross moving within bearish channel since Oct 2017 with supports at 0.8686/89 marking also Fibo 61.8% of larger 0.8312/0.9306, Apr/Aug 2017 ascend) and firm break here would be strong bearish signal for continuation of larger downtrend from 0.9306 (29 Aug peak).

Weekly studies are turning to bearish mode and showing space at the downside which could accommodate further easing.

Res: 0.8786; 0.8804; 0.8840; 0.8856

Sup: 0.8732; 0.8716; 0.8686; 0.8640

Sunset Market Commentary

Markets:

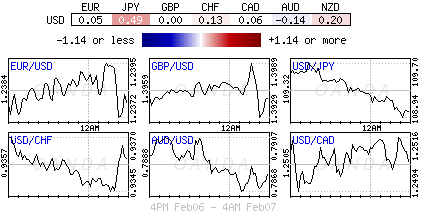

Global core bonds traded with a small downward bias today. US Congress' bipartisan agreement on a 2-yr funding bill which will increase spending by $300 bn and result in higher US budget deficits, still weighed on core bond sentiment in the first hours of trading. The sell-off accelerated around noon via the UK Gilt market after an hawkish inflation report by the Bank of England. Weakness on European stock markets couldn't turn the tide. ECB/Fed speak and eco data didn't influence trading neither. ECB governors Praet and Weidmann fulfilled their usual roles as monetary dove and hawk, though the former stressed future changes on interest rate guidance. Dallas Fed Kaplan and Philly Fed Harker aligned with the 2018 Fed scenario of 3 rate hikes. Weekly US jobless claims continue to hover near historically low levels. The US yield curve bear steepens with yields 0.2 bps (2-yr) to 3.8 bps (30-yr) higher. Changes on the German yield curve range between +0.7 bps (2-yr) and +3.4 bps (30-yr). 10-yr yield spread changes versus Germany are narrowly mixed with Greece underperforming (+6 bps). Greece returned to the bond market with a new syndicated 7-yr deal (€3 bn Feb2025). The bond was priced to yield 3.5%, at the tight end of 3.5%-3.625% guidance. The order book exceeded €6.8 bn. The Greek government aims to create a cash buffer of about €20 bn by the time its bailout program ends in August, of which half will come from markets.

Rising US yields and the prospect of higher US budget deficits propelled the dollar yesterday. The greenback remained well bid in Asia and in Europe this morning. USD/JPY was supported by a constructive equity sentiment. EUR/USD saw some follow-trough selling after yesterday's break below 1.2323 support. EUR/GBP selling after the BoE's policy statement pushed EUR/USD to an intraday low in the 1.2215 area. From there, the euro decline/USD rally stalled. EUR/USD returned to 1.2250/75 area. Core yields remain upwardly oriented, but for new it is no additional help for the dollar. US jobless claims dropped to a very low 221 000, but didn't help the dollar. This evening's 30-year US bond auction might be a next point of reference for interest markets and for the dollar.

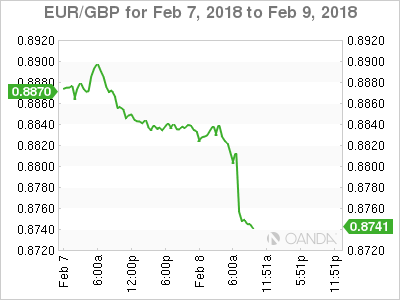

Focus for sterling trading was on the policy statement and inflation report of the Bank of England (BoE). The BoE as expected left is policy rate unchanged at 0.5%. The BoE was more optimistic on growth/demand compared to its November inflation report. A further reduction in the available spare capacity in the economy will keep inflation above target over the policy horizon. This indicates that a faster pace of rate hikes might be needed than anticipated until now. Market expectations for a May UK rate hike have risen to about 65% after the BoE policy statement (from about 50% before). The prospect of additional interest rate support propelled sterling. EUR/GBP dropped from the 0.88+ area and filled bids in the 0.8735 area. However, the 0.8690 range bottom stayed out of reach for now. Cable rebounded back above the 1.40 barrier.

News Headlines:

The Bank of England said that earlier and larger interest rises are likely to damp the effects of a stronger global economy on UK inflation. In a hawkish quarterly inflation report, all of the BoE's MPC agreed that the central bank was no longer willing to tolerate inflation above its 2% target for the next three years.

Germany's trade surplus fell last year for the first time since 2009, in a further sign that vibrant domestic demand is sucking in more imports and slowly re-balancing the country's export-oriented economy.

Canadian Housing Starts Remained Strong to Start 2018

Highlights:

- Housing starts came in a bit stronger than expected in January, holding steady at December's revised 216k annualized pace.

- Both single and multi-unit starts were little changed from the previous month.

- The six-month trend in starts edged up to a decade high of 227k

- Housing starts remained volatile in Ontario, rebounding strongly in January after a sizeable dip in December. That offset declines in BC, Quebec and Atlantic Canada to start the year.

Our Take:

Canadian homebuilders didn't seem to be impacted by a cold January as starts held up at a relatively strong 216k annualized pace. That follows decade-high housing starts last quarter and in 2017 as a whole. We doubt last year's 220k pace can be sustained but the underlying trend in homebuilding is clearly stronger than some household formation data would indicate. New construction has been solid despite slower home sales last year, though a pullback in single unit construction in Ontario relative to a year ago does seem to reflect softness in that segment of the resale market.

We expect housing starts will slow below a 200k pace this year, though yesterday's reported pickup in permit issuance in December indicates homebuilding could remain above that pace in the first quarter. That said, we do expect some payback in terms of residential investment following what looked like a strong Q4/17. Activity late last year was bolstered not only by solid housing starts but also by a surge in resales as homebuyers rushed into the market ahead of a regulatory change that took effect in January.

Sterling Uplifted by Rate Hike Expectations

Sterling bulls hit Thursday trading with a renewed sense of confidence after the Bank of England signaled that interest rates could rise faster than previously anticipated.

Although the MPC left rates unchanged at 0.5% for now, the relatively positive evaluation of the economy, and the overall hawkish tone of the meeting, boosted expectations that we could see a rate hike as soon as May. With the MPC stating that monetary policy will "need to be tightened somewhat earlier and by some greater extent over the forecast period than anticipated", the Pound may remain buoyant short-term. While heightened speculations of higher UK interest rates could result in further upside for Sterling, gains may face headwinds down the road. The horrible combination of Brexit uncertainty and political drama at home could obstruct the central bank's efforts to raise rates. An unfavorable situation where the UK is unable to secure a Brexit transition deal by the March 22-23 EU summit, could trigger uncertainty – ultimately weighing on the prospect of higher UK interest rates.

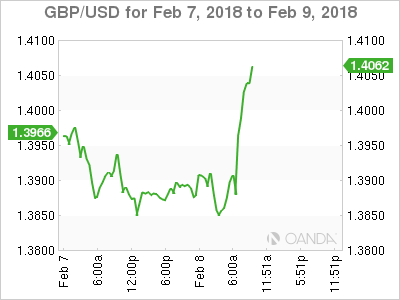

Taking a look at the technical picture, the GBPUSD staged an impressive rebound from the 1.3850 support level, with prices punching above 1.4000. A solid daily close above 1.4000 could encourage a further incline towards the next levels of interest at 1.4120 and 1.4230, respectively. Alternatively, a failure of prices to keep above the 1.4000 level may invite a decline back towards 1.3850.

Pound Jumps on ‘Hawkish’ BoE

Thursday February 8: Five things the markets are talking about

The global equity markets remain unnerved as U.S bond yields again trade atop of their four-year highs after U.S congressional leaders reached a two-year budget deal to raise government spending by almost +$300B.

The bi-partisan deal is expected to stave off a government shutdown, while at the same time widen the U.S federal deficit even further – bond dealers suggest that it could lead to a faster tightening cycle on inflation worries.

Note: The Senate and the House are both expected to vote on the proposed deal today, amid some opposition on both sides of the aisle.

1. Stocks mixed results

In Japan, the Nikkei share average rallied overnight, driven higher by bargain hunters. The Nikkei ended up +1.1%, but has still lost nearly -6%on the week. The broader Topix rose +0.9%.

Down-under, shrugging off early weakness on falling commodities stocks, the Aussie benchmark finished modestly higher, up for a second consecutive day, the S&P/ASX 200 rose +0.2%.

In Hong Kong, stock prices steadied after a five-day losing streak. At close of trade, the Hang Seng index was up +0.42%, while the Hang Seng China Enterprises index fell -0.43%.

In China, stocks ended lower to post a third consecutive session of losses overnight, with the benchmark Shanghai index hitting a six-month low, despite trade data showing the country's performance exceeded expectations. At the close, the Shanghai Composite index was down -1.42%, while the blue-chip CSI300 index was down -0.96%.

Note: China trade balance (USD): +$20.3b vs. +$54.7be; Exports y/y: +11.1% vs. +10.7%e, Imports y/y: +36.9% (fastest growth since Feb 2017) vs. +10.6%e. The yuan dropped the most in two-years amid speculation that policy makers will step up efforts to rein it in after trade figures missed estimates.

In Europe, regional indices are trading lower across the board, mirroring the decline in Wall Street yesterday.

U.S stocks are set to open in the black (-0.2%).

Indices: Stoxx600 -0.5% at 378.3, FTSE -0.6% at 7236, DAX -1.0% at 12466, CAC-40 -0.6% at 5226, IBEX-35 -0.8% at 9901, FTSE MIB -0.6% at 22840, SMI -0.2% at 8958, S&P 500 Futures -0.2%

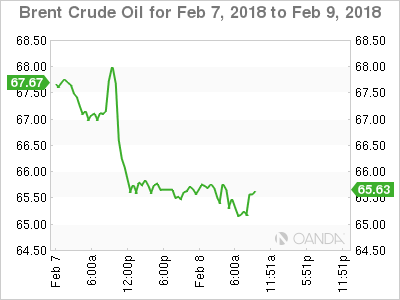

2. Oil slides as U.S output soars, gold lower

Oil prices have hit new six-week lows overnight after data showed U.S crude output had reached record highs and the North Sea's largest crude pipeline reopened following an outage.

Brent crude futures are down -14c at +$65.37 a barrel, while West Texas Intermediate (WTI) is down -15c at +$61.64 a barrel.

Note: Brent futures have lost around -8% from their four-year January high print of +$71. Futures positions suggest that investors are sitting on the largest 'bullish position in history.

The U.S. Energy Information Administration (EIA) this week upped its 2018 average output forecast to +10.59m bpd, up +320k bpd from its last forecast 10-days ago.

The output is now higher than the previous bpd record from 1970 and above that of top exporter Saudi Arabia.

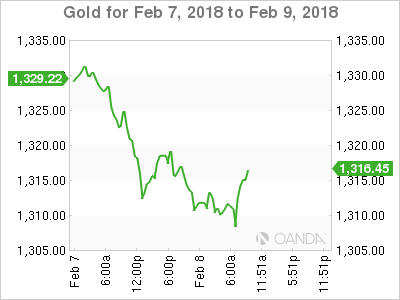

Ahead of the U.S open, gold prices have extended their drop and printed a fresh four-week low, on a firmer dollar and market expectations of more U.S rate hikes this year. Spot gold is down -0.4% at +$1,312.41 per ounce.

3. BoE to tighten sooner rather than later

The Bank of England (BoE), as expected, kept rates steady this morning, but indicated it is likely to 'tighten' monetary policy "faster and further" than it had anticipated three months ago.

In the BoE's view, investors had expected one quarter-point rise in 2018 and subsequent years. But at that rate, inflation would still be slightly above target in early 2021, so a slightly more aggressive series of moves is needed.

The BoE vote was unanimous to keep rates at +0.5%. Gilt yields have jumped, with 5-year backing up to +1.066% from +1% before the decision.

Yesterday, the Reserve Bank of New Zealand (RBNZ) again held overnight rates at a record low and projected they will stay there until mid-2019 as inflation remains subdued amid slower economic growth.

"Monetary policy will remain accommodative for a considerable period" according to acting Governor Grant Spencer.

4. Pound jumps on 'Hawkish' BoE

Sterling (£1.4035) has rallied aggressively across the board after the BoE brought forward its rate hike expectations – the pound was trading atop £1.3885 before the announcement and EUR/GBP has fallen -0.87% to a new one week low of €0.8750 from €0.8812 beforehand.

USD has consolidated its recent gains after its best daily performance in four months yesterday. The greenback caught a bid after the White House and Senate leaders stated that deal had been reached on a two-year budget that included large increases to both defense and non-defense spending.

Elsewhere, the EUR/USD (€1.2259) remains within striking distance of its two-week low outright as the pair tested €1.2235 in the overnight session. A plethora of ECB speakers have provided little new clues on the outlook for the Eurozone. From the techies, the key support for the pair remains at the psychological €1.21 level.

USD/JPY (¥109.67) is edging back to the upper end of its recent range with the 110 level back in play.

5. German goods exports soar to new records

Data from the German Statistical Office (Destatis) showed that exports of German goods hit a new high last year, amid strong global demand for premium engineering goods.

Exports of goods surged +6.3% to almost €1.3T last year to mark a new record.

Digging deeper, Germany's plant and machinery makers remain upbeat, with strong demand from China and the U.S. contributing to a +4% rise.

Sterling Jumps as BoE Hints at Earlier and Faster Rate Hikes

Quick update: US initial jobless claims dropped -9k to 221k in the week ended Feb 3. Four week averaged dropped by -10k to 224.5k, lowest since March 1973. Continuing claims dropped -33k to 1.92m.

Sterling jumps after BoE stands pat and indicates that it may raise interest rates earlier than expected. In the accompanying statement, the central bank noted "were the economy to evolve broadly in line with the February Inflation Report projections, monetary policy would need to be tightened somewhat earlier and by a somewhat greater extent over the forecast period than anticipated at the time of the November Report, in order to return inflation sustainably to the target." That is seen as the main trigger for the buying in the Pound. Other than that, there are many surprises. The votes on keeping the Bank rate at 0.50% and asset purchase at GBP 435b were unanimous. 2018 GDP forecast was raised to 1.8%, up from 1.6%. 2019 GDP forecast was raised to 1.8%, up from 1.7%.

ECB: Broad economic expansion to continue

ECB monthly bulletin noted that the broad based expansion in Eurozone is likely to continue. The report noted that "the ongoing broad and solid economic expansion is expected to continue beyond the near term" And, "the prevailing strong cyclical momentum could lead to further positive growth surprises in the near term." Also, "downside risks continue to relate primarily to global factors, including developments in foreign exchange markets."

ECB Chief Economist Peter Praet reiterated the three criteria for ending the asset purchase program. And, "if the flow of incoming data were to confirm the expectation of a gradual build-up of inflationary pressures, this would not necessarily be sufficient to affirm a sustained adjustment, as less supportive monetary policy conditions could imperil the inflation trajectory." The three criteria are inflation on track to 2% target, there is confidence that inflation would be met on a sustainable basis, and inflation outlook is not overly dependent on monetary support.

BoJ Kuroda: We need to stick with powerful monetary easing

BoJ Governor Haruhiko Kuroda told the parliament today that "we haven't reached the point where we should talk about the timing of an exit or exit strategies" And, "we need to stick with our powerful quantitative easing." BoJ board member Hitoshi Suzuki said that "the BOJ will patiently continue its powerful monetary easing now." And "if it becomes clear that more time would be needed (to achieve the BOJ's price target), there's a chance of modifying our policy framework to make it more sustainable and allow us to continue monetary easing for a longer period of time."

RBA Lowe: No strong case for near term hike

RBA Governor Philip Lowe said that the board "does not see a strong case for a near-term adjustment in monetary policy." He pointed out that "we are still some way from what could be considered full employment and our central scenario for inflation is for it to remain below the midpoint of the medium-target range for the next couple of years." Also, Lowe noted RBA didn't lower interest rate to that "extraordinarily low levels seen elsewhere after the financial crisis." And, "Just as we did not move in lock-step on the way down, we do not need to do so in the other direction."

RBNZ stands pat, lowered inflation forecasts

As widely anticipated, RBNZ left the OCR unchanged at 1.75%. Owing to the downside surprise in 4Q17 inflation, policymakers revised lower their inflation forecast, mainly driven by tradeable inflation. Meanwhile, the central bank now sees currency appreciation a less concern, as NDZUSD has retreated to a one-month low, and indicates that the positive impacts of fiscal stimulus (including KiwiBuild and the increase in minimum wages) have diminished. The overall monetary stance remains neutral with the first hike unlikely coming before the 2Q19. More in RBNZ Downgraded Inflation Forecasts, First Rate Hike Unlikely Until 2019.

Separately, RBNZ Assistant Governor John McDermott said in a Reuters interview that "Core inflation is sitting a little bit below the midpoint... it still needs a little shove to get it towards the midpoint. That strategy hasn't changed." He reiterated RBNZ's "neutral stance". And he added that "there is a significant probability that the next rate move could be an increase sometime in the future, and there's also a substantial probability that the next move could actually be a cut."

On the data front

German trade surplus narrowed to EUR 21.4b in December. UK RICS house price balance was unchanged at 8 in January. Japan current account surplus narrowed to JPY 1.48T in December. China trade surplus narrowed sharply to CNY 136b, or USD 20.3b in January. Australia NAB business confidence dropped to 6 in Q4.

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8812; (P) 0.8855; (R1) 0.8876; More...

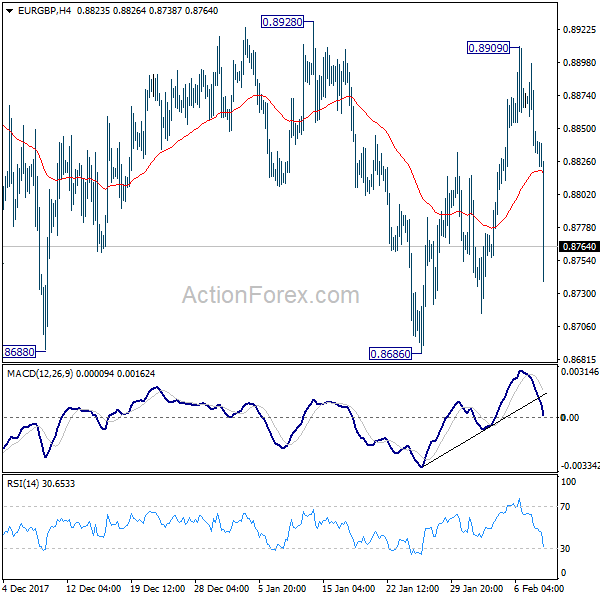

EUR/GBP drops sharply on hawkish BoE, but it's still bounded in range of 0.8686/8928. Intraday bias remains neutral for the moment. And, near term outlook will remain mildly bearish as long as 0.8928 resistance holds. On the downside, firm break of 0.8686 will resume whole decline from 0.9305. As 61.8% retracement of 0.8312 to 0.9305 should then be taken out too. Deeper decline would be seen to retest 0.8303/8312 support zone. Nonetheless, on the upside, break of 0.8928 will indicate near term reversal and turn outlook bullish for 0.9304 resistance.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 20:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% | 1.75% | |

| 23:50 | JPY | Current Account (JPY) Dec | 1.48T | 1.66T | 1.70T | |

| 0:01 | GBP | RICS House Price Balance Jan | 8.00% | 5.00% | 8.00% | |

| 0:30 | AUD | NAB Business Confidence Q4 | 6 | 7 | 8 | |

| 2:00 | CNY | Trade Balance (CNY) Jan | 136B | 325B | 362B | |

| 3:45 | CNY | Trade Balance (USD) Jan | 20.3B | 54.9B | 54.7B | |

| 5:00 | JPY | Eco Watchers Survey Current Jan | 49.9 | 53.6 | 53.9 | |

| 7:00 | EUR | German Trade Balance Dec | 21.4b | 21.0b | 23.7b | |

| 9:00 | EUR | ECB Economic Bulletin | ||||

| 12:00 | GBP | BoE Rate Decision | 0.50% | 0.50% | 0.50% | |

| 12:00 | GBP | BoE Asset Purchase Target Feb | 435B | 435B | 435B | |

| 12:00 | GBP | MPC Official Bank Rate Votes | 0--0--9 | 0--0--9 | 0--0--9 | |

| 12:00 | GBP | MPC Asset Purchase Facility Votes | 0--0--9 | 0--0--9 | 0--0--9 | |

| 12:00 | GBP | BoE Inflation Report | ||||

| 13:15 | CAD | Housing Starts Jan | 216K | 211K | 218K | |

| 13:30 | CAD | New Housing Price Index M/M Dec | 0.00% | 0.20% | 0.10% | |

| 13:30 | USD | Initial Jobless Claims (3 FEB) | 221K | 236K | 230K | |

| 15:30 | USD | Natural Gas Storage | -99B |

Pound Spikes above 1.40 vs Dollar in Expected Reaction to BoE’s Hawkish Hold

Sterling cracked 1.40 barrier and spiked to three-day high at 1.4014 after BoE maintained hawkish hold on its monetary policy meeting today. The UK's central bank kept interest rates as expected at 0.5%, with policymakers voting 9-0 to keep rate at 0.5%, but kept hawkish tone in its report, saying that the policy will be tightened (the earliest in May and latest in November) if economy grows as expected and to set monetary policy that inflation returns to target. Hawkish hold from BoE was boost for those advocating rate hike in May. Pound moved in rather expected reaction to such scenario, but needs to close above 1.40 barrier to generate signal for further recovery. Fresh strength improves near-term sentiment and reduces immediate downside risk for extension of steep three-day 1.4277/1.3835 fall. Fresh near-term bulls need to hold above 1.39 handle (daily Kijun-sen) which is seen as minimum requirement to keep immediate focus at the upside. Firm break above 1.40 barrier (Fibo 38.2% of 1.4277/1.3835 downleg) is needed to maintain fresh bullish bias for recovery extension towards 1.4056 (daily Tenkan-sen) and 1.4109 (Fibo 61.8% of 1.4277/1.3835). Bearish scenario expects return below 1.3900 to increase downside risk for retest of key support at 1.3841 (Fibo 38.2% of 1.3026/1.4344, Oct-Jan rally, reinforced by rising 30SMA), loss of which will be strong bearish signal.

Res: 1.4000; 1.4056; 1.4109; 1.4150

Sup: 1.3940; 1.3900; 1.3841; 1.3796

Canadian Dollar Under Pressure, Housing Starts Next

The Canadian dollar has posted small losses in the Wednesday session. Currently, the pair is trading at 1.2590, up 0.17% on the day. Canada will release Housing Starts, while the US publishes unemployment claims. On Friday, Canada releases key employment data – Employment Change and the unemployment rate.

The US dollar has posted broad gains this week, boosted by strong volatility in the stock markets. On Monday, the Dow Jones posted its biggest one-day loss, and US markets have pointed downwards for much of the week. The catalyst for the stock market slide is concern that inflation could rise in the US, which in turn would trigger additional rate hikes from the Fed. This would make the US dollar more attractive against other currencies. With investor risk appetite sharply lower, the Canadian dollar is under strong pressure. Earlier in the day, USD/CAD touched a high of 1.2598, its highest level since late December.

Canadian indicators disappointed on Tuesday. Canada's trade deficit widened from C$2.5 billion to C$3.2 billion, well above the estimate of C$2.3 billion. The export sector has been steady, but uncertainty over NAFTA is a dark cloud over the economy, and exports could suffer if the trilateral free trade pact is not renewed. The US has threatened to leave the pact if the Canada and Mexico do not agree to major concessions, such as increasing the percentage of US content in auto parts produced under NAFTA. Elsewhere, Canadian Ivey PMI continues to point to expansion, but slowed to 55.2, down from 60.4 in the previous release. This was well off the forecast of 60.7 points.

EURUSD Under Selling Pressure Below 1.2245

The euro has continued to drift lower against greenback during the European trading session, as the U.S dollar index extends its rally to the upside. Price-action on the EURUSD pair currently trades around the 1.2230 level, after breaking below the former weekly-low around the 1.2245 mark. Moving into the U.S trading session we see the release of weekly jobs data from the United States economy, and a scheduled speech from FOMC member Neel Kashkari.

The EURUSD pair is strongly bearish while trading below the 1.2245 level, downside support is now found at 1.2200 and 1.2265.

If the EURUSD pair can move above the 1.2245 level, we may see price-action correct back towards the 1.2275 and 1.2313 levels.

Sterling Testing 1.4000 after BoE Meeting

The British pound has spiked towards the 1.4000 level against the U.S dollar, following bullish comments on upcoming rates hikes inside the Bank of England's Monetary Policy Statement. The GBPUSD pair spiked over one-hundred and thirty pips higher, after BOE policy makers said they may need to raise UK interest rates sooner than expected in 2018. Going forward, the 1.4000 level remains pivotal for further upside gains for the pair, whilst the 1.3938 level is now acting as former resistance turned major support.

The GBPUSD pair is likely to see further buying interest above the 1.4000 level, upside targets remain 1.4058 and 1.4100.

Should price-action on the GBPUSD pair start to move below the 1.3938 level, we may see a correction back towards the 1.3900 and 1.3870 levels.