Sample Category Title

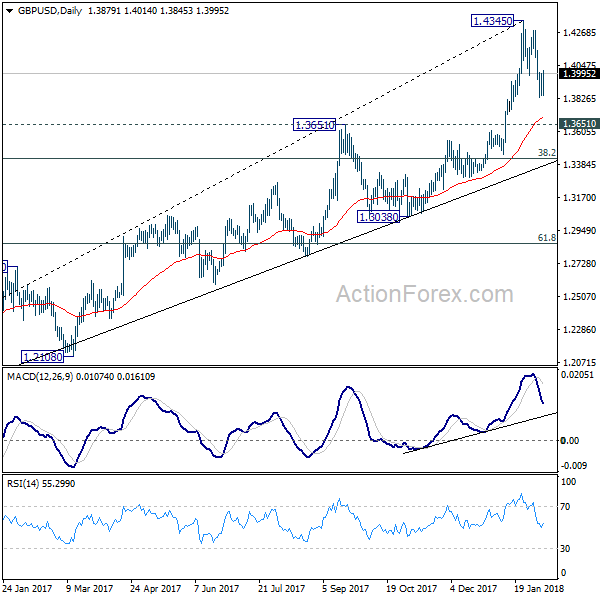

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3820; (P) 1.3907; (R1) 1.3967; More.....

GBP/USD recovers strongly on hawkish BoE. Break of 1.3999 minor resistance indicates temporary bottoming at 1.3835. Intraday bias is turned neutral first. At this point, it's still unsure whether decline from 1.4345 is correcting rise from 1.3038, or that from 1.1946, or it's reversing the trend. Below 1.3835 will target 1.3651 resistance turned support first. On the upside, break of 1.4345 is needed to confirm rally resumption. Otherwise, we'd expect more corrective trading with risk of at least another decline.

In the bigger picture, sustained break of 1.3835 key resistance level indicates that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. Further rise should now be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Medium term outlook will stay bullish 38.2% retracement of 1.1946 to 1.4345 at 1.3429, in case of deep pull back.

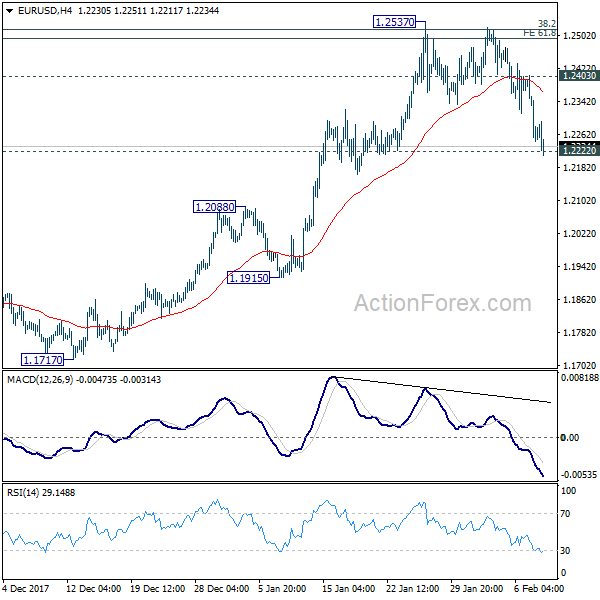

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2204; (P) 1.2305 (R1) 1.2364; More....

EUR/USD's decline continues today and the breaching of 1.2222 support now raise the chance of rejection from 1.2494/2516 key fibonacci level. Sustained trading below 1.2222 should at least confirm near term reversal on , on bearish divergence condition in 4 hour MACD. That could also signal completion of medium term up trend from 1.0339. In that case, near term outlook will be turned bearish for 1.2091 resistance turned support first. On the upside, though, above 1.2403 minor resistance will revive bullishness and turn focus back to 1.2537.

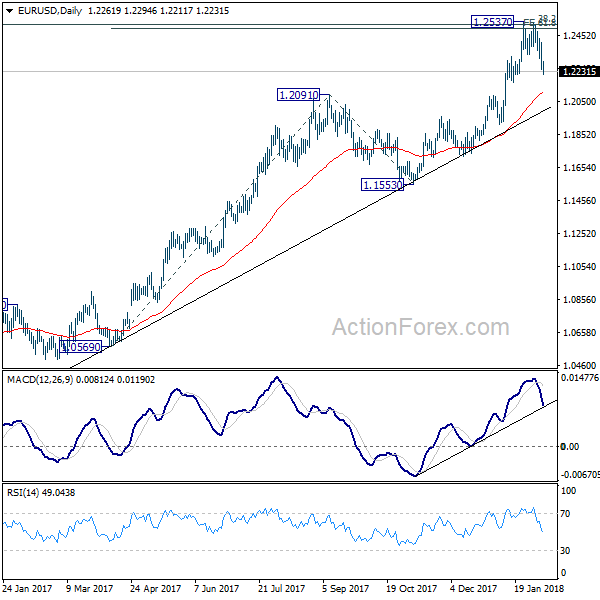

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. But key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 is looking vulnerable. Sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862. Nonetheless, rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive.

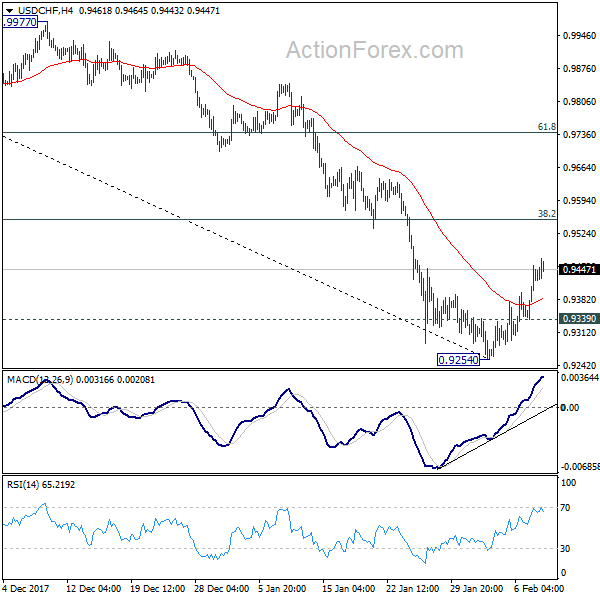

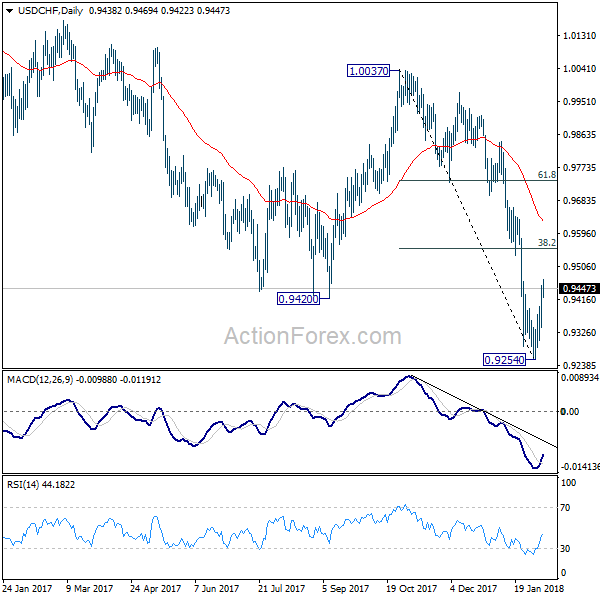

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9362; (P) 0.9408; (R1) 0.9477; More...

Intraday bias in USD/CHF remains on the upside for 38.2% retracement of 1.0037 to 0.9254 at 0.9553 first. At this point, there is no clear sign of trend reversal yet. We'd be cautious on strong resistance from 0.9553 to limit upside and bring decline resumption. On the downside, below 0.9339 minor support will turn bias to the downside for 0.9254. Nonetheless, firm break of 0.9553 will bring stronger rebound to 55 day EMA (now at 0.9627).

In the bigger picture, the strong break of 0.9420 support suggests that fall from 1.0342 is developing into a medium term down trend. Deeper fall should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, break of 0.9640 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish even in case of strong rebound.

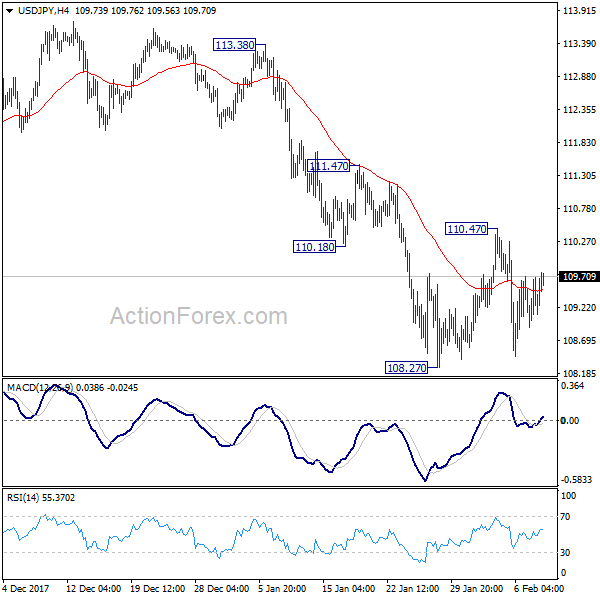

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.92; (P) 109.32; (R1) 109.72; More...

Intraday bias in USD/JPY stays neutral for the moment. As noted before, larger decline from 114.73 is possibly still in progress. Break of 108.27 will also resume the medium term correction from 118.65. That will send USD/JPY through 107.31 to 106.48 fibonacci level. Nonetheless, above 110.47 will turn intraday bias back to the upside and bring stronger rebound.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD/JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

CAC Spiral Continues as Market Turbulence Continues

The CAC index has posted considerable losses in the Thursday session. Currently, the index is at 5205.00, down 0.97% on the day. On the release front, there are no data releases on the schedule. On Friday, France releases Industrial Production, which is expected to post a small gain of 0.1%.

It's been a tumultuous week for global stock markets, and the CAC has dropped 2.3% percent this week. February has been dismal for European assets, and the CAC has shed 5.5% this month. US markets have set the tone, with the Dow Jones posting its biggest one-day loss on Monday. The catalyst for the current turbulence is investor concern that inflation could rise in the US, which in turn would trigger additional rate hikes from the Federal Reserve. This would make dollar-denominated assets more attractive than European assets. US stock markets posted losses on Wednesday, and the downward trend has continued in the European stock markets on Thursday.

As the largest member of the Eurozone, what happens in Germany often has a significant impact on the rest of the eurozone. There is an audible sigh of relief in France and elsewhere, as Germany appears on the verge of forming a new government, after months of negotiations. On Wednesday, the socialist SDP and Angela Merkel's conservatives announced that they had finalized a coalition agreement. In the last government, the SDP was the junior partner of the conservatives, but this time around the SDP has extracted major concessions from Merkel, notably control of the powerful finance ministry. This will likely mark a shift in Germany's eurozone policy, which had been marked by a conservative stance under former finance minister Wolfgang Schaeuble. The weaker members of the eurozone, such as Greece, will likely find a more sympathetic ear for financial help from the SDP than they did from Schauble. The coalition agreement still requires the consent of a majority of the 464,000 members of the SDP, but is expected to pass this final hurdle.

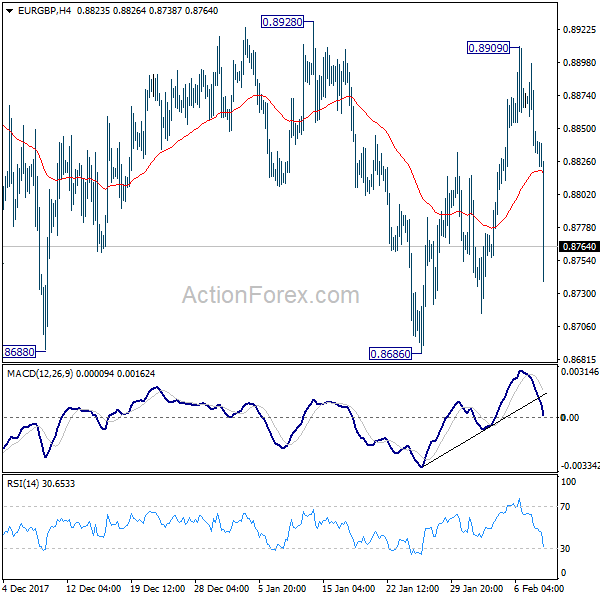

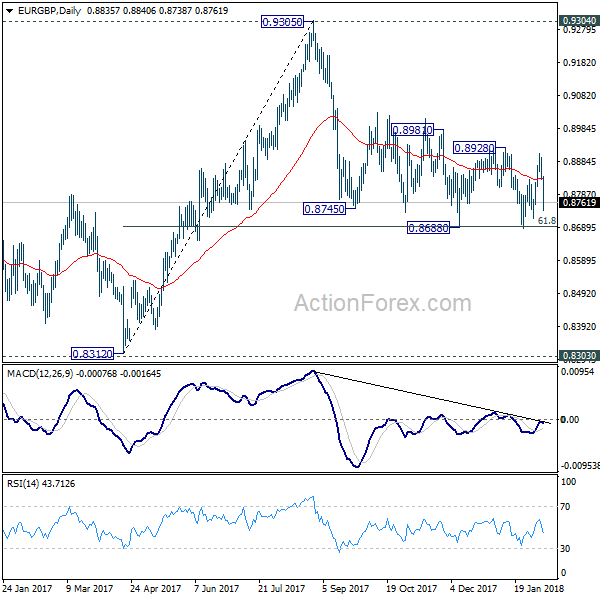

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8812; (P) 0.8855; (R1) 0.8876; More...

EUR/GBP drops sharply on hawkish BoE, but it's still bounded in range of 0.8686/8928. Intraday bias remains neutral for the moment. And, near term outlook will remain mildly bearish as long as 0.8928 resistance holds. On the downside, firm break of 0.8686 will resume whole decline from 0.9305. As 61.8% retracement of 0.8312 to 0.9305 should then be taken out too. Deeper decline would be seen to retest 0.8303/8312 support zone. Nonetheless, on the upside, break of 0.8928 will indicate near term reversal and turn outlook bullish for 0.9304 resistance.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

(BOE) Bank Rate Maintained at 0.50%

Our Monetary Policy Committee has voted unanimously to maintain Bank Rate at 0.50%. The committee also voted unanimously to maintain the stock of corporate bond purchases and UK government bond purchases.

The Bank of England's Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 7 February 2018, the MPC voted unanimously to maintain Bank Rate at 0.5%. The Committee voted unanimously to maintain the stock of sterling non-financial investment-grade corporate bond purchases, financed by the issuance of central bank reserves, at £10 billion. The Committee also voted unanimously to maintain the stock of UK government bond purchases, financed by the issuance of central bank reserves, at £435 billion.

The MPC's latest projections for output and inflation are set out in detail in the accompanying February Inflation Report. The global economy is growing at its fastest pace in seven years. The expansion is becoming increasingly broad-based and investment driven. Notwithstanding recent volatility in financial markets, global financial conditions remain supportive. UK net trade is benefiting from robust global demand and the past depreciation of sterling. Along with high rates of profitability, the low cost of capital and limited spare capacity, strong global activity is supporting business investment, although it remains restrained by Brexit-related uncertainties. Household consumption growth is expected to remain relatively subdued, reflecting weak real income growth. GDP growth is expected to average around 1¾% over the forecast, a slightly faster pace than was projected in November despite the updated projections being conditioned on the higher market-implied path for interest rates and stronger exchange rate prevailing in financial markets at the time of the forecast.

While modest by historical standards, that rate of growth is still expected to exceed the diminished rate of supply growth. Following its annual assessment of the supply side of the economy, the MPC judges that the UK economy has only a very limited degree of slack and that its supply capacity will grow only modestly over the forecast, averaging around 1½% per year. This reflects lower growth in labour supply and rates of productivity growth that are around half of their pre-crisis average. As growth in demand outpaces that of supply, a small margin of excess demand emerges by early 2020 and builds thereafter.

CPI inflation fell from 3.1% in November to 3.0% in December. Inflation is expected to remain around 3% in the short term, reflecting recent higher oil prices. More generally, sustained above-target inflation remains almost entirely due to the effects of higher import prices following sterling's past depreciation. These external forces slowly dissipate over the forecast, while domestic inflationary pressures are expected to rise. The firming of shorter-term measures of wage growth in recent quarters, and a range of survey indicators that suggests pay growth will rise further in response to the tightening labour market, give increasing confidence that growth in wages and unit labour costs will pick up to target-consistent rates. On balance, CPI inflation is projected to fall back gradually over the forecast but remain above the 2% target in the second and third years of the MPC's central projection.

As in previous Reports, the MPC's projections are conditioned on the average of a range of possible outcomes for the United Kingdom's eventual trading relationship with the European Union. The projections also assume that, in the interim, households and companies base their decisions on the expectation of a smooth adjustment to that new trading relationship. Developments regarding the United Kingdom's withdrawal from the European Union – and in particular the reaction of households, businesses and asset prices to them – remain the most significant influence on, and source of uncertainty about, the economic outlook. In such exceptional circumstances, the MPC's remit specifies that the Committee must balance any trade-off between the speed at which it intends to return inflation sustainably to the target and the support that monetary policy provides to jobs and activity.

Over the past year, a steady absorption of slack has reduced the degree to which it was appropriate for the MPC to accommodate an extended period of inflation above the target. Consequently, at its November 2017 meeting, the Committee tightened modestly the stance of monetary policy in order to return inflation sustainably to the target.

Since November, the prospect of a greater degree of excess demand over the forecast period and the expectation that inflation would remain above the target have further diminished the trade-off that the MPC is required to balance. It is therefore appropriate to set monetary policy so that inflation returns sustainably to its target at a more conventional horizon. The Committee judges that, were the economy to evolve broadly in line with the February Inflation Report projections, monetary policy would need to be tightened somewhat earlier and by a somewhat greater extent over the forecast period than anticipated at the time of the November Report, in order to return inflation sustainably to the target.

In light of these considerations, all members thought that the current policy stance remained appropriate to balance the demands of the MPC's remit. Any future increases in Bank Rate are expected to be at a gradual pace and to a limited extent. The Committee will monitor closely the incoming evidence on the evolving economic outlook, and stands ready to respond to developments as they unfold to ensure a sustainable return of inflation to the 2% target.

Technical Outlook: WTI Oil At Five-Week Low, Pressured By Rising US Output, Weekly Inventories Build

WTI oil is holding near new five-week low at $61.21 and remains under strong pressure on Thursday, following sharp fall on Wednesday. Oil price came under increased pressure after data showed US oil production rose above 10 million barrels per day last week and hit all-time high at 10.25 million barrels per day. In addition, EIA report showed US weekly crude stocks rose by 1.9 million barrels, which was well below forecasted build of 3.18 million barrels but weighed on oil price. Fresh weakness cracked 50% of $55.81/$66.64 rally ($61.23), eyeing rising 55SMA ($60.87) and psychological $60 support. Daily techs are turning to full bearish setup and favor further downside, accompanied by strong bearish sentiment which threatens to further dent OPEC-led action to tighten oil markets by reducing global output. Broken pivotal support at $62.50 (Fibo 38.2% of $55.81/$66.64) and former low at $62.83 (19 Jan) mark solid barriers which should ideally cap corrective upticks.

Res: 61.76, 62.50, 62.83, 63.46

Sup: 61.21, 60.87, 60.00, 59.45

Calm Returns To Markets Ahead Of BoE Event

- US Futures Flat After Uneventful Session in Europe;

- Will Carney Adopt Cautious Approach Given Market Volatility?

- Crypto Rebound May Be Short-Lived.

US Futures Flat After Uneventful Session in Europe

A sense of calm appears to be gradually returning to financial markets as we near the end of the week, with indices in Europe trading a little lower and US futures flat after ending Wednesday’s session in a similar manner.

While volatility in the markets has eased over the last couple of days, it has remained at very high levels which is probably a sign of the ongoing nervousness among investors which may leave markets vulnerable to further declines. Still, the European session has so far been relatively uneventful compared to the last few days which may be a positive sign ahead of the open in the US.

The sell-off on Monday was widely attributed to rising yields on the back of higher interest rate expectations in the US and Europe, although it was likely exacerbated by a combination of other factors, such as automated trading and fear of a broader correction given how long it had been since the last. It’s interesting then that while yields fell after the stock market sell-off, they have been creeping higher again and now find themselves not far from the levels they were at on Monday. Should we avoid another plunge in stocks, it would suggest that yields may have been the catalyst but ultimately, the selling that followed was driven by other factors, perhaps including a belief that a correction was overdue.

Will Carney Adopt Cautious Approach Given Market Volatility?

It will be very interesting to see what approach the Bank of England takes when it holds its quarterly press conference later on, given the recent market volatility. Central banks typically approach these events with incredible caution due to the ability of a seemingly harmless comment to cause excessive swings as traders pick apart everything that’s said.

Governor Mark Carney may have to be extra careful today then, particularly if the BoE is planning to lay the foundation for a rate hike this year, with an increasing number of people suggesting one will come in May. I remain unconvinced by this given the amount of economic uncertainty, soft economic data and the fact that inflation is believed to have peaked. Should the new forecasts contain an upgrade to the inflation outlook then perhaps this will nudge policy makers towards raising interest rates again.

With no change in interest rates expected, traders will be paying very close attention to the new forecasts, as well as the press conference with Carney and his colleagues. If the BoE is considering a hike in May, you would expect it to start laying the groundwork for it today and at the meeting in March, which could provide additional upside pressure in UK debt and sterling, which is already trading at pre-referendum levels against the dollar.

Crypto Rebound May Be Short-Lived

The rebound in bitcoin is continuing today, with the cryptocurrency now up more than 40% from the lows posted two days ago. In any other asset other than cryptocurrencies, this kind of move would be staggering but instead this is just another day for bitcoin. It is also only a small rebound compared to the declines it’s seen over the last couple of months and may prove to be yet another dead cat bounce, albeit one that exceeds 40%.

I’m not convinced yet that any rebound will be sustained as we continue to see a steady stream of negative news flow which has severely damaged sentiment in cryptocurrencies. The rally towards the end of last year was driven by the buzz and positive sentiment towards bitcoin and its peers – as well as a large speculative push from FOMO traders – and the reversal of this has equally weighed heavily on it. If that continues, I see no reason why it won’t be back below $6,000 in the not too distant future.

Market Update – European Session: BOE In Focus For Hints Of Potential Rate Rise During The First Half Of...

Notes/Observations

BOE in focus for hints of potential rate rise during the first half of this year

Asia:

New Zealand Central Bank (RBNZ) left Official Cash Rate (OCR) unchanged at 1.75%; maintained policy path outlook noting that monetary policy to stay accommodative for a considerable period of time

China Jan Trade Balance: $20.3B v $$54.7Be, Exports Y/Y: 11.1% v 10.7%e, Imports Y/Y: 36.9% v 10.6%e

China said to have resumed an outbound investment scheme, under the Qualified Domestic Limited Partnership (QDLP) plan after a 2-yearr break, granting licenses to ~12 global money managers

BoJ Suzuki reiterated stance that was important to 'patiently' maintain 'powerful' monetary easing; did not rule out a chance of 'tweak' under powerful easing

Europe:

ECB's Nowotny (Austria): US Treasury was deliberately putting pressure on the dollar and wanted to keep it low

UK Govt economic analysis: a no-deal Brexit would cost £80B in public finances, with the leave-voting heartlands of north-east England and West Midlands worst affected

Germany's SPD leader Schulz to step down as party leader; says party leader should not be part of the govt cabinet (Schulz will become Foreign Minister under the coalition deal)

Italy Northern League (part of centre-right coalition): Want to remain in euro only if we can renegotiate all treaties which limit our full legitimate sovereignty

Investor George Soros said to be backing a campaign to overturn Brexit

Americas:

White House aide: we have come to agreement on 2-year budget deal (agreement includes $300B boosts to defense and non-defense spending)

Sen Maj Leader McConnell (R-KY) "I am pleased to announce that our bipartisan, bicameral negotiations on defense spending and other priorities have yielded a significant agreement." Deal will unwind sequestration

Fed's Williams (moderate, voter): Fed on very gradual tightening path; saw US expansion across full range of sectors; did not view the economy as a bubble or headed to overdrive. Had no strong view between 3 or 4 Fed hikes in 2018

Fed’s Evans (non-voter, dove): Current strategy was to keep rates on hold until at least midyear but under an alternate scenario where inflation picked up more assuredly, would support 3 or even 4 rate hikes in 2018

Brazil Central Bank (BCB) cut Selic Rate by 25bps to 6.75%; hint of pause in current policy outlook

Mexico Official: To make proposal for regional content requirements for autos at the NAFTA talks in Feb

Economic Data:

(NL) Netherlands Jan CPI M/M: -0.1% v 0.0% prior; Y/Y: 1.5 v 1.3% prior

(NL) Netherlands Jan CPI EU Harmonized M/M: -0.4% v -0.1% prior; Y/Y: 1.5% v 1.0%e

(DE) Germany Dec Current Account Balance: €27.8B v €28.0Be; Trade Balance: €18.2B v €21.0Be, Exports M/M: +0.3% v -1.0%e, Imports M/M: +1.4% v -0.7%e

(DK) Denmark Dec Current Account Balance (DKK): 13.8B v 11.1B prior; Trade Balance: 6.4B v 6.6B prior

(TR) Turkey Dec Industrial Production M/M: 0.9% v 0.5%e; Y/Y: 8.7% v 6.8%e

(FR) Bank of France Jan Business (Industrial) Sentiment: 105 v 110e

(CZ) Czech Jan Unemployment Rate: 3.9% v 3.9%e

(ES) Spain Dec Industrial Output NSA Y/Y: 2.9% v 4.9% prior; Industrial Output SA Y/Y: 6.1% v 4.0%e

(PH) Philippines Central Bank (BSP) left its Overnight Borrowing Rate unchanged at 3.00%; as expected

(SE) Sweden Jan Average House Prices (SEK): 3.195M v 3.074M prior

(ZA) South Africa Dec Total Mining Production M/M: -3.1% v 0.0%e; Y/Y: 0.1% v 6.3%e

Fixed Income Issuance:

(GR) Greece Debt Agency (PDMA) opened its book to sell EUR-denominated 7-year note; yield guidance seen around 3.75% area

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.5% at 378.3, FTSE -0.6% at 7236, DAX -1.0% at 12466, CAC-40 -0.6% at 5226 , IBEX-35 -0.8% at 9901, FTSE MIB -0.6% at 22840 , SMI -0.2% at 8958, S&P 500 Futures -0.2%]

Market Focal Points/Key Themes: Indices trades lower across Europe after a strong rally yesterday, with the decline in Wallstreet overnight weighing on Indices. A heavy day of earnings throughout Europe with Banking names SocGen, Unicredit, Commerzbank, Zurich Insurance all trading higher following results, with Swiss Re pushing higher on talks of Softbank acquiring a majority stake. Else where Heidelberger Druck, Total, Pernod Ricard, Compass rise following earnings, while ABB, Thomas Cook, Tate are some of the names trading lower. In the M&A space Nordex trades over 15% higher after receiving a SEK60/shr mandatory offer valued at SEK6.7B. Looking ahead notable earners include Cardinal Health, Twitter, Tyson Foods and T-Mobile.

Movers

Consumer Discretionary [ Publicis [PUB.FR] +5.6% (Earnings), Pernod Ricard [RI.FR] +2.3% (Earnings), Thomas Cook [TCG.UK] -4.4% (Earnings)]

Industrials [ABB [ABBN.CH] -3.3% (Earnings), Heidelberger Druck [HDD.DE] +7.7% (Earnings)]

Financial [ SocGen [GLE.FR] +3.9% (Earnings), Zurich Insurance [ZURN.CH] +2.7% (Earnings), Unicredit [UCG.IT] +1.3% (Earnings), Commerbank [CBK.DE] +1.9% (Earnings), Swiss Re [SREN.CH] +4% (Reportedly Softbank to take stake), Nordex [NDX.SE] +15% (Takeover offer)]

Materials [Akzo Nobel [AKZA.NL] +3.0% (Prelim earnings),

Energy [ Total [FR.FR] +1.8% (Earnings)]

Speakers

ECB Economic Bulletin reiterated the robust regional recovery likely to continue; recent FX fluctuations was a source of concern. Wage growth could still be weighed down due to low inflation and weak productivity

ECB’s Weidmann (Germany) reiterated view that accommodative policy was still needed but saws no need for QE extension; should communicate without fear of market backlash. Policy should remain loose beyond QE. Recent IG Metall wage deal should support view of a gradual rise in inflation. Euro currency appreciation should not jeopardize expansion; not seeing growth abating anytime soon

ECB's Praet (Belgium, chief economist): Policy reaction would be in-line with forward guidance. Forward guidance on interest rates would naturally increase in importance. Basic assumption is for strong growth but have tools to counter any downturn

ECB Mersch (Luxembourg): Cryptocurrencies would be a concern if they drained liquidity

France Fin Min Le Maire: Interest rates are expected to rise in the Euro Zone as recovery proceeds. French budget was pricing in higher interest rates

France Budget Min Darmanin: EU Commission considers the French budget plans are on track

ECB again lowered its emergency liquidity assistance (ELA) cap for Greece banks from €22.0B to €19.8B

South Africa EEF Party: DA to ask for Zuma no confidence vote on Tuesday, Feb 13t

Philippines Central Bank Policy Statement saw upside risks in inflation and would tweak policy as needed. CPI expectations were well anchored but watchful of 2nd round effect. Inflation to moderate and settle with target in 2019. Domestic demand was firm with liquidity as adequate

RBA Gov Lowe: No case for near-term rate hike; would only rise with further progress on employment and inflation. Next move in interest rates was likely to be up with gradual normalization over time. Quarterly forecasts are largely unchanged with progress in reducing unemployment and lifting CPI to be gradual

Fed’s Kaplan (non-voter, dove): 3 rate hikes was still the base case for 2018. Expected stronger business spending in US and reiterated was expecting headline unemployment to dip below 4%

Currenciee

USD consolidating its recent gains with its best daily performance since Oct. The greenback caught a bid after the White House and Senate leaders stated that deal had been reached on a 2-year budget that included large increases to both defense and non-defense spending

EUR/USD was at 2-week lows as the pair tested 1.2235 during the session. Numerous ECB speak in the session provided any new clues on the outlook for the Euro Zone. The key support in the pair remains at the 1.21 level.

GBP/USD was lower by 0.2% at 1.3860 ahead of the BOE rate decision. The key focus would be on any hints of an earlier rate hike by the BOE. Currently the market saw a 50% change that the next hike could come as soon as May. Upbeat view in Quarterly Inflation Report would likely lift the prospect of 2018 rate hike coupled along with view that Brexit risks were receding - USD/JPY was edging back to the upper end of its recent range with the 110 level back in play.

AUD/USD was softer just above the 0.78 level after RBA Gov Lowe reiterated his stance that there was no case for near-term rate hike

Fixed Income

Bund Futures trades down 11 ticks at 157.91 as the bearish trend remains intact. Upside targets 159.85, while a continued move lower targets the 157.25 level.

Gilt futures trade at 121.52 down 2 ticks, with the medium-term technical outlook looking bleak ahead of the BOE meeting. Support continues to stand at 121.25 then 120.75, with upside resistance at 122.75 then 123.25.

Thursday’s liquidity report showed Wednesday’s excess liquidity rose to €1.895T from €1.888T prior. Use of the marginal lending facility fell to €50M from €51M prior.

Corporate issuance saw 5 issuers raise $3.5B in the primary market.

Looking Ahead

05:30 (LX) ECB’s Mersch (Luxembourg) in London

05:30 (HU) Hungary Debt Agency (AKK) to sell in 12-month Bills

05:30 (HU) Hungary Debt Agency (AKK) to sell Floating Rate Bonds

05:30 (PL) Poland to sell Bonds

05:45 (BE) ECB’s Praet (Belgium, chief economist) in Frankfurt

06:00 (BR) Brazil Jan IBGE Inflation IPCA M/M: 0.4%e v 0.4% prior; Y/Y: 3.0%e v 3.0% prior

06:00 (CL) Chile Jan CPI M/M: 0.3%e v 0.1% prior; Y/Y: 2.0%e v 2.3% prior, CPI Ex Food and Energy M/M: 0.2%e v 0.2% prior; Y/Y: 2.0%e v 1.9% prior

06:00 (ZA) South Africa Dec Manufacturing Production M/M: 0.5%e v 0.9% prior; Y/Y: 1.8%e v 1.7% prior

06:45 (US) Daily Libor Fixing

07:00 (UK) Bank of England (BOE) Interest Rate Decision: Expected to leave Interest Rates unchanged at 0.50%

07:00 (UK) Bank of England (BOE) Feb Minutes

07:00 (UK) Bank of England (BOE) Quarterly Inflation Report (QIR)

07:30 (UK) BOE Gov Carney post rate decision press conference

08:00 (RU) Russia Gold and Forex Reserve w/e Feb 2nd: No est v $452.8B prior

08:00 (US) Fed’s Harker (non-voter, hawk) on economy

08:05 (UK) Baltic Dry Bulk Index

08:15 (CA) Canada Jan Annualized Housing Starts: 210.0Ke v 218.0K prior (revised from 217.0K)

08:30 (US) Initial Jobless Claims: 232Ke v 230K prior; Continuing Claims: 1.94Me v 1.953M prior

08:30 (CA) Canada Dec New Housing Price Index M/M: 0.1%e v 0.1% prior; Y/Y: No est v 3.4% prior

08:30 (US) Weekly USDA Net Export Sales

09:00 (MX) Mexico Jan CPI M/M: 0.5%e v 0.6% prior; Y/Y: 5.5%e v 6.8% prior, CPI Core M/M: 0.3%e v 0.4% prior

10:30 (US) Weekly EIA Natural Gas Inventories

11:00 (NZ) New Zealand Jan QV House Prices Y/Y: No est v 6.6% prior

11:00 (US) Treasury announcement for 30-year TIPS auction set for Feb 15th

12:00 (US) USDA World Agricultural Supply and Demand Estimate (WASDE) Crop Report

(IT) Italy Debt Agency (Tesoro) announces BTP details for Feb 13th

12:45 (CA) Bank of Canada (BOC) Dep Gov Wilkins

13:00 (US) Treasury to sell $16B in new 30-Year Bonds

14:00 (MX) Mexico Central Bank (Banxico) Interest Rate Decision: Expected to raise Overnight Rate by 25bps to 7.50%

16:00 (NZ) New Zealand Jan ANZ Truckometer Heavy M/M: No est v -4.2% prior

18:00 (PE) Peru Central Bank (BCRP) Interest Rate Decision: Expected to leave Reference Rate unchanged at 3.00%