Sample Category Title

BoE Signals Faster Pace Of Rate Hikes. GBP Gives Up Gains

The Bank of England's monetary policy meeting yesterday surprised the markets with hawkish tone from the central. Officials voted to leave the interest rates unchanged at 0.50% at yesterday's meeting by a unanimous vote. However, the statement showed that the central bank expects faster pace of rate hikes given the uptick in the global growth.

Despite the hawkish tone from the BoE, the fact that the central bank acknowledged that the UK wasn't fully able to take advantage of the growth phase and the uncertainty from Brexit remained some key factors that offset the hawkish tone.

The equity markets resumed the selloff with the Dow Jones falling over 1000 points on the day on Thursday. Major U.S. stock indexes were down by at least 3%. The selloff extended to the Asian session with the Nikkei index down 2.7% while the Shanghai Index was seen losing 4.11% at the time of writing.

Earlier today, China's inflation data confirmed that consumer prices rose at a slower pace of 1.5% as expected. This is a weaker print compared to December’s inflation rate of 1.8%. Producer prices were also weaker, rising just 4.3% missing estimates and slower than December’s increase of 4.9%.

Looking ahead, the economic calendar will see Canada's unemployment details. Unemployment rate is expected to edge slightly higher to 5.8% while the economy is forecast to add 10.3k jobs during January.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

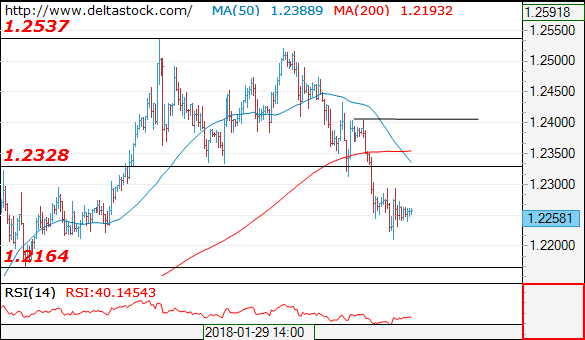

EUR/USD

Current level - 1.2258

Intraday allow a brief rebound to 1.2330 resistance area before next drowning towards 1.2160 target area. Crucial on the upside is 1.2405.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2330 | 1.2540 | 1.2210 | 1.2160 |

| 1.2405 | 1.2870 | 1.2160 | 1.2090 |

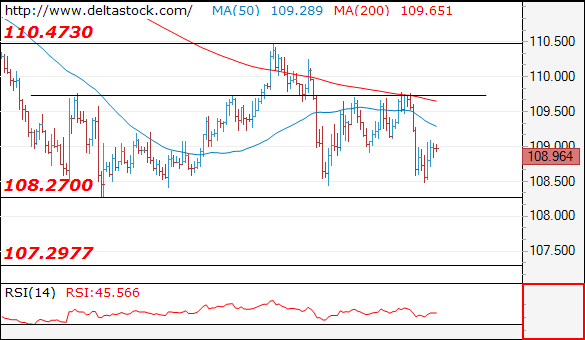

USD/JPY

Current level - 108.96

The recent test of 109.70 failed again and the pair is struggling above the lower range boundary at 108.30. The outlook is positive above 108.30, for a rise through 109.70, towards 110.50.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 109.70 | 111.90 | 108.30 | 108.30 |

| 111.50 | 113.40 | 108.30 | 107.30 |

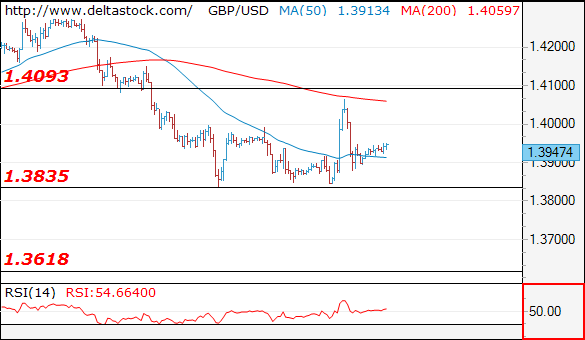

GBP/USD

Current level - 1.3947

Yesterday's spike to 1.4065 should be considered an inner part of the consolidation above 1.3835 and although there is an intraday risk of another climb to 1.4090 hurdle, the overall outlook on the senior frames remains bearish, for 1.3620.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3985 | 1.4090 | 1.3835 | 1.3730 |

| 1.4090 | 1.4174 | 1.3730 | 1.3620 |

Currencies: Dollar Struggles To Extend Gains As Global Market Volatility Remains High

Sunrise Market Commentary

- Rates: Core bonds hardly profit as US stocks take another dive

Core bonds made an intraday U-turn yesterday as US stock markets suffered another huge blow (-4%), but gains remained rather limited. It confirms underlying bearish sentiment. Spill-over effects to other markets are in general muted. Today's eco calendar is empty, so all eyes will be again on bourses. - Currencies: Dollar struggles to extend gains as global market volatility remains high

Yesterday, EUR/USD tried to extend its decline after Wednesday's break, but the move had no strong momentum. The dollar still has difficulties to play its save have role even as US yields remain elevated. Sterling jumped as the BoE signaled a steeper rate hike path, but the gains could not be sustained. EUR/GBP 0.8690 remains a very solid support

The Sunrise Headlines

- A late-afternoon rout sent S&P (-3.75%) to its lowest close since November. That leaves the S&P 500 benchmark 10% below its Jan. 26 record high. Volatility roared back with the VIX surging more than 20%. Asian stock markets lose up to 2.5% with China underperforming (up to -5%).

- US Congress missed a midnight deadline, failing to fund the government for a second time this year as a two-year bipartisan budget deal encountered delays in the Senate. A new vote is scheduled later today.

- A fast-growing mutual fund has told investors that it will not charge them to redeem what is left of their money, after losing more than 80% of its value in the wake of this week's turbulence. It's the biggest one-week drop for a mutual fund recorded in 20 years.

- China's producer and consumer inflation eased as expected in January. The PPI rose 4.3% Y/Y in January, the smallest rise in 14 months. CPI rose by 1.5% Y/Y.

- Australia's central bank said the economy is some way off full employment and inflation returning to the midpoint of its target, signalling policy will stay on hold.

- Moody's, the last of the major credit rating agencies to keep Portugal's debt in "junk" territory, considers it on the verge of regaining investment grade thanks to the country's economic and fiscal improvements.

- Today's eco calendar is thin with only UK industrial production data and UK trade balance.

Currencies: Dollar Struggles To Extend Gains As Global Market Volatility Remains High

EUR/USD decline slows even as volatility persists

The dollar maintained a positive momentum yesterday morning, but dynamics eased during the day. Some EUR/USD follow-trough selling occurred after the break below 1.2323. EUR/GBP selling after the BoE pushed EUR/USD to an intraday low in the 1.2215 area. From there, the euro decline/USD rally stalled, despite risk aversion. EUR/USD returned higher in the 1.22 big figure and closed the day at 1.2247. The return of volatility finally also triggered yen buying. USD/JPY dropped below 109. EUR/JPY tested 133 support, but a sustained break didn't occur. The moves in the FX majors stay modest given the swings on other markets.

Risk aversion still dominates Asian trading. Regional indices are losing up to 5%. Japan slightly outperforms. USD/JPY dropped temporary to the 108.50 area, but aggressive BOJ bund buying reinforces the Bank's will to maintain an easy policy, slowing the rise of the yen. USD/JPY trades again around 109. EUR/USD is going nowhere in the 1.2250 area. The yuan stabilizes after yesterday's correction against the dollar.

There are no important data in the US and Europe today. So, global factors will continue to dominate FX trading. Of late, the swings in the major USD cross rates were modest given the turmoil on other markets. The combination of higher core yields and an aggressive risk-off finally turned out USD positive. That said, the safe haven appeal of the dollar was far from impressive. It more looked like some cautious by default USD buying. We assume that this pattern can continue as long as the current global repositioning continues. Technical picture: the dollar decline slowed of late and EUR/USD finally dropped below 1.2323/35 support. A break below 1.2165 would call off the ST downside alert (for USD). We continue to monitor the EUR/JPY price action. A further risk-off correction in EUR/JPY might also put downward pressure on EUR/USD. However, in this respect, yesterday's price action was inclusive. The EUR/JPY decline was blocked at the key 133 support area.

Sterling jumped higher as the BoE indicated that rates will probably have to be raised faster than anticipated. Most of the rebound was reversed later as a new wave of risk-off repositioning weighed on sterling. Markets probably also realized that the Brexit-cliff isn't out of the way. EUR/GBP closed the session only marginally lower at 0.8803. UK production and trade balance data will be published today. Yesterday's price action confirmed our working hypothesis that the 0.8690 support probably won't be easy to break without big progress on Brexit.

EUR/USD: few follow-through gains despite Wednesday's break lower.

USDCAD Trades Higher After The Rebound On 1.2250

USDCAD rose as high as 1.2620, a level last experienced on December 28 and is posting a bullish rally following the rebound on the 1.2250 support level last Friday. Additionally, dollar/loonie is in progress to record the second consecutive green week as it also successfully surpassed the 23.6% Fibonacci retracement level at 1.2470 of the down-leg from 1.3800 to 1.2060.

Short-term momentum indicators are also pointing to a continuation of the bullish bias. However, the RSI is sloping to the downside in the positive territory, suggesting that the price could have a small retracement before its upward movement. On the other hand, the MACD oscillator is endorsing the bullish tendency as the indicator is rising near the zero line, deviating above its signal line.

If price jumps above the 1.2620 resistance level, which coincides with the upper Bollinger Band, there is scope to test the 38.2% Fibonacci mark near 1.2720. Rising above it could see prices re-test the 1.2910 peak taken from December 19.

In the event of a continuation of the major bearish trend, the 23.6% Fibonacci mark could be the next pause. A break below this level would shift the short-term outlook to bearish as it could take the pair towards the 1.2250 support barrier.

EURUSD Still Bearish Below 1.2275 Level

The EURUSD pair remains bearish and under downside pressure in early Friday trading, as risk-off trading sentiment continues to spread through broader financial markets. Price-action is currently range-bound between the 1.2240 to 1.2270 region, after the pair suffered more extreme volatility on Thursday, with the euro sinking to a new weekly low, hitting 1.2212. Moving into the European trading session, the U.S dollar index and fluctuating stock prices are likely to dictate the EURUSD pair next directional bias.

The EURUSD pair is strongly bearish while trading below the 1.2275 level, further losses towards the 1.2212 and 1.2192 levels may occur.

Should EURUSD price-action move above the 1.2275 level for a sustained period, we may see a move back towards the 1.2305 and 1.2332 resistance levels.

USDJPY Pair Looking For Direction Around 108.98

The USDJPY pair has moved back towards the pivotal 108.98 level, after suffering yet another pull-back towards the 108.50 zone, following the broad-based decline in global equity prices on Thursday. Investors continue to seek safe-haven asset classes on the last trading day of the week, as risk-off trading sentiment worsens, underpinning overall demand for the Japanese yen currency. Moving into the European trading session, traders will look to equity prices and the key 108.98 level for guidance on the USDJPY pairs next intraday move.

The USDJPY pair remains intraday bullish while price-action trades above the 108.98 level, further upside towards 109.44 and 109.71 may occur.

Should the USDJPY pair start to trade below the 108.98 level for an extended period, we may see a correction back towards the 108.70 and 108.45 support levels.

Has Bitcoin Bottomed?

In December, bitcoin soared to almost $20,000 following a series of positive news. The biggest news of all was the institutionalization of the currency following its listing at the Chicago Board Options Exchange (CBOE) and CME.

After that, the price started falling following another series of negative news, mostly from China and South Korea. Last week, bitcoin continued its decline following reports that Bitfinex, one of the largest exchanges was under investigation. It reached a low of $5860 on Tuesday, before starting to gain. So far, it has gained more than 20% of value from the Tuesday’s low.

Some people now believe that bitcoin has bottomed. Yesterday, Dan Morehead, who had predicted the correction accurately, told CNBC that he believed that bitcoin had bottomed. In the interview, he argued that on average, bear runs take 72 days. The cryptocurrencies bear run is in the 52nd day, which means within a few more days, the prices could move higher.

When Morehead speaks, traders listen. According to Hedge Fund Research Indexes, his fund has recently gained more than 22,000% by investing in cryptocurrencies. He believes that investors’ appetite in cryptocurrencies would help push the price higher.

Today, traders should watch out for the $7800 level, which provides an important support. They should also watch out for the $8626 level, which is the highest level it reached yesterday. A breach in either direction could see an extended price action in that direction.

UK Factory Data Headlines FInal Session Of The Week

A steady stream of economic data will flow through the financial markets on Friday, with reports on UK factory output and Canadian employment set to draw the most headlines.

Action begins at 07:45 GMT with a report on French industrial output. A similar report will be produced in Italy later in the morning.

The United Kingdom's Office for National Statistics will also release a spate of economic indicators on Friday, including industrial production, manufacturing production and the total trade balance. Industrial output is forecast to fall 0.9% in December, while manufacturing is expected to grow 0.3% month-on-month.

Analysts are projecting a total trade deficit of £2.4 billion for December, down from £2.8 billion the month before.

North American trading kicks off with a report on Canadian employment at 13:30 GMT. The Canadian economy is forecast to have added 10,000 jobs in December, following a net gain of 78,600 the month before. The unemployment rate is expected to rise slightly to 5.8% from 5.7% even as workforce participation wanes.

In the United States, the Commerce Department will report on December wholesale inventories at 15:00 GMT. The data series is used in the calculation of gross domestic product (GDP).

Earlier in the day, the Chinese government produced weaker than expected inflation data for the month of January, raising some concerns about the health of the world's second largest economy.

Beijing's consumer price index (CPI) rose 0.6% in January, which was slightly lower than the 0.7% reading forecast by economists. In annual terms, CPI inflation slipped to 1.5% from a previous reading of 1.8%.

The producer price index (PPI) slipped to an annualized rate of 4.3% in January, compared with 4.9% the month before.

EUR/USD

The euro continued to backtrack against the dollar on Thursday, as prices fell below 1.2300 for the first time in more than two weeks. The EUR/USD exchange rate was last seen trading at 1.2258, where it was little changed compared to the previous close. Support levels are located at 1.2210. On the flipside, resistance is likely found at 1.2295.

GBP/USD

The British pound spiked on Thursday on hawkish commentary from the Bank of England (BOE) before quickly surrendering gains. Cable touched a session high of 1.4059 before falling back down to 1.3900. It was last seen trading at 1.3938. The GBP/USD faces immediate support at the psychological 1.3800 level. On the opposite side of the spectrum, immediate support is located at the daily high.

USD/CAD

The US dollar extended gains against its northern rival on Thursday, with the USD/CAD climbing to fresh six-week highs. The pair was last seen trading just below 1.2600, with momentum on the side of the bulls.

Daily Wave Analysis: GBP/USD Bullish Spike Fails To Break 1.40 At First Attempt

Currency pair GBP/USD

The GBP/USD is probably still in a wave 4 (green) correction. A break above the resistance (red) could indicate a bullish rally whereas a bearish break below support (green) would make this wave analysis unlikely and could indicate a potential downtrend.

The GBP/USD made a strong move up but fell equally hard. Still, the pattern could be a wave 1-2 (grey) although a break above resistance (red) is needed before that becomes more likely. A break below the bottom of wave 1 invalidates the wave 1-2.

Currency pair EUR/USD

The EUR/USD remains in a bearish channel which is probably part of a wave 4 (purple) correction as long as price stays above the Fibonacci levels (purple). A break above resistance (red/orange) could see the start of a wave 5 (purple). A break below the 50-61.8% Fib support makes a wave 4 less likely.

The EUR/USD indeed made one more lower low within a wave 4-5 (orange). The bullish bounce could indicate a potential bullish wave 1-2 (blue) but price would need to break above resistance to confirm a potential wave 3 (blue) breakout.

Currency pair USD/JPY

The USD/JPY is still trapped in between strong support (green/blue) and resistance (red/orange). Price could be building a wave 1-2 (purple) pattern but a bullish break is needed. A bearish break below the bottom and 100% Fib invalidates the wave 2 (purple).

The USD/JPY needs to break above resistance (red) before an uptrend continuation is likely.

Equities Face A Nervous Session As The Weekend Draws Near

The global equity markets are bracing themselves for a stormy closing session this week, as data from Thomson Reuters' Lipper unit shows US fund investors withdrew the largest amount from US-based equity exchange-traded funds on record. The amount totals $23.9 billion coming out of equity ETFs in the week. The reason cited by the research unit was the overbought conditions, with a correction overdue. Asian stock markets fell overnight, as the Nikkei finished down 2.32% at 21382.62, but off the session low of 21119.00. The Chinese Shanghai Composite was down 5.07% at the time of writing, off its low of 6% earlier. Last Friday saw substantial selling, as fear took over, with a stronger follow through on the market open Monday.

German Current Account n.s.a. (Dec) was €27.8B v an expected €25.0B, from a previous €25.4B. Exports (MoM) (Dec) were 0.3% v an expected -1.0%, from 4.1% previously. Imports (MoM) (Dec) were 1.4% v an expected -0.5%, from 2.3% previously. Trade Balance s.a. (Dec) was €21.4B v an expected €21.7B, from a prior €22.3B. EURUSD moved higher from 1.22633 to 1.22943 because of this data release.

German Buba President Weidmann spoke on Monetary Policy in the European Context at the Monetary and Economic Policies on both sides of the Atlantic conference in Frankfurt. He said that a substantial extension of ECB QE is not justified if growth continues as expected. Euro appreciation is unlikely to jeopardise expansion and there is no sign of Eurozone growth abating anytime soon. The recent German wage deal supports expectation for gradually rising inflation. ECB policy should not remain loose beyond QE and should not be unsettled by the recent stock market sell-off.

RBA Governor Lowe spoke at the A50 Australian Economic Forum in Sydney. He stated that there is no strong case for near-term adjustment in policy and that rates will only rise on further progress with jobs and inflation. He added, it is likely that next Australian interest rate move will be up and quarterly economic forecasts are largely unchanged, and that progress in cutting the jobless rate and lifting inflation will be gradual. Volatility in stocks hasn't affected the RBA growth outlook, he said, and Australia does not have to tighten in ‘lock-step' with other central banks. The RBA are still carefully watching high household debt levels and the forecast for GDP growth is a bit above 3% over the next two years. Finally, a lift in wage growth is ‘likely to be necessary' to meet inflation goals.

The Bank of England Interest Rate Decision was left unchanged at 0.5%, as expected. The BOE Minutes, BOE Quarterly Inflation Report and the Monetary Policy Statement were released at the same time. The BOE Asset Purchase Facility was maintained at £435B. The BOE MPC Vote remained unchanged at 9. GBP crosses saw a spike in volatility after this data was released.

Canadian Housing Starts s.a. (YoY) (Jan) were 216.2K v an expected 210K, from a previous 217K. USDCAD continued its decline to 1.25453 from 1.25696.

US Initial Jobless Claims (Feb 2) were 221K v an expected 232K, from a previous 230K. Continuing Jobless Claims (Jan 26) were 1.923M v an expected 1.945M, from 1.953M previously. USDJPY moved up to 109.720 before resuming its decline to 109.239.

US FOMC Member Kaskari spoke in South Dakota, saying it's too soon to know if tax cuts will boost wage and hiring. Trust in the US may eventually erode amid rising debt. Deficit and debt are not currently near-term issues but this may change. The US is a long way away from wages and inflation rising. There is consistent wage growth needed to have an impact on rates. The bond market is signalling inflation is going to be under control, well into the future. If the tax cut does not lead to more optimism, it could be a net positive for the US economy.

Canadian BOC Governing Council Member Wilkins spoke on innovation and inclusive growth at the G7 Symposium in Quebec. She stated that high household debt is the biggest vulnerability to the economy, followed by NAFTA. The BOC is also factoring in the rest of the economy's performance as it sets policy. Some households may find debt service extremely difficult but, overall, the bank expects economy and consumption to continue to grow. The quarter didn't get off to the strongest start, in line with expectations; the bank is data dependent. The rising stock market volatility, in the context of a strong economy and rising bond yields, is to be expected. The asset prices feed through to monetary policy transmission mechanism and forecasts but this only matters to the extent they are in one direction and large. The bank looks at market pricing but it is rarely a source of concern and the focus is on setting the right policy to achieve its inflation target. There is often more potential being built in an up cycle than economists put in their projections.

Australian RBA Monetary Policy Statement was released this morning. Also released at this time was Home Loans (Dec) coming in at -2.3% v an expected -1.1%, from a previous 2.1%, which was revised down to 1.6%. Investment Lending for Homes (Dec) came in at -2.6% v a previous 1.5%. AUDUSD sold down from 0.77859 to 0.77706 after this data was made public.

Chinese Consumer Price Index (YoY) (Jan) was as expected at 1.5% from 1.8% prior. Producer Price Index (YoY) (Jan) was 4.3% v an expected 4.4%, from 4.9% previously. Consumer Price Index (MoM) (Jan) was 0.6% v an expected 0.7%, from 0.3% previously.

Japanese Tertiary Industry Index (MoM) (Jan) was -0.2% v an expected 0.2%, from 1.1% previously.

Swiss Unemployment Rate s.a. (MoM) (Jan) remained unchanged, as expected, at 3%.

EURUSD is up 0.11% overnight, trading around 1.22601.

USDJPY is up 0.19% in early session trading at around 108.947.

GBPUSD is up 0.36% to trade around 1.39614.

USDCNH is down -0.31% overnight, trading around 6.34260.

Gold is up 0.11% in early morning trading at around $1,320.10.

WTI is down -3.31% this morning, trading around $60.20.

Major data releases for today:

At 09:30 GMT, UK Industrial Production (YoY) (Dec) is expected to be 0.3% from a previous 2.5%. Manufacturing Production (MoM) (Dec) is expected to be 0.3% from 0.4% previously. Industrial Production (MoM) (Dec) is expected to be -0.9% from 0.4% previously. Manufacturing Production (YoY) (Dec) is expected to be 1.2% from 3.5% previously. GBP pairs could move because of this data release.

At 10:30 GMT, the Russian Interest Rate Decision will be released. The expectation is for a drop to 7.50% from 7.75%. This could affect the pricing in RUB crosses.

At 13:00 GMT, the UK NIESR GDP Estimate (3M) (Jan) is expected to be 0.3% from 0.6% prior. GBP may be exposed to price volatility from this data release.

At 13:30 GMT, Canadian Unemployment Rate (Jan) is expected to be 5.8% from a previous 5.7%. Participation Rate (Jan) is expected to be 65.7% from 65.8% prior. Net Change in Employment (Dec) is expected to be 10.0K from a prior 78.6K. CAD pairs could see an increase in price movement from this data.

At 16:45 GMT, UK MPC Member Cunliffe will be speaking at the Asset Management Derivatives Forum in California. GBP crosses may experience volatility around this time in reaction to his comments.

At 18.00 GMT, the Baker Hughes US Oil Rig Counts will be released, with a headline number from last week of 765. The expected number this week is 758. WTI Oil could become volatile around this data release and will be in traders' minds when trading resumes on Monday.