Sample Category Title

Summary 2/5 – 2/9

Monday, Feb 5, 2018

[php_everywhere] [/php_everywhere]

Tuesday, Feb 6, 2018

[php_everywhere] [/php_everywhere]

Wednesday, Feb 7, 2018

[php_everywhere] [/php_everywhere]

Thursday, Feb 8, 2018

[php_everywhere] [/php_everywhere]

Friday, Feb 9, 2018

[php_everywhere] [/php_everywhere].

Weekly Economic and Financial Commentary: Happy Days Are Here Again

U.S. Review

A Strong Start to the New Year

- Nonfarm employment blew past expectations, with payrolls adding 200,000 jobs in January and data for the past year were revised higher to show an average gain of 181,000 jobs per month, or 10,000 more than previously thought.

- The unemployment rate was unchanged in January at 4.1 percent, but average hourly earnings shot up to 2.9 percent year to year, which suggests the tightening job market may finally be pulling wages higher.

- The ISM manufacturing survey showed surprising strength, indicating that business fixed investment will likely be much stronger in 2018, adding some upside risks to GDP growth.

Happy Days Are Here Again

The past week marked a particularly tumultuous period for the U.S. economy. Most key economic data came in well ahead of expectations, causing many forecasters to reassess their expectations about how tax reform will impact U.S. economic growth and whether they should upgrade their forecasts. The yield on the 10-year Treasury spiked, as concerns about rising inflation and larger budget deficits pushed yields past key benchmarks. More forecasters have also raised their expectations for Federal Reserve rate hikes, adding a fourth hike in December 2018.

The strong start to 2018 appears to be fairly broad based. Manufacturing is clearly leading the way. The ISM manufacturing survey ticked down 0.2 points to 59.1, but new orders remained exceptionally strong and the backlog of unfilled orders increased. While the index declined slightly, it does not signal a slowing in manufacturing activity or the economy. The ISM survey is a diffusion index and measures the breadth of strength in the factor sector, not the magnitude of that strength. The current reading is consistent with solid growth in manufacturing and real GDP growth in the 4 percent range. Along those lines, the closelywatched Atlanta Fed GDPNow forecast for first quarter GDP growth jumped from 4.2 percent to a whopping 5.4 percent.

Other data released earlier this week also show the economy had strong momentum at the end of 2017 that was carrying over into the new year. Consumer confidence rose 2.3 points in January, with all of the gain coming from the expectations series. The rise in expectations likely reflects the surge in the stock market earlier in the month as well as growing optimism about tax reform. The present situation index fell slightly but remains near historic highs.

Rising consumer confidence helps explain the persistent drop in the saving rate. Consumers have become much more optimistic about their employment prospects and are willing to spend a larger proportion of their take-home pay. Attitudes are also likely being bolstered by the run-up in the stock market and rising home prices. S&P CoreLogic Case-Shiller home prices rose slightly more than expected and were up 6.2 percent year over year in November.

The Federal Reserve's January FOMC meeting ended with little fanfare. The Fed kept the federal funds rate unchanged and made few meaningful changes to their policy statement. The financial markets are looking for the Fed's new leadership to take a slightly more hawkish tone and will get the first good look into the Fed's mindset when the Fed's new chair, Jerome Powell, delivers his Semi-Annual Testimony to Congress later this month.

The January employment report came in well ahead of expectations. Nonfarm employment rose by 200,000 in January. Hiring rose solidly in construction and manufacturing. The factory sector appears to be benefitting from stronger global economic growth and the weaker dollar. The unemployment rate was unchanged at 4.1 percent, but average hourly earnings jumped up to a 2.9 percent year-to-year gain. The increase adds to concerns the economy might grow too fast for its own good in 2018, which sent bond yields higher immediately after the report was released.

U.S. Outlook

ISM Non-Manufacturing • Monday

The ISM non-manufacturing index slowed to 56.0 in December after hitting its highest level in more than a decade in the prior month. Hurricane-related distortions may have played a role. Employment rose in December, further suggesting that the slowdown seen in the December payrolls report was not particularly worrisome.

The new orders index slowed over the month to 54.5, its lowest level in more than a year. Coming off of its impressively high average of 61.2 over the past three months, this slowdown is worth noting. Input price pressures were revised down slightly and continue to remain below the elevated levels seen at manufacturers.

On Monday, we receive data for January. We expect the ISM nonmanufacturing index to pick up marginally to 56.4, based on continued growth and increased demand within the services sector.

Previous: 56.0 Wells Fargo: 56.4 Consensus: 56.5

Trade Balance • Tuesday

The U.S. trade deficit widened to $50.5 billion in November, registering the first time that the deficit has exceeded $50 billion since March 2012. There was broad-based strength on both the export and import side of the ledger. With the value of exports up 6.0 percent in the September-November period year over year, overall exports clearly have rebounded in 2017 after experiencing weakness in 2016. Similarly, import growth has strengthened over the course of 2017, in-line with higher commodity prices, but more importantly due to an up-tick in domestic demand.

As we noted at the time of the November release, the strong levels of exports and imports were likely to cause real net exports to be a drag, on Q4 GDP growth. The advance GDP report, published last week, disclosed net exports produced about a 1 percentage point drag on overall GDP growth in the fourth quarter. We expect a modest drag from trade to continue for the next few quarters.

Previous: -$50.5B Wells Fargo: -$52.2B Consensus: -$52.0B

JOLTS • Tuesday

After registering a sharp run-up over the first three quarters of 2017, job openings fell for the second consecutive month in November. Although total job openings are still up 4.4 percent over the past year, this rate marks a slowdown from earlier in the year and, if sustained, suggests a more moderate pace of hiring ahead.

Gross hiring fell in November, coming off of storm-related increases in October. However, the hiring rate, currently sitting at 3.7 percent, remains low relative to the previous cycle. This perhaps points to the less dynamic labor market that exists today.

The quits rate remains high, which perhaps explains the better than expected growth in average hourly earnings in this week's jobs report. The strength of the January jobs report signals that overall demand for labor is holding up.

Previous: 5,879

Global Review

Mexican Growth Improves in Q4; Europe and Japan

- According to the "flash" release for the performance of economy in Q4-2017, the Mexican economy improved a bit in the last quarter of the year, up 1.0 percent, sequentially and not annualized. On a year-earlier basis, the economy grew 1.8 percent non-seasonally adjusted.

- Eurozone GDP grew 2.7 percent versus a year earlier in the fourth quarter, according to the advance release, while inflation continues to remain benign.

- Japanese industrial production increased a larger-thanexpected 2.7 percent month on month and 4.2 percent year over year in December.

Mexican Economy Improves in Q4

According to the "flash" release for the performance of the economy in Q4 2017, the Mexican economy improved a bit in the last quarter of the year, up 1.0 percent, sequentially and not annualized. On a year-earlier basis, the economy grew 1.8 percent non-seasonally adjusted. This means that the Mexican economy grew 2.08 percent for the whole of 2017. Our forecast for the Mexican economy in 2017 was 2.0 percent after reversing our original call for a slight recession due to the increased risks of the United States abandoning the NAFTA agreement between Canada, the United States and Mexico.

However, the details of the release were relatively weak with the economy being driven by the service sector, up 1.2 percent sequentially and not annualized and by 2.6 percent on a yearearlier basis. For the year as a whole, the service sector increased a strong 3.1 percent. That is, economic growth continues to be driven, fundamentally, by domestic consumption. The allimportant industrial sector was very weak at the end of the year, driven by a very weak mining sector. As this is a flash release, we do not have the details on the supply side or information on the demand side, but we are able to infer where the weakness resided during the year, something that we believe did not change as the year came to a close. The industrial sector managed to increase 0.1 percent sequentially and not annualized in the last quarter of the year but was down 0.7 percent on a year-earlier basis, not seasonally adjusted. The industrial sector however, declined 0.6 percent for the year as a whole. Meanwhile, the primary sector, which is a highly volatile sector and includes agriculture, cattle and fisheries, saved the day for the fourth quarter GDP release as it increased 3.1 percent on a sequential basis and not annualized and by 4.2 percent on a year-earlier basis, not seasonally adjusted. For the year as a whole, the sector increased a strong 2.8 percent.

Thus, even if the Mexican economy improved in the last quarter of the year it remains weak and we are not expecting much change regarding the Mexican economy's performance this year as it continues to navigate a still risky NAFTA negotiating process and a contentious presidential election slated for July.

European and Japanese Expansion Continues

Meanwhile, Eurozone GDP grew 2.7 percent versus a year earlier in the fourth quarter, according to the advance release, while inflation continues to remain benign. In light of this, there is renewed talk of the ECB starting to tighten monetary policy in the near future. For more on this see "Eurozone Economic Outlook: Does Monetary Tightening Lie Ahead?," which is available on our website. In the U.K., the Markit manufacturing PMI was a bit lower than expected in January, at 55.3, compared to a slightly downwardly revised 56.2 print for December but well above the 50 demarcation point between expansion and contraction, while in Japan industrial production increased a larger-than-expected and strong 2.7 percent month over month and 4.2 percent year over year in December. All these data point to a relatively strong growth contribution from the developed side of the global economy.

Global Outlook

China FX Reserves • Tuesday

Last month, rumors that Chinese officials were considering slowing or halting purchases of U.S. Treasuries briefly roiled the bond market, sending Treasury yields higher. Although this attentiongrabbing headline quickly faded, hard data on Chinese FX reserves can partially help corroborate any change in China's policy regarding Treasuries, were it to occur.

Foreign central banks have many instruments through which they can hold FX reserves, but they typically hold them via liquid, interest-earning assets such as U.S. Treasury securities. Chinese FX reserves declined rapidly for about a two-year stretch from 2014 to 2016 as the Chinese renminbi encountered significant selling pressure, and Chinese Treasury holdings declined accordingly. Since then, Chinese FX reserves have stabilized and even grown slightly as capital flows out of the country have slowed. The Bloomberg consensus looks for another month of little change in January.

Previous: $3.14 Trillion Consensus: $3.17 Trillion

Bank of England Meeting • Thursday

Economic growth in the United Kingdom has generally been sluggish, rising a modest 1.5 percent year over year in Q4. The sharp depreciation of sterling after Brexit led to a rise in inflation that subsequently eroded income growth and led to a drag on consumer spending. Growth in investment spending also slowed over the past year as Brexit uncertainties likely inhibited more expansionary business decisions. Amid above-target inflation and fading recession fears, the Monetary Policy Committee (MPC) of the Bank of England hiked rates 25 bps in October 2017.

In our view, growth will remain slow enough over the next few quarters to keep the MPC on hold for now. By the end of the year, however, real GDP growth should be showing signs of strengthening anew as inflation recedes. We forecast that the MPC will tighten by 25 bps in Q4-2018, and we look for two more 25 bps rate hikes over the course of 2019.

Previous: 0.50% Wells Fargo: 0.50% Consensus: 0.50% (Bank Rate)

Canadian Employment • Friday

Canadian employment surged to end 2017, posting the second strongest cumulative two-month gain on record. These job gains helped drive the unemployment rate a stunning 0.6 percentage points lower over the course of just two months. A rapidly tightening labor market and economic growth of 3 percent year over year gave the Bank of Canada (BoC) the confidence to lift its main policy rate 25 bps to 1.25 percent at its first meeting of 2018.

The BoC has been willing to move quickly based on economic data, with its September and January rate hikes following unexpectedly strong GDP and employment growth, respectively. That said, we believe high household debt levels and uncertainty over the future of the North American Free Trade Agreement will give the BoC pause about ratcheting up the pace of tightening further. Next Friday's jobs report will give policymakers a look at whether the recent trend in job growth will come back to Earth or keep heading to the moon.

Previous: 78,600 Consensus: -2,000

Point of View

Interest Rate Watch

Loan Growth: Where We're Going

As recorded economic growth and expectations for growth in 2018 increase, the expectations are that bank lending will increase as well. With more growth comes more opportunities to lend by banks and a greater willingness by their customers to borrow. How can we monitor the change—if it comes?

The Incentive to Lend: Expectations

For banks, the profitability on lending has diminished in recent years (top graph). Banks continue to face competitive pressures from non-banks and capital markets in general. Bank loans to nonfinancial corporations represented 25 percent of credit in the 1980s, and are down to a representation of 11 percent today. In addition, the decline of interest rates since the early 1980s has also lowered the spread in lending credit to non-financial institutions.

Expectations matter here. If lending institutions, both banks and non-banks, anticipate better economic growth going forward, then in an environment of modestly rising interest rates, lending spreads would widen and offer better returns to all creditors.

Demand Side for Credit

Credit demand at banks typically is very pro-cyclical. In the early years of the recoveries of 1990, 2002 and 2010 (middle graph), there was a distinct upswing in the reported demand for credit at banks. This upswing reflects the improved optimism of business on future growth and therefore the willingness to borrow.

Currently, it remains to be seen if the optimism reported in surveys will translate to an upswing in demand.

CRE: A Less Cyclical Issue

While the tax program aims at stimulating business investment with immediate expensing, it is less obvious if the tax program, or the pick-up in economic growth, will stimulate commercial real estate (CRE) investment. As illustrated in the bottom graph, the demand for CRE loans at banks has been declining for several years. This may reflect a less cyclical pattern for real estate credit and thereby less of a lift due to the current fiscal package going forward.

Credit Market Insights

Loan Growth: Where We've Been

Commercial and industrial (C&I) loans at commercial banks grew 1.1 percent in December on a year-ago basis. This rate is up slightly from November's 0.9 percent pace, but still near a six-year low.

C&I loan growth has slowed broadly across institution types. However, small domestic banks have fared better than their foreign and large domestic counterparts, with loans up 4.4 percent on the year in December. At foreign-related institutions, C&I loans declined 3.8 percent for a ninth straight month of negative growth.

Companies may be turning to other sources of funds, explaining lower loan demand growth. Rising corporate profits likely mean less need for financing. In addition, corporate bonds are making up a larger share of total liabilities for nonfinancial corporations as capital markets open up. Since small domestic banks tend to have customers with less access to capital markets, this factor could help explain their smaller drop-off in loan growth.

Loan demand has been tepid despite relatively easy financial conditions. According to the Senior Loan Officer Opinion Survey, banks on net are still loosening or maintaining standards for C&I loans. Short term rates ticked up with the fed funds rate in 2017, but long term rates stayed about put. This led to a flattening in the yield curve to around a decade low. However, long-term rates have marched higher since the start of the year, which may constrain loan demand further.

Topic of the Week

When Supply Doesn't Meet Demand

U.S. Treasury yields have jumped to start the year, with the benchmark 10-year Treasury yield rising nearly 40 bps since January 1. A key driver has been concerns surrounding supply and demand in the Treasury market.

On the supply side, net issuance is set to accelerate in 2018 for a variety of reasons, including less tax revenue due to recently enacted legislation, steady spending growth and technical reasons related to the debt ceiling. We forecast a federal budget deficit of $750 billion in FY 2018 and $950 billion in FY 2019, up from a deficit of $666 billion in FY 2017. This jump in issuance is set to occur right as the Fed's balance sheet reduction program begins to meaningfully ramp up in the coming months. The result is a significant increase in the supply of Treasuries the market must absorb, a topic we have covered at length (top chart).

Rising supply has raised questions about who will buy all this new debt, and at what price. In a report published last fall, we found that price-sensitive buyers, such as U.S. households and foreign-private purchasers, are the most likely candidates to become the marginal buyers. We noted that "if demand for Treasury securities falls short of supply at current prices, then yields will need to rise to clear the market." This appears to be playing out now as the market adjusts to less demand from central banks amid an expected onslaught of new supply.

First, however, Congress must increase the debt ceiling, or the legal upper-bound on the nation's borrowing limit. Since December, the Treasury has been utilizing extraordinary measures to remain solvent. In a report published Tuesday, our analysis indicated that the extraordinary measures will last until the first week of March, at which point the Treasury will likely become dangerously low on cash. The combination of another potential budget impasse, in conjunction with a debt ceiling countdown, could rattle consumer confidence and financial markets in the weeks ahead (bottom chart).

The Weekly Bottom Line: Faster Growth + Inflation = Higher Bond Yields

U.S. Highlights

- Another week, another sell-off in the bond market. As of the time of writing the U.S. 10-year yield stood at over 2.8%, up more than 10 basis points from the end of last week.

- U.S. payrolls expanded by 200k in January while the unemployment rate remained steady at 4.1%. The big story though was the acceleration in wage growth. Average hourly earnings growth hit 2.9% year-on-year, up from 2.6% and the fastest growth since 2009.

- Recent economic data cement the case for the Federal Reserve to raise interest rates at its next meeting in March. Expect at least another two rate hikes from the Powell-led Fed before the end of 2018.

Canadian Highlights

- The TSX continued to sell-off this week with the composite benchmark tumbling to a 14-week low, making it one of the worst performing major bourses so far this year. The index was weighed on by the energy, utilities and telecoms sectors.

- Economic data was more positive, with real GDP advancing a solid 0.4% in November, boosted by a strong gain in the goods sector.

- The 6th round of NAFTA negotiations wrapped up early in the week, with a somewhat more optimistic tone emerging. Still, all sides remain far apart on many key issues with uncertainty likely to weigh on business investment as a result.

U.S. - Faster Growth + Inflation = Higher Bond Yields

Another week, another sell-off in the bond market. As of writing the U.S. 10-year yield stood at over 2.8%, up more than 10 basis points from the end of last week. Since the beginning of the year, the yield has risen over 40 basis points and now sits at its highest level since 2014.

The rise in yields is both a real growth and inflation story. On the real side, the sell-off has come as the median Bloomberg forecast for 2018 real GDP moved up 30 basis points to 2.6%, from 2.3% last October. Undoubtedly, tax cuts played a role. The biggest increases came as they were announced and then passed into law.

On the inflation side, market-based measures of inflation expectations have also moved up. The five-year forward inflation rate (an indicator of expectations for inflation five-to-ten years from now) has moved up over 20 basis points since the start of the year (Chart 1). Tax cuts are expected to push economic growth further above its trend rate and also increase the supply of Treasury securities, even as the economy approaches full employment.

Bond market moves have also been supported by economic data. Most relevant, the job market shows little signs of slowing. Job growth in January hit the 200k mark, ahead of the 181k per month averaged over the course of 2017. What's more, wage growth accelerated noticeably to 2.9% year-on-year, from 2.7% in December (Chart 2). The rise in compensation is evident in other metrics as well. The employment cost index (ECI) rose to 2.7% (from 2.5%) year-on-year in the fourth quarter, while compensation per hour in the productivity and costs (PLC) data jumped to 2.2% (from 0.9%).

The acceleration in wage growth will come as a relief to believers in the Phillips curve, giving credence to the notion that as workers become scarce, the wages offered to attract and retain them should rise. At the same time, recent data have also shown the importance of "shadow slack." While the unemployment rate has been fairly steady, the employment to population ratio of 25 to 54 year olds has moved higher (it edged down ever so slightly in January to 79.0% from a cycle high of 79.1%). Still, its steady improvement is more consistent with the gradual rise in wage growth than the unemployment rate alone.

The increase in bond yields over the start of 2018 makes sense given these cyclical dynamics. Still, we would caution about extrapolating recent moves much further going forward. While the economic data support an ongoing expansion, the structural forces weighing on interest rates have not changed. Population aging will continue to exert downward pressure on the economy's trend growth rate and the terminal (or neutral) level of the federal funds fate. At the same time, continued pressure on global bond yields from elevated debt levels and structural impediments to growth will keep a lid on U.S. yields.

All told, economic data and fiscal policy developments cement the case for the Federal Reserve to continue to normalize policy. Still, with a neutral rate in the neighborhood of 2.5%, three hikes in 2018 should be more than sufficient to keep a lid on inflation and allow any remaining labor market slack to be absorbed.

Canada - Economy on Good Footing But Risks Remain

The TSX sell-off continued this week, with the composite benchmark tumbling to a 14-week low, making it one of the worst performing major bourses so far this year. The energy sector was the main drag, weighed down by natural gas prices with Henry Hub futures down nearly 20%. The rise in WTI crude oil prices was also of little help for the loonie, given the spread to the WCS benchmark, which widened by nearly $3 to $30.50. But, the pain wasn't confined to the energy sector, with rate-sensitive telecom and utilities sectors also sharply lower as Canadian bonds sold-off in lockstep with their U.S. counterparts. The loonie gained some ground early in the week, but more than gave up those gains following the solid U.S. payroll report which telegraphed strong hiring and rapidly rising wages south of the border.

In contrast to the bourses, Canadian economic data released this week painted a positive picture of the underlying economy. Real GDP advanced by a solid 0.4% in November, boosted by a rebound in the goods sector (Chart 1). Manufacturing output surged as production resumed at several major auto plants following earlier shutdowns. Not to be outdone, the services sector expanded for the 20th straight month. In fact, one of the most impressive aspects of the report was the breadth of the monthly gain (Chart 2), with wall-to-wall growth indicating that the economy was operating on all cylinders. Importantly, available data for December points to another solid month of growth, thanks to surging employment, a healthy gain in hours worked and firm housing activity. All told, November's monthly gain, coupled with our expectations for a healthy December print, put the economy on track for a 2.4% annualized quarterly gain, representing another quarter of above-potential growth and indicating good momentum heading into 2018.

This week also marked the end of the 6th round of NAFTA negotiations and despite some gloomy headlines, the tone coming out of the talks appeared somewhat more optimistic. Indeed, the U.S. Trade Representative, Robert Lighthizer, noted that serious discussions finally began on core issues, with this round representing a positive step forward. With that said, no major decisions were made during this round, leaving plenty of work still ahead. Despite the cautiously optimistic tone that emerged, the latest round of negotiations doesn't materially change our view of the balance of risks related to NAFTA. The final outcome of negotiations remains an open question and, until resolved, the uncertainty will continue to weigh on businesses, particularly north of the border. The next round of talks is currently scheduled to take place late this month in Mexico, before wrapping up in Washington the following month.

All in all, the robust GDP data should be viewed as constructive by the Bank of Canada, largely confirming their Q4 growth estimate. But, despite the cautiously optimistic tone struck during the NAFTA negotiations, the outcome remains highly uncertain. As such, events this week have done little to move the needle as far as the interest rate path is concerned, with the next hike unlikely to take place until the July fixed announcement date – assuming the outlook continues to evolve as expected.

Canada: Upcoming Key Economic Releases

Canadian International Trade - December

Release Date: February 6, 2018

Previous Result: -$2.5bn

TD Forecast: -$2.0bn

Consensus: N/A

The international merchandise trade deficit is forecast to narrow to $2.0bn in November, reflecting a further recovery in non-energy exports. As presaged by US advance trade data, motor vehicle exports should provide the largest source of strength as production ramps up following plant shutdowns. Energy exports will be constrained by pipeline bottlenecks after a spill shutdown the Keystone pipeline for part of the month. Higher crude prices and increased rail shipments will provide a key offset to weaker pipeline volumes and as a result, nominal crude exports should be down more modestly on the month. On the other side of the spectrum, imports are likely to moderate from its previous jump, allowing for a narrowing in the deficit. We expect export volumes to reinforce an upbeat report.

Canadian Employment - January

Release Date: February 9, 2018

Previous Result: 65k, unemployment rate: 5.8%

TD Forecast: -12k, unemployment rate: 5.8%

Consensus: -2k, 5.8%

We expect some give back in jobs to finally materialize in January and forecast a net loss of 12k. The pullback is coming off a string of over 12 months of consecutive gains, which have averaged 64k in Q4. The minimum wage hike in Ontario, which was implemented on January 1, should lead to job losses totaling 90k over the mid-term. As a result, we expect Ontario to underperform in January and drive the net loss of jobs. Consistent with the slowdown in employment, we expect the unemployment rate to rise to 5.8%. Offsetting the weakness in jobs will be wage growth, where we anticipate a significant jump in average hourly earnings from the 22% increase in the Ontario minimum wage. We look for average hourly earnings of permanent employees, our preferred measure, to jump to 4% y/y from 2.9% y/y in December. So the LFS report should send mixed signals and markets could be grappling with weakness in jobs but a surge in wage growth on account of the Ontario minimum wage hike. Because we see wages as a lagging indicator relative to jobs, and because the monthly surge in wages will be largely driven by a one-off policy adjustment, we expect the Bank to be concerned by the underlying trends in the labour market and focus more on jobs this month.

Dollar Rebounds After Strong Jobs Report

US added 200,000 positions in January

The US dollar rose against major pairs on Friday. The release of the U.S. non farm payrolls (NFP) proved to be the much needed shot in the arm after the greenback was under pressure for most of 2018. The job gains were above expectations but more importantly the hourly wages came in higher, giving the Fed a potential green light to hike 3 or 4 times in 2018. The market is estimating a 77.5 percent probability of the first rate lift to come in March.

- The Reserve Bank of Australia (RBA) will publish its rate statement on February 5

- the Reserve Bank of New Zealand (RBNZ) will follow on February 7

- The Bank of England (BoE) will host a super Thursday on February 8

USD surged after wages rose more than expected

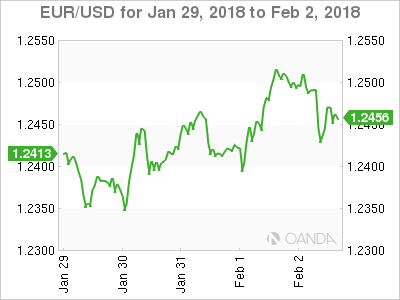

The EUR/USD gained 0.22 percent in the last five days. The single currency is trading at 1.2424. The USD was having a week to forget but a jobs week is not done until the U.S. non farm payrolls (NFP) report is released. The gain of 200,000 jobs in January was the boost the dollar needed after the Fed and the ADP did now sway the market. The USD reversed most of the losses of the week, gaining 0.43 percent against the EUR. The biggest boost came from the hourly wages growth at 0.3 percent for an annualized gain of 2.9 percent.

The disappointing December jobs report played a part as investors were estimating 180,000 positions and instead got pleasantly surprised by both strong gains and positive inflation signals. The move in the USD could be under threat next week as there are few economic released of note in the US and the political drama in Washington has not been beneficial to the greenback.

Fundamentals indicators and monetary policy has been supportive of the USD, but political uncertainty has hurt the dollar's status as a reserve currency. The upgraded growth expectations around the world have also shrunk the gap between the US and the rest of the world.

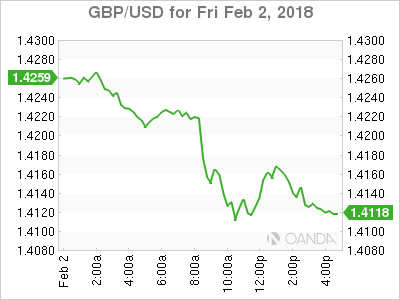

The GBP/USD lost 0.31 percent during the trading week. The currency pair is trading at 1.4120 ahead of the Bank of England (BoE) monetary policy meeting on Thursday, February 8 at 7:00 am EST. The central bank is not expected to change its benchmark rate but it could signal a hike sooner rather than later specially as expectations of a softer Brexit and economic growth has been encouraging. The BoE made its first rate rise in a decade back in November. The data released on Super Thursday, so called because of the sheer number of announcements, will guide the market and shape the monetary policy expectations going further into 2018.

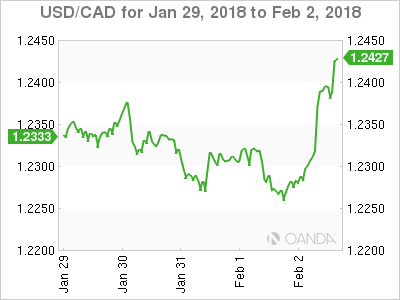

The USD/CAD gained o.86 percent during the week. The currency pair is trading at 1.2421. The USD appreciated against the loonie and put the Canadian currency at weekly lows. The greenback rose 1.22 versus the CAD on Friday after the release of the U.S. non farm payrolls (NFP). The U.S. Federal Reserve meeting and positive employment numbers earlier in the week did little for the USD, but with the release of the biggest indicator it all turned.

The economic data releases form Canada will start with on Tuesday, February 6 at 8:30 EST with publication of the trade balance. Later that same day the Ivey Purchasing Managers Index will be posted at 10:00 am EST. Employment data will be the highlight of the week on Friday, February 9 at 8:30 am with a 2,000 job loss report expected after the back to back gains of 70,000 positions in the previous months.

Market events to watch this week:

Monday, February 5

- 4:30am GBP Services PMI

- 10:00am USD ISM Non-Manufacturing PMI

- 7:30pm AUD Retail Sales m/m

- 7:30pm AUD Trade Balance

- 10:30pm AUD Cash Rate

- 10:30pm AUD RBA Rate Statement

Tuesday, February 6

- 8:30am CAD Trade Balance

- 4:45pm NZD Employment Change q/q

- NZD Unemployment Rate

Wednesday, February 7

- 10:30am USD Crude Oil Inventories

- 3:00pm NZD Official Cash Rate

- 3:00pm NZD RBNZ Monetary Policy Statement

- 3:00pm RBNZ Rate Statement

- 4:00pm NZD RBNZ Press Conference

Thursday, February 8

- 4:00am AUD RBA Gov Lowe Speaks

- 7:00am GBP BOE Inflation Report

- 7:00am GBP MPC Official Bank Rate Votes

- 7:00am GBP Monetary Policy Summary

- 7:00am GBP Official Bank Rate

- 7:30pm AUD RBA Monetary Policy Statement

Friday, February 9

- 4:30am GBP Manufacturing Production m/m

- 8:30am CAD Employment Change

- 8:30am CAD Unemployment Rate

*All times EDT

Australia & New Zealand Weekly: RBA on hold, unlikely to signal material changes in thinking but could reinstate AUD...

Week beginning 5 February 2018

- RBA on hold, unlikely to signal material changes in thinking but could reinstate AUD warning.

- RBA: policy decision, Statement on Monetary Policy, RBA Governor Lowe speaking.

- Australia: retail sales Dec & Q4, trade balance, housing finance.

- NZ: RBNZ Monetary Policy Statement, labour force survey, labour cost index.

- UK: BoE policy decision.

- US: ISM non-manufacturing, and various Fed speakers.

- Key economic & financial forecasts.

Information contained in this report was current as at 2 February 2018.

RBA on hold, unlikely to signal material changes in thinking but could reinstate AUD warning

The Reserve Bank Board holds its first meeting for 2018 next week on February 6. We expect policy to remain unchanged.

The Bank often uses its first meeting of the year to re-frame the policy discussion with an overhaul of the wording in the Governor's statement accompanying the decision and the Statement on Monetary Policy (SoMP) released the following Friday providing an opportunity to present revised forecasts and a fuller elaboration of its views.

We do not expect to see a major shift this time around. The Bank will acknowledge the more positive tone from abroad and from some of the domestic data. It may also alter its commentary, particularly around the AUD. However, its central view from late last year - that "continuing spare capacity in the economy and the subdued outlook for inflation mean that there is not a strong case for a near-term adjustment in monetary policy" - is likely to remain in place.

There have been several notable developments since the RBA Board's December meeting:

- The global backdrop has again improved with robust momentum, tax cuts and supportive financial conditions in the US, China's growth coming in above expectations and the IMF upgrading its global outlook for 2018 and 2019. The Fed is now widely expected to raise rates 75bps this year but markets have taken the shifting view in their stride.

- Locally, the Q3 national accounts, released the day after the last Board meeting, showed growth still tracking below potential and a weak picture around the consumer (spending flat, savings up and incomes mixed at best).

- Labour markets have continued to show strong momentum, with 98k jobs added over Nov-Dec and a clearer lift coming through in the mining states. There is still considerable slack in the market though - the unemployment rate holding around 5.5%, well above the 5% mark regarded as 'full employment', and broader measures showing even more spare capacity once underemployment is included.

- Confidence has lifted, with consumer sentiment recovering from its Q3 'hole' and business surveys remaining buoyant. While a welcome improvement for the RBA, the lift in consumer sentiment is still not quite a break-out with the detail suggesting ongoing spending restraint. We expect next week's retail report - due the morning of the RBA meeting - to confirm a recovery Q4 but with sales growth still subdued.

- Inflation finished 2017 a touch softer than expected, the CPI rising 0.6% in Q4 to be up 1.9%yr. Core inflation also came in at 1.9%yr but tracked a 1.6% annual pace over the second half of the year.

- The AUD/USD cross has risen 5.5% since the RBA's December meeting to be back above the levels prevailing at the Board's August meeting. The move is mainly about the USD, with the AUD showing a much more muted 2.3% gain in TWI terms.

On balance, these shifts are unlikely to have a material impact on the RBA's medium term views. We expect the Bank to stick with the real GDP growth profile from its November SoMP: 2.5% for end 2017, lifting to and holding at 3.25% for end 2018 and end 2019. While some of the detail was soft, the September quarter GDP outcome (0.6%qtr for real GDP) was in line with the RBA's expectations as implied by the 2017 growth forecast. In addition, economic growth over the first half of 2017 was revised up, to 1.4% from 1.2%.

More generally, a slightly softer picture around consumer spending following the September quarter national accounts is balanced by a more supportive global backdrop, commodity price resilience, jobs growth, and upbeat private business surveys.

The technical assumptions underpinning the RBA's forecasts are unlikely to prompt shifts either. While the currency is higher against the US dollar, 80¢ currently vs 77¢ in the November SoMP, it is unchanged on a TWI basis, at 65 - and hence unlikely to be a reason to revise growth forecasts.

That said, the currency move is likely to see a shift in commentary. The Governor's statement following the December Board meeting included wording changes that indicated the Bank was less concerned about the AUD, noting simply that "the Australian dollar remains within the range that it has been in over the past few years". It may choose to reinstate the wording that had been in place previously: "An appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast."

On inflation, the Bank's broad view that it will remain around or slightly below the 2-3% target band throughout 2018 and 2019 is unlikely to change. The RBA may consider nudging its near term forecasts for underlying inflation up slightly. The November SoMP had underlying inflation at 1.75% in December 2017 and holding at this pace throughout 2018. This looked overly weak at the time (our forecasts were for underlying inflation to hold at 2%yr) and with the December 20107 quarter coming in at 1.9%yr to anticipate a near term slight step down now looks a little awkward. However, the Bank would emphasise any shift as being a minor rounding 'tweak' rather than a material change in view.

Aside from acknowledging the mostly positive developments since its December meeting, and restating its 'on hold' policy stance, we expect the Governor's decision statement, the SoMP commentary, as well as the speech by the Governor on Thursday to again highlight the main areas of concern for policy. These were set out clearly in Governor Lowe's ABE speech in late November, with the focus on three key issues:

- how the 'cross-cutting themes' of rising businesses confidence and a subdued consumer resolve;

- the degree to which an improving labour market will translate into a pick-up in wage growth and inflation; and

- how high and rising household debt levels will affect the stability of the economy over the medium term.

These questions will take longer to resolve, with the main focus on quarterly wage inflation and national accounts updates.

Most of the Bank's concerns centre on the Australian consumer. The Governor's speech also noted that "for a number of years consumption growth has been weaker than we had originally forecast" and that "it has not exceeded 3 per cent for quite a few years". With the RBA's upbeat growth forecasts relying on a lift in consumption to 3%, the Governor is rightly nervous about prospects for the consumer.

We continue to see a more challenging year ahead for the Australian consumer and another sub-par year for wider economic growth - a mix that means policy will remain firmly on hold. Westpac expects rates to remain unchanged throughout 2018 and 2019.

The week that was

Inflation and housing have been the focus for Australia this week. Offshore, President Trump and the FOMC stole the limelight, but a timely update on Chinese growth was also delivered.

The December quarter CPI report for Australia carried a high degree of importance given the market was close to fully pricing a RBA rate hike before year end. An upside surprise on core inflation would have cemented this expectation, but in the event, both core and headline inflation disappointed. The headline CPI rose 0.6% in Q4, with half of the gain coming from higher tobacco prices and the remainder fuel. There was little momentum elsewhere, the other CPI components netting out against each other. Stripping out outsized movements, core inflation rose 0.4% for a second consecutive quarter, leaving annualised core inflation at just 1.6%yr. Looking ahead, the disinflationary pulse from competition in the consumer sector and housing are expected to persist, and the recent rise in the Australian dollar will also act as a headwind. The net effect is that core inflation will remain at or below the bottom of the RBA's target band of 2.0%yr through 2018 (and 2019). This will see market expectations for a rate hike pushed further out from early 2019 currently. We remain of the view that the RBA will be on hold through 2018 and 2019.

Like inflation, the housing market is also unlikely to justify tighter policy anytime soon. The latest price data from CoreLogic suggests home prices fell a further 0.5% in January to be down 1.0% since October (but still up 3.2% over the year). There remains a material disparity between price growth in Sydney and Melbourne, respectively 1.3%yr and 8.0%yr in January (from 7.7%yr and 11.0%yr three months ago). Elsewhere, annual growth of near 2.0%yr is occurring in Adelaide and Brisbane, while price declines in Perth are tracking around 2.5%yr. Whereas the price deceleration was initially concentrated in houses, it is now spreading to units as supply ramps up. An unfolding slowdown in housing credit and caution amongst households towards the sector indicate price growth is unlikely to accelerate meaningfully in 2018.

While projects nearing completion will continue to add to supply, a renewed downtrend in dwelling approvals suggests that the flow of new supply will taper. Having surged 13% in November, total approvals slumped 20% in December to be 5.5% lower over the year. This monthly volatility was driven by high-rise approvals, particularly in Victoria. Site purchase data suggests this high-rise downtrend has further to run. Non high-rise approvals are also down 3.5%yr on a trend basis. Looking through recent volatility, our expectation that dwelling investment will subtract from growth in 2018 and 2019 has a firm foundation.

Moving offshore, the US was the market's focus this week as debate over the stance of policy and US dollar weakness raged on. In his first State of the Union address, President Trump called for greater investment in the US economy (a mooted $1.5trn infrastructure spending plan, primarily funded by state and local governments and the private sector), but this was paired with further protectionist and geopolitical rhetoric. The net effect for the US dollar and interest rates was negligible. Markets are likely to leave both issues to the side until concrete detail is provided. In the meantime, anxiety over another potential government shutdown next week and the debt ceiling debate will continue to weigh on the currency. On rates however, the FOMC's more confident tone at their January meeting was enough to cement expectations of a March rate hike.

Further out, the market is close to pricing in our own view, that a further two hikes will be delivered by September to take the mid-point of the fed funds range to 2.125%. Come the December quarter, the Committee will have to be more aware of the potential consequences of balance sheet reduction on financial conditions - in addition to the effect of the three rate hikes. The main consequence for Australia is likely to be that our currency will depreciate from the current level around USD0.80 to USD0.72 at end-2018. However, a repricing of rate expectations outside the US based on the FOMC's progress and renewed financial market volatility are risks to watch out for.

Finally, while it received little attention, China's official PMI update provided an important insight into the economy's momentum as 2018 began. On the whole, activity in the manufacturing and services sectors remains robust. But there is clear evidence that it is slowing, most notably due to weaker external demand (i.e. exports). A much reduced contribution from net exports will be a key reason why 2018 growth will slow to around 6.2% from 6.9% in 2017; weaker growth in investment will also be behind this softening. In contrast, consumer demand should hold up, unless we see a further deterioration in employment conditions.

New Zealand: week ahead & data wrap

The past week has been fairly quiet, but next week will be huge with a labour market update from Stats NZ, a dairy auction, and a Reserve Bank Monetary Policy Statement on the calendar.

The economy lost momentum over 2017, with GDP growth slowing and business confidence tanking. But this growth slowdown has not yet affected the labour market. The unemployment rate has fallen steadily over the past year. Job advertisements, benefit numbers and business opinion surveys have all continued to improve steadily, and firms are now reporting the greatest difficulty finding labour since 2005. Given these indicators, we expect next week's Household Labour Force survey to report that unemployment fell from 4.6% to 4.5% in December 2017.

Although the labour market is unambiguously firm, we expect data volatility will lead to a weak - looking employment number this quarter. In September, employment rose a whopping 2.2%, and the labour force participation rate experienced a matching jump. This was incongruous with other data and may have partly reflected sampling error. We've assumed some pullback in the participation rate, and a relatively small 0.2% rise in employment for the December quarter.

After several years of falling unemployment, one could be forgiven for wondering whether wage growth is about to accelerate. There are no signs that wage growth did accelerate in the December quarter - we expect the Labour Cost Index will register another 0.4% quarterly rise in private sector salaries and wages. What happens to wage growth in 2018 is a more open question, but in our view it will accelerate only slightly. We expect the economy to continue losing momentum, which could stall or reverse the trend of falling unemployment, and forestall any significant market pressure for rising wages. Wage increases are more likely to come about via government policies that tip the balance of power more towards workers, such as changes to employment laws, higher minimum wages and a shift towards collective agreements.

The Reserve Bank will watch the labour data with interest, given the Government's plans to include employment as well as price stability in the Reserve Bank's monetary policy goals. This probably wouldn't have made much difference to the RBNZ's actions in years past - employment and inflation both argued for keeping interest rates low. But with the unemployment rate now around neutral and inflation below target, there is more scope for conflict between the two mandates. That said, the RBNZ won't be able to take this quarter's labour data into account for its Monetary Policy Statement, which is due the following day.

We are expecting very much a steady - as - she - goes MPS. We anticipate no material change from the RBNZ's previous OCR forecasts, and no change to the policy guidance paragraph, which for a year now has remained more - or - less unchanged:

"Monetary policy will remain accommodative for a considerable period. Numerous uncertainties remain and policy may need to adjust accordingly".

The RBNZ's press release, and the detail of the Monetary Policy Statement, will no doubt allude to the key developments and surprises since November, of which we count five:

Inflation was substantially lower than forecast in December 2017. The exchange rate has risen unexpectedly. The RBNZ may return to its previous rhetoric that "a lower exchange rate is needed," which could cause the exchange rate to fall on the day.

The housing market has a new lease of life, which will reinforce the RBNZ's apprehension about keeping interest rates too low for too long.

Revisions to historical GDP data from Stats NZ have shown that the economy grew more over 2015 and 2016 than previously estimated. This implies that the output gap is higher and the economy is closer to experiencing inflation pressure than previously thought.

Global economic data has been strong and global equity prices have risen rapidly. This will rate a mention from the RBNZ, but probably won't affect their overall assessment much.

Some of these developments are positive for inflation and others are negative, but we judge the overall balance to be roughly neutral from the RBNZ's perspective.

We have long argued that the RBNZ's forecasts of GDP growth, house prices and inflation are too high. The Government may be planning something of a fiscal boost to the economy, but it also plans a range of measures specifically designed to cool the housing market and slow net migration. We think these measures will have a more marked effect on house prices than the RBNZ anticipates, and a slower housing market would, in turn, impact GDP growth. Moreover, the recent sharp decline in business confidence portends weaker GDP growth in the short run. Hence our GDP forecast is markedly lower than the RBNZ's previously published forecasts. Slower GDP growth naturally leads us to fret less about inflation accelerating. But there is another leg to our lower inflation view. A range of factors, including new technology, have also been supressing inflation for years, and we expect this trend will continue - we doubt that inflation would accelerate in the fashion the RBNZ expects, even if GDP growth did accelerate.

Our low - inflation view leads us to expect that any OCR hike will be delayed until late - 2019 (and we have even occasionally warned that there is still a chance of further OCR cuts). Our view stands in stark contrast to financial markets, where pricing is consistent with the OCR rising in late - 2018 or early - 2019. We doubt that market pricing will shift following the Reserve Bank's statement, but we do expect market pricing for OCR hikes to drift later over the course of this year.

Data Previews

Aus Dec retail trade

Feb 6, Last: 1.2%, WBC f/c: - 0.3%

Mkt f/c: -0.2%, Range: -1.2% to 0.4%

- Retail sales surged 1.2% in Nov, a surprisingly strong result that was the biggest monthly gain since Feb 2013. The ABS cited the launch of Apple's iPhone X and the increased popularity of 'Black Friday' sales as major factors with electrical and electronic goods retailers recording a 9.3%mth surge and sales for 'other retail n.e.c', which includes non store retailers, up 3.9%mth. Sales excluding these two sub-categories were up a milder 0.4%mth.

- While there were clearly extenuating circumstances in Nov, 'underlying' sales look to have recovered somewhat from the weakness in Q3 with consumer sentiment improving steadily through Oct-Jan. That said, family finances are still under pressure with spending intentions subdued and private sector business surveys indicating retailers continued to struggle with soft conditions in Dec. On balance we expect sales to retrace 0.3% in Dec as one-off factors drop out but leaving a modest gain over the last 3mths.

Aus Q4 real retail sales

Feb 6, Last: 0.1%, WBC f/c: 0.6%

Mkt f/c: 1.0%, Range: -1.4% to 1.2%

- Retail volumes stalled in Q3, rising just 0.1% vs a 1.5% gain in Q2, a weather-affected 0.2% gain in Q1 and a 0.9% gain in Q4. The quarterly profile is choppy but has been tracking a weak underlying trend.

- The Q4 update will show a significant improvement. Even with a pull back in the Dec month, nominal sales are on track to be up over 1% for the quarter. The Q4 CPI detail showed mixed results for retail prices. Intense competition saw increased discounting in categories such as household contents and clothing. However, food, which makes up over 40% of retail sales, posted a stronger than expected 1% rise in the quarter vs a 0.9% fall in Q3. The mix suggests about half of the gain in nominal sales in Q4 is due to prices. We expect real retail sales to be up 0.6% for the quarter. With price moves mixed across categories, there is some upside risk to the quarter particularly if spending patterns have responded to relative price shifts.

Aus Dec trade balance, AUDbn

Feb 6, Last: - 0.6, WBC f/c: 0.7

Mkt f/c: 0.2, Range: -0.9 to 0.7

- Australia's trade balance slipped into deficit in October and November on a dip in exports.

- For December, we anticipate a return to surplus, a forecast $0.7bn, a $1.3bn turnaround on November, led by a rebound in exports.

- Export earnings in December increased by a forecast 4.5%, $1.4bn, centred on iron ore, coal and LNG, reflecting a rebound in volumes and higher prices.

- Imports are expected to edge higher, 0.4% (+$0.1bn), on rising volumes. Prices are likely little changed, with the currency consolidating in the month, so too global energy prices.

Aus RBA policy decision

Feb 6, Last: 1.50%, WBC f/c: 1.50%

Mkt f/c: 1.50%, Range: 1.50% to 1.50%

- The RBA left interest rates unchanged throughout calendar 2017, Governor Lowe noting in his final speech of the year that: "the continuing spare capacity in the economy and the subdued outlook for inflation mean that there is not a strong case for a near-term adjustment in monetary policy".

- We expect the RBA to leave rates unchanged at its Feb meeting. Developments over the summer hiatus have been mixed with the Q3 national accounts disappointing but more positive news around global conditions, labour markets and confidence. Inflation remains subdued, with latest figures showing core inflation running at a 1.6% annual pace over the second half of 2017. There is also no new information around the Bank's key areas of uncertainty - the impact of lacklustre consumer demand; the extent to which weak labour income growth continues; and the risks around household debt. We expect consumer weakness to persist in 2018, leading the RBA to again leave rates on hold all year.

Aus Dec housing finance (no.)

Feb 9, Last: 2.1%, WBC f/c: - 1.5%

Mkt f/c: -1.0%, Range: -1.9% to 0.5%

- Finance approvals have held up much better than expected through 2017, the most recent figures showing a 2.1% rise in the number of new owner occupier loans in Nov and a 1.5% rise in the value of investor loans. The latter are down - 8.3%yr but the total value of finance approvals is up 4%yr despite auction activity, turnover and price growth all showing a material slowdown in the major eastern markets.

- Industry figures point to a softer month for owner occupier approvals some - Dec is expected to show a 1.5% decline. However, the general picture is still better than might have been expected given macro-prudential measures and a similar sized slowdown in 2015, which saw the total value of loans fall 13% peak to trough. It may indicate that weaker foreign buyer demand had a bigger hand in the 2017 slowdown.

NZ Q4 Household Labour Force Survey

Feb 7, Employment last: 2.2%, WBC f/c: 0.2%, Mkt f/c: 0.3%

Unemployment last: 4.6%, WBC f/c: 4.5%, Mkt f/c: 4.7%

- We expect a small decline in the unemployment rate from 4.6% to 4.5%, which would be a new nine - year low. Job advertisements, benefit numbers and business opinion surveys all point to steady rather than rapid improvement in the jobs market over the quarter.

- Both employment and labour force participation have been very volatile recently. We expect some payback from their sharp gains in the September quarter, without affecting the broader picture of a stronger jobs market.

- The employment figures will undoubtedly come under more scrutiny this year, with diminishing slack in the labour market and a new Government focused on tipping the balance of power more towards workers.

NZ Q4 Labour Cost Index

Feb 7, Private sector Last: 0.7%, WBC f/c: 0.4%, Mkt f/c: 0.5%

- We expect a 0.4% rise in the private sector Labour Cost Index for the December quarter. Wage growth has been running at the same quarterly pace for the last couple of years, aside from the 0.7% rise last quarter, which included the equal pay settlement for aged and disability care workers.

- We have no evidence to suggest there was a stirring of wage pressures in the December quarter. Indeed, the latest Westpac - McDermott Miller employment confidence survey found fewer workers reporting a rise in earnings over the last year.

- The Quarterly Employment Survey (QES) suggests a stronger rate of growth in hourly earnings. However, this measure is affected by changes in the composition of jobs.

NZ RBNZ Monetary Policy Statement

Feb 8, Last: 1.75%, Market: 1.75%, Westpac 1.75%

- We expect the RBNZ to continue with its firmly neutral OCR outlook and repeat its long - held guidance that "Monetary policy will remain accommodative for a considerable period".

- Recent developments have been roughly neutral, with low inflation and the high exchange rate counterbalanced by a resurgent housing market and upwardly revised GDP.

- Foreign exchange markets may react to any comment about the exchange rate being too high, but interest rate markets are unlikely to be perturbed by a steady - as - she - goes MPS.

UK Bank of England Bank Rate decision

Feb 8, Last: 0.5%, Mkt: 0.5%, WBC f/c: 0.5%

- Inflation is sitting at the top of the BOE's target band and while growth remains sluggish, spare capacity has been eroded and there are positive signs in parts of the economy. Against this back drop, BOE Governor Carney recently noted that "we've moved into a more conventional area for monetary policy where the focus is increasingly on returning inflation sustainably to target over an appropriate horizon."

- We expect the BOE will keep the Bank Rate on hold at 0.5% at its February meeting. In addition, the BOE is expected to maintain the very gradual tightening bias it adopted late last year, when it noted that some modest interest rate increases were likely over the next few years. The Governor's recent comments suggest some risk that the MPC strengthens its rhetoric around the rates outlook. However, given the lingering downside risks for activity stemming from Brexit, we continue to see the risk that any tightening comes later, rather than sooner.

Week Ahead – BoE, RBA and RBNZ Meet: Will FX Moves Influence Monetary Policy after Strong Rally?

Central bank meetings will dominate next week's economic calendar as the Bank of England, the Reserve Bank of Australia and the Reserve Bank of New Zealand meet to set monetary policy. All three are expected to stand pat but surprises could be in store for the markets as policymakers adjust their outlook following recent developments pertaining to their economies and in forex markets. Economic data will not go amiss with most countries releasing monthly figures on trade and services PMIs.

Soaring aussie and kiwi a concern for the RBA and the RBNZ

Weaker-than-expected inflation in Australia and New Zealand has kept the RBA and the RBNZ on hold even as growth has remained solid and the labour market has been improving in both countries. Fourth quarter inflation numbers released last month showed Australian CPI rising by less than anticipated and missing the RBA's 2-3% target band for the third straight quarter, and in New Zealand, the annual rate unexpectedly fell by 0.3 percentage points.

And while growth in the two Asian-Pacific economies has picked up some steam, a sharp appreciation in the exchange rate threatens to depress growth and dampen already subdued inflationary pressures. The aussie gained just over 8% versus its US counterpart in 2017 and is up a further 2.5% so far in 2018. The kiwi rose by a more modest 2% last year but has rallied almost 4% in January.

Both the RBA and RBNZ could toughen their language on the exchange rate in their upcoming meetings on February 6 (Tuesday) and 8 (Thursday) respectively. However, investors are likely to ignore such comments if the central banks also raise their outlooks on the economy as this would bring forward expectations about the timing of a rate increase. Based on recent data, the RBNZ is more likely to strike an upbeat tone, while the RBA could sound more cautious.

Aussie traders should be braced for additional volatility on Tuesday as Australian retail sales and trade figures will be published ahead of the RBA announcement. Moreover, the RBA will publish its quarterly Monetary Policy Statement on Friday, giving a more detailed insight into the Bank's updated economic projections. In New Zealand, fourth quarter employment data due on Wednesday will provide traders with the final clue as to what to expect from the RBNZ the following day.

Loonie eyes Canadian jobs report

Concerns about NAFTA drove the Canadian dollar to retrace half of its gains in 2017 that were made on the back of the Bank of Canada joining the rate hike bandwagon. But the loonie is once again heading higher and this week hit a 4-month top of C$1.2246 to the US dollar. A stronger-than-anticipated employment report on Friday could help the Canadian dollar target the C$1.20 level again. Also to watch out of Canada in the coming week are trade figures and the Ivey PMI on Tuesday.

China releases trade and inflation numbers

With risk aversion making its first appearance of 2018 this week, markets could be sensitive to economic indicators out of China in the next seven days. Trade data on Thursday will be watched to see how China's exports and imports fared in January. Inflation figures will follow on Friday, which will include both the consumer and producer price indices for January. The yuan touched a 2½-year high of 6.2677 per dollar this week, with the PBOC seemingly at ease with a stronger currency, even though China's economy appears to be heading for softer growth this year. Strong numbers next week would reinforce the view that China is only headed for a mild slowdown.

Quiet week for the US and the Eurozone

It will be a quieter seven days for the US and the Eurozone with only a handful of major data releases. In the US, the highlight will be the ISM non-manufacturing PMI due on Monday. The closely watched indicator of services activity in the United States is expected to improve to 56.3 in January, from 56.0 in the prior month. December trade figures and the JOLTS job openings could also attract some attention on Tuesday.

Looking at the European calendar, business surveys will start the week on Monday, which will include the Eurozone final services PMI readings for January, as well as December retail sales and the sentix index for February. However, industrial output and trade data out of Germany and France are likely to prove more exciting for traders. German industrial production data is due on Wednesday, followed by the trade numbers on Thursday. The French trade figures will be published on Wednesday, with the industrial output number coming out on Friday. The data are unlikely to give the euro much direction, which could be headed for another week of consolidation versus the greenback.

Will Bank of England flag a rate hike?

The Bank of England is widely expected to hold interest rates unchanged at 0.5% when it convenes on Wednesday and Thursday, but the meeting could still be an eventful one as the Bank will also publish its quarterly inflation report on Thursday and will be followed by a press conference with the Governor Mark Carney. Markets may have already gotten a glimpse as to what to expected from Carney from his testimony before Parliament's Economic Affairs Committee earlier this week. Carney said "the focus is increasingly on returning inflation sustainably to target over an appropriate horizon". This perhaps is a signal that rates may need to be raised sooner, possibly in May or August, than the current market forecasts of November.

The pound gained on the back of Carney's remarks, climbing back above $1.42. A not-so-hawkish than expected BoE could send sterling below $1.40 but UK data also poses a risk. The January services PMI is due on Monday. Given that services accounts for 80% of UK GDP, it will be important to see how the sector performed at the start of the year. The index is forecast to moderate by 0.2 to 54.0 in January. Other data will include industrial and manufacturing output figures on Friday, alongside the trade balance, all for December.

Weekly Focus: Politics and Central Banks in Focus

Market movers ahead

- Next week is set to be fairly quiet in terms of data releases and more focus will be put on speeches/political events.

- In the Fed, we believe the speech by William Dudley (the second most important person on the FOMC now) is likely to be the most interesting, with his reflections following the FOMC becoming more confident on the economic outlook.

- In the euro area, new developments on the German coalition talks are the main event. The parties have set themselves a deadline of 4 February to wrap up the coalition negotiations.

- In the UK, the most important event is the Bank of England meeting on Thursday, including an updated Inflation Report and a press conference.

Global macro and market themes

- Belief in reflation has fuelled central bank 'normalisation' pricing but is it too early?

- It may be but central banks are set to move slowly on rates in any case. The Bank of Japan, SNB and Riksbank are particularly wary about not throwing the 'baby out with the bath water' in this context.

- Movements in both the level and slope of yield curves plus hedging costs are key to understanding cross-border capital flows as 'normalisation' unfolds.

- EU fixed income may become increasingly attractive relative to US fixed income and eventually lure capital back to Europe. In our view, EUR support will follow.

Sunset Market Commentary

Markets

Global core bond trading was confined to narrow sideways ranges ahead of the US payrolls amid an empty EMU eco calendar. The core bond sell-off continued after a strong US payrolls report with strong wage growth popping out. It adds to recent confidence that inflation will be upwardly bound during 2018. Market-based inflation expectations reached multi-year highs while the Fed (but also the ECB) embraced positive growth and inflation dynamics in their recent policy statements. Ultra-dovish Fed member Kashkari (who voted against last year's rate hike) admitted after the labour market report that if wage growth continues, it may effect Fed hikes this year. The US yield curve bear steepens at the time of writing with yields 0.9 bps (2-yr) to 3.8 bps (10-yr) higher. The German yield curve shifts in similar fashion with yields 0.1 bp (2-yr) to 3 bps (10-yr) higher. 10-yr yield spread changes versus Germany range between -1 bp and +2 bps with Greece outperforming (-7 bps).

The dollar continued trading weak in the run-up to the US payrolls, but the trade-weighted dollar didn't set a new cycle low anymore. EUR/USD hovered around the 1.25 pivot. The yen lost its safe haven appeal and didn't profit from the correction of European equities. The BOJ's commitment to keep an easy policy and the rise in core (US and EMU) yields are preventing a yen rebound. US payrolls were strong (200k net job growth) and wage growth accelerated substantially to 2.9% Y/Y (vs 2.6% expected). The report triggered a further rise in US yields. USD/JPY spiked north of 110. The dollar gained modest ground against the euro. EUR/USD trades in the 1.2450 area. The move remains unconvincing from an USD point of view. Topside resistance (1.2537/98) stays within reach.

Sterling underperformed the euro and the dollar today. EUR/GBP trading is still confined to tight ranges, but the 0.8690 range bottom looked solid of late. The pair did build on yesterday's rebound from the start of European trading. The UK construction PMI was substantially weaker than expected at 50.2 (52.0) expected. The release was in line with the intraday momentum, but there was no acceleration of GBP losses after the release. Comments from UK trade Secretary Fox that the UK must not enter a new customs union didn't help sterling. The pick-up in global volatility was a tentative negative for sterling, too. Sterling lost further ground after the US payrolls release. Cable is losing more than a full big figure (at 1.4150). EUR/GBP is again nearing the 0.88 area.

European equity indices are losing about 1.0% as the rise in core yields and the strong euro are weighing. US equity markets are also under pressure, opening with losses of 0.5% to 1.0%. The Dow underperforms.

News Headlines

The US labour market remained in very good shape in January. The US economy added an additional 200 000 jobs, beating the consensus by 20 000. The unemployment rate was stable at 4.1%, the lowest level since 2000. Wage growth also beat expectations rising 0.3% M/M and 2.9% Y/Y. The Y/Y AHE growth was the highest since 2009.

The UK must not enter into a new customs union with the EU after it leaves the bloc, Trade Secretary Liam Fox said, setting a new red line for Theresa May's negotiations with Brussels and her own party on Brexit.

Growth in Britain's construction sector came almost to halt in January. The construction PMI fell to 50.2 in January from 52. The consensus estimate was 52.0. Uncertainty on Brexit caused new orders to dry up according the survey.

ECB's Coeure urged European governments to push ahead with plans to strengthen the monetary union to avoid stretching his institution's mandate in the next crisis. "To assume that the current economic expansion will heal all wounds is naive. The euro area needs reform." he said in a speech in Slovenia.

US: Jobs, Wages and Hours Improve: Fed on Path to Raise Rates

January's solid gain for jobs and wages supports household incomes and thereby consumer spending. The trend improvement in aggregate hours indicates more production and 2.5-3 percent GDP growth in 2018.

January Jobs at 200,000: Solid Sign for Income and Growth

Nonfarm payrolls rose 200,000 in January with the three-month average at a solid 192,000 jobs. Job gains are consistent with 2.5-3.0 percent economic growth in the first half of 2018, with steady consumer spending, better business investment and a likely FOMC March rate hike with another one in Q2-2018. The diffusion index indicates that 63 percent of industries added jobs in January compared to 52 percent a year ago.

Jobs gains appeared in many sectors including business services, trade & transport as well as education & health (top graph). Only information services jobs have declined in each of the past three months due to drops in jobs in telecommunications and motion pictures.

Over the past three months, aggregate hours worked are up, consistent with continued growth in personal income, personal consumption and overall GDP growth.

Wages: A Micro Model on Inflation and Productivity

Nominal average hourly earnings rose 0.3 percent in January and are up 2.9 percent over the year. While job growth remains strong, the gradual rise in earnings over the past six months signals higher incomes but also pressure on profits as firms have modest top-line pricing power (especially in the goods sector).

Longer term, the subdued inflation readings and weak productivity numbers have limited the gains in nominal wage growth (middle graph). Lackluster productivity growth in the current cycle has weighed on wage growth and will likely continue to hamper wage appreciation. Moreover, inflation has been persistently below the FOMC's target of 2 percent and has struggled to sustain upward momentum. With both productivity growth and inflation continuing to prove sluggish, it is not altogether surprising that wage growth has disappointed given the performance of the fundamentals.

Achieving Higher Economic Growth: Need Participation

Quarterly annualized GDP growth rates of 3 percent are not out of the question; however, sustained growth of 3 percent should largely be written off if the labor force participation rate does not improve. Structural issues continue to hold back growth in this metric. While the labor force participation rate for men is higher than for women, growth in the prime age participation rate during this expansion has been led by women. The overall labor force participation rate peaked in the early 2000s and trended sharply downward until 2016, where it has been relatively stable at just under 63 percent.

The unemployment rate held steady at 4.1 percent, its fourth consecutive month at this rate. We expect the unemployment rate to decline as employment growth outpaces growth in the labor force.