Sample Category Title

Dollar Rises after Solid NFP, Reversing against Yen, But Unsure about Europeans

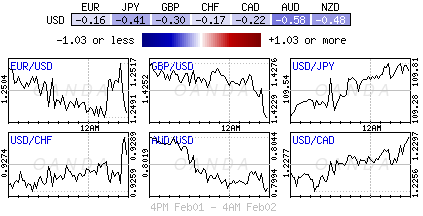

Dollar jumps in early US session after another set of solid employment data. Non-farm payrolls report shows 200k growth in January, above expectation of 180k. Prior month's figure was revised up by 12k to 160k. Unemployment rate was unchanged at 4.1% as expected. Average hourly earnings also grew 0.3% mom, in line with consensus. The recovery in greenback is broad based. But we'd like to point out that firstly, USD/JPY's break of 110.18 resistance is now seen as a sign of near term reversal. AUD/USD has topped out earlier this week and the post NFP decline also affirms the case of near term reversal. However, against European majors, Dollar is just in staying in range and the rebound might just be part of consolidation patterns.

UK PMI construction indicated a difficult start to 2018

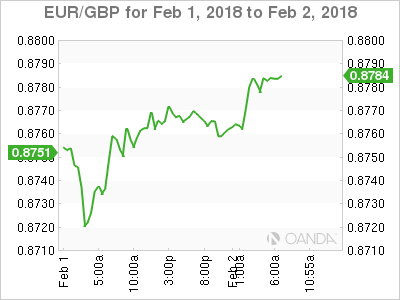

UK construction PMI dropped to 50.2 in January, down from 52.2 and missed expectation of 52.0. Markit noted in the release that "January's PMI data indicated a difficult start to 2018 for the UK's construction sector, underlined by business activity growth slumping to a four-month low and new orders sliding back into decline." Also, "a contraction in house building added to lackluster commercial building and civil engineering markets, and reduced inflows of new work suggest overall activity could slip into decline in February." And further more, "cost pressures remained intense, fuelled by shortages of input materials and high costs for imported products."

ECB Coeure: The euro area needs reform

ECB Executive Board member Benoit Coeure warned today that "to assume that the current economic expansion will heal all wounds is naive. The euro area needs reform." He pointed out that the next financial crisis could force ECB interest rates "much deeper into negative territory" or "require purchases of assets that are riskier than public or corporate debt", or " it may draw us dangerously close to monetary financing of governments." He suggested greater integration in services and in financial markets, and a more complete banking union.

Released from Eurozone, PPI rose 0.2% mom, 2.2% yoy in December.

Nomination for BoJ Governor might be revealed mid-to-late February

In Japan, it's reported that the government will likely announce the nominations of next BoJ Governor and Deputy Governors around mid-to-late February. At this point, it's still believed that current Governor Haruhiko Kuroda is the front runner, given the praises by Prime Minister Shinzo Abe and his officials. However, it's far from being certain. From the government's point of view, the choices could be indifferent if the next Governor will be persistent enough in following through with Abenomics.

BoJ conducted a special bond purchase operation today, offering to buy an "unlimited" amount of long-term JGBS. That's the first time in six months that such special operations were conducted. On the top of that, the purchase of 5- to 10- years JGBs was also raised from PY 410b to JPY 450b. It's seen by the markets as a pre-emptive move to fend off rise in JGB yields, which was taken higher by global counterparts in recent weeks.

Released from Japan, monetary base rose 9.7% yoy in January.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.07; (P) 109.41; (R1) 109.73; More...

USD/JPY's rebound from 108.27 extends higher today. Break of 110.18 support turned resistance is taken as the first sign of near term reversal. Intraday bias is turned back to the upside for 111.47 resistance first. Sustained break there will also have 55 day EMA (now at 11.39) firmly taken out. In such case, further rise would be seen back to 113.38/114.73 resistance zone. On the downside, however, below 109.22 minor support will turn focus back to 108.27 instead.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD/JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Dec | -9.60% | 10.80% | 9.60% | |

| 23:50 | JPY | Monetary Base Y/Y Jan | 9.70% | 11.00% | 11.20% | |

| 00:30 | AUD | PPI Q/Q Q4 | 0.60% | 0.40% | 0.20% | |

| 00:30 | AUD | PPI Y/Y Q4 | 1.70% | 1.20% | 1.60% | |

| 09:30 | GBP | Construction PMI Jan | 50.2 | 52 | 52.2 | |

| 10:00 | EUR | Eurozone PPI M/M Dec | 0.20% | 0.20% | 0.60% | |

| 10:00 | EUR | Eurozone PPI Y/Y Dec | 2.20% | 2.30% | 2.80% | |

| 13:30 | USD | Change in Non-farm Payrolls Jan | 200K | 180K | 148K | 160K |

| 13:30 | USD | Unemployment Rate Jan | 4.10% | 4.10% | 4.10% | |

| 13:30 | USD | Average Hourly Earnings M/M Jan | 0.30% | 0.30% | 0.30% | |

| 15:00 | USD | Factory Orders Dec | 0.90% | 1.30% | ||

| 15:00 | USD | U. of Mich. Sentiment Jan F | 95 | 94.4 |

Dollar Posts Gains ahead of NFP Report; European Stocks Tumble

Here are the latest developments in global markets:

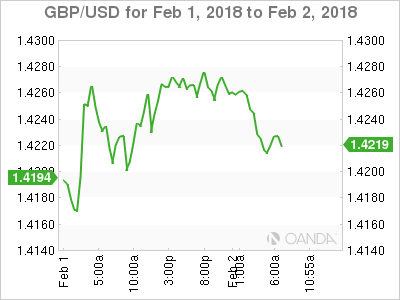

FOREX: The dollar continued to rise slowly against its major peers after US Treasury yields peaked at fresh highs early today but remained closed to 3-year lows. The dollar index inched up to an intra-day high of 88.88 (+0.16%) and dollar/yen was on track to break above 110, posting a fresh one-week high at 109.91 (+0.46%). Today's news that the BOJ was planning to buy an unlimited amount of Japanese government bonds also worked in favor of the greenback. Euro/dollar slipped to 1.2475 (-0.18%) and pound/dollar declined to 1.4229 (-0.34%) on the back of a stronger dollar, while weaker-than-expected readings on the British construction PMI and the Eurozone PPI also weighed on the two currencies. The antipodean currencies were the bigger losers as spreads between the local and US yields were falling. Aussie/dollar stretched downwards to 0.7975 (-0.63%) and kiwi/dollar retreated to 0.7141 (-0.61%).

STOCKS: A sharp loss in Deutsche Bank's shares dragged the pan-European STOXX 600 lower on Friday, with the index falling by 0.91% at 1100 GMT and being set to post its bigger weekly loss since August after a strong start to the year. The blue-chip Euro STOXX 50 dived by 1.01% and the German DAX 30 tumbled by 1.13%. The UK FTSE 100 was down by 0.28%, weighed by losses in telecommunication services. US stock futures were mixed.

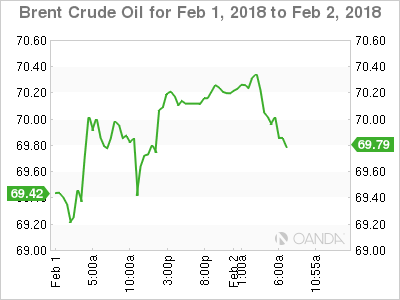

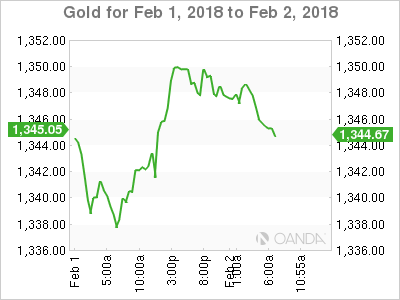

COMMODITIES: WTI crude oil was trading 0.10% up on the day at $65.88/barrel supported by OPEC-led supply cuts despite rising US production. Brent was down by an equivalent percentage at $69.58/barrel. Gold was last seen at $1345.40/ounce, down by 0.25% on the day.

Day ahead: NFP report said to show better results in January

US Nonfarm payrolls will take center stage during the day with the potential to shake the dollar which has been gaining against a basket of major currencies so far in the day.

Following Wednesday's upbeat APD employment report which tracks changes in the private sector, the government's comprehensive nonfarm payrolls due at 1330 GMT are expected to come higher at 180,00 new positions in January compared to 148,000 seen in December. Regarding the unemployment rate, this is anticipated to remain steady at a 17-year low of 4.1%. However, wage growth figures are expected to be of greater importance for the dollar as the Fed has been long concerned about subdued wages which probably are the reason why inflation is weak. Analysts believe that average hourly earnings have risen by 2.6% y/y in the twelve months to January compared 2.5% in the previous month, while on a monthly basis they project that the measure has continued to increase at the December's pace of 0.3%. Any upside surprise in the wage growth, though, would add optimism that the Fed's monetary policy is going in the right direction and hence justify any plans for further policy tightening this year. Note that private sector wages rose by 2.8% y/y in the fourth quarter, above the previous print of 2.6%, posting the highest increase since the first quarter of 2015.

In other data out of the US, December's factory orders and the University of Michigan's final readings on consumer sentiment for the month of January will also gather attention at 1500 GMT. Both measures are anticipated to show some improvement.

In energy markets, the US Baker Hughes oil rig count is due at 1800 GMT.

Public appearances today will involve comments by the Dallas Fed President Robert Kaplan – a non-voting FOMC member in 2018 – who will be participating in a Q&A session before the Teacher Retirement System of Texas Annual Conference at 1830 GMT. A few hours later, the San Francisco Fed President John Williams – a voting FOMC member in 2018 – will be talking about the US economy before the Financial Women of San Francisco at 2030 GMT.

Energy companies Chevron and Exxon Mobil and pharma firm Merck & Co. are among firms releasing quarterly results on Friday. All three will be releasing their reports before the US market open.

Canadian Dollar Lower, Investors Eye Nonfarm Payrolls, Wage Growth

The Canadian dollar is lower in the Friday session, erasing the gains seen on Thursday. Currently, the pair is trading at 1.2305, up 0.31% on the day. On the release front, the US will release key employment numbers, and the numbers could affect the movement of USD/CAD. Wage growth is expected to edge downwards to 0.2%. The markets are forecasting that nonfarm payrolls will jump to 181 thousand. The unemployment rate is expected to remain pegged at 4.1%. We'll also get a look at UoM Consumer Sentiment, which is expected to slow to 95.0 points. There are no Canadian releases to wrap up the week. On Thursday, Canadian Manufacturing PMI pointed to stronger expansion in January, climbing to 55.9 points. This marked the strongest reading since April 2017.

The sixth round of NAFTA talks ended in Montreal last week, with little progress to report. Negotiators are working against a self-imposed deadline to wrap up talks by March, with limited progress. Still, the sides are at least talking, and a Merrill Lynch report has lowered the odds of the United States leaving the pact to 25 percent. The US has demanded far-reaching concessions from Canada and Mexico, such as shifting more auto production to the US. Canada and Mexico are strongly opposed to the US demands, but both economies would take a sharp hit if NAFTA is terminated. At the same time, many US businesses don't want to blow up NAFTA and are pressuring President Trump to remain in the trade pact. The next round of negotiations is scheduled for late February in Mexico. Bank of Canada Governor Stephen Poloz recently noted that the uncertainty over NAFTA keeps him awake at night, and the Canadian dollar will likely remain under pressure while the negotiations continue.

There were no dramatic announcements from the Federal Reserve on Wednesday, and EUR/USD showed little movement in the Wednesday session. The Fed held the course on monetary policy, with the benchmark rate remaining between 1.25%-1.50%. In the rate statement, policymakers said that they expected the economy to continue to expand at a moderate pace and that the labor market would remain strong in 2018. What was more noteworthy was that the Fed predicted that inflation would rise to the Fed's 2 percent target this year. This marks an upgrade in the inflation forecast, as the December statement said that inflation was expected to "remain somewhat below 2 percent." Higher inflation is likely to open the door to tighter monetary policy, and the Fed appears on track for three, or even four rate hikes in 2018, assuming that the US economy remains strong. This policy meeting was the last under Janet Yellen, as Jerome Powell will take over as Fed chair on February 3. The slightly hawkish tone of the rate statement has raised the odds of a rate hike to 83% when the Fed next meets in March.

USDJPY: Recovers Further Higher, Bullish

USDJPY: The pair now threatens to recover further higher as it continues to hold on to its recovery. On the downside, support lies at the 109.50 level where a break if seen will aim at the 109.00 level. A cut through here will turn focus to the 108.50 level and possibly lower towards the 108.00 level. On the upside, resistance resides at the 110.50 level. Further out, we envisage a possible move towards the 111.00 level. Further out, resistance resides at the 111.50 level with a turn above here aiming at the 112.00 level. On the whole, USDJPY faces further corrective upside pressure.

EURUSD Bulls in Control Above Key Trendline

The euro is likely to see further buying interest against the U.S dollar while trading above the pairs key monthly trendline, found at the 1.2470 region. The EURUSD retains a strong bullish bias heading into today's Nonfarm Payrolls Job Report, with buyers looking towards the multi-year price-high set last month at the 1.2538 level. Looking to the downside, only a higher-time-frame price-close below the 1.2385 level can negate the pairs medium-term bullish outlook.

The EURUSD pair retains a strong bullish above the 1.2470 level, further upside towards 1.2538, 1.2600 and 1.2640 appears possible.

Should the EURUSD pair fall move below the 1.2432 level today, sellers will likely try to test towards the key 1.2385 support level.

USDJPY Bullish Headed into NFP Job Report

The U.S dollar retains a short-term bullish bias against the Japanese yen currency heading into this afternoons Non-Farm Payrolls job report, although the overall downtrend in the pair still prevails. The USDJPY pair continues to set new daily higher high's, with buyers maintaining the price-action above the 109.20 area on pullbacks. Today's job report from the United States economy should set the intraday directional bias, with the U.S dollar index also likely to place some role in the USDJPY price movements.

The USDJPY pair retains an intraday bullish bias while price trades above the 109.44 level, upside targets remain 110.18,110.58 and 110.88.

If the USDJPY pair falls below the 109.44 level, strong daily support is found at the 108.98 and 108.58 levels.

Deutsche Bank Sell-Off Sends CAC Lower

The CAC index has posted losses in the Friday session. Currently, the index is at 5385.25, down 1.27% on the day. A sharp loss in Deutsche Bank shares has dragged European stock markets lower. On the release front, there is just one event out of the eurozone. The Producer Price Index edged lower to 0.2%, missing the estimate of 0.4%. Later in the day, the US releases nonfarm payrolls, which is expected to improve to 181 thousand.

European stock markets are in the red on Friday, reacting to dismal news form Deutsche Bank, the largest bank in Germany. Shares of the giant German bank are currently down 5.5% on the day, and the stock price hits at its lowest level since November. The giant bank posted its third straight annual loss in 2017. The fourth quarter was weak, with a decline in investment bank revenue and the US tax reform bill weighing on share price. The banking sector is under pressure, with BNP Paribas and Credit Agricole showing daily losses of 1.01% and 1.08%, respectively. All listings on the CAC are in red territory and all but one are currently listed as a "strong sell", so the CAC could continue to lose ground during the day.

The ECB recently extended its asset-purchase program (QE) in September, but what happens after that? With the eurozone economy continuing to perform well, there has been speculation that the ECB could simply wind up QE and shift to a normative policy, and perhaps raise interest rates. However, Mario Draghi and other ECB members have taken pains to reiterate that the Bank is in no rush to end monthly asset purchases. On Wednesday, executive board member Benoit Coeure joined the chorus, saying that although QE "will not last forever" policymakers were in agreement "that we have to be patient and prudent because we are not yet where we want to be in terms of inflation". Investors would be well advised to keep a close eye on eurozone and German inflation numbers, as QE could be extended beyond September if inflation remains well below the ECB target of around 2.0%.

What To Look For In U.S Payrolls (NFP)

Friday February 2: Five things the markets are talking about

The U.S labor department is expected to report that 2018 has kicked off with a pickup in hiring.

Market consensus is looking for non-farm payrolls (NFP) to rise by +180k last month, while the unemployment rate continued to hover atop of +4.1% – its lowest level in 18-years.

What to look for in today's payrolls report:

More hiring

The pace of job creation has been slowing as the U.S economy encroaches on full employment. Employers added an average of +171k jobs a month in 2017. After a slightly softer December (+148k), the market expects todays jobs report to rebound to around its recent trend.

Steady unemployment

The U.S unemployment rate is expected to remain atop of +4.1% last month. Fed officials continue to monitor domestic wage and price pressures, and a falling unemployment rate supports their expectation that tighter labor market will eventually boost inflation.

Note: Fed policy makers' median projection in December saw the jobless rate dipping to +3.9% by late 2018.

Wage Growth

The biggest surprise in 2017 was that U.S wage gains actually softened after two consecutive years of gains. Average hourly earnings for private-sector workers were up +2.5% in December y/y, but down from +2.9% annual growth at the end of 2016. Minimum-wage increases in many states should help boost earnings for January.

Housekeeping matters

As is typical for the January jobs report, today's release will include a number of routine changes from the Labor Department. New population controls mean the household-survey figures for the number of employed and unemployed will not be directly comparable between December and January.

The payrolls data will include an annual benchmark revision – roughly +4% of payroll employment will be 'reclassified' by industry due to the adoption of updated classifications.

1. Stocks see red as yields back up

In Japan, the Nikkei share average fell overnight on weakness in most sectors, with banking stocks down on worries that JGB bond yields would be kept low after the BoJ conducted a special bond purchase operation to curb rising yields. The Nikkei dropped -0.9% while the broader Topix shred -0.3%.

Down-under, Australia's S&P/ASX 200 Index rose +0.5%, supported by higher commodity prices. In S. Korea, the Kospi index declined -1.7%.

In Hong Kong, the Hang Seng Index ended Friday marginally down, but posted its biggest weekly loss in two-months, pressured by rising sovereign bond yields. At the close, the Hang Seng index was down -0.12%, while the Hang Seng China Enterprises index rose +0.78%. For the week, the Hang Seng lost -1.7%.

In China, stocks reversed earlier losses and ended higher on Friday, supported by gains in resources firms. Nevertheless, regional indexes still posted hefty weekly drops, led by the Shanghai benchmark index, which posted its worst week in 14-months. At the close, the Shanghai Composite index was up +0.5%, while the blue-chip CSI300 index was up +0.6%.

In Europe, regional indices continue to trade lower with the German DAX registering another -1% decline as rising sovereign rates and mixed earnings continue to weigh on equity markets.

U.S stocks are set to open in the 'red' (-0.7%).

Indices: Stoxx600 -0.9% at 389.8, FTSE -0.3% at 7466, DAX -1.4% at 12822, CAC-40 -1.2% at 5390, IBEX-35 -1.3% at 10264, FTSE MIB -1.1% at 23279, SMI -0.7% at 9229, S&P 500 Futures -0.7%

2. Oil prices extend gains on compliance with output cuts, gold lower

Crude oil prices are rallying for a third consecutive session after a survey showed strong compliance with output cuts by OPEC and others including Russia. It's currently offsetting market concerns about surging U.S production.

Brent futures are up +24c, or +0.3% at +$69.89 a barrel, while U.S West Texas Intermediate (WTI) crude is up +33c or +0.5% at +$66.13 a barrel.

A Reuters survey this week showed that production by OPEC rose in January from an eight-month low as higher output from Nigeria and Saudi Arabia offset a further decline in Venezuela and strong compliance with a supply reduction pact.

Stateside, an EIA report Wednesday disclosed that U.S crude output surpassed +10m bpd in November for the first time in nearly half a century.

Gold has edged lower ahead of the U.S open, under pressure from a stronger USD outright. Investors will take their cues fro today's NFP report. Spot gold is down -0.3% at +$1,345.22 an ounce.

3. Global bond yields break higher

Overnight, the Bank of Japan (BoJ) again conducted a fixed-rate JGB purchase operation (the fourth time performed). Japanese officials offered to buy unlimited amount of 10-year JGB's at +0.11% in an attempt to control their yield curve. The BoJ said its action to cap rises in bond yields was consistent with the central bank's current easy monetary policy.

The market is also taking a look at bund yields – higher yields stateside seem justified, given expectations of further rate increases by the Fed, but rising yields in German Bunds seem to be 'out of sync' with ECB policy. The ECB is set to remain a 'net' buyer of bonds until at least September 2018 and isn't expected to raise policy rates until 2019.

The yield on U.S 10-years has gained less than +1 bps to +2.79%, the highest in almost four-years. In Germany, the 10-year Bund yield has climbed +2 bps to +0.74 percent, the highest in more than two-years, while in the U.K, the 10-year Gilt yield increased +5% bps to +1.531%, its highest yield in 21-months. In Japan, the 10-year yield has declined -1 bps to +0.086%, the largest drop in 11-weeks.

4. Dollar comes up for air

With higher sovereign bond yields supporting a number of higher currency values, both the ECB and BoJ are beginning to show increasing uneasiness around the recent appreciation of their respective currencies (€1.25 and ¥109.87). The somewhat 'outlier' to higher domestic yield has been the USD – it cannot seem to rely on rate and yield differential for solid support.

EUR/USD continued to probe the psychological €1.25 level area on removal of stimulus expectations, but the 'single' unit seems unable to sustain any momentum through this key resistance point. ECB officials have upped its rhetoric on volatility concerns. EUR bulls continue to look at pullbacks to add to current 'long' positions.

The BoJ's commitment of keeping its 10-year yield fixed despite rising upward pressure on global yields might allow 10-year yield differentials to move against the JPY. For now, JPY is confined to its ¥107-112 range.

GBP (£1.4216) is trading softer ahead of the U.S open after a weaker U.K Construction PMI print (see below) and housing activity contracting for the first time in 17-months.

Last December, bitcoin appeared to be marching toward $20,000/coin after climbing as high as $19,511 on Dec. 18. Since then, the cryptocurrency (BTC) has plummeted -56%, leaving it just above $8,000.

5. UK Construction PMI falters

Data this morning showed that U.K activity in the construction sector eased to a four-month low at the start of this year.

Markit's U.K's purchasing managers' index for the construction industry fell to 50.2 in January, down from 52.2 a month earlier – the figure was just above the 50.0 no-change mark, suggesting only a fractional rate of growth.

Digging deeper, concerns about the U.K.'s economic outlook has weighed on new orders, with residential building activity contracting. Cost pressures remain intense, fuelled by shortages of input materials and high costs for imported products.

Bitcoin’s Slump Continues As Losses Near 60% Since Mid-December

- Are Rising Yields Weighing on Equity Markets?

- US Jobs Data Eyed as Fed Insists That Inflation Will Rise;

- Bitcoin's Slump Continues as Losses Near 60% Since Mid-December.

Are Rising Yields Weighing on Equity Markets?

It's been another rocky start to trading in Europe on Friday and the US looks on course for a similar open, with Dow futures off around 1%.

It's been another big week for earnings, with Apple, Amazon and Alphabet all releasing number after the close on Thursday and another 11 S&P 500 companies reporting today. At the same time, there's been a number of important data releases this week as well as a monetary policy announcement from the Federal Reserve which has triggered another rally in US yields, with the 10-year Treasury having hit a high of 2.8%, the first time we've seen these levels since April 2014.

We've also seen corresponding rises in Europe with Gilt yields at their highest since May 2015 and Bunds at their highest since September 2015. This may well be contributing to the declines we've seen recently across Europe – along with the corresponding appreciation of the euro and pound – and could now be taking its toll on US stocks. That doesn't necessarily mean we've entered a risk-off period or that stocks are headed for a correction but a sharp rise in yields, as we've seen, can also weigh on equity markets.

US Jobs Data Eyed as Fed Insists That Inflation Will Rise

With yields now rising, all eyes will be on the US jobs report today. With the Fed anticipating higher inflation and markets buying into the idea of higher rates, the jobs data will be very closely monitored. Naturally, the non-farm payrolls and unemployment numbers will be noted, with around 180,000 new jobs expected, but it's the earnings that people will be most interested in.

If we're going to see a sustainable increase in inflation to 2%, wages will need to rise at a faster rate than they have for years now. The Fed has repeatedly claimed that labour market slack is deteriorating and that higher wages and inflation should follow but that is yet to materialise. Whether that's due to slack still existing that standard measures overlook or other structural issues, it creates a problem for the central bank which is intent on continuing to raise rates. Wages are expected to have risen by 2.6% in January, up from 2.5% in December which is an improvement but not enough to satisfy the doubters.

Bitcoin's Slump Continues as Losses Near 60% Since Mid-December

Bitcoin's slump is continuing on Friday, with the cryptocurrency now trading close to $8,000 and down another 10%, with a raft of stories being blamed for its latest decline. In much the same way that every day seemed to produce another good news story for cryptocurrencies in November and early December during its ascent, we're currently seeing the opposite in motion during its downfall with hardened regulation, outright bans, hacking and investigations being a daily occurrence.

DAX Slips To 4-Week Lows As Deutsche Bank Shares Plunge

The DAX has headed downwards for a second straight day. In the Friday session, the index is trading at 12,863.50, down 1.08% on the day. It’s a quiet end to the week, with just one eurozone event. The Producer Price Index edged lower to 0.2%, missing the estimate of 0.4%. Later in the day, the US releases nonfarm payrolls, which is expected to improve to 181 thousand.

Deutsche Bank shares have dropped sharply on Friday, sending European stock markets into red territory. Shares of the giant German bank are currently down 5.5% on the day. The picture is not a pretty one, as the stock price is at its lowest level since November, and the bank posted its third straight annual loss in 2017. A decline in investment bank revenue and the US tax reform bill contributed to a weak fourth quarter for Deutsche Bank shares. The banking sector showing losses on Friday, with Commerzbank down by 1.62%. Almost all listing on the DAX are in negative territory and showing “strong sell”, so traders can expect the DAX to continue to decline in the Friday session.

With the eurozone economy continuing to perform well, there has been speculation that the ECB could wind up its asset-purchase program (QE) in September and shift to a normative policy, and perhaps raise interest rates. However, Mario Draghi and other ECB members have taken pains to reiterate that the Bank is in no rush to end QE. On Wednesday, executive board member Benoit Coeure joined the chorus, saying that although QE “will not last forever” policymakers were in agreement “that we have to be patient and prudent because we are not yet where we want to be in terms of inflation”. Investors would be well advised to keep a close eye on eurozone and German inflation numbers, as asset purchases could be extended beyond September if inflation remains well below the ECB target of around 2.0%.