Sample Category Title

RBNZ’s Orr: No more 50bps cuts without a shock, sees stable inflation ahead

RBNZ Governor Adrian Orr reaffirmed that a 50bps rate cut would only happen again in the event of an economic shock, reinforcing the central bank’s guidance for two 25bps cuts in the first half of 2025.

Speaking before a parliamentary committee today, Orr noted that New Zealand is now in an environment of low and stable inflation, though global uncertainty remains a key risk.

He expressed optimism, stating that “GDP growth, employment growth, and low and stable inflation” should support an improving economic environment throughout the year. However, he warned that “geoeconomic fragmentation” is weighing on global growth, leading to increased price volatility in international markets.

RBNZ Chief Economist Paul Conway told the committee that escalating trade tensions will contribute to higher inflation, weaker global growth, and reduced economic efficiency. He stressed that "The best thing we can do is have headline inflation at 2% so that we can sort of absorb that future volatility."

Fed’s Jefferson: No rush to cut rates as economy remains strong

Fed Vice Chairman Philip Jefferson said in a speech overnight that the central bank can “take our time” in assessing economic data before making any changes. With the U.S. economy performing well and the labor market remaining solid, Jefferson indicated that there is no immediate urgency to ease policy further.

He acknowledged that progress toward the Fed’s 2% inflation target "has been slow in the past year." He added that the path of inflation will likely remain “bumpy”.

While the 100 basis points of cumulative rate cuts last year have moved policy closer to a neutral stance, he reiterated that monetary policy is still "restrictive".

Fed’s Bostic keeps rate cuts on the table but stresses need for more data

Atlanta Fed President Raphael Bostic reiterated in an interview that rate cuts remain a possibility this year, but emphasized the need for further data clarity before making any decisions.

He maintained a neutral stance, stating, “I am not taking anything off the table. I am not putting anything extra on the table.”

Bostic acknowledged that January’s hotter-than-expected inflation data raised questions about whether it represents "a new trend or just a bump in the road". He will be closely analyzing economic developments “over the next several months” to determine the correct policy response.

Bostic also defended Fed’s current position, insisting, “I don’t think we have cut too much. We are still in a restrictive posture and that’s what we need.” He reaffirmed that monetary policy remains tight enough to bring inflation down, arguing that waiting until inflation fully reaches 2% before easing would have been a mistake.

Fed minutes signal no rush to cut rates, inflation risks remain in focus

FOMC’s January meeting minutes reinforced Fed’s cautious stance, with policymakers emphasizing the need for “further progress on inflation” before considering any rate cuts. The officials acknowledged a “high degree of uncertainty” in the economic outlook, justifying a “careful approach” to policy adjustments.

While Fed remains confident that inflation will ease in the coming months, officials largely pointed to "upside risks to the inflation outlook", rather than concerns over the job market.

he minutes highlighted several factors that could disrupt the disinflation process, including shifts in trade and immigration policy, geopolitical disruptions to supply chains, and stronger-than-expected household spending. These risks suggest that inflationary pressures could remain stickier than anticipated, keeping the Fed on hold for longer.

(FED) Minutes of the Federal Open Market Committee

January 28–29, 2025

A joint meeting of the Federal Open Market Committee and the Board of Governors of the Federal Reserve System was held in the offices of the Board of Governors on January 28, 2025, at 8:30 a.m. and continued on Wednesday, January 29, 2025, at 9:00 a.m.1

Annual Organizational Matters2

The agenda for this meeting reported that advices of the election of the following members and alternate members of the Federal Open Market Committee for a term beginning January 28, 2025, were received and that these individuals executed their oaths of office.

The elected members and alternate members were as follows:

John C. Williams, President of the Federal Reserve Bank of New York, with Sushmita Shukla, First Vice President of the Federal Reserve Bank of New York, as alternate;

Susan M. Collins, President of the Federal Reserve Bank of Boston, with Patrick Harker, President of the Federal Reserve Bank of Philadelphia, as alternate;

Austan D. Goolsbee, President of the Federal Reserve Bank of Chicago, with Beth M. Hammack, President of the Federal Reserve Bank of Cleveland, as alternate;

Alberto G. Musalem, President of the Federal Reserve Bank of St. Louis, with Lorie K. Logan, President of the Federal Reserve Bank of Dallas, as alternate;

Jeffrey R. Schmid, President of the Federal Reserve Bank of Kansas City, with Neel Kashkari, President of the Federal Reserve Bank of Minneapolis, as alternate;

By unanimous vote, the following officers of the Committee were selected to serve until the selection of their successors at the first regularly scheduled meeting of the Committee in 2026:

| Jerome H. Powell | Chair |

| John C. Williams | Vice Chair |

| Joshua Gallin | Secretary |

| Matthew M. Luecke | Deputy Secretary |

| Brian J. Bonis | Assistant Secretary |

| Michelle A. Smith | Assistant Secretary |

| Mark E. Van Der Weide | General Counsel |

| Richard Ostrander | Deputy General Counsel |

| Reena Sahni | Assistant General Counsel |

| Trevor A. Reeve | Economist |

| Stacey Tevlin | Economist |

| Beth Anne Wilson | Economist |

| Shaghil Ahmed | |

| Kartik B. Athreya | |

| James A. Clouse | |

| Brian M. Doyle | |

| Eric M. Engen | |

| Carlos Garriga | |

| Joseph W. Gruber | |

| Anna Paulson | |

| William Wascher | |

| Egon Zakrajšek | Associate Economists |

By unanimous vote, the Committee selected the Federal Reserve Bank of New York to execute transactions for the System Open Market Account (SOMA).

By unanimous vote, the Committee selected Roberto Perli and Julie Ann Remache to serve at the pleasure of the Committee as manager and deputy manager of the SOMA, respectively, on the understanding that these selections were subject to being satisfactory to the Federal Reserve Bank of New York.

Secretary's note: The Federal Reserve Bank of New York subsequently sent advice that the selections indicated previously were satisfactory.

By unanimous vote, the Committee voted to reaffirm without revision the FOMC Authorizations and Continuing Directives for Open Market Operations.

All participants indicated support for, and agreed to abide by, the FOMC Policy on Investment and Trading for Committee Participants and Federal Reserve System Staff, the Program for Security of FOMC Information, the FOMC Policy on External Communications of Committee Participants, and the FOMC Policy on External Communications of Federal Reserve System Staff. The Committee voted unanimously to approve those four policies.2

Review of Monetary Policy Strategy, Tools, and Communications

Committee participants began discussions related to their review of the Federal Reserve's monetary policy framework. This review is focused on two specific areas: the Committee's Statement on Longer-Run Goals and Monetary Policy Strategy, which presents the Committee's approach to the conduct of monetary policy, and the Committee's policy communication practices. The Committee's 2 percent longer-run inflation goal will be retained and is not a focus of the review.

In support of these discussions, staff briefings provided a retrospective on the Committee's 2019–20 framework review and summarized the experience abroad in conducting reviews of monetary policy frameworks. The staff presentation began by recapping the creation and evolution of the Committee's Statement on Longer-Run Goals and Monetary Policy Strategy and the context of the Committee's 2019–20 review. The adoption of the statement in 2012 introduced the Committee's 2 percent inflation target and codified long-standing practices followed by the Committee and, as such, was an important step in improving the transparency, accountability, and predictability of U.S. monetary policymaking. The launch of the 2019–20 review was motivated in part by a desire to evaluate the experience of the Global Financial Crisis and its aftermath. During this period, inflation had run persistently below the Committee's 2 percent objective, even as the unemployment rate and interest rates remained low. These developments indicated a greater risk that the federal funds rate would be constrained by its effective lower bound (ELB) more often in the future, posing challenges to the achievement of the Committee's dual-mandate goals over the medium term. The staff summarized the scope and components of the 2019–20 review, including its outreach to a broad range of individuals and groups, and the rationale behind the changes made to the statement at the end of the review.

In summarizing the international experience, the staff noted that occasional reviews of monetary policy frameworks were seen as useful in adapting to evolving economic environments, promoting transparency, and fostering public understanding and, therefore, were becoming the norm in advanced economies. Reviews abroad had covered various aspects related to monetary policy goals, strategies, tools, communications, forecasting, and governance, with some of the recent reviews giving particular attention to topics such as the experience of the COVID–19 pandemic, the ensuing global inflation episode, and the conduct and communication of monetary policy in times of unusual uncertainty.

Participants viewed the statement as having played an important role in building a common understanding among policymakers of the congressionally mandated monetary policy goals and of their monetary policy strategy. The statement and other means of policy communication also figured importantly in conveying that understanding to the public and helping to anchor inflation expectations, thereby supporting the effective transmission of monetary policy. Participants indicated that they were looking forward to their discussions at upcoming meetings and to hearing a range of perspectives at various Fed Listens events as well as at a planned research conference, and that they were approaching the review with open minds.

Participants noted that the economic consequences of the COVID–19 pandemic were largely unforeseen at the time of the 2019–20 review and that the current economic environment differed greatly from the period leading up to that review, which was characterized in part by persistently low inflation and interest rates. In light of the experience of the past five years, participants assessed that it was important to consider potential revisions to the statement, with particular attention to some of the elements introduced in 2020. Participants highlighted as areas of consideration the statement's focus on the risks to the economy posed by the ELB, the approach of mitigating shortfalls from maximum employment, and the approach of aiming to achieve inflation moderately above 2 percent following periods of persistently below-target inflation. Participants emphasized the need for the FOMC's monetary policy framework to be robust to a wide range of economic circumstances. They noted that economic uncertainty—including about the values of the longer-run neutral policy rate, the economy's potential growth rate, and the level of maximum employment—would remain an important factor affecting their decisionmaking. Participants also mentioned aspects of the statement that they thought should continue to be emphasized—including the Committee's firm commitment to achieving maximum employment and 2 percent inflation, as well as the importance of keeping longer-term inflation expectations well anchored.

Participants expected that their discussions related to the framework review would continue at upcoming meetings. They expected the review to wrap up by late summer and intended to report the outcomes of the review to the public.

Developments in Financial Markets and Open Market Operations

The manager turned first to a review of developments in financial markets. Over the intermeeting period, broad equity price indexes had declined moderately, credit spreads had remained very tight, and the trade-weighted value of the dollar had risen slightly. In considering the expected path of the federal funds rate, the manager noted that the modal policy rate path implied by options prices had not changed appreciably on net over the intermeeting period and was broadly consistent with a single quarter-point lowering of the target range for the federal funds rate taking place during 2025. The average rate path implied by futures prices was also little changed and was above the corresponding median rates in the December 2024 Summary of Economic Projections. The modal path implied by the Open Market Desk's Survey of Market Expectations shifted up somewhat over the intermeeting period, with respondents generally judging that policy rate reductions would occur later than previously assessed, and was broadly consistent with market-implied paths at horizons up to early 2026. Beyond that period, however, the survey-based path was notably below the market-implied path. This discrepancy likely partly reflected positive market risk premiums as well as survey biases. In their expectations of Federal Reserve balance sheet policy, survey respondents on average saw the process of runoff concluding by mid-2025, slightly later than they had previously expected.

The manager next considered the recent behavior of Treasury yields. Longer-term nominal Treasury yields had risen sharply following the Committee's December meeting and the release of the unexpectedly strong December payrolls report. Subsequently, a partial retracing of this increase took place after consumer price index (CPI) data indicated that prices rose more slowly than expected in December. Over the intermeeting period, longer-dated Treasury yields rose 15 to 20 basis points, while shorter-dated yields were little changed. The manager discussed staff analysis that had aimed at decomposing the increase of nearly 100 basis points in longer-term Treasury yields that had taken place since mid-September 2024. That analysis suggested an upward revision in financial markets' evaluation of the path of the real policy rate required to achieve the Committee's goals, especially at longer horizons. Nevertheless, much of the increase in real yields was in real term premiums, likely reflecting uncertainty about the policy rate trajectory as well as a number of other factors. The manager noted that measures of inflation compensation had generally risen slightly. However, both survey measures of inflation expectations and pricing in the Treasury Inflation-Protected Securities market remained broadly consistent with the anticipation that inflation would return to the Committee's 2 percent inflation objective.

With respect to money markets, the manager noted that December's quarter-point lowering of the target range for the federal funds rate had been fully passed through to other short-term interest rates. In addition, the 5 basis point technical adjustment to the overnight reverse repurchase agreement (ON RRP) offering rate implemented in December appeared to have been transmitted nearly in full to repurchase agreement (repo) rates. Money market conditions had been orderly over year-end, with the technical adjustment to the ON RRP offering rate directly contributing to a lower rate environment by keeping repo rates below the values that would have otherwise prevailed. Throughout the week of year-end, the Desk conducted standing repo facility (SRF) auctions each morning, in addition to the regular afternoon auctions. Although there was no take-up, market contacts suggested that the morning auctions may also have helped contain year-end pressures. The manager noted that morning SRF auctions may be conducted again in the future. On December 26, a considerable volume of activity had taken place in the noncentrally cleared segment of the repo market, in which the SRF operates, at rates above the SRF rate. The manager stated that, in the future, the Desk may consider possible ways to improve the efficacy of the facility in that market segment.

The manager observed that usage of the ON RRP facility increased as expected at year-end but had declined on net over the intermeeting period. The manager also noted that a range of indicators continued to suggest that reserves had remained abundant over the intermeeting period. However, the manager cautioned that the debt limit situation may cloud the signals provided by the indicators. In addition, reserves might decline quickly upon resolution of the debt limit and, at the current pace of balance sheet runoff, might potentially reach levels below those viewed by the Committee as appropriate.

Next, the deputy manager briefed policymakers on possible alternative strategies that the Committee might follow with regard to purchases of Treasury securities in the secondary market after the eventual conclusion of the process of balance sheet runoff. These strategies would further implement the policy laid out in the Committee's Principles and Plans for Reducing the Size of the Federal Reserve's Balance Sheet. The briefing outlined a few illustrative scenarios; under each scenario, principal payments received from agency debt and agency mortgage‑backed securities (MBS) holdings would be directed toward Treasury securities via secondary-market purchases. The scenarios presented corresponded to different trajectories of the holdings of Treasury securities in the SOMA. Under all scenarios considered, the maturity composition of Treasury holdings in the SOMA portfolio moved into closer alignment with the maturity composition of the outstanding stock of Treasury securities. The scenarios differed on how quickly this alignment would be achieved and, correspondingly, on the assumed increase over coming years in the share of Treasury bills held in the SOMA portfolio.

By unanimous vote, the Committee ratified the Desk's domestic transactions over the intermeeting period. There were no intervention operations in foreign currencies for the System's account during the intermeeting period.

Staff Review of the Economic Situation

The information available at the time of the meeting indicated that real gross domestic product (GDP) rose at a solid pace in 2024. After a period of considerable rebalancing, labor market conditions had stabilized, and the unemployment rate remained low. Consumer price inflation remained somewhat elevated.

Total consumer price inflation—as measured by the 12-month change in the price index for personal consumption expenditures (PCE)—was 2.4 percent in November, down from its year-earlier pace of 2.7 percent. Core PCE price inflation, which excludes changes in consumer energy prices and many consumer food prices, was 2.8 percent in November, down from 3.2 percent a year ago. In December, the 12-month change in the CPI was 2.9 percent and core CPI inflation was 3.2 percent; both were below their year-earlier rates. Based on the CPI and the producer price index, the staff estimated that total PCE price inflation would be reported as 2.6 percent over the 12 months ending in December and that core PCE price inflation would be 2.8 percent.

Recent data suggested that labor market conditions remained solid and that the labor market was not especially tight. Average monthly gains for nonfarm payrolls over the fourth quarter were slightly higher than their third-quarter pace. The unemployment rate edged down to 4.1 percent in December, while the labor force participation rate was unchanged and the employment-to-population ratio moved up slightly. The unemployment rates for African Americans and for Hispanics moved down but remained higher than the rates for Asians and for Whites. The ratio of job vacancies to unemployed workers edged up to 1.2 in December, its average over 2019, and the quits rate fell back to 1.9 percent and remained well below its 2019 average. Average hourly earnings for all employees rose 3.9 percent over the 12 months ending in December, down from 4.3 percent a year ago.

Available data indicated that real GDP rose at a solid pace in the fourth quarter. Real private domestic final purchases, which comprises PCE and private fixed investment and which often provides a better signal than GDP of underlying economic momentum, appeared to have risen faster than real GDP in the fourth quarter, led by continued strength in consumer spending. By contrast, monthly trade data were volatile but overall pointed to a step-down in both export and import growth relative to the third quarter.

The pace of foreign economic activity appeared to have moderated at the end of last year. Indicators suggested that in both the euro area and Mexico, economic growth had slowed notably in the fourth quarter amid lackluster manufacturing activity and subdued private consumption. By contrast, Chinese growth had picked up, in large part because of policy stimulus, and elsewhere in emerging Asia the pace of activity looked to have remained solid, supported by strong global demand for high-tech manufacturing goods.

Inflation abroad continued to ease. In most advanced foreign economies (AFEs), headline inflation hovered near target levels, mainly reflecting the rapid pass-through of lower energy prices in the second half of 2024. Even so, services price inflation remained elevated in some of these economies, such as Germany. In China, inflation remained close to zero, partly reflecting lower food prices. By contrast, in some Latin American countries, most notably Brazil, inflation continued to increase, in part spurred by currency depreciation.

Many foreign central banks eased policy during the intermeeting period, including the Bank of Canada, the European Central Bank, and the Swiss National Bank among the AFEs, and the central banks of Colombia, Indonesia, and Mexico among the emerging market economies (EMEs). In contrast, amid improving economic conditions, the Bank of Japan increased its policy rate, taking a further step in gradually removing policy accommodation.

Staff Review of the Financial Situation

The market-implied path of the federal funds rate over the next year was little changed on net over the intermeeting period. Yields on shorter-term nominal Treasury securities edged down, but longer-term rates rose moderately. The increase in longer-term yields appeared to be partly attributable to higher term premiums. Measures of inflation compensation over the near term moved up, but measures of longer-term inflation compensation remained at levels consistent with inflation returning over time to the Committee's 2 percent objective.

Broad equity price indexes were little changed on net, while measures of the equity risk premium remained low, and corporate bond spreads remained compressed by historical standards. The VIX—a forward-looking measure of near-term equity market volatility—was also roughly unchanged on net and remained at a moderate level by historical standards.

Foreign financial market moves over the intermeeting period mainly reflected developments in the U.S., including trade policy news and the relative strength of the U.S. economic data releases during the period. The broad dollar index increased slightly on net. Longer-term AFE yields edged higher, reflecting in part spillovers from higher U.S. yields. Stock price indexes increased in most foreign countries, with the notable exception of China, in which equity prices declined moderately, in part reflecting weaker-than-expected forward-looking manufacturing indicators. Capital outflows from emerging markets continued, and several EME central banks drew down their foreign exchange reserves, including their holdings of U.S. Treasury securities, to resist currency depreciation pressures.

Conditions in U.S. short-term funding markets remained generally stable over the intermeeting period, with the lowering of the target range for the federal funds rate in December fully passing through to both secured and unsecured reference rates. Rates in secured markets exhibited temporary, and typical, upward pressure around year-end. Excluding the year-end period, rates in secured markets declined somewhat relative to the effective federal funds rate, likely reflecting the effects of the nearly full pass-through of December's technical adjustment to the ON RRP offering rate and of declining bill issuance. ON RRP usage increased around year-end but declined slightly on net over the intermeeting period.

In domestic credit markets, borrowing costs for households and most businesses remained elevated. Rates on 30-year fixed-rate conforming residential mortgages rose. Interest rates for credit cards and new auto loans declined but remained elevated relative to their historical ranges. Meanwhile, interest rates on commercial and industrial (C&I) loans and small business loans remained elevated. Yields rose for an array of fixed-income securities, including investment-grade corporate bonds and senior commercial MBS tranches, consistent with movements in long-term Treasury yields.

Financing through capital markets and nonbank lenders remained broadly available for public corporations and for large and midsize private corporations. With respect to smaller firms, however, credit availability remained relatively tight. Issuance of corporate bonds and leveraged loans moderated toward year-end, likely reflecting seasonal factors. Regarding bank credit, banks in the January Senior Loan Officer Opinion Survey on Bank Lending Practices (SLOOS) reported leaving their C&I loan standards basically unchanged on net over the fourth quarter.3 Meanwhile, growth in C&I loan balances picked up from modest levels. Banks in the January SLOOS reported tighter lending standards for all commercial real estate (CRE) loan categories. Consistent with tight standards, growth in CRE loans on banks' books remained subdued in the fourth quarter.

Credit remained available for most households, though standards appear to have tightened somewhat for lower-credit-score borrowers. Growth in credit card loan balances at banks picked up in the fourth quarter, but issuance of new credit cards to nonprime borrowers continued to decline. In the residential mortgage market, credit remained easily available for high-credit-score borrowers but tightened slightly in November and December for lower-score borrowers. In the January SLOOS, respondents on net indicated that standards tightened for credit cards, eased for auto loans, and were about unchanged for most residential mortgages.

Credit quality remained solid for large and midsize firms, most home mortgage borrowers, and municipalities but continued to deteriorate in other sectors. The credit performance of corporate bonds and leveraged loans showed some signs of deterioration but remained generally stable. Delinquency rates on loans to small businesses ticked down but remained elevated. Credit quality in the CRE market deteriorated further, driven largely by office and multifamily loans. Regarding household credit quality, the delinquency rate on Federal Housing Administration mortgages edged up in November and remained elevated relative to the past few years. In contrast, delinquency rates on most other mortgage loan types remained low. Delinquency rates for credit cards increased a bit further in the third quarter, while those for auto loans stayed about flat.

The staff provided an update on its assessment of the stability of the U.S. financial system and, on balance, continued to characterize the system's financial vulnerabilities as notable. The staff judged that asset valuation pressures were elevated. In contrast to valuations in equity, corporate debt, and residential real estate markets, CRE property prices have declined notably in recent years, though price indexes were about flat in the third quarter.

Vulnerabilities associated with business and household debt were characterized as moderate. Nonfinancial business leverage was elevated by historical standards, but the ability of publicly traded firms to service their debt remained strong, supported by robust earnings and the low interest rates that firms continued to enjoy on the portion of fixed-rate debt issued early in the pandemic. That said, the fraction of private firm debt having very low interest coverage ratios continued to increase, pointing to further deterioration in the balance sheets of riskier firms. Household balance sheets remained solid overall, as aggregate home equity remained high and delinquencies on mortgage loans continued to be low.

Vulnerabilities associated with leverage in the financial sector were characterized as notable. Regulatory capital ratios in the banking sector remained high; however, banks continued to hold large quantities of long-duration assets, leaving them more exposed than usual to an unexpected rise in longer-term interest rates. In the nonbank sector, leverage at hedge funds remained high.

Vulnerabilities associated with funding risks were characterized as moderate. Large nonglobal systemically important banks and regional banks reduced their reliance on uninsured deposits notably since the end of 2021. Though assets in prime money market funds had been growing recently, their size relative to GDP remained well below levels seen before 2016.

Staff Economic Outlook

The staff projection for economic activity was similar to the one prepared for the December meeting, with the output gap expected to narrow further until early next year and to remain roughly flat thereafter, and with the unemployment rate expected to remain close to the staff's estimate of its natural rate. For this projection, the staff had used the same preliminary placeholder assumptions for potential policy changes that were used for the previous baseline forecast, and continued to note elevated uncertainty regarding the scope, timing, and potential economic effects of possible changes to trade, immigration, fiscal, and regulatory policies. The staff highlighted the difficulty of assessing the importance of such factors for the baseline projection and had prepared a number of alternative scenarios.

The staff's inflation projection was also essentially unchanged from the one prepared for the previous meeting. Inflation in 2025 was expected to be similar to 2024's rate, as the effects of the staff's placeholder assumption for trade policy put upward pressure on inflation this year. After that, inflation was projected to decline to 2 percent by 2027.

The staff continued to view the uncertainty around the baseline projection as similar to the average over the past 20 years, a period that saw a number of episodes during which uncertainty about the economy and federal policy changes was elevated. The staff judged that the risks around the baseline projections for economic activity and employment were roughly balanced. The risks around the baseline projection for inflation were seen as skewed to the upside because core inflation had not come down as much as expected in 2024 and because changes to trade policy could put more upward pressure on inflation than the staff had assumed.

Participants' Views on Current Conditions and the Economic Outlook

In their discussion of inflation developments, participants observed that inflation had eased significantly over the past two years. Inflation remained somewhat elevated, however, relative to the Committee's 2 percent longer-run goal, and progress toward that goal had slowed over the past year. Available data suggested that total PCE prices had risen about 2.6 percent over the 12 months ending in December and that, excluding the volatile consumer food and energy categories, core PCE prices rose 2.8 percent. A number of participants remarked that current readings of 12-month inflation were boosted by relatively high inflation readings in the first quarter of last year, and several participants noted that cumulative inflation over the past 3, 6, or 9 months showed greater progress than 12‑month measures. Most participants commented that month-over-month inflation readings in November and December had exhibited notable progress toward the Committee's goal of price stability, including in some key subcategories. Many participants, however, emphasized that additional evidence of continued disinflation would be needed to support the view that inflation was returning sustainably to 2 percent. Regarding the subcategories, housing services inflation, which had remained elevated for much of the previous year, had shown a decline, as had market-based measures of core nonhousing services inflation. Several participants noted that some nonmarket-based services price categories, such as financial and insurance services, had shown less improvement, but a few also observed that price movements in such categories typically have not provided reliable signals about resource pressures or the future trajectory of inflation. Several participants observed that core goods prices had not declined as much on net in recent months compared with earlier in 2024.

With regard to the outlook for inflation, participants expected that, under appropriate monetary policy, inflation would continue to move toward 2 percent, although progress could remain uneven. Participants cited various factors as likely to put continuing downward pressure on inflation, including an easing in nominal wage growth, well-anchored longer-term inflation expectations, waning business pricing power, and the Committee's still-restrictive monetary policy stance. A few noted, however, that the current target range for the federal funds rate may not be far above its neutral level. Furthermore, some participants commented that with supply and demand in the labor market roughly in balance and in light of recent productivity gains, labor market conditions were unlikely to be a source of inflationary pressure in the near future. However, other factors were cited as having the potential to hinder the disinflation process, including the effects of potential changes in trade and immigration policy as well as strong consumer demand. Business contacts in a number of Districts had indicated that firms would attempt to pass on to consumers higher input costs arising from potential tariffs. In addition, some participants noted that some market- or survey-based measures of expected inflation had increased recently, although many participants emphasized that longer-term measures of expected inflation had remained well anchored. Some participants remarked that reported inflation at the beginning of the year was harder than usual to interpret because of the difficulties in fully removing seasonal effects, and a couple of participants commented that any increase in reported inflation in the first quarter due to such difficulties would imply a corresponding decrease in reported inflation in other quarters of the year.

Participants judged that labor market conditions had remained solid and that those conditions were broadly consistent with the Committee's goal of maximum employment. Payroll gains had averaged 170,000 per month over the last three months of 2024 and the unemployment rate had stabilized at a relatively low level. Participants also noted that recent readings of indicators such as job vacancies, the quits rate, and labor turnover were generally consistent with stable labor market conditions. Participants anticipated that under appropriate monetary policy, conditions in the labor market would likely remain solid. Nonetheless, participants generally noted that labor market indicators merited close monitoring. Business contacts in a few Districts noted that they were expecting stable employment levels and moderate wage growth at their firms. A couple of participants noted that the upcoming benchmark revision to the payroll growth estimates by the Bureau of Labor Statistics could provide more clarity regarding labor market conditions.

Participants observed that the economy had continued to expand at a solid pace and that recent data on economic activity, and consumer spending in particular were, on balance, stronger than anticipated. Participants remarked that consumption had been supported by a solid labor market, elevated household net worth, and rising real wages, which had been associated in part with productivity gains. Several participants cautioned that low- and moderate-income households continued to experience financial strains, which could damp their spending. A few participants cited continued increases in rates of delinquencies on credit card borrowing and automobile loans as signs of such strains.

With regard to the business sector, participants observed that investment in equipment and intangibles was strong over the past year, though it appeared to have slowed in the fourth quarter. Some participants noted that favorable aggregate supply developments—including increases in labor supply, business investment, and productivity—continued to support a solid expansion of business activity. Many participants remarked that District contacts or surveys of businesses reported substantial optimism about the economic outlook, stemming in part from an expectation of an easing in government regulations or changes in tax policies. In contrast, some participants noted that contacts reported increased uncertainty regarding potential changes in federal government policies. A couple of participants remarked that the agricultural sector continued to face significant strains stemming from low crop prices and high input costs.

A number of participants commented on the financial conditions bearing on spending by households and businesses. Participants generally saw it as important to continue to keep a close watch on such conditions and their potential effects on economic activity and inflation. Many participants noted that certain financial conditions had tightened over the past several months. For example, longer-term Treasury and corporate bond yields and mortgage rates had risen notably. A couple of participants commented that high equity valuations or low credit spreads were providing some support to economic activity.

In their evaluation of the risks and uncertainties associated with the economic outlook, the vast majority of participants judged that the risks to the achievement of the Committee's dual-mandate objectives of maximum employment and price stability were roughly in balance, though a couple commented that the risks to achieving the price stability mandate currently appeared to be greater than the risks to achieving the maximum employment mandate. Participants generally pointed to upside risks to the inflation outlook. In particular, participants cited the possible effects of potential changes in trade and immigration policy, the potential for geopolitical developments to disrupt supply chains, or stronger-than-expected household spending. A couple of participants remarked that, in the period ahead, it might be especially difficult to distinguish between relatively persistent changes in inflation and more temporary changes that might be associated with the introduction of new government policies. Participants pointed to various risks to economic activity and employment, including downside risks associated with an unexpected weakening of the labor market, a weakening of consumers' financial positions, or a tightening of financial conditions, as well as upside risks associated with a potentially more favorable regulatory environment for businesses and continued strength in domestic spending.

In their discussion of financial stability, participants who commented noted a range of factors that warranted monitoring. Several participants mentioned issues related to the banking system. A few commented that bank funding risks had lessened and that many banks had improved their ability to access the discount window; however, a couple observed that some banks had increased their reliance on reciprocal deposits, and that the stability of these deposits had not been tested in a time of stress. Several participants noted that some banks remained vulnerable to a rise in longer-term yields and the associated unrealized losses on bank assets. Several participants also mentioned potential vulnerabilities at nonbank financial institutions or nonfinancial corporations to a rise in longer-term yields or to leverage in these sectors. A few participants noted concerns about asset valuation pressures in equity and corporate debt markets. A few participants discussed vulnerabilities associated with CRE exposures, noting that risks remained, although there were some signs that the deterioration of conditions in the CRE sector was lessening. Several participants commented on cyber risks that could impair the operation of financial institutions, financial infrastructure, and, potentially, the overall economy. Several participants commented on vulnerabilities in the Treasury market, including concerns about dealer intermediation capacity and the degree of leveraged positions in the market. The migration to central clearing was noted by a few as an important development to track in this regard.

In their consideration of monetary policy at this meeting, participants noted that inflation remained somewhat elevated. Participants also observed that recent indicators suggested that economic activity had continued to expand at a solid pace, that the unemployment rate had stabilized at a low level, and that labor market conditions had remained solid in recent months. With the stance of policy significantly less restrictive than it had been before the Committee's policy easing over its previous three meetings, all participants viewed it as appropriate to maintain the target range for the federal funds rate at 4-1/4 to 4-1/2 percent. Participants judged that it was appropriate to continue the process of reducing the Federal Reserve's securities holdings.

In discussing the outlook for monetary policy, participants observed that the Committee was well positioned to take time to assess the evolving outlook for economic activity, the labor market, and inflation, with the vast majority pointing to a still-restrictive policy stance. Participants indicated that, provided the economy remained near maximum employment, they would want to see further progress on inflation before making additional adjustments to the target range for the federal funds rate. Participants noted that policy decisions were not on a preset course and were conditional on the evolution of the economy, the economic outlook, and the balance of risks.

In discussing risk-management considerations that could bear on the outlook for monetary policy, a majority of participants observed that the current high degree of uncertainty made it appropriate for the Committee to take a careful approach in considering additional adjustments to the stance of monetary policy. Factors mentioned by participants as supporting such an approach included the reduced downside risks to the outlook for the labor market and economic activity, increased upside risks to the outlook for inflation, and uncertainties concerning the neutral rate of interest, the degree of restraint from higher longer-term interest rates, or the economic effects of potential government policies. Many participants noted that the Committee could hold the policy rate at a restrictive level if the economy remained strong and inflation remained elevated, while several remarked that policy could be eased if labor market conditions deteriorated, economic activity faltered, or inflation returned to 2 percent more quickly than anticipated.

A number of participants also discussed some issues related to the balance sheet. Regarding the composition of secondary-market purchases of Treasury securities that would occur once the process of reducing the size of the Federal Reserve's holdings of securities had come to an end, many participants expressed the view that it would be appropriate to structure purchases in a way that moved the maturity composition of the SOMA portfolio closer to that of the outstanding stock of Treasury debt while also minimizing the risk of disruptions to the market. Regarding the potential for significant swings in reserves over coming months related to debt ceiling dynamics, various participants noted that it may be appropriate to consider pausing or slowing balance sheet runoff until the resolution of this event. Several participants also expressed support for the Desk's future consideration of possible ways to improve the efficacy of the SRF.

Committee Policy Actions

In their discussions of monetary policy for this meeting, members agreed that recent indicators suggested that economic activity had continued to expand at a solid pace. The unemployment rate had stabilized at a low level in recent months and labor market conditions had remained solid. Members concurred that inflation remained somewhat elevated. Almost all members agreed that the risks to achieving the Committee's employment and inflation goals were roughly in balance. Members viewed the economic outlook as uncertain and agreed that they were attentive to the risks to both sides of the Committee's dual mandate.

In support of its goals, the Committee agreed to maintain the target range for the federal funds rate at 4-1/4 to 4-1/2 percent. Members agreed that in considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee would carefully assess incoming data, the evolving outlook, and the balance of risks. Members agreed to continue to reduce the Federal Reserve's holdings of Treasury securities and agency debt and agency MBS. All members agreed that the postmeeting statement should affirm their strong commitment both to supporting maximum employment and to returning inflation to the Committee's 2 percent objective.

Members agreed that in assessing the appropriate stance of monetary policy, the Committee would continue to monitor the implications of incoming information for the economic outlook. They would be prepared to adjust the stance of monetary policy as appropriate if risks emerged that could impede the attainment of the Committee's goals. Members also agreed that their assessments would take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

At the conclusion of the discussion, the Committee voted to direct the Federal Reserve Bank of New York, until instructed otherwise, to execute transactions in the SOMA in accordance with the following domestic policy directive, for release at 2:00 p.m.:

"Effective January 30, 2025, the Federal Open Market Committee directs the Desk to:

- Undertake open market operations as necessary to maintain the federal funds rate in a target range of 4-1/4 to 4-1/2 percent.

- Conduct standing overnight repurchase agreement operations with a minimum bid rate of 4.5 percent and with an aggregate operation limit of $500 billion.

- Conduct standing overnight reverse repurchase agreement operations at an offering rate of 4.25 percent and with a per‑counterparty limit of $160 billion per day.

- Roll over at auction the amount of principal payments from the Federal Reserve's holdings of Treasury securities maturing in each calendar month that exceeds a cap of $25 billion per month. Redeem Treasury coupon securities up to this monthly cap and Treasury bills to the extent that coupon principal payments are less than the monthly cap.

- Reinvest the amount of principal payments from the Federal Reserve's holdings of agency debt and agency mortgage‑backed securities (MBS) received in each calendar month that exceeds a cap of $35 billion per month into Treasury securities to roughly match the maturity composition of Treasury securities outstanding.

- Allow modest deviations from stated amounts for reinvestments, if needed for operational reasons.

- Engage in dollar roll and coupon swap transactions as necessary to facilitate settlement of the Federal Reserve's agency MBS transactions."

The vote also encompassed approval of the statement below for release at 2:00 p.m.:

"Recent indicators suggest that economic activity has continued to expand at a solid pace. The unemployment rate has stabilized at a low level in recent months, and labor market conditions remain solid. Inflation remains somewhat elevated.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. The Committee judges that the risks to achieving its employment and inflation goals are roughly in balance. The economic outlook is uncertain, and the Committee is attentive to the risks to both sides of its dual mandate.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 4-1/4 to 4-1/2 percent. In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. The Committee is strongly committed to supporting maximum employment and returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments."

Voting for this action: Jerome H. Powell, John C. Williams, Michael S. Barr, Michelle W. Bowman, Susan M. Collins, Lisa D. Cook, Austan D. Goolsbee, Philip N. Jefferson, Adriana D. Kugler, Alberto G. Musalem, Jeffrey R. Schmid, and Christopher J. Waller.

Voting against this action: None.

Consistent with the Committee's decision to leave the target range for the federal funds rate unchanged, the Board of Governors of the Federal Reserve System voted unanimously to maintain the interest rate paid on reserve balances at 4.4 percent, effective January 30, 2025. The Board of Governors of the Federal Reserve System voted unanimously to approve the establishment of the primary credit rate at the existing level of 4.5 percent, effective January 30, 2025.

It was agreed that the next meeting of the Committee would be held on Tuesday–Wednesday, March 18–19, 2025. The meeting adjourned at 10:10 a.m. on January 29, 2025.

Notation Vote

By notation vote completed on January 8, 2025, the Committee unanimously approved the minutes of the Committee meeting held on December 17–18, 2024.

Attendance

Jerome H. Powell, Chair

John C. Williams, Vice Chair

Michael S. Barr

Michelle W. Bowman

Susan M. Collins

Lisa D. Cook

Austan D. Goolsbee

Philip N. Jefferson

Adriana D. Kugler

Alberto G. Musalem

Jeffrey R. Schmid

Christopher J. Waller

Beth M. Hammack, Patrick Harker, Neel Kashkari, Lorie K. Logan, and Sushmita Shukla, Alternate Members of the Committee

Thomas I. Barkin, Raphael W. Bostic, and Mary C. Daly, Presidents of the Federal Reserve Banks of Richmond, Atlanta, and San Francisco, respectively

Joshua Gallin, Secretary

Matthew M. Luecke, Deputy Secretary

Brian J. Bonis, Assistant Secretary

Michelle A. Smith, Assistant Secretary

Mark E. Van Der Weide, General Counsel

Richard Ostrander, Deputy General Counsel

Trevor A. Reeve, Economist

Stacey Tevlin, Economist

Beth Anne Wilson, Economist

Shaghil Ahmed, Kartik B. Athreya, James A. Clouse, Brian M. Doyle, Carlos Garriga, Joseph W. Gruber, Anna Paulson, William Wascher, and Egon Zakrajšek, Associate Economists

Roberto Perli, Manager, System Open Market Account

Julie Ann Remache, Deputy Manager, System Open Market Account

Stephanie R. Aaronson, Senior Associate Director, Division of Research and Statistics, Board

Jose Acosta, Senior System Engineer II, Division of Information Technology, Board

Isaiah C. Ahn, Information Management Analyst, Division of Monetary Affairs, Board

David Altig,4 Executive Vice President, Federal Reserve Bank of Atlanta

Roc Armenter, Executive Vice President, Federal Reserve Bank of Philadelphia

Alyssa Arute, Assistant Director, Division of Reserve Bank Operations and Payment Systems, Board

Alessandro Barbarino, Special Adviser to the Board, Division of Board Members, Board

David Bowman, Senior Associate Director, Division of Monetary Affairs, Board

Jennifer J. Burns, Deputy Director, Division of Supervision and Regulation, Board

Michele Cavallo, Special Adviser to the Board, Division of Board Members, Board

Kathryn B. Chen,5 Director of Cross Portfolio Policy and Analysis, Federal Reserve Bank of New York

Andrew Cohen,6 Special Adviser to the Board, Division of Board Members, Board

Wendy E. Dunn, Adviser, Division of Research and Statistics, Board

Eric C. Engstrom, Associate Director, Division of Monetary Affairs, Board

Glenn Follette, Associate Director, Division of Research and Statistics, Board

Etienne Gagnon,4 Senior Associate Director, Division of International Finance, Board

Jenn Gallagher, Assistant to the Board, Division of Board Members, Board

David P. Glancy, Principal Economist, Division of Monetary Affairs, Board

Grey Gordon,4 Senior Economist, Federal Reserve Bank of Richmond

François Gourio,4 Senior Economist and Economic Advisor, Federal Reserve Bank of Chicago

Luca Guerrieri, Senior Associate Director, Division of International Finance, Board

Valerie S. Hinojosa, Section Chief, Division of Monetary Affairs, Board

Jane E. Ihrig, Special Adviser to the Board, Division of Board Members, Board

Benjamin K. Johannsen,4 Assistant Director, Division of Monetary Affairs, Board

Michael T. Kiley, Deputy Director, Division of Financial Stability, Board

Edward S. Knotek II, Senior Vice President, Federal Reserve Bank of Cleveland

Anna R. Kovner, Executive Vice President, Federal Reserve Bank of Richmond

David E. Lebow, Senior Associate Director, Division of Research and Statistics, Board

Sylvain Leduc, Director of Research, Federal Reserve Bank of San Francisco

Andreas Lehnert, Director, Division of Financial Stability, Board

Kurt F. Lewis, Special Adviser to the Chair, Division of Board Members, Board

Canlin Li, Senior Economic Project Manager, Division of International Finance, Board

Dan Li, Deputy Associate Director, Division of Monetary Affairs, Board

Laura Lipscomb, Special Adviser to the Board, Division of Board Members, Board

David López-Salido, Senior Associate Director, Division of Monetary Affairs, Board

Benjamin W. McDonough, Deputy Secretary and Ombudsman, Office of the Secretary, Board

Karel Mertens, Senior Vice President, Federal Reserve Bank of Dallas

Ann E. Misback, Secretary, Office of the Secretary, Board

Raven Molloy, Deputy Associate Director, Division of Research and Statistics, Board

Fernanda Nechio,4 Vice President, Federal Reserve Bank of San Francisco

Edward Nelson, Senior Adviser, Division of Monetary Affairs, Board

Anna Nordstrom, Interim Head of Markets, Federal Reserve Bank of New York

Julio L. Ortiz,4 Senior Economist, Division of International Finance, Board

Michael G. Palumbo, Senior Associate Director, Division of Research and Statistics, Board

Lubomir Petrasek,7 Section Chief, Division of Monetary Affairs, Board

Eugenio P. Pinto, Special Adviser to the Board, Division of Board Members, Board

Andrea Prestipino, Principal Economist, Division of Monetary Affairs, Board

Odelle Quisumbing,5 Assistant to the Secretary, Office of the Secretary, Board

Andrea Raffo, Senior Vice President, Federal Reserve Bank of Minneapolis

Nellisha D. Ramdass,4 Deputy Director, Division of Monetary Affairs, Board

Brett Rose,5 Treasury and Mortgage Markets Director, Federal Reserve Bank of New York

Zack Saravay, Senior Financial Institution Policy Analyst I, Division of Monetary Affairs, Board

Zeynep Senyuz, Special Adviser to the Board, Division of Board Members, Board

Benjamin Silk,4 Lead Financial Analyst, Division of International Finance, Board

Yannick Timmer, Principal Economist, Division of Monetary Affairs, Board

Paula Tkac, Director of Research, Federal Reserve Bank of Atlanta

Clara Vega, Special Adviser to the Board, Division of Board Members, Board

Annette Vissing-Jørgensen, Senior Adviser, Division of Monetary Affairs, Board

Jeffrey D. Walker, Senior Associate Director, Division of Reserve Bank Operations and Payment Systems, Board

Min Wei, Senior Associate Director, Division of Monetary Affairs, Board

Paul R. Wood,8 Special Adviser to the Board, Division of Board Members, Board

_______________________

Joshua Gallin

Secretary

1. The Federal Open Market Committee is referenced as the "FOMC" and the "Committee" in these minutes; the Board of Governors of the Federal Reserve System is referenced as the "Board" in these minutes. Return to text

2. Committee organizational documents are available at www.federalreserve.gov/monetarypolicy/rules_authorizations.htm. Return to text

3. The SLOOS results reported are based on banks' responses, weighted by each bank's outstanding loans in the respective loan category, and might therefore differ from the results reported in the published SLOOS, which are based on banks' unweighted responses. Return to text

4. Attended through the discussion of the review of the monetary policy framework. Return to text

5. Attended through the discussion of developments in financial markets and open market operations. Return to text

6. Attended the discussion of economic developments and the outlook. Return to text

7. Attended Tuesday's session only. Return to text

8. Attended through the discussion of developments in financial markets and open market operations, and from the discussion of current monetary policy through the end of the meeting. Return to text

EUR/JPY Technical: On the Verge of a Potential Bearish Breakdown After 6 Months of Consolidation

- The recent Euro strength in the past week has fizzled out.

- The ongoing trend of the 2-year yield premium shrinkage between the 2-year German Bunds over Japanese Government Bonds reinforced further potential downside in EUR/JPY.

- Watch the 155.45 downside trigger level of the EUR/JPY.

After a multi-month downtrend in the Euro Currency Index from the September 2024 high of 112.14 to the January 2025 low of 101.92, the Euro has started consolidating due to speculative net short positioning. The Euro futures market has seen a significant increase in net short positions of large speculators to -104,399 contracts in the recent two weeks as of 11 February 2025, close to a five-year low.

Hence, any positive related news flow such as last week’s looming peace talks negotiations between Russia and Ukraine brokered by US President Trump can trigger a rally in the EUR/USD and the Euro Currency Index via the partial closure of such significant leveraged net short positions in the Euro futures market.

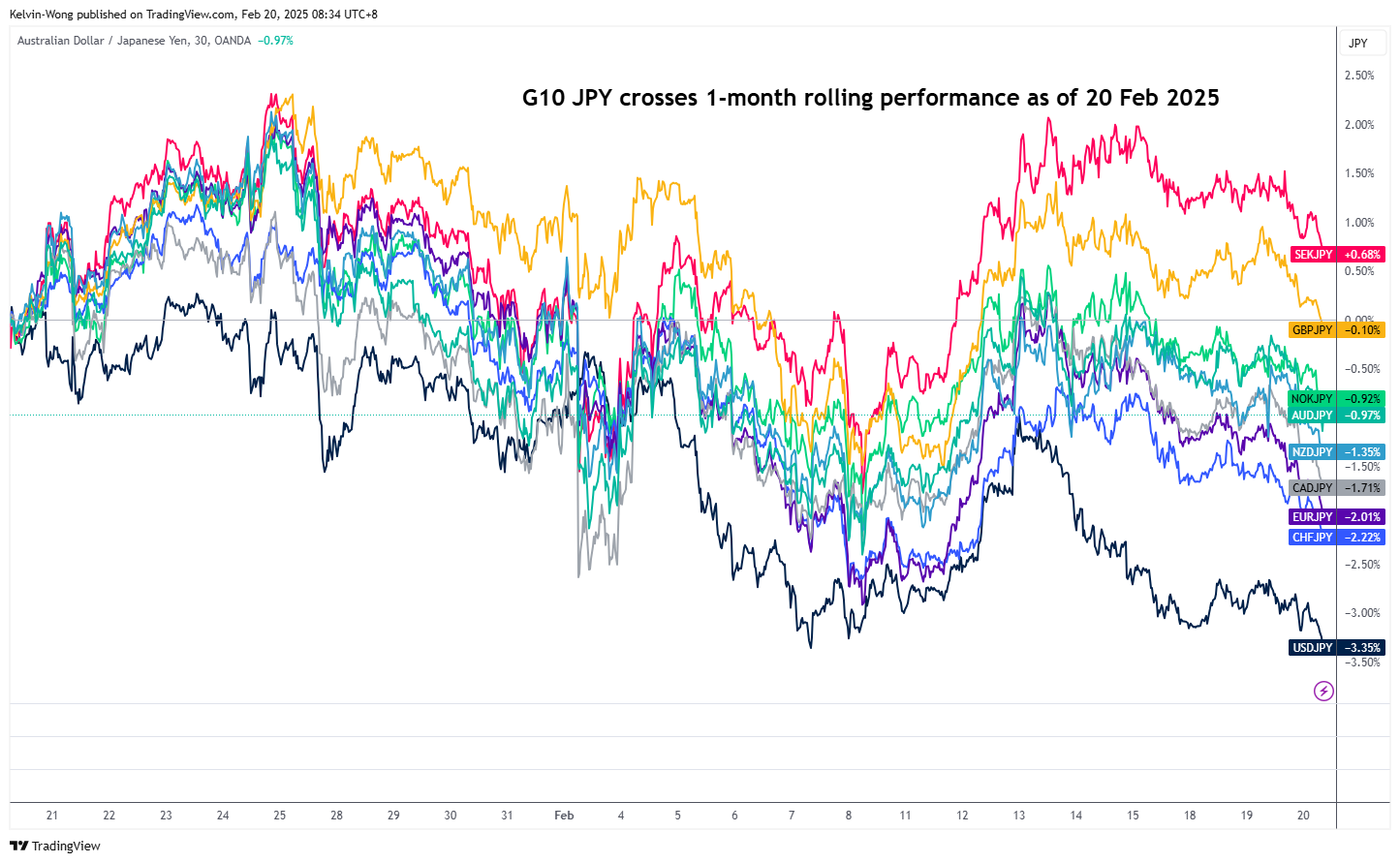

JPY has strengthened across the board in the past month

Fig 1: 1-month rolling performance of the JPY against major currencies as of 20 Feb 2025 (Source: TradingView, click to enlarge chart)

On the other hand, the Japanese yen has strengthened since mid-January 2025 after several prominent Bank of Japan (BoJ) officials, including Governor Ueda, talked up the yen which increases the odds of further interest rate hikes in 2025 with the possibility of two more hikes of 25 basis points each to raise the key policy short-term interest rate to 1% coupled with an improvement in wage growth and stable inflationary trend in Japan.

Therefore, an emerging medium-term Japanese yen strength trend has started to flash across the board in the currency market, one of the major yen cross pairs is the EUR/JPY.

Based on the one-month rolling performance, the EUR/JPY is the third worst performer (Japanese yen strength against Euro) among the major JPY crosses that shed -2% at this time of the writing (see Fig 1).

EUR/JPY is tracing out a major bearish reversal formation

Fig 2: EUR/JPY medium-term & major trend phases as of 20 Feb 2025 (Source: TradingView, click to enlarge chart)

Two significant technical analysis elements have emerged on the EUR/JPY. Firstly, it has broken below the former long-term secular ascending channel support from March 2022 low on 1 August 2024. Secondly, the price actions configuration of the swing highs of 16 November 2023, 11 July 2024, and 31 October 2024 has formed an impending major bearish reversal “Head & Shoulders” formation.

These observations suggest that the EUR/JPY is likely on the brink of a major trend change from bullish to bearish that may transform into a multi-month bearish trend phase.

In addition, the ongoing 2-year sovereign bond yield premium shrinkage between the German Bund and the Japanese Government Bond (JGB) also supports further potential weakness in EUR/JPY as Eurozone fixed income instruments are getting less attractive relatively versus Japanese fixed income.

Watch the 155.45 potential downside trigger level on the EUR/JPY (the neckline support of the major “Head & Shoulders” bearish reversal formation). A break with a daily close below it may open up scope to kickstart a major multi-month downtrend phase that may expose the next medium-term supports of 151.00 and 145.60 in the first step (see Fig 2).

On the other hand, clearance above the 163.80 key medium-term pivotal resistance invalidates the bearish scenario to see the next medium-term resistances coming in at 166.80 and 171.60.

Natural Gas Wave Analysis

- Natural gas broke resistance zone

- Likely to rise to resistance level 4.400

Natural gas recently broke through the resistance zone at the intersection of the resistance trendline of the daily up channel from November and the resistance levels 3.800 and 4.000 (which have been reversing the price from December).

The breakout of this resistance zone accelerated the active impulse waves iii, 3, which belong to the medium-term impulse wave (3) from November.

Given the clear multi-month uptrend, Natural gas can be expected to rise to the next resistance level 4.400 (target price for the completion of the active impulse wave (3)).

AUDNZD Wave Analysis

- AUDNZD reversed from the resistance zone

- Likely to fall to support level 1.1100

AUDNZD currency pair recently reversed from the resistance zone between the key resistance level 1.1165 (former monthly high from last November) and the resistance trendline of the wide weekly up channel from 2022.

This resistance zone was further strengthened by the upper daily and weekly Bollinger Bands.

Given the strength of the resistance level 1.1165, AUDNZD can be expected to fall to the next support level 1.1100.

Sunset Market Commentary

Markets

ECB executive board member Schnabel is the first to suggest that the direction of travel (of monetary policy) is not so clear anymore. She thinks that Frankfurt nears the point where it should start the discussion on pausing or halting rate cuts. Schnabel pointed out that an April rate cut is no longer fully priced in. Domestic inflation is still high and risks to the inflation outlook are somewhat skewed to the upside. She can’t say with confidence that monetary policy is still restrictive and suggests dropping that label from the policy statement at the March meeting. ECB president Lagarde hinted in the same direction at the January press conference. Schnabel downplayed the ECB study earlier this month on the level of neutral interest rates: “the ECB staff analysis that was published recently had one main message: we know that we know very little.” The theoretical concept of R* is therefore ill-suited to determine the appropriate policy stance. She also wanted to straighten out that the focus on the narrow 1.75%-2.25% outcome from the study was for models which estimated were available for Q4 2024. If you look at the R* estimates for the third quarter, you see that the range actually goes up all the way to 3%. Schnabel’s key message going forward is that maintaining price stability over the medium term is likely to require higher real rates in the future than before the pandemic. When talking about future ECB policy, she advocates one of the outcomes of the BoE’s Bernanke review: to make greater use of scenario analysis. Another key point is that the ECB should be more tolerate to both moderate downward and upward deviations from the 2% target and only act when there is a threat of de-anchoring. In between the lines, she suggests that the ECB might have overdone it in the past. Asset purchases for example have proven very effective in stabilizing markets, but haven been less beneficial and costlier than thought as a monetary policy instrument.

European bonds extend their underperformance today on the Schnabel comments. They add to the change of heart at ECB speak which based on language models examining policy statements, speeches,… started turning less dovish since the December policy meeting. EU swap rates add over 4 bps across the curve with German Bund yields climbing by up to 6 bps (5-yr). US Treasury yields on the contrary are broadly unchanged. The euro fails to profit from the yield differential with EUR/USD slipping from 1.0460 towards 1.0430 as European risk sentiment soured. Key European benchmarks drop over 1% after the EuroStoxx50 set a record high only last week. Tariff threats and disappointing earnings from a big US chemical player cause underperformance of industrials.

News & Views

The ECB today released EMU 2024 current account data. The euro zone current account surplus rose substantially last year to €419bn from €241bn. The rise in the nominal amount raised the surplus ratio in terms of GDP to 2.8% from 1.6% in 2023. The increase was mainly driven by a bigger surplus in the goods balance, rising from €256bn (1.6% of GDP) to €390bn (2.6% of GDP). The services balance showed a more modest rise from €123bn to €162bn (1.1% of GDP). The negative balance of the secondary income balance (redistribution of income via transfers for international aid and multilateral organizations, amongst others) declined slightly from -€170bn to -€165bn. The primary income balance was unchanged at €32bn. Regarding the financial account, EMU residents made net direct investments of €74bn. Non-residents divested net €102bn. Net purchases of non-euro area equity increased to €145bn, up from €89bn in 2023. Net purchases of non-euro area debt securities increased to €519bn, up from €380 bn. Non-residents’ net purchases of euro area equity increased to €350bn from €158bn in 2023. Over the same period, non-residents made net purchases of EMU debt securities amounting to €461bn, following net purchases of €398bn in 2023.

A survey of the Origo Group commissioned by the Swedish Riksbank mapping expectations among money market players, showed Swedish inflation expectations tentatively rising in February compared to January with the CPIF inflation at 1, 2 and 5 years rising to 1.9%, 2% and 2.2% respectively, all 0.1 ppt higher. Expectations for growth are also put higher at 2.2% for this year and 2.3% next year. Respondents anticipate the Riksbank policy rate to be higher in a medium term perspective (12 month 2.1% from 2%, 24 months 2.3% from 2% and 60 months 2.5% from 2.4%). The upward revision come as the Riksbank indicated that it could be at the end of its easing cycle.