Sample Category Title

Draining The Punch Bowl

Draining the Punch Bowl

Tuesday's session was all about the cross-asset selling of equities, oil, and bonds as bear “steepener” returned in vogue. The USD dollar remained tethered to a yo-yo string putting in a very mixed performance.

Stocks and Bonds

Stock markets are being pulverised recording their most significant two-day wobble since Jun 24, 2016, when Brexit rocked markets.

Highflying equity markets are falling back to earth as the reality sets in that global central banks are preparing to trim their bloated balance sheets and will finally begin to drain the party's punch bowl.

Rising bond yields head investors fear as the possibility of interest rates rising quicker than expected has stoked concerns of an extended equities market purge. Compounding the issues is that hedging becomes much more costly because of those very same interest rate expectations.

Unlike episodic bond sell-offs in 2017 that were little more than a series for a false start. The latest bond market fire sale is more than “false dawn” as the defining move on 10y UST's above 2.70 roiled markets and has many bracing for more volatility ahead. Especially with a burdening supply of US debt issues set to hit the markets in 2018 and beyond.

Few traders expected this sudden shift in Bond curve sentiment. Also, for the most part, they were planning to sleepwalk through this week's FOMC. To a degree, this may have contributed to a panicky move as markets adjust to a bearish bond market sentiment after spending years riding the bull thanks to central bank largesse.

Nevertheless, investors will be watching closely for any subtle change in Dr Yellen's language in language as any hawkish shift could cause another repricing on the rate curve and further squeeze equity markets.

Oil Markets

Oil prices slipped lower in early Asia trade after a more significant increase in US inventories than expected, according to the American Petroleum Institute.

While still holding on to fundamental positives from a crash in Venezuelan supply and OPEC compliance. The Elephant in the room is shale oil producers as their unlikely to sit idly hoping for higher prices. However, until that wave of tight oil materialises long-term speculators are unlikely to give up the plot as in the absence of a shale ramp, WTI could head north to $70.00 per barrel plus.

Gold Markets

There is no escaping this week FOMC folly, which will be the most significant driver of near-term sentiment. The Feds will keep its monetary policy unchanged. However, the makeup of the FOMC is changing so Yellen my deliver a hawkish surprise setting the stage for a possible policy pivot while trumpeting in the Powell era. Gold bears may take advantage of this move, as USD will strengthen unthinkingly. With the Central Banks taking centre stage, uncertainty around this crucial interest policy decisions will have more Gold investors taking to the sidelines until clearer signals develop.

March hike will not come as a surprise, but a quicker pace of Fed normalisation or even a shift in terminal rate thinking, possess the most significant risk to this nascent Gold rally.

Currency Markets

G-10 traders have a terrible case of the heebie-jeebies ahead of the FOMC, and Friday's payrolls data as the uptick in inflation rhetoric has traders thinking something will snap, or at a minimum, there will be a rapid unwinding of 2018 consensus currency trades ( short dollar vs everything ). Either way, it could be a case of picking your poison carefully and minimum getting some optionality in place regardless of the premiums.

With so much noise in the markets, it's becoming deafening, and there is no sign of let up as we now pivot the most significant noisemaker of them all, President Trump and the State of the Union. Address

The Australian Dollar

Without wasting ink, much is riding on today's CPI print, but with a measly five bps priced in the May RBA decision, it is too cheap relative to the current stream of economic data. Hence, the reason the Aussie is holding up well despite the shaky risk sentiments.

Malaysian Ringgit

The sudden aggressive shift higher in USD bond yields has caught more than a few investors off guard, but clarity will be a forthcoming post tomorrow mornings FOMC. If Dr Yellen indicates the Feds see an uptick in inflation pressure, this could pressure US interest rates higher and strengthen the USD over the short term.

However, since BNM is also moving on a path of interest rate normalisation, the MYR might be less sensitive to US yield than regional peers.

If that scenario plays out, then it will become a contest of economic data, and if the Malaysian economy counties to outperform, then the Ringgit should remain, stable to stronger.

Interest rates are only one part of the equation the other is equity inflow, and if the global economic environment remains risk friendly, then that will support regional sentiment.

Finally, higher oil prices remain supportive for the MYR, but with today's drop in price, it offered little support for the Ringgit but does not weigh negative at these higher levels.

Oil prices are moving lower this after the more significant increase in US inventories than expected, according to the American Petroleum Institute (API) said on Tuesday.

US Jobs And Fed To Guide Dollar

Dollar Lower Awaiting Employment Data and Fed Statement

Chair Yellen's Last Fed Meeting as Chair

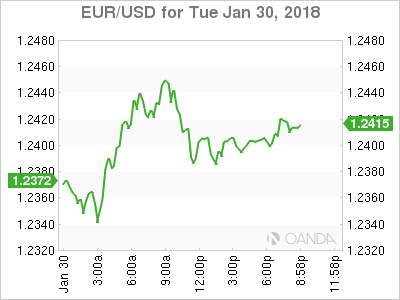

The USD is trading lower versus most majors ahead of US President Donald Trump's first State of the Union address, January's monetary policy statement from the US Federal Reserve and the ADP private payrolls report. Strong economic data from both sides has seen the EUR/USD gain in the last 24 hours with a little bit of help from the US Treasury secretary who said today that a strong dollar would be in the country's best interest.

- Trump will deliver his first State of the Union address

- US private payrolls forecasted to have added 191,000 jobs

- Fed expected to keep rates unchanged on Janet Yellen's last meeting as Chair

The EUR/USD gained 0.12 percent on Tuesday. The single currency is trading at 1.2396 after strong eurozone data was released today. The yearly GDP growth was higher than the estimate at 2.7 percent and validating the forecasts for an end of QE and higher rates by the end of the year. The European Central Bank (ECB) has tried to tone down optimism but the market is buying EURs as political uncertainty remains in the US despite strong fundamentals and tighter monetary policy.

European inflation has remained subdued and one of the main talking points by ECB President Mario Draghi. The European Consumer Price Index (CPI) estimate will be released by Eurostat on Wednesday, January 31 at 5:00 am EST. A higher than the expected 1.3 percent reading could further pressure the central bank to act sooner rather than later to shift from stimulus to tightening.

The U.S. Federal Reserve hiked three times in 2017 and is on track to do the same in 2018. Fed Chair Janet Yellen will step down later this week with Jerome Powell ready to assume the reigns of the central bank. With no press conference in the January meeting the market will be left to scan the statement looking for clues, but more will come in March when Powell helms his first Federal Open Market Committee (FOMC) and faces the financial press.

The ADP non farm payrolls report will be published on Wednesday, January 31 at 8:15 am EST. Economists are anticipating a gain of 191,000 jobs slowing down from the 250,000 gains in December. The ADP report will set further expectations for Friday's release of the U.S. non farm payrolls (NFP) expected to add 184,000 jobs after the disappointing 148,000 at the end of last year.

The USD has been on the back foot against major currencies for most of 2018. The rally that followed the victory of Donald Trump in the November 2016 elections was driven by tax reform and infrastructure promises. The 12 month period before the promise and the reality proved to be too much for a market that was expecting a quicker turn around and the greenback depreciated in 2017. This year follows a similar trend with the euro hitting three year highs and even the pound recovering to pre-Brexit levels thanks to a softer dollar.

Market events to watch this week:

Wednesday, January 31

8:15am USD ADP Non-Farm Employment Change

8:30am CAD GDP m/m

10:30am USD Crude Oil Inventories

2:00pm USD FOMC Statement

2:00pm USD Federal Funds Rate

Thursday, February 1

4:30am GBP Manufacturing PMI

10:00am USD ISM Manufacturing PMI

Friday, February 2

4:30am GBP Construction PMI

Gold Trading Sideways Ahead Of Fed Rate Statement

Gold has ticked lower in the Tuesday session. In North American trade, the spot price for an ounce of gold is $1339.51, down 0.13% on the day. On the release front, CB Consumer Confidence rose to 125.4, above the estimate of 123.2 points. Later on Tuesday, President Trump will deliver his State of the Union address before Congress. On Wednesday, there are a host of key indicators in the US, led by ADP Nonfarm Employment Change. The Federal Reserve will release a monetary policy statement, with the markets expecting the benchmark rate to remain unchanged at a range between 1.25%-1.50%.

Gold took advantage of last week's USD selloff, but the dollar has steadied this week. Gold moved higher earlier on Tuesday, but these gains were mostly wiped out after a superb consumer confidence report. CB Consumer Confidence continues to move upwards, as the US consumer is showing strong optimism about the economy. This has triggered stronger consumer spending, which led to a surge of imports in Q4, weighing on Advance GDP, which was softer than expected at 2.6%.

All eyes are on the Federal Reserve, which will make a rate announcement on Wednesday, the final one under Janet Yellen's watch. The tone of the rate statement could affect investor sentiment and have an impact on gold prices. It's a virtual certainty that the Fed will leaves rates unchanged this time around, although it's likely that the Fed will raise rates by a quarter-point at the March meeting. Yellen will make way for Jerome Powell, who takes over as chair in early February. Powell is expected to hold the course on monetary policy, which was marked by small, incremental interest rates in order to keep the robust US economy from overheating.

Yen Ticks Lower On Mixed Japanese Consumer Reports

The Japanese yen continues to have an uneventful week. In Tuesday's North American session, USD/JPY is trading at 108.91, down 0.04% on the day. On the release front, Japanese consumer indicators were a mixed bag. Household Spending disappointed with a decline of 0.1%, well off the estimate of 1.6%. There was better news from Retail Sales, which jumped 3.6%, beating the estimate of 2.1%. This marked the strongest gain since May 2015. On the inflation front, BoJ Core CPI rose 0.7%, its highest level since July 2015. Later in the day, Japan releases Preliminary Industrial Production, which is expected to post a strong gain of 1.5%. In the US, CB Consumer Confidence rose to 125.4, above the estimate of 123.2 points. Later on Tuesday, President Trump will deliver his State of the Union address before Congress. On Wednesday, there are a host of key indicators in the US, led by ADP Nonfarm Employment Change. The Federal Reserve will release a monetary policy statement, with the markets expecting the benchmark rate to remain unchanged at a range between 1.25%-1.50%.

The Federal Reserve will be in the spotlight on Wednesday. The markets will be keeping a close eye on the rate statement, the final one under Janet Yellen's tenure. It's a virtual certainty that the Fed will leaves rates unchanged this time around, although it's likely that the Fed will raise rates by a quarter-point at the March meeting. Yellen will make way for Jerome Powell, who takes over as chair in early February. Powell is expected to hold the course on monetary policy, which was marked by small, incremental interest rates in order to keep the US economy from overheating.

The yen has looked sharp in recent weeks, having gained 3.2% in January. Last week, a sell-off of the US dollar pushed the currency below the 109 level for the first time since September 2017. On Wednesday, US Treasury Secretary Steven Mnuchin put more pressure on the dollar when he stated that the US had no problem with a weak dollar. Mnuchin has since backtracked, saying that his words were taken out of context and that the US has a long-term interest in a strong dollar. President Trump added that Mnuchin was misinterpreted, but the yen has held its own against the struggling greenback.

WTI Oil Futures Correct Below 65; Scope to Extend Lower

WTI oil futures for March delivery broke below what was thought of as a strong support at the 50-period simple moving average of 64.67 in the 4-hour chart, hinting that further corrections could emerge in the near term. This followed unsuccessful efforts to crawl back to a three-year high of 66.63 reached last week.

The market is building negative momentum in the short-term as the RSI is below 50 and is heading lower, while the MACD is well below its signal line in bearish territory and the Tenkan-sen (red line) crossed below the blue Kijun-sen line.

Immediate support could now be provided by the 78.6% Fibonacci of 63.57 of the upleg from 62.75 to 66.63 and any additional losses from here could next find support at the previous bottom of 62.75.

Alternatively, a move to the upside could find resistance at 64.67, where the 50-period MA and the 50% Fibonacci are located. A substantial close above this level might drive prices back to the 20-period MA of 65.53, opening the way towards the three-year high of 66.63.

Chinese PMIs Pose Another Risk to the Aussie

China's official manufacturing and non-manufacturing PMIs for the month of January are both scheduled for release on Wednesday at 0100 GMT. According to forecasts, the manufacturing index is set to tick down, while the non-manufacturing print is anticipated to remain unchanged, albeit at a level consistent with healthy expansion in the sector.

Even though a slight slowdown in manufacturing activity would normally be perceived as a discouraging development for the Chinese economy, this may not be the case this time around. The economics community seems to be almost unanimous in anticipating Chinese economic growth to slow this year, as the nation restricts credit growth in order to deleverage the economy and address the financial stability risks that have been building in recent years. Bearing this in mind, a slight deceleration in the growth pace of the manufacturing industry could be perceived as normal, and may thus have little immediate impact in financial markets.

That said, however, any potential surprises in these prints do have the capacity to spur market movements. A more pronounced slowdown in manufacturing activity than what is anticipated, for example, or an unexpected downturn in the non-manufacturing index, could trigger a negative reaction in the yuan as well as in the Australian dollar. The Aussie is considered a liquid proxy for China's economic performance, as developments in China can have a major impact on Australia too, due to the close trading relationship between the two nations. Thus, a downside surprise in China's PMIs may push aussie/dollar lower. A potential downside break of the 0.8040 barrier - Tuesday's low with the area around it being congested in previous months - could pave the way for more downside extensions, perhaps towards the 0.8000 psychological territory.

On the other hand, should these data come in stronger than projected, we may see some concerns regarding a slowdown in China subside, triggering a positive reaction in aussie/dollar. In this scenario, buyers could push the pair higher for a test of its recent highs at 0.8135. If they prove strong enough to overcome that hurdle, then 0.8165 may be the next level to provide some resistance.

Finally, it should be noted that half an hour prior to the release of the Chinese PMIs (at 0030 GMT), Australia's inflation data for the fourth quarter will be released as well. Thus, any market movement in aussie/dollar at around that time may be affected by those prints too, as they could determine whether Australia's central bank will shift to an optimistic tone sometime soon, or whether it will remain sidelined for a while longer.

Fed Meeting Statement: Dollar Could Rebound on “Hawkish Hold”

Tuesday sees the Federal Reserve's Federal Open Market Committee (FOMC) commencing its two-day meeting on monetary policy, with a policy decision due on Wednesday at 1900 GMT. Markets widely expect rates to remain unchanged, though a delivery of a "hawkish hold" seems to increasingly be the view among analysts. Should this materialize, then the US currency is anticipated to post gains relative to other currencies.

Indicative of the broadly held view that rates will remain on hold is the fact that futures markets are currently pricing in a close to 95% chance for the federal funds rate to remain within the target range of 1.25% to 1.50%.

Despite the headline number of the preliminary estimate of US Q4 GDP growth coming in weaker than forecasted, overall there were reasons to cheer for after the reading's release on Friday January 26, with consumer spending that accounts for the largest portion of GDP expanding at its fastest rate in more than a year and spurring optimism moving forward. The improved economic outlook, combined with rising inflation expectations, are the factors lending support to those favoring the case for a hawkish take by Fed policymakers as the central bank's two-day meeting comes to an end, with of course a March rate hike - an outcome that is priced in for the most part by markets - anticipated to be clearly communicated.

Should a hawkish tone indeed prevail, then the US currency is likely to advance as market participants are expected to revise upwards their projections in terms of the number of quarter percentage point hikes to be delivered in 2018. The Fed's latest dot plot projected three such interest rate moves during the year, with the markets currently having priced in less than that. In this dollar-positive scenario, dollar/yen could meet resistance around the 110 handle, this being an area of congestion in recent months, as well as 110 being a level of potential psychological significance.

If the Fed's message falls short in terms of "hawkishness" however, then dollar/yen could continue its declines that saw it touch a four-and-a-half-month low last week. In this case, the aforementioned low of 108.27 could provide some support to the pair, with steeper falls shifting the focus to the 14½-month low of 107.31 that was recorded on September 8.

Wednesday's interest rate decision will be accompanied by the FOMC statement that investors will use to gauge Fed policymakers' outlook on the economy, inflation and thus the tightening cycle. No press conference will take place after the meeting, while fresh forecasts and projections (including the Fed dot plot) by FOMC policymakers will be released upon completion of the Fed's next meeting on March 21.

The current meeting constitutes Janet Yellen's last one as Fed chair, with Jerome Powell subsequently taking over the role. Powell, a Fed Board of Governors member, was dubbed by many as "Mr. Continuity"; barring adverse economic conditions that justify "outside-the-box" thinking, the Fed is projected to continue along the policy normalization path Yellen set under Powell's guidance.

Finally, it is worth noting that this is going to be a hectic week in terms of data out of the US, with the nonfarm payrolls report out of the world's largest economy also hitting the markets on Friday. Beyond economic releases, President Trump will be giving his first State of the Union address at 0200 GMT on Wednesday, with trade, infrastructure spending and immigration plans being among the expected topics of discussion. These too have the capacity to act as market movers for dollar pairs.

Sunset Market Commentary

Markets

The global core bond sell-off paused today, but there are no real signs of a comeback to challenge broken resistance levels in yield terms. German Bunds outperform US Treasuries. Core bond gains are limited given the downward correction on European equity markets, rumoured end-of-month extension buying and lower-than-forecast German CPI inflation (1.4% Y/Y vs 1.6% Y/Y). EMU eco data remained strong. Some investors remained sidelined ahead of president Trump's "State of the Union" (tonight) and the Fed meeting (tomorrow). Risks are that Trump advocates his America First policy more strongly than he did in Davos and that the Fed upgrades its economic/inflation assessment. Both factors are negative for US Treasuries. Changes on the German yield curve range between -1.3 bps (5-yr) and +0.4 bps (30-yr). The US yield curve bear steepens with yields 0.6 bps (2-yr) to 1.7 bps (30-yr) higher. 10-yr yield spread changes vs Germany are limited.

There were on follow-through gains on the USD rebound that started at the end of last week. This morning, the risk-off correction pushed USD/JPY, EUR/JPY and EUR/USD temporary lower but this classic risk-off trade evaporated soon. EUR/USD tested yesterday's low just below 1.2340. The test was rejected, triggering a new intraday short squeeze in the euro. The EMU eco data were mixed. Q4 GDP was strong as expected. German inflation was softer than expected. However, the data were of little importance for FX trading. Interest rate differentials also didn't provide guidance hovering near recent levels. USD caution prevails ahead of president Trump's 'State of the Union' tonight and the Fed policy statement tomorrow. The risk-off sentiment slightly favours the yen but the decline of USD/JPY (currently 108.50) develops in a very gradual way. The euro remains the 'by defaut' preferred choice as long as caution persists due to upcoming (US) event risk. EUR/USD trades in the 1.2440 area.

Sterling was in the defensive this morning. Negative headlines on the impact of Brexit and a new flaring up of political bickering inside the UK government weighed on the UK currency. EUR/GBP filled offers in the 0.8830 area, but selling gradually eased. UK monetary data were mixed. Mortgage approvals declined more than expected but had no negative impact on sterling. Cable rebounded as the dollar came again under pressure (currently 1.4130 area). EUR/GBP settles near 0.88. BoE governor Carney speaks before the economic affairs committee at CET 16.30.

European equities decline up 1% as investors ponder the potential impact from the recent rise in yields. US equities also continue yesterday's correction opening with losses of 0.75%/1.0%. Brent oil eases further to $69 p/b

News Headlines

The EMU economy expanded at its fastest rate in a decade in 2017 (0.6% Q/Q, 2.7% Y/Y) and EC EMU sentiment remained high at the start of 2018 despite a slight dip from a 17-year peak (114.7 from 115.3), signaling a strong start to the year. The 1y-ahead inflation expectations component within consumer confidence hit the highest level since February 2013. German inflation unexpectedly slowed for a second month in January (-1% M/M & 1.4% Y/Y), highlighting the challenge the ECB faces as it gauges when it can start unwinding stimulus..

Britain's economy will be worse off after Brexit whether it leaves the EU with a free trade deal, single market access, or with no deal at all, according to leaked analysis that fed the view that the government is badly prepared.

Germany's would-be coalition parties have reached a compromise on the divisive question of family reunions for migrants, both sides involved in the negotiations said, clearing a major hurdle in talks on a ruling partnership.

WTI OIL – Deeper Pullback Could Extend to Key $62.50 Fibo Support; US Oil Inventories Reports in Focus

WTI oil price stays in red for the second day and extends pullback, probing through initial support provided by rising 10SMA at $64.67.

Oil price was pressured by rising US shale oil output which weighs on OPEC-led efforts to drain oil market from excess supplies and boost oil prices.

Bearish divergence on daily indicators (RSI/MACD/slow stochastic) was negative signal with RSI and slow stochastic heading south after reversing from overbought territory and showing plenty of room downside.

Close below 10SMA today will be next bearish signal as weekly studies are also overbought and warn of correction.

Bears focus next supports at $64.08 (Fibo 23.6% of %55.81/$66.64 rally) and $63.88 (rising 20SMA), with further easing to pressure pivotal support at $62.50 (Fibo 38.2% of $55.81/$66.64). Correction should ideally reverse here to keep underlying bulls intact for fresh attempts higher as prevailing bullish sentiment keeps oil prices supported.

Near-term focus turns towards releases of US weekly crude stocks (API report is due late Tuesday) and EIA report which will be released on Wednesday.

Traders are looking for data to estimate the strength of demand for oil in the US, world's largest energy consumer, after recent data showed heathy demand which resulted in 10 straight weeks of draws in US crude inventories.

Res: 64.67; 65.54; 66.64; 66.75

Sup: 64.08; 63.88; 62.83; 62.50

CADJPY Approaches Ascending Trend Line; Bearish Correction in Progress

CADJPY remains under strong pressure after the pullback on the 89.60 resistance level on January 17. The pair plummeted towards the ascending trend line, which has been holding since September and dropped below the two-short-term simple moving averages, 20 and 40.

Looking at the daily timeframe, technical indicators are holding below their neutral levels. The MACD oscillator slipped below its trigger line in the bullish area, however, the RSI indicator is pointing to the downside in the negative territory.

If price action drops below the 23.6% Fibonacci retracement level of the last up-leg at 87.65 with the low of 74.80 and the high of 91.60, it could open the way for the next immediate support area 86.70 – 87.20. Clearing this key level would see additional losses towards the 38.2% Fibonacci mark, which stands near the 85.40 support barrier.

Upsides moves are likely to find resistance at the 89.60 obstacle. Rising above this area would help to endorse the focus to the upside towards the 4-month high of 91.60.