Sample Category Title

DAX Under Pressure After Global Stock Markets Slip

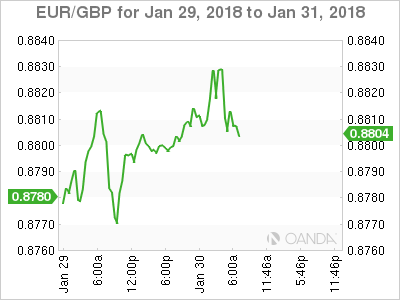

The DAX is showing little movement in the Monday session. Currently, the index is trading at 13,234.50, down 0.68% since the close on Monday. On the release front, Eurozone Preliminary Flash GDP for the fourth quarter remained unchanged at 0.6%, matching the forecast. Later in the day, the eurozone releases Preliminary CPI for Q4, with the markets braced for a decline of 0.5%. In the US, Consumer Confidence is expected to rise to 123.2 points. As well, President Trump will deliver his State of the Union address before Congress. Wednesday will be busy. Germany releases retail sales and the eurozone will publish CPI Flash Estimate. Investors will be keeping an eye on the Federal Reserve, which releases a monetary policy statement, with the markets expecting the benchmark rate to remain unchanged at a range between 1.25%-1.50%.

Eurozone numbers for fourth quarter 2016 remain solid, led by strong German data. Eurozone Preliminary Flash GDP posted a respectable gain of 0.6%, unchanged from the Q3 release. The markets are expecting some weak consumer numbers out of Germany this week, which could hurt investor confidence and send the DAX downwards. Preliminary CPI is expected to contract 0.5%, and retail sales is forecast to decline 0.4%. If the markets prove accurate and these indicators do point downwards, investors will be hoping that they are only blips, as eurozone and German consumer numbers have generally been strong.

Investors are also concerned about the streaking euro, which could hurt exports and affect company earnings. The euro posted strong gains on Wednesday, after US Treasury Secretary Robert Mnuchin said that the US had no problem with a weak dollar. ECB policymakers were not pleased with Mnuchin's statement, and Mario Draghi, without naming Mnuchin, said that such comments amounted to "targeting the exchange rate". Mnuchin sheepishly backtracked, claiming his remarks had been taken out of context and that he was in favor of a stronger dollar.

Dollar Stretches Losses ahead of Fed Meeting; Trump’s State of Union Speech in Focus

Here are the latest developments in global markets:

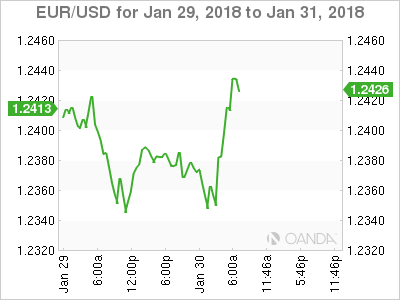

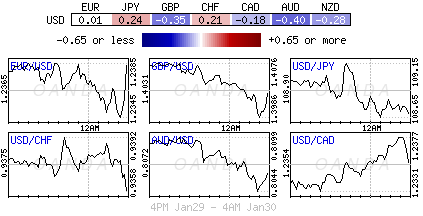

FOREX: The euro erased earlier losses against the dollar, bouncing up to an intra-day high of $1.2423 (+0.22%) after Eurostat revised upwards GDP growth readings for the third quarter. Sterling managed to rebound to $1.4111 (+0.38%) after reaching a one-week low at 1.3979 during the Asian session. On the other hand, the dollar, stretched its downleg towards 108.52 versus the yen (-0.31%) and reversed yesterday's gains against a basket of major currencies, falling to 89.08 (-0.27%) as Treasury yields firmed from recent peaks. The antipodean currencies, the kiwi and the aussie, also held onto gains on the back of a weaker dollar.

STOCKS: European stocks moved lower following their peers in Asia. The pan European STOXX 600 and the blue-chip Euro STOXX 50 were down by 0.45% and 0.58% in the day at 1100 GMT, with the majority of their components being in the red. The Spanish IBEX 35 tumbled by 0.93%, the German DAX 30 declined by 0.46%, the French CAC 40 retreated by 0.30% and the British FTSE 100 decreased by 0.56%. US future stocks were pointing to a negative open.

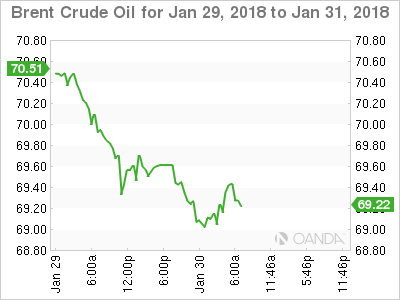

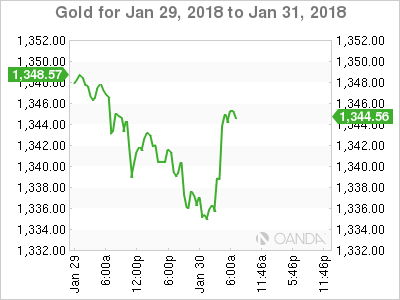

COMMODITIES: Oil prices extended their losses for the second day amid a strengthening dollar. WTI crude fell by 0.67% to $65.12/barrel and Brent slipped by 0.20% to $69.31/barrel. Gold was trading 0.20% higher at $1344.20 per ounce.

Day ahead: Fed starts monetary policy meeting; Trump delivers the State of Union address

Looking ahead in the day, the economic calendar will see the release of the German preliminary CPI figures for the month of January at 1300 GMT, with the inflation gauge turning negative in monthly terms for the first time since May.

In the US, stats on consumer confidence will attract attention at 1300 GMT. Analysts project the index to remain robust, rising from 122 to 123.1 in January. The markets will also keep a close eye on any potential monetary policy news as the Fed starts its two-day policy meeting today. However, expectations are for the central bank to maintain interest rates unchanged at the end of the meeting on Wednesday. Note that, this will be Janet Yellen's final meeting before Jerome Powell takes over the role as the new Fed chair. This could also be Yellen's chance to express more upbeat views on the US economy.

In other events today, the US President, Donald Trump, will deliver his first State of the Union address probably calling Republicans and Democrats to unify ahead of a government spending bill vote on February 8. He is also expected to highlight the country's upbeat economic performance and propose new legislative measures for the new year.

Bank of England Governor Mark Carney will be speaking before the House of Lords Economic Affairs Committee at 1530 GMT.

Japan will publish preliminary readings on industrial production for the month of December at 2350 GMT. According to forecasts, industrial output is anticipated to triple on a monthly basis.

In energy markets, API weekly report on US crude oil stocks will come into view at 2135 GMT.

The earnings season remains underway with pharma giant Pfizer being among companies releasing quarterly earnings on Tuesday.

Dollar Diddles For The Middle As Stocks See Red

Tuesday January 30: Five things the markets are talking about

Are surging sovereign interest rates testing individual's appetite for equities at elevated valuations or is it just another buying opportunity on dips?

European equities are currently following their Asian counterparts lower, while U.S stock futures retreat as the selloff in Treasuries eases and investors books some hard earned profits on this strong start to this New Year.

The 'mighty' dollar has again pared back some of this weeks early gains, while oil prices drop for a second consecutive day.

Tomorrow, Fed policy makers gather for Chair Janet Yellen's final meeting on interest rates before her term ends on Feb 3.

Later this evening, President Trump delivers his first State of the Union address (9 pm EDT) – he is expected to build momentum for legislation on infrastructure and immigration.

It's also jobs week stateside and on Friday U.S employers are expected to have added more jobs in January than in December (+184k vs. +148k).

1. Global equities see red

In Japan, the Nikkei share average dropped to a one-month low overnight, led by weakness in tech suppliers, while mining shares underperformed on lower oil prices. The Nikkei ended -1.4% lower, while the broader Topix fell -1.2%.

Down-under, broad selling across the region pushed Aussie stocks into negative territory for the month of January with one trading day left. The S&P/ASX 200 fell -0.9%, led lower by commodity names. In S. Korea, after three-straight record closing highs and five gains overall, the Kospi fell -1.2% and inline with the region's wide declines.

In Hong Kong, the Hang Seng posted its biggest one-day loss in six-weeks, as yesterday's Wall Street weakness prompted investors to book profits. At close of trade, the Hang Seng index was down -1.09%, while the Hang Seng China Enterprises index fell -1.98%.

In China, stocks extended their losses overnight, led by real estate and banking firms. At the close, the Shanghai Composite index was down -0.99%, while the blue-chip CSI300 index was down -1.07%.

In Europe, regional European indices are trading lower; following the lead from the U.S, but currently off the session lows.

U.S stocks are set to open in the red (-0.3%).

Indices: Stoxx600 -1.3% at 398.53, FTSE -0.4% at 7,639, DAX -0.2% at 13,299, CAC-40 -0.1% at 5,516; IBEX-35 -0.7% at 10,481, FTSE MIB -0.3% at 23,732, SMI +0.3% at 9,482, S&P 500 Futures -0.3%

2. Oil under pressure from a strong dollar, gold lower

Oil prices remain closely tethered to the dollar in an inverse relationship, and the greenback's gains this week, albeit off their highs vs. G10 currencies, is helping push crude oil futures lower.

Brent crude futures are down -20c to +$69.26 a barrel, after having touched a session low of +$68.75, while U.S West Texas Intermediate futures have dropped -51c to +$65.05 a barrel.

U.S rig-count data last Friday showed a big jump in U.S oil-drilling activity – which could lead to even more output and supply – is also weighing on prices.

Other factors that are expected to sway oil markets this week include tomorrow's FOMC decision, oil earnings from major oil companies and refiners, and weekly inventory reports.

Ahead of the U.S open, gold prices are under pressure for a second consecutive session, hitting its lowest in a week, as the U.S dollar strengthened a tad and U.S bond yields remain elevated. Spot gold is down -0.4% at +$1,335.49 per ounce, after a -0.7% drop in yesterday's session.

3. Sovereign yields remain elevated

The recent backup in the U.S 10-year Treasury note has prompted some dealers to declare an end to the bull market in bonds. However, the longest-dated Treasury's could suggest those calls may be premature.

With the yield on the benchmark U.S 10's rising above +2.70% yesterday, above its 2017 peak, the U.S long-bond, the 30-year yield, is at +2.949% – still well below its 2017 high of +3.194%.

The back up in the U.S belly reflects bets that recent U.S tax cuts will increase the pace of growth and inflation, prompting the Fed to hike interest at a faster pace. Looking at the U.S 30-year bond yield suggests that the longer-term outlook may not be quite so rosy. Owners of this duration indicate that they are not convinced that a prolonged surge in U.S growth and inflation lies ahead.

Note: The Fed's 'dot plot' forecasts three rate increases for 2018.

The odd's for a Fed hike in March – the first meeting this year that has a press conference and fresh projections outlook, is around +70%.

The yield on U.S 10-year Treasuries fell -1 bps to +2.69%. In Germany, the 10-year Bund yield has declined -2 bps to +0.67%, the first retreat in a week, while in the U.K, the 10-year Gilt yield declined -1 bps to +1.441% and the biggest fall in a fortnight.

4. 'Big' dollars mixed reaction

Ahead of the U.S open, the USD's price action is trading somewhat mixed. Initially the USD was firmer against the EUR (€1.2428) and GBP (£1.4083) as the session began in Europe aided by higher Treasury yields.

However, the rise in foreign sovereign yields yesterday has triggered a risk-off mentality and is supporting safe-haven currencies like JPY (¥108.55) and CHF ($0.9335).

Overnight, EUR/USD tested an intraday low €1.2335 before recovering, aided by various German State CPI data and stronger Euro GDP data (see below). Also supporting the 'single' unit is the German SPD and Merkel's party is said to have reached an agreement on refugee family's pact – a major hurdle for forming a German government.

GBP was softer in this morning's session with the weakness attributed to an internal U.K government Brexit analysis that concluded that the U.K would be worse off outside the E.U under every scenario modeled. The pound tested £1.3980 before finding some support.

Note: U.K 's PM Theresa May is said to be under growing pressure from the party's donors to quit as soon as the outline of trade deal is negotiated with the E.U in the autumn.

5. Euro, French and Spanish GDP (Q4)

Euro data this morning shows that Euro-zone GDP growth continued at a healthy pace in Q4. The so-called preliminary flash estimate of GDP showed that the economy expanded by +0.6% q/q, in line with the consensus expectation, but slightly slower than the +0.7% recorded in Q4, 2017.

Digging deeper, the breakdown for France and Spain indicates that the French economy's healthy expansion in Q4 rounded off a strong year, while tensions in Catalonia had little impact on Spanish growth.

The +0.6% increase in French GDP was slightly sharper than the consensus forecast of +0.5%, leading to an annual GDP growth of +1.9% for 2017.

Note: That's up from +1.1% in 2016 and marks the strongest year in six-years.

In France growth was broad-based, with consumer spending growing by +0.3% q/q, while investment growth accelerated, from +0.9% to +1.1%.

In Spain, GDP expanded by +0.7%, q/q in Q4. This was only marginally slower than the +0.8% recorded in Q3, suggesting that tensions in Catalonia had minimal impact.

EURUSD Now Intraday Bullish Above 1.2385

The euro has staged a dramatic reversal against the U.S dollar during the European trading session, with price-action now trading well above the 1.2385 level, after earlier finding strong dip-buying demand at the 1.2334 level. The U.S dollar index quickly reversed earlier gains, with the greenback now trading in lockstep with the broader U.S bond market. So far, the EURUSD pair has found intraday resistance around the 1.2420 level, with the next major upside resistance hurdles found at 1.2432 and 1.2470.

The EURUSD pair remains intraday bullish while trading above the 1.2385 level, major upside resistance is found at 1.2432 and 1.2470.

Should price-action on the EURUSD pair trade back below the 1.2385 level, a further decline towards 1.2360 and 1.2334 seems possible.

USDJPY Sellers Retain Control 108.98 Level

The U.S dollar remains under heavy selling pressure against the Japanese yen currency, as the Nikkei225 and broader equity markets suffer triple-digit intraday losses. Risk-on sentiment remains weak on Tuesday, limiting USDJPY upside, as financial markets fear a swift is underway, with investors rotating away stocks and into higher yielding bonds. Price-actions now sits close to the 108.50 level, as traders await a key-note speech from President Trump and key Industrial Production figures from the Japanese economy.

The USDJPY pair is heavily bearish while trading below the 108.98 level, further losses towards the 108.13 and 107.32 remain likely.

Should the USDJPY pair start to move above the 108.98 level, an upside correction towards 109.59 and 110.18 may ensue.

Euro Edges Higher, Eurozone GDP Matches Estimate

The euro has posted slight gains in the Tuesday session, offsetting the losses we saw on Monday. Currently, EUR/USD is trading at 1.2411, up 0.23% on the day. On the release front, Eurozone Preliminary Flash GDP for the fourth quarter remained unchanged at 0.6%, matching the forecast. Later in the day, the eurozone releases Preliminary CPI for Q4, with the markets braced for a decline of 0.5%. In the US, Consumer Confidence is expected to rise to 123.2 points. As well, President Trump will deliver his State of the Union address before Congress. Wednesday will be busy. Germany releases retail sales and the eurozone will publish CPI Flash Estimate. There are a host of key indicators in the US, led by ADP Nonfarm Employment Change. The Federal Reserve will release a monetary policy statement, with the markets expecting the benchmark rate to remain unchanged at a range between 1.25%-1.50%.

The euro posted strong gains last week, after US Treasury Secretary Robert Mnuchin said that the US had no problem with a weak dollar. ECB policymakers were not pleased with Mnuchin’s statement, and Mario Draghi, without naming Mnuchin, said that such comments amounted to “targeting the exchange rate”. Mnuchin has since backtracked, saying that his words were taken out of context and that the US has a long-term interest in a strong dollar. President Trump added that Mnuchin was misinterpreted, but these attempts at damage control haven’t had much effect, as EUR/USD has traded sideways since the Mnuchin comments.

The markets have become accustomed to GDP releases above 3.0% in the US, so Advance GDP for Q4 was disappointing. The reading of 2.6% fell short of the estimate of 3.0%. The economy grew 2.3% in 2017, compared to 1.6% in 2016. Growth in Q4 was affected by stronger consumer spending, which led to a surge in imports. At the same time, the increase in consumer spending also boosted inflation, as the personal consumption expenditures index, which the Fed prefers to use, rose 1.9% in the fourth quarter, up from 1.3% in Q3. Meanwhile, the US manufacturing sector is booming, as durable goods orders in December hit 2.9%, crushing the estimate of 0.6%. This was the highest gain in six months, and helped make 2017 a banner year. Durable good orders increased 5.8% in 2017, the sharpest expansion since 2011.

Technical Outlook: EURUSD – Solid EU GDP Data Supported Bounce Above 1.24

The Euro bounces above 1.24 handle after failure to break below Monday’s low at 1.2336, underpinned by rising 10SMA (1.2322) which stayed intact. Fresh advance cracked barrier at 1.2412 (Fibo 38.2% of 1.2537/1.2334 pullback) and pressuring base of thickening hourly cloud (spanned between 1.2424 and 1.2450). Extension of recovery rally from hourly double-bottom at 1.2335 needs lift above hourly cloud to turn near-term focus higher signal higher low formation at 1.2335. Solid EU GDP data released today gave fresh boost to the single currency. The Gross Domestic Product in the Eurozone rose 2.7% y/y, meeting the forecast while Q3 result was revised to 2.8% from initial release at 2.6%. The EU economy expanded at its fastest rate in a decade in 2017 and maintains positive sentiment at the beginning of 2018. Strong GDP data would further boost the Euro which holds in year-long uptrend from 1.0340 (Jan 2017 low) and recently probed above 1.2500 barrier, focusing target at 1.2597 (Fibo 61.8% retracement of 2014-2017 fall from 1.3992 to 1.0340).

Res: 1.2424, 1.2450, 1.2460, 1.2493

Sup: 1.2376, 1.2335, 1.2322, 1.2300

Market Update – European Session: Euro Zone Q4 GDP At Fastest Pace In A Decade

Notes/Observations

Rise in foreign yields yesterday triggered a risk-off sentiment in markets as participant ponder a trend in global monetary tightening; question begs considerable where the scope for bond yields rise before they weigh on growth and equities. US 10-year yield at 2.72% (highest since July 2017)

German State CPI data mixed but slowed down into year-end as expected by ECB - Euro Zone and Spain Q4 GDP data in-line with expectations

Euro Zone confidence misses expectations and moves off from recent cycle highs

Asia:

Japan Dec Jobless Rate: 2.8% v 2.7%e (1st rise since May) v 2.7% prior; Job-to-Applicant Ratio: 1.59 1.57 ((highest since Jan 1974)

Japan Dec Overall Household Spending Y/Y: -0.1% v +1.5%e

Japan Dec Retail Sales beat expectation with annual pace being fastest pace since April 2015 (M/M: +0.9% v -0.2%e; Retail Trade Y/Y: 3.9% v 2.1%e

Japan PM Abe Adviser Hamada: JPY currency (Yen) could 'firm' in short-term on factors such as US currency policy. Praises BoJ Gov Kuroda's handling of BoJ policy. Important that next BoJ Gov continue 'Abenomic's if not Kuroda (**Note: Kuroda’s current term ends on April 2018)

Europe:

ECB officials said to be assuming the QE program would be wound down over about 3 months (rather than suddenly halting the program). Even the hawkish members of the council were said to support a short taper period rather than a sudden halt to QE

Germany govt to raise 2018 GDP forecast from 1.9% to 2.4%

Brexit Min Davis: hope to have transition talks concluded by March summit; Brexit talks may extend a little longer than the Oct deadline

Unreleased, internal UK govt Brexit analysis: UK would be worse off outside the EU under every scenario modeled . A "No deal" scenario would cut growth by 8% over 15 years while a soft Brexit option would see growth cut by 2%

UK PM May said to be under growing pressure from the party’s donors to quit Downing Street as soon as the outline of trade deal was negotiated with the EU in the autumn

Americas:

President Trump State of the union address to address trade, immigration

Treasury Sec Mnuchin commented before Tuesday's Senate Banking Committee Testimony and reiterated Treasury could fund government into Feb

Economic Data:

(NL) Netherlands Jan Producer Confidence: 10.3 v 8.9 prior

(FR) France Q4 Advance GDP Q/Q 0.6% V 0.6%e; Y/Y: 2.4% V 2.3%e

(CH) Swiss Dec Trade Balance (CHF): 2.6B v 2.6B prior, Exports Real M/M: 2.8% v 0.4% prior, Imports Real M/M: 0.6% v 3.7% prior, Swiss Watch Exports Y/Y: 0.7% v 6.3% prior

(NO) Norway Dec Retail Sales W/Auto Fuel M/M: -1.0% v -0.5%e

(TR) Turkey Jan Economic Confidence: 104.9 v 95.3 prior

(FR) France Dec Consumer Spending M/M: -1.2% v -0.1%e v 2.2% prior; Y/Y: 1.0% v 1.6%e

(DE) Germany Jan CPI Saxony M/M: -0.8%% v +0.6% prior; Y/Y: 1.4% v 1.7% prior

(ES) Spain Q4 Preliminary GDP Q/Q: 0.7% v 0.7%e; Y/Y: 3.1% v 3.1%e

(CH) Swiss Jan KOF Leading Indicator: 106.9 v 110.8e

(HU) Hungary Dec Unemployment Rate: 3.8% v 3.8% prior

(DE) Germany Jan CPI Bavaria M/M: -0.7% v +0.5% prior; Y/Y: 1.8% v 1.7% prior

(DE) Germany Jan CPI Brandenburg M/M: -0.5% v -0.5%; Y/Y: 1.7% v 1.7%

(DE) Germany Jan CPI Hesse M/M: -0.8% v +0.6% prior; Y/Y: 1.3% v 1.7% prior

(IT) Italy Jan Consumer Confidence: 115.5 v 116.7e; Manufacturing Confidence: 109.9 v 110.5e, Economic Sentiment: 105.6 v 108.7 prior

(PL) Poland 2017 GDP Y/Y: 4.6% v 4.5%e

(DE) Germany Jan CPI North Rhine Westphalia M/M: -0.6% v +0.5% prior; Y/Y: 1.5% v 1.5% prior

(UK) Dec Mortgage Approvals: 61.0K v 63.5Ke

(UK) Dec Net Consumer Credit: £1.5B v £1.4Be; Net Lending: £3.7B v £3.3Be

(DE) Germany Jan CPI Baden Wuerttemberg M/M: -0.7% v +0.6% prior; Y/Y: 1.7% v 1.8% prior

(BR) Brazil Jan FGV Inflation IGPM M/M: 0.8% v 0.8%e; Y/Y: -0.4% v -0.4%e

(EU) Euro Zone Q4 Advance GDP Q/Q: 0.6% v 0.6%e; Y/Y: 2.7% v 2.7%e (fastest annual pace since 2007)

(EU) Euro Zone Jan Business Climate Indicator: 1.54 v 1.68e; Consumer Confidence (Final): 1.3 v 1.3e, Economic Confidence: 114.7 v 116.2e, Industrial Confidence: 8.8 v 8.9e, Services Confidence: 16.7 v 18.5e

Fixed Income Issuance:

(ID) Indonesia sold total IDR17.55T vs. 17T target in 2-month and 12-month bills and 5-year, 10-year and 15-year Bonds

(DK) Denmark sold total DKK3.16 in 1-month and 6-month Bills

(ZA) South Africa sold total ZAR3.3B vs. ZAR3.3B indicated in 2035, 2040, 2044 and 2048 bonds

(CH) Switzerland sold CHF376.1M in 3-month Bills; Avg Yield: -0.884% v -0.884% prior

(IT) Italy Debt Agency (Tesoro) sold total €6.25B vs. €5.25-6.25B indicated range in 5-year and 10-year BTP Bonds

Sold €1.75B vs. €1.25-1.75B indicated range in 0.9% Aug 2022 BTP bonds; Avg Yield: 0.66% v 0.60% prior; Bid-to-cover:1.61 x v 1.74x prior

Sold €4.5B vs. €4.0-4.5B indicated range in new 2.00% 2028 BTP bonds; Avg Yield: 2.06% v 1.83% prior; Bid-to-cover: 1.25x v 2.2x prior

(IT) Italy Debt Agency (Tesoro) sold €750M vs. €250-750M indicated range in 2.80% Mar 2067 BTPbond; Avg Yield: 3.19% v 3.44% prior; Bid-to-cover: 1.85x v 1.57x prior

(IT) Italy Debt Agency (Tesoro) sold €2.0B vs. €1.5-2.0B indicated range in Apr 2025 CCTeu (Floating Rate Note); Avg Yield: 0.42% v 0.48% prior; Bid-to-cover: 1.63x v 1.68x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -1.3% at at 398.53, FTSE -0.4% at 7,639, DAX -0.2% at 13,299, CAC-40 -0.1% at 5,516; IBEX-35 -0.7% at 10,481, FTSE MIB -0.3% at 23,732, SMI +0.3% at 9,482 , S&P 500 Futures -0.3%]

Market Focal Points/Key Themes:

European indices traded lower, following the lead from the US, but off the session lows.

Speakers

Spain PM Rajoy: Catalan Parliament is breaching its Constitutional Court order (**Note: Catalan separatists agreed to vote Puigdemont back into office remotely. Spain Constitutional Court on Jan 28th ruled that Puigdemont could only be selected if physically present in chamber)

German SPD and Merkel bloc said to reach an agreement on refugee families pact (removes a hurdle for forming a govt)

Turkey Central Bank Gov Cetinkaya presented its Quarterly Inflation Report (QIR) which reiterated to maintain its tight monetary policy stance until there was a convincing drop in inflation as core goods inflation increased notably due from TRY currency depreciation

Turkey Central Bank Quarterly Inflation Report Raised its 2018 CPI forecast from 7.0% to 7.9% and2019 CPI from 6.0% to 6.5%

South Africa ANC's national working committee (NWC) has instructed the party's top 6 officials to tell President Zuma to step down

Sweden Financial Supervisory Authority (FSA): Maintains counter-cyclical buffer at 2.0%

Thailand Central Bank noted that it had penalized some banks regarding THB currency (THB) speculation and was prepared to to review capital flow measures

China to hold its National People Congress (NPC) on March 5th - S&P affirmed New Zealand sovereign rating at AA; outlook stable

Canada Commerce Min Champagne: Cautiously optimistic on NAFTA meeting but toughest discussions remain

Currencies

USD price action was mixed. Initially the USD was firmer against the Euro and GBP as the session began in Europe aided by higher Treasury yields. However, the rise in foreign yields yesterday triggered a risk-off mentality and this aided safe-haven currencies like the yen and Swiss franc.

EUR/USD tested 1.2335 before recovering. Various German State CPI data showed above consensus reading for the month of Jan. helping to pull the Euro back towards the 1.24 area. Dealers note that German SPD and Merkel bloc said to reach an agreement on refugee families pact (removes a hurdle for forming a govt)

GBP was softer in the session with the weakness attributed to an internal UK govt Brexit analysis which concluded that the UK would be worse off outside the EU under every scenario modeled. The GBP/USD tested 1.3980 before finding some support.

Fixed Income

Bund Futures trades up 1 tick at 159.01 as stocks come under pressure and ahead of German CPI data. Continued upside targets 162.00, while a move lower targets the158.75 low.

Gilt futures trade at 122.62 up 15 ticks rebounding off the 122.28 lows. Support continues to stand at 122.25 then 121.75, with upside resistance at 123.75 then 124.33.

Tuesday’s liquidity report showed Monday’s excess liquidity rose to €1.885T from €1.874T prior. Use of the marginal lending facility rose to €65M from €50M prior.

Corporate issuance saw 4 issuers raise $6.4B in the primary market.

Looking Ahead

(BE) Belgium Jan CPI M/M: No est v 0.2% prior; Y/Y: No est v 2.1% prior

05.30 (UK) Weekly John Lewis LFL sales data

05:30 (EU) ECB allotment in 7-day Main Financing Tender (MRO) tender

05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

05:30 (BE) Belgium Debt Agency (BDA) to sell €1.3B in 3-month Bills

06:00 (PT) Portugal Dec Industrial Production M/M: No est v 0.8% prior; Y/Y: No est v 3.2% prior

06:00 (PT) Portugal Dec Retail Sales M/M: No est v 3.9% prior; Y/Y: No est v 4.8% prior

06:00 (IE) Ireland Jan Unemployment Rate: No est v 6.2% prior

06:00 (BR) Brazil Dec PPI Manufacturing M/M: No est v 1.6% prior; Y/Y: No est v 4.4% prior - 06:45 (US) Daily Libor Fixing

07:00 (ZA) South Africa Dec Budget Balance (ZAR): No est v -15.3B prior

07:00 (RU) Russia announces weekly OFZ bond auction

07:45 (US) Weekly Goldman Economist Chain Store Sales

08:00 (DE) Germany Jan Preliminary CPI M/M: -0.6%e v +0.6% prior; Y/Y: 1.7%e v 1.7% prior

08:00 (DE) Germany Jan Preliminary CPI EU Harmonized M/M: -0.7%e v +0.8% prior; Y/Y: 1.6%e v 1.6% prior

08:00 (HU) Hungary Central Bank (NBH) Interest Rate Decision: Expected to leave Base Rate unchanged at 0.90%

08:05 (UK) Baltic Dry Bulk Index

08:55 (US) Weekly Redbook Sales

09:00 (US) Nov S&P/ Case-Shiller 20-City MoM: 0.60%e v 0.7% prior; YoY: 6.35%e v 6.38% prior; House Price Index (HPI): No est v 203.84 prior

09:00 S&P Case-Shiller (overall) HPI YoY: No est v 6.17% prior; Overall HPI Index : No est v 195.63 prior

09:00 (EU) Weekly ECB Forex Reserves

09:00 (MX) Mexico Q4 Preliminary GDP M/M: +0.7%e v -0.3% prior; Y/Y: 1.6%e v 1.5% prior

09:00 (HU) Hungary Central Bank Gov Matolcsy post rate decision statement

09:00 (US) FOMC begins 2-day policy meeting (decision on Wed)

10:00 (US) Jan Consumer Confidence: 123.0e v 122.1 prior

10:30 (UK) BOE Gov Carney in Parliament - 11:30 (US) Treasury to sell 4-Week and 52-Week Bills

11:30 (LX) ECB’s Mersch (Luxembourg) in Frankfurt

15:00 (US) Jan Agriculture Prices Received: No est v 9.1% prior

16:30 (US) Weekly API Oil Inventories

18:00 (KR) South Korea Dec Cyclical Leading Index Change: No est v -0.1 prior

18:00 (KR) South Korea Dec Industrial Production SA M/M: 0.1%e v 0.2% prior; Y/Y: -2.0%e v -1.6% prior

18:50 (JP) Bank of Japan (BOJ) Summary of Opinions

18:50 (JP) Japan Dec Preliminary Industrial Production M/M: 1.5%e v 0.5% prior; Y/Y: 3.2%e v 3.6% prior

18:50 (JP) Japan Dec Loans & Discounts Corp Y/Y: No est v 3.1% prior

18:50 (JP) BOJ Summary of Opinions

19:01 (UK) Jan BRC Shop Price Index Y/Y: No est v -0.6% prior

19:01 (UK) Jan GfK Consumer Confidence: -13e v -13 prior

19:01 (UK) Jan Lloyds Business Barometer: No est v 28 prior

19:30 (AU) Australia Q4 CPI Q/Q: 0.7%e v 0.6% prior; Y/Y: 2.0%e v 1.8% prior; Trimmed Mean Q/Q: No est v 0.4% prior; Y/Y: No est v 1.8% prior

19:30 (AU) Australia Dec Private Sector Credit M/M: No est v 0.5% prior; Y/Y: No est v 5.4% prior

20:00 (CN) China Jan Govt Official Manufacturing PMI: 51.6e v 51.6 prior; Non-manufacturing PMI: 54.9e v 55.0 prior

20:10 (JP) BOJ Outright Bond Purchase in 1~3 Years; 3~5 Years; 10~25 Years and 25 Years

20:30 (JP) BOJ Iwata speech in Oita

21:00 (US) President Trump State of the union

21:00 (SG) Singapore Dec Bank Loans and Advances Y/Y: No est v 7.1% prior- 21:00 (SG) Singapore Dec Credit Card Bad Debts (SGD): No est v 24.0M prior; Credit Card Billings: No est 4.929B prior

21:00 (SG) Singapore Dec M2 Money Supply Y/Y: No est v 3.2% prior; M1 Money Supply Y/Y: No est v 7.3% prior

22:00 (CN) China to sell 1-yeasr and 10-year government bonds

22:30 (TH) Thailand Dec Manufacturing Index: 2.9%e v 4.2% prior; Capacity Utilization: No est v 64.2% prior

23:00 (JP) Japan Dec Vehicle Production Y/Y: No est v 0.9% prior

Bitcoin Unable To Break $10,000, Is Upward The Only Way!

Is it time for Bitcoin to reverse momentum?

After recovering during the weekend, the price of Bitcoin has reversed momentum since Monday, sliding 6.10% from $11,770 to $11,040. Following early January dell-off – and just like Bitcoin - the entire crypto-market has been trading sideways since mid-January. However, performances of alt-coins has been quite heterogeneous as certain projects are expected to release major update or/and building expectations for major announcement in the first quarter (Populous, OmiseGo NEO/GAS or Walton); while for others, price have kept grinding lower as no major update are expected in the coming months (e.g. LINK). Wanchain, that is seeking to create a new distributed financial structure, which would allow among other features to allow cross-chain smart contracts, is expected to be ready for trading soon. Since yesterday, ICO investors have the possibiblity to swap their ERC20 tokens to Wanchain Mainnet Wancoins. Therefore, this is just a matter of hours (or maybe a couple of days) before Wancoins is available for trading. It is going to rise fast!

Bitcoin has suffered from bearish bets from speculators, with leveraged funds being net short Bitcoin most since the introduction of Bitcoin futures in December last year. However, according to the last CFTC report released last Friday, the wind is turning slowly as leveraged funds are now net long Bitcoin by 624 contracts. In addition, the price of Bitcoin has been unable to break the $10,000 threshold in spite of numerous attempts. After two weeks of consolidation, we believe that the bear market is over that the momentum will reverse in the coming days.

US GDP Growth disappoints

Friday’s Preliminary 4Q 2017 US Gross Domestic Product publication is deceiving and lies below expectations at 2.60% (consensus: 3.0%; real GDP at 2.30% and +1.50% in 2016) while December core PCE Y/Y stands at 1.50% (3Q: 1.35%), signaling a relatively weak performance, lower than 3Q GDP of 3.20%. With a December Personal Income M/M increase of 0.40% (0.30% consensus) and Household Real Consumption of 3.80% (consensus: 3.70%; fastest pace since 2014 while savings fell at 2.40%, lowest since September 2005) confirms that US consumption steered expansion during the last quarter of the year, also supported by Trump’s tax reform outlook and US global market optimism in the stock market. However, the drawback of this consumption boost is the increasing import rate (November 30th 2017 Y/Y: 8.40% and October 31st 2017 Y/Y: 7.0%) that underscores annual GDP.

Weakening USD (USD/EUR -2.38%, USD/GBP: -3.48%, USD/JPY: -3.09% and USD/CHF: -4.09%) might however be a driver to the 3% GDP growth target of Trump’s administration. Due to almost full employment conditions within the US economy (US December Seasonally Adjusted Unemployment rate at 4.10%, its lowest rate since December 31st 2000), effective corporate tax reform contribution (from 35% to 21%) to GDP growth remains limited for further growth. Government total expenditures also largely contributed to actual growth within the US economy, accounting for USD 6’586.71 billion (+1.027% increase from Q3 to Q4 2017) and remains at historical highs.

CRUDE OIL Slight Decrease

Crude oil is slightly declining, though maintained above 64. Strong support is given at 60.93 (05/01/2018 low). Expected to keep increasing as demand remains strong.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness is very likely. For the time being the pair lies in an upside trend since June 2017. Support lies at 42.20 (16/11/2016) while resistance point is located at 77.83 (20/11/2014). Crude oil is trading largely above its 200 DMA.