Sample Category Title

Currencies: Will Fed Help To Stop The USD Bleeding?

Sunrise Market Commentary

- Rates: Steeper US yield curve after Fed meeting?

The market implied probability of a Fed rate hike tonight is 20%. We expect the Fed to postpone a continuation of its tightening cycle to March, but upgrade its assessment on the economy and on inflation. This combination could trigger a steepening of the US yield curve with a short term downward correction at the front end and higher rates at the 10y. - Currencies: Will Fed help to stop the USD bleeding?

The dollar failed to build on the bottoming out process that started at the end of last week. Today’s eco calendar is well filled, but the focus turns to the Fed statement. We expect the Fed to upgrade its assessment on growth and on inflation. Will this be enough to help to put a floor for the dollar?

The Sunrise Headlines

- US stock markets corrected around 1% lower yesterday with Dow Jones underperforming. The sell-off eases overnight bar Japan. Strong Samsung earnings and the announcement of a stock-split cause Korean outperformance.

- In his first State of the Union, President Trump again called for a bill that would underwrite a program to repair the nation’s infrastructure, relying on state/local government funding along with private investment that would add up to $1.5tn.

- The BOJ offered to buy more bonds (3-5y tenor) at a regular operation for the first time since July, helping to bring down yields and weaken the yen as Governor Kuroda reaffirmed a commitment to his ultra-loose monetary policy

- Powerful German union IG Metall has called for full-day walkouts through Friday, firing a last warning shot before it ballots for extended industrial action amid a dispute over wages and working hours.

- China’s manufacturing sector grew at a slower pace than forecast in January (51.3 vs 51.6) as output and new orders dipped. The non-manufacturing PMI unexpectedly improved from 55 to 55.3.

- Australian CPI rose 0.6% Q/Q in Q4, undershooting 0.7 Q/Q forecast and unchanged from the September quarter. Inflation rose 1.9% on a yearly basis, below 2% consensus but picking up from a 1.8 Y/Y increase.

- Today’s eco calendar contains EMU inflation data, German unemployment figures, US ADP employment change, Chicago PMI and the Fed meeting. Germany taps the market and ECB Coeuré is scheduled to speak

Currencies: Will Fed Help To Stop The USD Bleeding?

Will Fed help to stop the USD bleeding?

The dollar was again the defensive yesterday. EUR/USD rebounded off the 1.2335/37 ST lows. The traded-weighted USD also didn’t make any headway. EMU eco data were mixed with German inflation printing soft. US consumer confidence was OK, but didn’t support the dollar. Investors stayed cautious ahead of Trump’s State of the Union and today’s Fed statement. A further correction of US equities had little impact on USD. USD/JPY held up well, closing at 108.78. EUR/USD closed at 1.2405.

Overnight, US president Trump didn’t bring many details on policy. He asks Congress $1.5tn for infrastructure spending. The BOJ offered to buy more bonds at a regular operation. BOJ’s Kuroda committed to further policy easing in order to reach the 2% target. The BOJ tries to counter recent speculation on a reduction in policy stimulation. USD/JPY temporary revisited the 109 barrier, but trades again in the 108.70 area. EUR/USD trades (1.2440) with a cautious upward bias.

Today, the calendar contains the German & EMU labour data and the EMU CPI. CPI is expected to ease to 1.2% from 1.4%, but will this change fortunes of the euro? The reaction to the US ADP labour report and the Chicago PMI will probably be muted just hours ahead of the FOMC statement. We see risks for the Fed to indicate better growth prospects and more conviction on reaching the inflation target. In theory this should confirm the recent uptrend in US yields and be supportive for the dollar. However, of late the greenback reacted very muted to supportive news. So, we look out whether this time is different. From a technical point of view, EUR/USD 1.2537/98 marks important topside resistance. A break would signal more trouble for the dollar. A sustained return below 1.2323/1.2165 improves the ST picture for USD.

Sterling trading faced conflicting signals yesterday. A new discord within the conservative party on Brexit and calls for PM May to resign were sterling negative. On the other hand, BoE’s Carney indicated that the bank could give more weight to bringing inflation back to target, raising chances for a next rate hike later this year. EUR/GBP declined further off the 0.88 area after the Carney comments. Overnight, UK eco data were mixed to marginally above consensus. For now we expect EUR/GBP to hold the 0.8690/0.8928 consolidation pattern. A topside break has become less evident after Carney’s comments

USD (DXY-trade-weighted) holding near recent low

Bitcoin Falls Below $10,000 Again

It has been a sad month for bitcoin. This month, its price has fallen from a high of $17,159 to a low of $9218. As of this writing, bitcoin is currently trading at $9818.

Bitcoin has faced multiple problems this month with South Korea being the biggest one as the nation started a crackdown on exchanges.

Another problem was the eventual realization that bitcoin was ‘probably’ not a better alternative to fiat currency. As you know, bitcoin was invented to create a decentralized mode of payment, free from any regulatory authority. Bitcoin has however become inefficient in terms of speed and costs of transactions. A new report by CNBC found that bitcoin’s popularity was waning among crooks who are now shifting to other currencies like Litecoin and ethereum.

The problems keeps on coming. Last week, Weiss Ratings released its first ratings on cryptocurrencies. Bitcoin received a weak C rating, below Ethereum, which received a B.

Yesterday, Facebook announced that it would stop accepting adverts from all bitcoin-related companies, ICOs, and promotions. To many people in the cryptocurrencies space, this is major news because they use Facebook to reach to millions of users.

As shown below, from a monthly chart, bitcoin seems to be forming an asymmetrical triangle formation. It is also trading lower than the 50-period moving average and in line with the 14-day MA. These moves are an indication that consolidation is happening in the bitcoin/dollar pair. This means the price could break the barrier in either direction.

EURO Further Bullish Above 1.2432 Level

The euro continues to hold well-above the 1.2400 level against the U.S dollar, as traders keep positioned into the overall long-term uptrend in pair, with strong bullish momentum well intact above the pivotal 1.2385 level. The EURUSD is again benefiting from weakness in the greenback on Wednesday, as the U.S dollar lags-behind ahead of the FOMC interest rate decision and policy statement later today. During the upcoming European trading session, we see a slew of high-impacting data, with the release of eurozone and German CPI Inflation and Unemployment figures.

The EURUSD pair will likely extend upside gains above the 1.2432 level, intraday resistance is currently found at 1.2470 and 1.2538.

Should the EURUSD start to falter around the 1.2432 level, we may see another correction towards the 1.2385 and 1.2355 levels.

GBPUSD Reversal Only Bullish Above 1.4130 Level

The British pound has moved sharply higher against the U.S dollar, with price-action now fast approaching the 1.4200 technical level, after a sharp reversal in direction on Tuesday. The GBPUSD pair found strong dip-buying demand from the 1.3979 level, with pair rallying strongly on a return of U.S dollar weakness and bullish comments from UK PM Theresa May, who denied rumours of a leadership challenge. Going forward sterling traders will look to the release of the ADP Jobs Report and the FOMC Interest Rate Decision and Policy Statement.

The GBPUSD pair remains strongly bullish while trading above the 1.4130 level, upside resistance is now found at 1.4220 and 1.4284.

Should price-action on the GBPUSD pair fall back below the 1.4130 level, key technical support is found at 1.4082 and 1.4033.

Wednesday Is Fed Day

The month of January is going out with a bang on Wednesday, as investors monitor a deluge of economic data and a key rate announcement from the US Federal Reserve.

In terms of economic data, the German government will get the ball rolling at 07:00 GMT with its monthly report on retail sales. Receipts at retail stores are forecast to fall 0.3% in December, following a 2.3% increase the month before.

Over the next several hours, reports on French producer inflation, German unemployment and Italy's labour market will make headlines. The European Commission's statistical agency will also report on unemployment and consumer inflation for the 19-member currency zone.

The Eurozone consumer price index (CPI) is forecast to fall to 1.3% annually in January, down from 1.4% the previous month. So-called core inflation, which strips away volatile goods such as food and energy, is projected to slip to 1% from 1.1% in December.

In North America, ADP Inc. will release its preliminary US jobs report at 13:15 GMT. ADP is expected to show the creation of 185,000 private sector jobs in January, following a gain of 250,000 the month before.

Other US reports on Wednesday include pending home sales and the Chicago purchasing managers' index.

The US Federal Open Market Committee (FOMC) will hand down its policy statement at 19:00 GMT. Although interest rates are expected to hold steady at 1.5%, officials could provide clues about the pace and timing of future adjustments. Last month, the FOMC forecast three additional rate hikes for 2018.

Earlier in the session, China's official manufacturing PMI survey showed slight weakness in factory output. The manufacturing PMI slid to 51.3 in January from 51.6 the month before.

A separate PMI gauge tracking service activity strengthened to 55.3 from 55.0.

Meanwhile, US President Donald Trump delivered his first State of the Union address In Washington, where he promoted his infrastructure plan and indicated an intent to work with Democrats on immigration. Trump's first year in office was highly contentious politically but was very well received by Wall Street.

EUR/USD

The euro has carved out a rangebound pattern against the dollar this week, with prices fluctuating between 1.2400 and 1.24500. The outlook remains firmly positive after the common currency surged to multi-year highs last week.

GBP/USD

Cable has ebbed slightly lower this week, as prices peeled back from multi-year highs. The GBP/USD exchange rate was last seen trading at 1.4149, having declined roughly 150 pips from last week's highs.

USD/JPY

The dollar put up a mild rally against the yen on Tuesday but failed to hold gains above 109.00. The USD/JPY was last seen trading around 108.80, where it continued to face firm downside pressure.

Market Update – Asian Session: China PMIs Remain In Expansion

Headlines/Economic Data

General Trend:

Samsung Electronics rallies over 5% amid planned stock split

Australian Telecoms and REITs outperform amid Q4 inflation data

Australia CPI remains below RBA target of 2-3%

China Jan PMI data mixed (manufacturing below ests, services above ests)

BoJ raises daily purchases of 3-5 year JGBs

US Fed decision later today

Japan

Nikkei 225 opened -0.4%; closed -0.8%

(JP) Japan's Topix passes 1,900 for the first time since 1991

TOPIX Real Estate Index -1.2%, Iron & Steel -1.1%

Canon [7751.JP]: Trades higher by over 2% (guided FY Op profit above ests)

Daiwa Securities [8601.JP]: Gains over 1% after 9-month results

Chip equipment firm Tokyo Electron [8035.JP]: Declined over 3% (reported profits below ests)

(JP) Bank of Japan (BOJ) Summary of Opinions from Jan 22-23rd meeting: May need to consider rate adjustment if economy, prices improve

(JP) Japan Dec Prelim Industrial Production M/M: 2.7% v 1.5%e (highest since April 2017) ; Y/Y: 4.2% v 3.2%e

(JP) Bank of Japan (BoJ) Gov Kuroda: taking time to change Japan deflationary mindset; will persistently continue easing for price goal – Parliament

(JP) BoJ Deputy Gov Iwata: Still some distance from 2% inflation target; need to continue with powerful monetary easing

(JP) BOJ announcement related to daily bond buying operation: raises daily purchases of 3-5 year JGBs to ¥330B v ¥300B prior

Korea

Kospi opened -0.4%

Samsung Electronics gains over 5% amid planned stock split, final Q4 results and outlook

(KR) US ITC finds certain South Korea tapered roller bearings are being dumped – press

(KR) According to a scholar, South Korea should consider restricting imports of US liquefied natural gas (LNG) in response to US safeguard measures

(KR) SOUTH KOREA DEC INDUSTRIAL PRODUCTION M/M: -0.5% V +0.1%E; Y/Y: -6.0% V -1.5%E

Samsung Electronics, 005930.KR Reports final Q4 (KRW) Net 12.0T v 12.1Te, Op 15.15T v 15.1T prelim ; Rev 65.98T v 66.0T prelim; Guides FY18 Capex to be lower y/y; Planning 50:1 stock split

China/Hong Kong

Hang Seng opened -0.5%, Shanghai Composite -0.5%

Hang Seng Information Tech Index +1%, Financials +0.6%; Energy -0.8%, Property/Construction -0.7%

(CN) CHINA JAN GOVT OFFICIAL MANUFACTURING PMI: 51.3 V 51.6E; NON-MANUFACTURING PMI: 55.3 V 54.9E

(CN) China to address price collusion in the areas of natural gas and auto – China Daily

(CN) PBoC: Skips OMO (5th straight session) v skipped prior; Net drain CNY210B v CNY240B drain prior

USD/CNY (CN) PBOC SETS YUAN REFERENCE RATE AT 6.3339 v 6.3312 PRIOR

(CN) Moody's: New US tax cuts have limited credit implications for China and Chinese companies

(CN) China MoF sells 1-yr at 3.38%, bid to cover 2.95x and 10-yr bonds at 3.85%, bid to cover 3.09x

Looking Ahead: China Jan Caixin Manufacturing PMI due for release on Thursday

Australia/New Zealand

ASX 200 opened -0.1%; closed %

ASX 200 Telecom Services Index +1.7%, REIT +1.2%, Financials +0.2%; Resources -1%, Energy -0.9%

(AU) AUSTRALIA Q4 CPI Q/Q: 0.6% V 0.7%E; Y/Y: 1.9% V 2.0%E; TRIMMED MEAN Q/Q: 0.4% V 0.5%E; Y/Y: 1.8% V 1.8%E

(NZ) New Zealand Finance Min Robertson: Drop in business confidence is not unusual, reflects change of government; Budget to be delivered on May 17th

Sirtex Medical, SRX.AU To be acquired by Varian Medical System for A$28/shr in cash; enterprise value ~A$1.58B (~49% premium vs prior close); Varian sees deal accretive to EPS in first full year; +46%

North America

US equity markets ended broadly lower: Dow -1.4%, S&P500 -1.1%, Nasdaq -0.9%, Russell 2000 -1.0%

S&P 500 Health Care Sector -2.1%, Energy -2%

Xerox [XRX]: Gained over 7% in the afterhours: Said to be close to a deal with FujiFilm for cash and implied premium of shares, Xerox shareholders would continue to own just under 50% of the new company

Xerox [XRX]: Japan’s FujiFilm declined comment on the report

(US) US President Trump: US seeing rising wages on strength of economy; Wants Congress to produce legislation that generates at least $1.5T for new infrastructure investment. - State of the Union Address

(US) Treasury Sec Mnuchin: Reiterates target of sustained GDP growth of 3% or more; A strong dollar is in the long-term interests of the US; supports free FX markets with no intervention - Senate testimony

(US) Weekly API Oil Inventories: Crude: +3.2M v +4.8M prior

Looking Ahead: US Fed decision due on Wednesday, along with Jan ADP Nonfarm Employment Change, Jan Chicago PMI and Weekly DoE Crude Inventories

Europe

(UK) BOE Gov Carney: UK economy's outperformance versus BOE's Aug outlook is because of a stronger world economy and looser fiscal stance than expected

(UK) PM May confirms seeking trade deal with China - speaking on plane to China

(UK) Ahead of PM May arrival in China, she warned China it must play by global rules, including intellectual property rights, if it is to maximize new trading opportunities with Britain and the west - FT

(UK) Jan BRC Shop Price Index Y/Y: -0.5% v -0.6% prior

(UK) Jan GfK Consumer Confidence: -9 v -13e

(UK) Jan Lloyds Business Barometer: 35 v 28 prior

(EU) ECB's Knot (Netherlands): it's reasonable to end QE in a short taper after Sept

(DE) ECB’s Weidmann (Germany): German surplus will shrink as investment rises

(EU) ECB's Mersch (Luxembourg) discusses limits of central bank financing in resolution proceedings

Levels as of 01:00ET

Nikkei225 -0.8%, Hang Seng -0.0%; Shanghai Composite -0.6%; ASX200 +0.3%, Kospi +0.3%

Equity Futures: S&P500 +0.1%; Nasdaq100 +0.1%, Dax +0.2%; FTSE100 +0.0%

EUR 1.2434-1.2397; JPY 109.09-108.69; AUD 0.8105-0.8047;NZD 0.7387-0.7327

Feb Gold +0.4% at $1,340/oz; Mar Crude Oil -0.9% at $63.91/brl; Mar Copper +0.2% at $3.19/lb

Forex Analysis: Trump’s First State Of The Union Address Strikes Positive Tone

President Donald Trump delivered his first State of the Union Address last night from Capitol Hill. He said that he wants Congress to produce legislation that generates at least $1.5 trillion for new infrastructure investment. Every federal dollar for infrastructure should be leveraged by partnering with state and local governments and tapping private sector investment. Infrastructure permitting approval process should be streamlined down to one or two years. He commented that the US is seeing rising wages on the strength of the economy. On Trade, he said 'we will protect American workers and American intellectual property'. On North Korea, he said that it could very soon threaten the US and he would not make the same mistakes of previous administrations. Overall the speech struck a positive tone. USDJPY moved higher from 108.741 to 109.084.

Tonight will be the last FOMC meeting for the current Fed Chair Janet Yellen. No change is expected with the rate to be left at 1.5%. The release won't be accompanied by a press conference or a forecast update which may result in a non-event. The last hike was in December and the current consensus is for three hikes this year. The next meeting in March will see Jerome Powell take over as chair. Therefore, the statement could be very similar to last months to avoid limiting his first meeting.

UK Consumer Credit (Dec) was £1.52B against an expected £1.30B, from £1.40B previously, revised up to £1.5B. Mortgage Approvals (Dec) was 61.039K v an expected 63.500K, from 65.139K prior, which was revised down to 64.712K. GBPUSD rallied from 1.40221 to a high of 1.41042 following the data being released.

Eurozone Gross Domestic Product s.a. (QoQ) (Q4) was as expected, remaining unchanged at 0.6%. Gross Domestic Product s.a. (YoY) (Q4) was 2.6% v an expected 2.7%, from 2.6% previously. Services Sentiment (Jan) was 16.7 v an expected 18.6, from 18.4 previously, which was revised down to 18.0. Consumer Confidence (Jan) was as expected, remaining unchanged at 1.3. Industrial Confidence (Jan) was 8.8 v an expected 9.0, from 9.1 previously, which was revised down to 8.8. Economic Sentiment Indicator (Jan) was 114.7 against an expected 116.3, from 116.0 previously, which was revised down to 115.3. Business Climate (Jan) was 1.54 v an expected 1.69, from 1.66 prior, revised down to 1.60. EURUSD rose from 1.23943 to 1.24406 after this release.

German Harmonised Index of Consumer Prices (YoY) (Jan) was as expected, unchanged at 1.6%.

US S&P/Case-Shiller Home Price Indices (YoY) (Nov) was as expected at 6.4%, from a prior reading of 6.4%, which was revised down to 6.3%. EURUSD sold off from 1.24260 to a low of 1.24033 before recovering and hitting a high of 1.24536.

Bank of England Governor Mark Carney testified before the House of Lords Economic Affairs Committee in London. He said that he expects investment in the UK to pick up in 2019, with clarity on Brexit supporting investment. He added that he expects inflation to remain above 2% in the near future due to the effects of the Pound.

EURUSD is up 0.35% overnight, trading around 1.24456.

USDJPY is down -0.09% in early session trading at around 108.675.

GBPUSD is down 0.38% to trade around 1.41973.

USDCAD is down -0.27%, trading around 1.23005.

Gold is up 0.40% in early morning trading at around $1,343.80.

WTI is unchanged this morning, trading around $63.98.

Major data releases for today:

At 07:45 GMT, French Consumer Price Index (EU norm) (YoY) (Jan) will be released with an expected 1.1% from 1.2% previously.

At 09:00 GMT, German Unemployment Change (Jan) is expected to be -17K from -29K previously. Unemployment Rate s.a. (Jan) is expected to be unchanged at 5.5%. EUR crosses could be affected by this data.

At 10:00 GMT, Eurozone Unemployment Rate (Dec) is expected to be unchanged at 8.7%. Consumer Price Index – Core (YoY) (Jan) is also expected to be unchanged at 1.0%. Consumer Price Index (YoY) (Jan) is expected to be 1.3% from 1.4% previously. EUR pairs may be moved by this release.

At 13:15 GMT, US ADP Employment Change (Jan) is expected to be 185K from 250K previously. Employment Cost Index (Q4) is expected to come in at 0.6% from 0.7% previously. USD crosses could see an increase in volatility from this data release.

At 14:45 GMT, US Chicago Purchasing Managers' Index (Jan) is expected to be 64.1 against a prior read of 67.8, which was revised up from 67.6.

At 15:00 GMT, Pending Home Sales (YoY) (Dec) is expected to be -0.2% against a prior reading of 0.6%. Pending Home Sales (MoM) (Dec) is expected to be 0.4% against a prior reading of 0.2%.

At 19:00 GMT, US Fed's Monetary Policy Statement and Interest Rate Decision, which is expected to be left unchanged at 1.5%. USD crosses may experience volatility during this time.

Euro Area Q4 17 GDP Growth Came Out Strong

Market movers today

In the euro area all eyes will be on the January HICP figures today. We expect headline inflation to fall temporarily to 1.1% in January due to energy price base effects but bounce back to the 1.4% level shortly after. However, we do not believe headline inflation will pick up significantly from 1.4% before 2019 despite higher expected energy price inflation. Wage growth remains subdued, so underlying inflation pressure is not strong enough to lift headline inflation towards t he ECB's 2% target just yet . For core inflation we expect a slight acceleration in January to 1.0%, mainly due to goods price inflation, while service price inflation will likely stay muted. Note that the French and Spanish HICP figures are also released earlier in the morning.

In the US, today's key event is t he Fed meeting. We expect no policy changes and also no major changes to the statement , as markets are already beginning to price in the three hikes t he Fed is signalling. It will be Janet Yellen's last meeting; for our view on t he Jerome Powell Fed wee also Flash Comment US: Fed Chair Powell is 'Yellen in disguise’ amid discussions about price level targeting, 24 January.

In Scandinavia, we get Danish unemployment figures for December.

Selected market news

The EUR fixed income market recovered slightly yesterday after the 'ECB sources story' on Monday stating that ECB's QE will end with a short taper rather than a sudden stop. According to the story, even the more hawkish GC members endorse a gradual slowdown of QE after September. In addition, yesterday, ECB GC member Klas Knot (hawkish) said that QE may end with a short taper after having said over the weekend that t he QE program has to end 'as soon as possible'.

On the euro area data front, euro area Q4 17 GDP growth came out strong yesterday at 0.6% q/q (2.7% y/y). This was slightly lower than the previous quarter (0.7% q/q), but still a solid expansion pace. This leaves annual 2017 euro area GDP growth at 2.5%, the highest since 2007 and activity indicators such as PMIs and ESI still point to a continued strong expansion pace for the next quarter. German HICP inflation came out slight ly lower than expected yesterday at 1.4% y/y in January. The lower than expected German figure supports our below consensus call for euro area headline inflation of 1.1% in January (due today).

It was a relatively mu ted market re action on Trump's first State of the Union speech in Washington overnight with the EUR/USD increasing slightly and the 10-year US government benchmark bond yield dropping around 1bp.

Yesterday, the Irish Minister of Finance officially nominated the Irish Central Bank Governor Philip Lane to replace Vi tor Constancio as VP of the ECB. Const ancio's term expires in May this year. Countries can nominate a candidate from each country until 7 February.

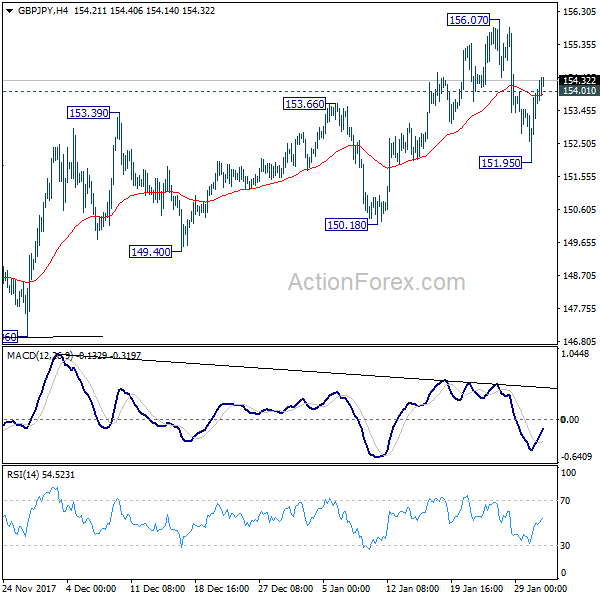

GBP/JPY Daily Outlook

Daily Pivots: (S1) 152.55; (P) 153.31; (R1) 154.66; More...

GBP/JPY recovered strongly after hitting 151.95 and intraday bias is turned neutral first. But still, as 156.07 is seen as a short term top, another fall is expected ahead. Break of 151.95 will target 150.18 support first. Break will extend the decline to 149.96 key support level. Meanwhile, above 156.07 will resume larger up trend to 167.78 fibonacci level.

In the bigger picture, as long as 146.96 key support holds, medium term outlook remains bullish. Rise from 122.36 is in favor to extend to 61.8% retracement of 195.86 to 122.36 at 167.78. However, break of 146.96 support will indicate trend reversal. And there would be prospect of retesting 122.36 in that case.

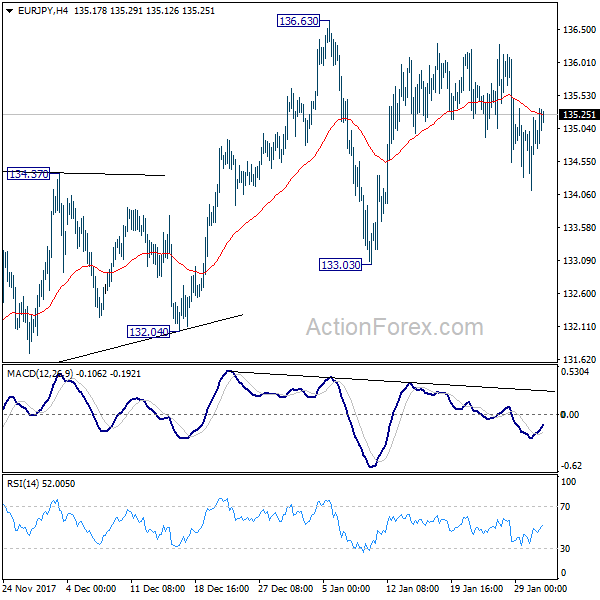

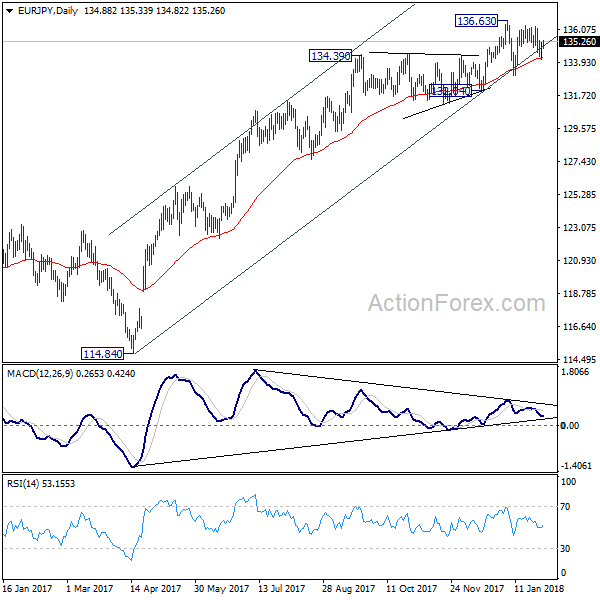

EUR/JPY Daily Outlook

Daily Pivots: (S1) 134.28; (P) 134.74; (R1) 135.36; More....

Intraday bias in EUR/JPY remains neutral but outlook stays bullish with 133.03 support intact. Break of 136.63 will resume medium term up trend. However, on the downside, break of 133.03 will have 55 day EMA and medium term channel support firmly taken out. Also, considering bearish divergence condition in daily MACD too, that will suggest medium term reversal. Deeper fall should then be seen to 132.04 support for confirmation.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). It should be targeting 141.04/149.76 resistance zone. On the downside, break of 132.04 support is needed to indicate medium term reversal. Otherwise, outlook will stay bullish in case of deep pull back.