Sample Category Title

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3479; (P) 1.3517; (R1) 1.3576; More.....

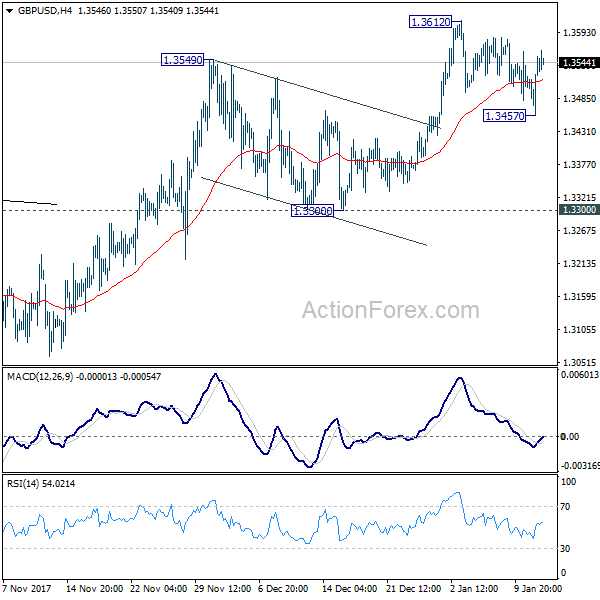

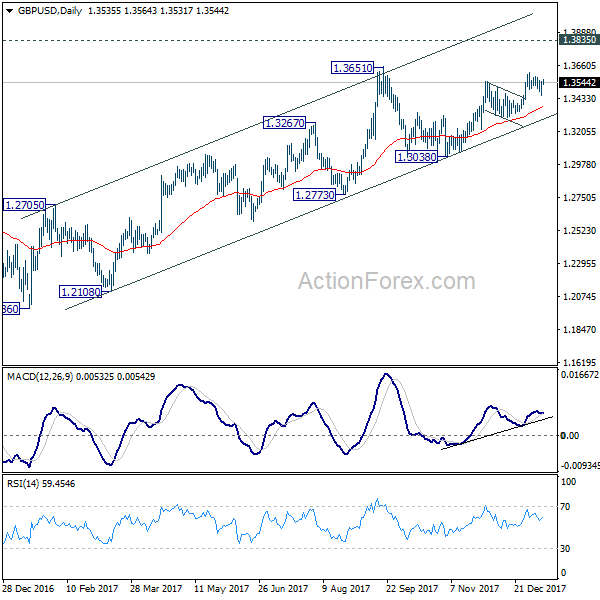

GBP/USD dipped to 1.3457 but recovered quickly again. The price actions from 1.3612 are now clearly corrective. Hence even in case of another fall, downside should be contained well above 1.3300 support to bring rise resumption. And, break of 1.3612/51 resistance zone will now target 1.3835 key resistance level next.

In the bigger picture, the break of long term trend line resistance from 1.7190 (2014 high) is seen as a sign of long term reversal. However, rise from 1.1946 (2016 low) is not impulsive looking. And the pair is limited below 1.3835 key resistance. Hence, we won't turn bullish yet and would continue to monitor the development. On the downside, break of 1.3038 support will now indicate that rebound from 1.1946 has completed and turn outlook bearish. Meanwhile, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

Euro Surged on Hawkish ECB Minutes, Dollar to Look into CPI

Risk appetite continued to be generally strong. DOW closed up 205.6 pts, or 0.81% overnight to 25574.73. S&P 500 and NASDAQ were up 0.7% and 0.8% respectively. All hit new record highs. Positive sentiments continue in Asian session with gains in China and HK markets even though Nikkei weakens mildly on recent Yen strength. WTI crude oil also extended recent rally to as high as 64.77 and is set to test 65 handle. Gold is firm, consolidation around 1320, as Dollar is back under pressure. The greenback will look into today's CPI reading for direction.

Euro surged on ECB minutes

Euro jumped sharply yesterday the December ECB minutes signaled that policymakers might begin changing the forward guidance in coming months in response to a better macroeconomic backdrop. As the minutes noted, "the view was widely shared among members that the Governing Council's communication would need to evolve gradually... if the economy continued to expand and inflation converged further towards the Governing Council"s aim. The language pertaining to various dimensions of the monetary policy stance and forward guidance could be revisited early in the coming year". Moreover, the minutes suggested that the members noticed "a gap appeared to be emerging between favorable economic conditions and a policy stance that remained in a crisis configuration". More in Hawkish ECB Signals To Revisit Forward Guidance As Recovery Pace Accelerates.

The news sent EUR/USD above 1.2 handle while EUR/GBP is also back pressing 0.89. But EUR/JPY remains in near term decline despite a relatively weak recovery. EUR/CHF is also still limited below 1.1777 resistance. Underlying strength in Euro remains to be confirmed.

Fed Dudley warned tax cuts will come at a cost

A key Fed official, New York Fed President William Dudley warned that the Republican's tax cuts "will come at a cost. After all, there is no such thing as a free lunch". He said that "the economy has considerable forward momentum, monetary policy is still accommodative, financial conditions are easy, and fiscal policy is set to provide a boost. But, there are some significant storm clouds over the longer term". He added further that "keeping the economy on a sustainable path may become more challenging" for the Fed due to the risk of "overheating."

Earlier in the week, Dallas Fed President Robert Kaplan also said that the short-term boost from the tax cuts to the economy will eventually "tail off". The government would be saddled with more debt in the future and "it would create a future headwind for economic growth".

On the data front

China trade surplus widened sharply to USD 54.7b, or in Yuan term CNY 362b. US CPI and retail seals will bee the main focus for today.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1953; (P) 1.2006 (R1) 1.2084; More....

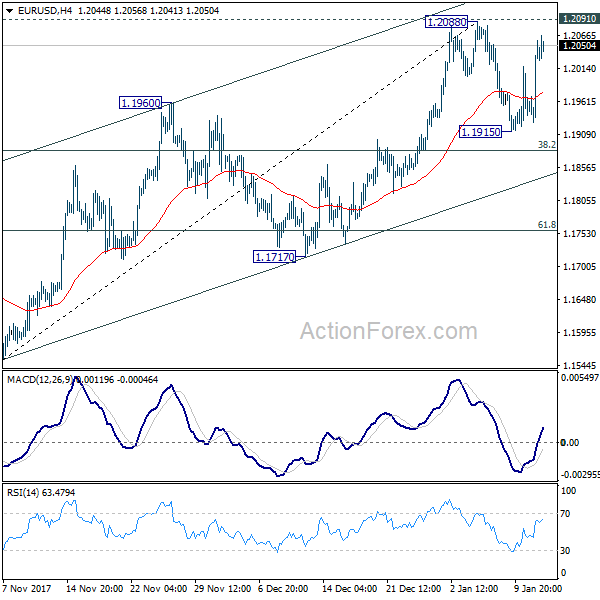

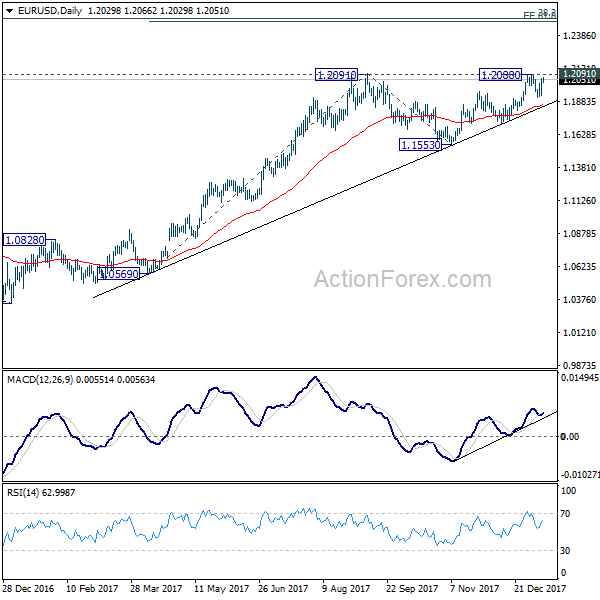

EUR/USD's rebound from 1.1915 extends higher but it's still limited below 1.2091 key resistance. Intraday bias remains neutral at this point. Again, decisive break of 1.2091 key resistance is needed to confirm up trend resumption. Otherwise, more corrective trading should be seen with risk of another fall. Below 1.1915 will turn bias to the downside for 38.2% retracement of 1.1553 to 1.2088 at 1.1884. Break will target 61.8% retracement at 1.1757 and below. Nonetheless, firm break of 1.2091 will resume whole medium term rise from 1.0339 towards 1.2516 long term fibonacci level.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1953; (P) 1.2006 (R1) 1.2084; More....

EUR/USD's rebound from 1.1915 extends higher but it's still limited below 1.2091 key resistance. Intraday bias remains neutral at this point. Again, decisive break of 1.2091 key resistance is needed to confirm up trend resumption. Otherwise, more corrective trading should be seen with risk of another fall. Below 1.1915 will turn bias to the downside for 38.2% retracement of 1.1553 to 1.2088 at 1.1884. Break will target 61.8% retracement at 1.1757 and below. Nonetheless, firm break of 1.2091 will resume whole medium term rise from 1.0339 towards 1.2516 long term fibonacci level.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494.

Hawkish ECB Signals To Revisit Forward Guidance As Recovery Pace Accelerates

The December minutes turned out more hawkish than expected. While the policymakers generally judged that the existing monetary policy remained 'appropriate'. They also agreed that the forward guidance might warrant some adjustments as the pace economic recovery accelerated. The minutes noted that the 'transition would take place without a change in sequencing', suggesting that no rate hike would be implemented before the end of the asset purchase program. The minutes indicate that the forward guidance would be a key policy tool in the year ahead.

Upbeat Economic Outlook

On the economic developments, Executive Board member Praet described the pace of expansion as 'robust'. He acknowledged that drivers of growth were becoming 'increasingly self-supporting' while the expansion had become 'increasingly broad-based across countries'. Indeed, the optimism has been revealed in the staff economic projections released last month. Recall that the staff upgraded the GDP growth estimates to +2.3% in 2018 and +1.9% in 2019, up from previous projections of +1.8% and +1.7%, respectively. The staff also projected growth to be +1.7% in 2020.

On inflation, Praet noted that 'measures of underlying inflation had weakened overall and had yet to show convincing signs of a sustained upward trend'. He added that 'steady absorption of economic slack gave grounds for increased confidence that price pressures would gradually take hold'. The Governing Council largely agreed with Praet's assessment and it was remarked that some of the downside surprises to core inflation appeared to 'be of a temporary nature, reflecting one-off factors'. The staff in December also revised headline inflation higher, by +0.2 percentage point, to +1.4% in 2018. However, core inflation is revised -0.2 percentage point lower to +1.1% next year. Inflation forecast stayed unchanged for 2019, with both headline and core HICP readings at +1.5%. For 2020, headline and core inflation are projected to be +1.7% and +1.8% respectively

Revisiting Forward Guidance

Against the backdrop of a stronger recovery, the members 'widely shared' the view that 'the Governing Council's communication would need to evolve gradually, without a change in sequencing, if the economy continued to expand and inflation converged further towards the Governing Council's aim'. The minutes added that 'the language pertaining to various dimensions of the monetary policy stance and forward guidance could be revisited early in the coming year'.

While there were remarks that 'a gap appeared to be emerging between favorable economic conditions and a policy stance that remained in a crisis configuration', it is believed that the favorable recovery situation is still dependent on 'an ample degree of monetary accommodation'.

ECB's key policy tool for the year ahead would be the gradual transition in the forward guidance from 'the present conditionality focused on APP net purchases' to 'a broader concept of forward guidance comprising various dimensions of the monetary policy stance'. The tweak would be data-dependent and hence link the future policy rate path to the inflation outlook.

Doves’ Blood In The Eurozone Water

When the ECB drops a hint of tightening it's like a drop of blood in a shark tank, as the market showed on Thursday. NZD and EUR were the top performers while the US dollar lagged. Japanese current account data will close out the week. A 3rd EUR trade has been issued to the Premium Insights.

The ECB minutes offered a small hint about what's coming next, referring to the area's 'expansion' rather than its continued 'recovery' but that was all it took to send the euro to 1.2050 from 1.1940. In recent press conferences, Draghi has taken pains to keep the currency from jumping but the minutes offered more colour about the 'continued robust and increasingly self-sustaining economic expansion' as policymakers contemplate what to do next.

The market is extremely one-sided with net euro longs at the most extreme on record but even this week's three-day, 170-pip decline wasn't enough to shake out any longs.

The stability got a hand from the continued struggles of the US dollar. An extremely strong 30-year bond auction Thursday weighed on the dollar along with a miss on PPI. Friday features the CPI and retail sales reports. Both will be critical for the US dollar and the Fed deciding what to do next.

First, Japanese current account numbers will be released at 2305 GMT. Don't expect a significant market reaction. Instead, watch out for continued reports about bond buying, trade and Bitcoin exchanges.

Market Morning Briefing: WTI Is Trading Above Support At 63

STOCKS

Global stocks are all stable without any sharp movement just now.

Dow (25574.73, +0.81%) has come off from immediate resistance on the daily candles but the upside may not be over yet. A test of 25200-25000 is possible before again moving up towards 25400-25600 levels in the medium term. Overall Dow is in an uptrend and is likely to continue.

Dax (13202.90, -0.59%) was almost stable yesterday. While the resistance near 13400 holds strong, the index is likely to come off towards 13000 in the near term.

Nikkei (23697.46, -0.05%) came off slightly to test 23600. Near term looks bearish with enough room on the downside towards 23200 and lower.

Shanghai (3429.21, +0.11%) is almost stable just now. Upside possibility of testing 3440 remains open for the near term.

Nifty (10651.20, +0.18%) is testing immediate support near 10600 and while that holds, it is likely to see another upmove towards 10700-10750 in the near term. Sensex (34503.49, +0.20%) has support at 34250 and while that holds, the index looks positive towards 34750.

COMMODITIES

Brent (69.30) tested 70.05 yesterday before coming off to close at slightly lower levels. While resistance at 70 holds, the price could trade sideways for some sessions and come off towards 68 before trying to attempt another rise. A break above 70, if seen and sustains could indicate further sharp upmove towards 71.00-71.50 (less preferred just now)

WTI (63.65) is trading above support at 63 and while that holds, the price could move up towards 65 in the coming sessions.

Gold (1326) has risen above the 1320-1310 region possibly initiating a fresh upmove towards 1340 or higher in the near term. Ner term looks bullish.

Silver (17.08) is holding below resistance near 17.30 and is likely to consolidate within 17.30-16.70 region for sometime. Note that 17.30 is an important long term resistance.

Copper (3.2375) is trapped above 3.20 and is trading in narrow movements within 3.20-3.30 region. An initial attempt to 3.30 is possible but on a medium term, we may expect a fall towards 3.20-3.15 levels.

FOREX

Keep an eye on the Euro-Yen (133.30). It saw a low just below 133 yesterday. Although it can bounce a bit towards 133.70-90 in the near term, there are increasing chances that it might eventually break below the crucial Support at 133. It would then target 130 in the medium term.

Such a dip in the Euro-Yen would be triggered/ accompanied by a fall in Dollar-Yen (111.44) over the coming days. These two together could try and pull the Euro (1.1960) below 1.19.

To prevent that from happening, the Euro needs to convincingly rise past 1.20 over today-tomorrow. While the potential is still there and it did, in fact, bounce from 1.19 to above 1.20 yesterday, it's failure to sustain that bounce is a little puzzling. We need to watch this carefully over today-tomorrow.

The Chinese Yuan (USDCNY = 6.5054) strengthened a goodish bit yesterday on news that Chinese officials are recommending a halt/ reduction in the purchase of US Bonds. Let us see whether the USDCNY breaks below 6.49 today or moves back up today. A bounce/ rise is a little more probable.

As expected, the Pound (1.3507) is relatively calm amidst the volatility in other currencies and is likely to remain so for some more days.

Contrary to our expectation of a dip to 0.7750, the Aussie (0.7875) did not even fall below 0.7800 and has, in fact, risen strongly today morning. This seems to be fresh strength that could pull the Aussie up towards 0.7950-8000 this time.

As expected, Dollar-Rupee (63.60) found Resistance just above 63.80 and can dip to 63.50-45 today. Direction after that is unclear.

INTEREST RATES

Global bond markets could well be entering a bearish phase with higher crude prices raising inflation and consequently, investors’ expectations for higher yields.

The US 10Yr (2.5495%) reached highs near 2.588% with news of China’s reluctance to buy US bonds coming in. We could now expect the 10 Yr yields to consolidate near 2.55% for sometime before targeting 2.62% on the upside, seen as resistance on short term charts. US 30 Yr (2.8928%) could move up to resistance near 2.94% on the short term chart and stay below that level for few days before attempting another rise. Expectations of higher inflation being reflected in the CPI data release (due tomorrow) seems to have been already factored into the rise in yields recently. However, we still need to see if some surprises could push the yields further up.

Japanese 10 Yr Yield (0.075%) dipped from yesterday’s levels around 0.088%, where we see resistance on the short term charts. This resistance could hold for the time being.

The German 10 Yr Bund Yield (0.543%) is testing resistance on the medium term chart and could dip from here. The German-US 10 Yr Yield Spread (-2.0095%) has gone up appreciably from yesterday and might attempt a test of resistance near -1.9% on the long term chart in the coming sessions.

GBPUSD – Looks To Weaken Further

GBPUSD - The pair faces further downside pressure as it retains its corrective pullback threats. Support lies at the 1.3450 level where a break will turn attention to the 1.3400 level. Further down, support lies at the 1.3350 level. Below here will set the stage for more weakness towards the 1.3300 level. Conversely, resistance stands at the 1.3500 levels with a turn above here allowing more strength to build up towards the 1.3550 level. Further out, resistance resides at the 1.3600 level followed by the 1.3650 level. On the whole, GBPUSD looks to weaken further on correction

A Week Of Headline Hullabaloo: TGIF

Headline nonsense

The advent of headline reading robots is changing the marketplace and likely causing capital market traders to react first and check later( fact-finding ) for fear of missing out. So with the volumes of spurious headlines over the last 24-48 hours, the challenges now facing traders in the age of information overload is assessing the wheat from the chaff when it comes to ” fake news.” But unfortunately, these factious headlines are becoming all to commonplace in 2018.

Oil

Brent climbed to the critical $70 per barrel for the first time since 2014 and Oil is having its usual far-reaching influence on cross-asset markets as Wall Street soars to new record territory

The market was caught a bit short when Suhail al-Mazrouei, UAE energy minister and current OPEC president, said Thursday that OPEC remains “committed to maintaining strong compliance.” which spurred a wave of short covering rather than topside buying.

By all appearances at the future open, the market is showing signs of finally succumbing to that anticipated correction.

Gold

Gold put in another strong showing after the Hawkish ECB minutes weighed on USD sentiment. But there appears to be a broader move afoot as the USDJPY zeroed in on the critical 111 level amidst BoJ tapering speculation.

Indeed, the weaker dollar narrative amidst increased demand for equity market hedges suggests the near-term outlook for Gold is glittering.

G-10

The Euro

The Euro exploded higher after a hawkish glean from the ECB minutes caught trader flat-footed as most had shallow expectations from the release. But as usual when it comes to Mario and gang its best to expect the unexpected especially when fissures within the ECB board are starting to appear.

As usual, traders couldn’t help but trip over themselves getting topside exposure at the thought of catching a significant policy shift. The Euro Bulls are now banking on a possible change in ECB language as early as March.

Of course, this feels like ” Deja Vu all over again ” as traders consider the merits of parlaying the minutes versus another dovish surprise from Draghi. But with the bullish fundamental narrative solidly intact, it’s hard to argue against warehousing some form of Euro proxy trade on the back of the ECB’s apparent hawkish shift.

The Canadian Dollar

Speaking of fake news, after the imminent demise of NAFTA was denied the Loonie had retraced about 60 % of yesterday’s panicked move, but the fact it has not fully recovered is probably due to overextending shorts ahead of Bank of Canada announcement. In the where there’s smoke their fire category and as far as the broader North American trade picture is concerned. In a WSJ interview this morning, President Trump reiterated he would terminate NAFTA unless he gets a fair and “Trump deal” but added to “leaving it a bit flexible” until after the Mexico election. Predictably USDCAD gapped higher some 35 pips in low liquidity before coming back.

The Japanese Yen

Given the general dollar malaise, USDJPY is struggling against the backdrop of BoJ taper overhang and another strong US 10 year Treasury auction. The bid to cover ratio came in at 2.74, which is the highest level seen since December 2014. The markets were convincingly dollar offered overnight, but so far in early trade, APAC traders are showing a higher propensity of cover shorts heading into the weekend probably looking to put this silly week of headline hullabaloo in the rearview mirror.

The Australian Dollar

The Aussie dollar benefited from of all things iPhone sales after the release of data showing better-than-expected retail spending in November.

The currency continued to gather steam overnight influenced by external drivers as the weaker US dollar and surging commodity prices led the charge.

Asia FX

Thankfully local EM Fx traders remain calm while doubting the validity of the China treasuries story and were rewarded for their patience when China’s FX authority SAFE was quick castigate those reports as ‘false news and predictably USDAsia sold off in tandem with US Bond Yields.

The Yuan

Regional currency markets are finding themselves in a much happier spot this morning with USDCNH trading sub 6.50 unwinding both the Treasury headline nonsense and Counter-Cyclical squeeze.

The Ringgit

The Ringgit made the highlight reel once again after a substantial industrial production number yesterday which cemented the markets BNM rate hike view. While we’re likely to enter a healthy correction on oil prices, WTI is at such a lofty levels, and any sell-off is unlikely to have any sustainable adverse effect on the MYR.

Fed Speak

A late NY speech delivered my Dudley is attracting some attention where he sounds very optimistic regarding the US economy reaching its inflation targets but doesn’t expect “transitory” factors to fade out until after Spring 2018. USDJPY came off the 111.05 low, but there was little significant broader based USD impact

Cryptocurrencies

The barrier for Bitcoin to be considered a viable asset class continue to mount. The threat from increased regulatory oversight in the wake of South Korea imposing a ban on Crypto trading could spread and severely dent sentiment. But also the excessive volatility makes trading Crypto coins a fool’s errand with only two discernable strategies investors are apparently using. 1) Buy on dips, sit on your hands and hope it rises or 2) Sell at the current tops and pray it fall. Probably not a quantified methodology for managing risk and suggests the product in its infancy will not be sold as a viable investment grade product by Major investment houses.

Dollar Drops Ahead Of Inflation And Retail Sales

Hawkish ECB minutes and China's US bond purchases driving greenback lower

The US dollar is weaker across the board a day before the release of the US consumer price index (CPI) and retail sales data for December. The Bureau of Labor Statistics will publish the monthly report on Friday, January 12 at 8:30 am EST. Economists expect inflation to remain subdued with CPI coming in at 0.1 percent and core CPI at 0.2 percent. Retail sales are also forecasted to slow down with sales at 0.5 percent and the core reading at 0.4 percent. A surprise to the upside would boost the USD, but a confirmation of lower inflation combined with a hawkish European Central Bank (ECB) as per the minutes released earlier could further put pressure on the currency.

- ECB December meeting minutes signal earlier end to QE

- CAD rebounds from end of NAFTA rumours

- US inflation and retail sales to guide dollar on Friday

The EUR/USD gained 0.72 percent on Thursday. The single currency is trading at 1.2033 after the European Central Bank (ECB) released the notes from its December monetary policy meeting. The central bank is preparing the market for the end of its massive quantitative easing program as it talks up the strength of the Eurozone economy. The language change reflects a focus going forward on continued expansion. Inflation has not risen near the desired target, which is why the ECB is not considering raising rates until 2019, but reducing the 30 billion euros a month in bond purchasing would be a step in the rate normalization goal.

The USD was under pressure yesterday when the financial press reported that China was considering diversifying away from its US treasury holdings. China denounced the rumours, but as global trade comes to the forefront and the Trump Administration has decided to play an America First strategy there has been a shift in what is considered a safe haven. The euro has advanced 0.24 percent this year and remained above the 1.20 price level.

The USD/CAD lost 0.16 percent since market open on Thursday. The currency pair is trading at 1.2528 with the CAD recovering from yesterday's reports that the US was ready to withdraw from NAFTA. Canadian officials have increased the odds that the Trump Administration would pull out of the renegotiation table and invoke a six month period before terminating their participation in the two decade agreement. The White House has denied the rumours but gave no assurances about the fate of NAFTA saying the President's mind changed.

Mexican and Canadian officials are now seeking new ways to approach the demands of the United States in particular regarding the auto sector. The US wants to increase the content of vehicles to 85 percent American from the current 62 percent.

The loonie remains higher against the greenback year to date at 0.42 percent with the upcoming monetary policy decision by the Bank of Canada (BoC) on January 17 expectation of a lift to the interest rate after a strong jobs report in December. The fate of NAFTA has been singled out as a concern by Governor Poloz, but it remains to be seen what was the desired impact of the two anonymous Canadian officials who spoke on the record to the press. If the intent was to sound out the White House and get a reaction, it was muted as very little seems to have changed. But if the plan was to measure market reaction to a possible end of NAFTA then the BoC could end up delaying its rate hike until NAFTA negotiation talks reach a conclusion however diluted it might be.

Market events to watch this week:

Friday, January 12

8:30am USD CPI m/m

8:30am USD Core CPI m/m

8:30am USD Core Retail Sales m/m

8:30am USD Retail Sales m/m

Gold Moves Higher On Weak US Inflation Numbers

Gold prices continue to point upwards, and the trend has continued in the Thursday session. In North American trade, the spot price for an ounce of gold is $1322.22, up 0.41% on the day. On the release front, PPI and Core PPI both missed their estimates, with declines of 0.01%. On the employment front, unemployment claims jumped to 261 thousand, above the forecast of 246 thousand. On Friday, traders should be prepared for some movement from gold, as the US releases CPI and retail sales reports for December.

Gold has restored some luster in recent weeks, as the base metal has climbed 3.7% percent since December 1. The rally has been all the more impressive, as risk appetite has been high, with the US economy looking strong and the Fed raising interest rates in December. Gold prices often fall when investors are more comfortable with riskier assets, but a weaker US dollar has helped gold post higher – on Wednesday, gold touched a high of $1327, its highest level since mid-September.

The US dollar was broadly lower on Wednesday, and gold took advantage with considerable gains. The catalyst for this move was a report on Wednesday that China was considering slowing or halting the purchase of US government bonds. China boasts the largest currency reserves, estimated at $3 trillion. It is also the biggest holder of US government bonds, in the amount of $1.19 trillion. Why would China make this move? One reason is that it may consider US treasuries less attractive compared to other assets. As well, it could be part of China’s strategy to flex some muscle as a possible trade war looms between the US and China, which are the two largest economies in the world. The report has pushed US Treasury yields higher and sent the US dollar downwards.