Sample Category Title

DAX Edges Higher As German Industrial Production Jumps

The DAX has posted slight gains in the Tuesday session. Currently, the index is at 13,380.00, up 0.10% on the day. On the release front, German Industrial Production rebounded with a sharp gain of 3.4%, above the estimate of 1.9%. Germany’s trade surplus widened to EUR 22.3 billion, beating the forecast of EUR 20.7 billion. The eurozone unemployment rate ticked down to 8.7%, matching the forecast.

World stock markets have been pointing upwards early in the New Year, and the DAX has also looked sharp, climbing 3.8% in January. Led by a robust German economy, the eurozone is on track for a strong fourth quarter, as the economy continues to expand and unemployment falls. Inflation has also moved higher, although the ECB is unlikely to reconsider its current stimulus program, which ends in September. One area of concern is the political vacuum in Germany. President Angela Merkel is running a caretaker government, as she has been unable to form a coalition, following the September elections. Merkel is now looking at the Social Democrats to help her make a new government, and preliminary talks are scheduled to begin on Sunday. The negotiations are moving slowly, and are likely to continue for several more months.

German indicators looked sharp on Tuesday. Industrial Production jumped 3.2%, after two consecutive declines. This marked only the second gain since July. Germany’s trade surplus climbed to EUR 22.3 billion in December, its highest surplus since May 2016. December indicators have pointed upward, including manufacturing and services PMIs, retail sales, and employment data. However, the political landscape in the eurozone’s largest economy remains cloudy. President Angela Merkel is now looking at the Social Democrats to help her make a new government, and preliminary talks are underway. The negotiations are likely to be lengthy, and the current caretaker government could remain in office for several more months.

Euro Dips Despite Sharp German Numbers

The euro has edged lower in the Tuesday session, following two straight losing sessions. Currently, EUR/USD is trading at 1.1929, down 0.35% on the day. On the release front, German Industrial Production rebounded with a sharp gain of 3.4%, above the estimate of 1.9%. Germany’s trade surplus widened to EUR 22.3 billion, beating the forecast of EUR 20.7 billion. The eurozone unemployment rate ticked down to 8.7%, matching the forecast. In the US, today’s key event is JOLTS Job Openings, which is expected to climb to 6.05 million.

More German indicators more positive news. Industrial Production jumped 3.2%, after two consecutive declines. This marked only the second gain since July. Germany’s trade surplus climbed to EUR 22.3 billion in December, its highest surplus since May 2016. December indicators have pointed upward, including manufacturing and services PMIs, retail sales, and employment data. However, the political landscape in the eurozone’s largest economy remains cloudy. President Angela Merkel is now looking at the Social Democrats to help her make a new government, and preliminary talks are underway. The negotiations are likely to be lengthy, and the current caretaker government could remain in office for several more months.

When the Federal Reserve makes the financial headlines, the discussion is usually focused on interest rates. The Fed took advantage of a strong US economy in 2017, raising interest three times. Another quarter-point hike is widely expected later in January. As of this month, the Fed has started to shrink its massive balance sheet of $4.4 trillion. The balance sheet ballooned during the financial crisis of 2008-2009, and good times have allowed the Fed to begin trimming its portfolio. Incoming Fed Chair Jerome Powell, who takes over in February, has estimated that the balance sheet could drop to anywhere between $2.4 trillion to $2.9 trillion after several years of cuts. Fed policymakers have not indicated a magic number for the balance sheet, but the cuts indicate a vote of confidence in the US economy.

German Industrial Data Boost Sentiment | Bitcoin Above 15K | Samsung Misses Its Profit Forecast

Yen Strengthens on BOJ's QE tightening

400 days without a 5% correction for US indices

Samsung chip business undeforms

European markets are trading higher as investors have reacted to positive German industrial data. The number was simply astonishing, and it printed the reading of 3.4% when the market was expecting a number of 1.8%.

However, the Euro-Dollar paid is still facing it's inevitable correction and this is purely because traders are quick on their feet to take some profit off the table (as the pair touched its high of 1.2083). The strong rebound in the dollar may keep the pressure on the euro for a while but we are not expecting any major selloff. The strength of the Eurozone's economy is robust and it's economic indicators are still pointing that the economy would continue to accelerate at a respectable pace in 2018.

The recent CFTC data also confirms that the recent retracement is only a healthy correction as institutional money still holds a record amount of net long positions. The German industrial data released today puts the approval stamp for traders to hold the bullish view for the euro.

The Eurozone's unemployment number could lift the confidence for amid investors and for the ECB. A Lower unemployment rate doesn't necessarily mean inflation would improve, a measure which the ECB watches very closely, but it is a step in the right direction.

Looking at the performance of the US indices, one thing becomes apparent that the market has moved higher mostly on basis of positive sentiment. It is this very fact that we have not have seen the usual 5% healthy correction which the traders crave for. A correction of 5-10% mostly represents an opportunity for those who have been sitting on the sideline and have not had a chance to participate. In nearly 400 days, we have seen a 5% correction from its 52 week's high.

Similarly, the MSCI world index has also logged its longest winning streak in history without facing a 5% correction. Looking at these record numbers, it becomes evidently clear that the odds are stacked in favour of correction and the correction could extend even further from 5% but we do not expect a meltdown in the market because it's foundation appears to be on strong fundamentals.

The dollar-yen pair is one the most intriguing pair to watch today after the BOJ decided tow tweaked it's bond purchase program. The bank curbed its buying of 10-to -25 years year debt by 10 billion yen. The first cut in debt purchase since 2016 sends the signal to the markets that the super-loose monetary policy party is also coming to an end.

Bitcoin Above 15K

Bitcoin has broken the 15K level once again, an important junction (because if it stays above this, chances are going to continue to make record highs), due to the regulatory concerns. South Korea wants to tighten the regulatory screw again by looking at some specific accounts and China wants to limit the bitcoin mining operation. But these aspects have proven only a blip for Bitcoin and nothing more. Every time, we have heard any regulatory news impacting the cryptocurrency, it has proven to be only an opportunity for bargain hunters to jump onboard. Of course, one may say that Bitcoin is a bubble and it will burst, but the only reality about bubbles is that once they burst, they never come back again. For bitcoin, we have seen several massive price crashes over time, however, the price has bounced back up. Just like the S&P500 index, the big drop during the financial crisis presented the biggest opportunity in a decade.

Samsung Missed It's Earning

It wasn't the kind of quarter that investors were hoping for Samsung. A 1 trillion won or $937 million fourth-quarter profit miss is really a sad news if you are holding Samsung stock. This is primarily due to the downturn in firms chip prices. It was company's strong chip business performance which aided the firm to report robust quarterly earnings in Q2 and Q3. Of course, there is an element of strengthening currency effect which cannot be ignored. Samsung has a strong and prominent position when it comes to its next generation of screens known as organic light -emitting diodes and this area of their business did fuel a rise in sales. Going into Q1 of 201, we do expect their marketing strategies in Q4 of 2017 may bring a steep rise in the top line profit number. Having said that we do believe that their memory chip cycle has peaked as firms like Apple which buys OLED screen and memory chips are looking to make them under their own roof or looking at an alternative method.

Technical Outlook: USDCHF – Improving Environment Could Attract Further Advance

Strong bullish acceleration on Tuesday extended recovery leg from 0.9699 (02 Jan low) and penetrated daily cloud (cloud base lies at 0.9813).

Increasing risk appetite on brighter US rate outlook and improving environment on lift above daily Tenkan-sen (0.9801), support the advance.

Narrowing daily cloud which twists next week also attracts as 100/200SMA bull-cross (formed on 04 Jan) underpins the action.

Bulls face immediate barrier at 0.9832 (Fibo 61.8% of 0.9915/0.9699 bear-leg / falling 20SMA), break of which would open cloud top (0.9863) for test.

Initial support lies at 0.9800, followed by pivotal supports at 0.9780 zone, which are expected to hold and keep the downside protected.

Res: 0.9832, 0.9863, 0.9881, 0.9915

Sup: 0.9800, 0.9780, 0.9750, 0.9732

Market Update – European Session: Unemployment Continues To Fall For Various EU Members

Notes/Observations

Euro Zone data continues to show the regional recovery is robust and broad-based

Germany's Nov industrial Production handily beats expectations

Unemployment Rate continues to fall with Italy at a 5-year low and Euro Zone at a 9-year low

BoJ aiming for a relative steepening of the back end after cutting purchases of debt maturing in the 10-25-year and more than 25-year sectors; will the BOJ will follow the lead of the Fed and other central banks in embarking on the rate hikes???

Koreas hold first official talks in two years; although deemed not a game-changer, it should reduce miscalculation risks

Asia:

Japan Nov Real Cash Earnings registers its 1st rise in 11-months (+0.1% v -0.1%e )

BOJ reduces planned daily purchases of 10-25 year and over 25-year JGBs each by ¥10B

China PBoC: Skips OMO for 12th straight session noting that liquidity was moderate (prior banking liquidity at relatively high level

China PBoC Gov Zhou: 2018 GDP growth seen at 6.4%, slowing due to deleveraging

South Korea and US to start annual military drills April 1st (delayed due to Olympics); Trump administration said to weigh a risky strategy as Seoul and Pyongyang prepare to meet. US officials debating if possible to mount limited military strike on North Korea.

South Korea Foreign Ministry: To consider temporary lifting of sanctions against North Korea if necessar

Europe:

Brexit Min Davis viewed EU's no-deal Brexit planning as 'damaging' to the process

Americas:

Fed's Bostic (2018 voter, dove): Fed may not need 3 or 4 rate hikes a year; policy is approaching a more neutral stance that could be close to 2%; Should continue to slowly remove accommodation. Fed should consider adoption of an inflation price level target; Price level targeting is really a very modest change

Fed's Williams (moderate, 2018 voter): central banks have less room to cut rates in the next crisis

President Trump: we are reviewing all trade agreements to ensure they are reciprocal; we're still working to get a better NAFTA deal. NAFTA ‘not the easiest negotiation' because Mexico and Canada are ‘making all of that money' on trade - Special counsel Muller likely to interview Trump as part of Russia probe; could happen within weeks

Economic Data:

(NL) Netherlands Dec CPI M/M: 0.0% v -0.2% prior; Y/Y: 1.3%e v 1.5% prior

(NL) Netherlands Dec CPI EU Harmonized M/M: -0.1%e v -0.4% prior; Y/Y: 1.2% v 1.5% prior

(CH) Swiss Dec Unemployment Rate: 3.3% v 3.2%e; Unemployment Rate (Seasonally adj): 3.1% v 3.0%e

(DE) Germany Nov Current Account: €25.4B v €25.3Be; Trade Balance: €23.7B v €21.3Be; Exports M/M: 4.1% v 1.2%e; Imports M/M: 2.3% v 0.4%e

(DE) Germany Nov Industrial Production M/M: 3.4% v 1.8%e; Y/Y: 5.6% v 3.9%e

(DK) Denmark Nov Current Account (DKK): 15.0Be; Trade Balance: 7.0Be

(FR) France Nov Trade Balance: -€5.7B v -€4.7Be

(FR) France Nov Current Account: -3.3B v -€2.6B prior

(CH)S wiss Dec Foreign Currency Reserves (CHF): 743.9B v 738.1B prior

(CZ) Czech Dec Unemployment Rate: 3.8% v 3.7%e

(CH) Swiss Nov Real Retail Sales Y/Y: -0.2% v -2.6% prior

(SE) Sweden Dec Budget Balance (SEK): -69.6B v +17.0B prior

(IT) Italy Nov Preliminary Unemployment Rate: 11.0% v 11.0%e (lowest since Sept 2012)

(EU) Euro Zone Nov Unemployment Rate: 8.7% v 8.7%e (lowest since JDec 2008 )

Fixed Income Issuance:

(ID) Indonesia sold total IDR13.0T vs. IDR9.0T indicated in 2018, 2020, 2022, 2025, 2031 and 2037 bonds

(NL) Netherlands Debt Agency (DSTA) sold €1.89B vs. €1.5-2.5B indicated range in 0% Jan 2024 DSL bond; Yield: 0.052% v 0.050% prior

(ZA) South Africa sold total ZAR3.3B vs. ZAR3.3B indicated range in 2032, 2040, 2044 and 2048 bonds

(CH) Switzerland sold CHF483.6M in 3-month Bills; Avg Yield: -0.872% v -1.05% prior

(AT) Austria Debt Agency (AFFA) sold total €1.38BB vs. €1.38B indicated range in 2027 and 2047 RAGB bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.3% at 399.7 , FTSE +0.3% at 7720 , DAX +0.2% at 13394, CAC-40 +0.5% at 5514 , IBEX-35 +0.5% at 10450, FTSE MIB 0.6% at 22992 , SMI +0.4% at 9579, S&P 500 Futures +0.1%]

Market Focal Points/Key Themes: European markets trade higher higher across the board with outperformance in Italy as well as France. The French CAC tops 5500, while the Eurostoxx 600 approaches 400. Altice rebound after announces approval of a planned separation of Altice USA and Europe, on the M&A front Nestle has received an increased off for its US confectionery business to $2.5B from Ferrero. Elsewhere the retail sector has got a boost in the UK following strong Christmas sales figures out of UK Supermarket chain Morrisions, with Sainsburys set to report results tomorrow. Looking ahead earnings in the US include Acuity Brands and Schnitzer Steel, as well as a continuation of preliminary earnings out of numerous names ahead of various conferences.

Movers

Consumer Discretionary [ Morrisons [MRW.UK] +2.7% (Trading update), Robert Walters [RWA.UK] -2.0% (Trading update)]

Consumer Staples [Carr's Group [CARR.UK] +13% (Trading update)

Materials [SIG plc [SHI.UK] -1.3% (Trading update), Topps Tiles [TPT.UK] +9% (Trading update)]

Materials [ Bauer [B5A.DE] -7% (Cuts outlook) ]

Industrials [Carillion [CLLN.UK] -7% (No news for price rise yester), Bauer [B5A.DE] -7% (Cuts outlook)]

Healthcare [Bioquell [BQE.UK] +10% (Trading update), Abylnx [ABLX.BE] +8% (Chairman to resign)]

Telecom [ Altice [ATC.NL] +5.2% (Reorganisation)]

Real Estate [Persimmon [PSN.UK] -2.1% (Prelim FY17 results)]

Speakers

Spain PM Rajoy stated that the country would be close to balance budget in 2020. Catalonia was the only shadow over the outlook. Believed that 2018 GDP could be over 2.3% with a stable govt in Catalonia

Ireland Debt Agency (NTMA): Strong domestic economy facing rising risks

Former Italy PM Berlusconi: Euro should continue to be handled in the same manner that ECB's Draghi has done

North Korea restored military communication line with South Korea after holding hold first talks since 2015

Iran Oil Min Zanganeh: OPEC did not want to see Brent oil prices above $60/barrel because of shale oil

Currencies

USD was still trying to consolidate against the major European pairs in the session and its slight strength in the session was attributed to re-positioning following year-end losses.

EUR/USD was off approx. 0.3% to test 1.1930 area despite better German Industrial production data for Nov and continued drop in unemployment levels for various Euro Zone members

GBP was softer in the aftermath of the UK Cabinet reshuffle. Dealers noted that such an event took hold as PM May's ability came to light she could not successfully navigate the Brexit talks with such rebellion within the ranks. Although no major members were reshuffled, the GBP was unable to find any footing. GBP/USD was hovering around the 1.3520 area just ahead of the NY morning.

USD/JPY was holding onto its Asian session losses after the BoJ trimmed the size of a bond-buying operation that sent JGB yields higher. The price action stabilized during the European session as market participants did not believe the move was any early indication of the BoJ adjusting its yield curve management policy. The recent improvement in Japanese data seemed to remain hopeful the BoJ would eventually start to unwind its ultraloose policy somewhere down the road. Key support in the pair seen at 112.00 area in which any break could open the door for a bigger test lower.

Fixed Income

Bund Futures trade down 13 ticks at 161.64 as JGBs set the tone, ahead of a heavy supply week. A continued move below 161.00 low targets 160.71 then 160.45, with a continued rebound targeting 162.36.

Gilt futures trade at 124.48 down 23 ticks at the session lows and approaching last week's low. Continued upside eyeing 125.25 then 125.82. Downside targets include 124.25 then 123.75.

Monday's liquidity report showed Friday's excess liquidity rose to €1.847T from €1.838T prior. Use of the marginal lending facility fell rose to €40M from €54M prior.

Corporate issuance remained strong with Barclays and Vonovia coming to the market.

Looking Ahead

(AR) Argentina Central Bank Interest Rate Decision: Expected to leave 7-Day Repo Reference Rate unchanged at 28.75%

(RU) Russia Dec Sovereign Wealth Funds: Reserve Fund: $B v $17.1B prior; Wellbeing Fund: $B v $66.9B prior

(ZA) South Africa Dec Nammsa Vehicle sales Y/Y: No est v 7.2% prior

05.30 (UK) Weekly John Lewis LFL sales data

05:30 (EU) ECB allotment in 7-day Main Financing Tender (MRO)

05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

05:30 (DE) Germany to sell €0.5B in 0.10% Apr 2046 Inflation Link Bond (Bundei)

05:30 (UK) DMO to sell £2.25B of 1.25% 2027 Gilts

05:30 (BE) Belgium Debt Agency (BDA) to sell €2.7B in 3-month and 12-month Bills

06:00 (US) Dec NFIB Small Business Optimism: 107.8e v 107.5 prior

06:00 (PT) Portugal Nov Trade Balance: No est v -€1.5B prior

06:00 (BR) Brazil Nov Retail Sales M/M: 0.2%e v 0.9% prior; Y/Y: 3.8%e v 2.5% prior

06:00 (BR) Brazil Nov Broad Retail Sales M/M: +0.3%e v -1.4% prior; Y/Y: 5.9%e v 7.5% prior

06:00 (PL) Poland PM Morawiecki said to announce new Cabinet

06:00 (TR) Turkey to sell 2019 bonds

06:30 (EU) ESM to sell €2.0B in 3-month bills; Avg Yield: % v -0.7320% prior; Bid-to-cover: x v 6.3x prior (Dec 5th 2017)

06:45 (US) Daily Libor Fixing

07:00 (RU) Russia announces weekly OFZ bond auction .

07:45 (US) Weekly Goldman Economist Chain Store Sales

08:05 (UK) Baltic Dry Bulk Index

08:15 (CA) Canada Dec Annualized Housing Starts: 211.0Ke v 252.2K prior

08:55 (US) Weekly Redbook Sales

09:00 (MX) Mexico Dec CPI M/M: 0.6%e v 1.0% prior; Y/Y: 6.8%e v 6.6% prior; Core CPI M/M: 0.5%e v 0.3% prior

09:00 (EU) Weekly ECB Forex Reserves

10:00 (US) Nov JOLTS Job Openings: 6.025Me v 5.996M prior

10:00 (US) Fed's Kashkari (non-voter, dove) on panel

11:30 (US) Treasuries to sell 4-Week Bills

12:00 (US) DOE Short-Term Crude Outlook

13:00 (US) Treasuries to sell $24B in 3-Year Notes

16:30 (US) Weekly API Oil Inventories

CRUDE OIL Bullish Breakout

Crude oil is has broken resistance given at 62.21 (04/01/2018 high). Strong support is given at 55.82 (07/12/2017 low). Expected to keep increasing.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. For the time being the pair lies in an upside momentum. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

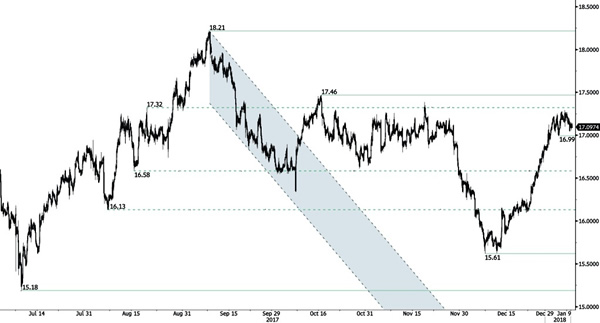

SILVER Continued Increase

Silver has been bouncing on hourly support at 16.99 (04/01/2018 low). Hourly resistance is given at 17.46 (16/10/2017 high). Expected to show continued bullish pressures.

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

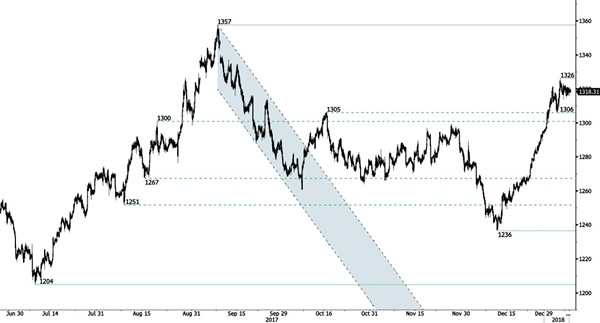

GOLD Pausing Before Another Leg Higher

Gold is pushing higher after the strong collapse even though traders are taking some profit. Hourly support is given at 1236 (12/12/2017 low). Resistance is located at 1326 (04/01/2018).

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

BITCOIN Volatile Within Uptrend Channel

Bitcoin's bullish momentum is far fom over despite strong consolidation phase. The technical structure has shown a tremendous positive short-term momentum so far. Hourly support area located around 10775 (22/12/2017 low). In the short-term, the technical structure suggests further bearish momentum. Expected to show further decline.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will reach $40'000 in 2018.

EUR/CHF Slow Increase

EUR/CHF is trading slightly higher. Hourly resistance is given at 1.1778 (25/12/2017 high). Expected to show continued short-term increase.

In the longer term, the technical structure has reversed. Strong resistance is given at 1.20 (level before the unpeg). Yet, the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).