Sample Category Title

US Yields Surged With Strong Risk Appetite, Dollar Preparing for Sustainable Rebound

Risk appetite remains strong in global financial markets. All three major US indices, DOW, S&P 500 and NASDAQ made record highs over night. Optimism carries on in Asian session. Even though Nikkei is trading a touch lower, stocks in China and Hong Kong are strong. The biggest surprise overnight was the surge in US treasury yields. 10 year yield close up 0.066 at 2.546. 2.621 key medium term resistance is now within reach. The development also helped lifting the dollar index back above 92.5. The greenback is probably finally preparing for a sustainable rebound.

10 year yield surged sharply to close at 2.546. The development continues to affirm the case that correction from 2.621 has completed at 2.034. Rise from there is in progress for retesting 2.621 resistance. Decisive break there will resume the up trend from 2016 low at 1.336. Such development should give a strong boost to Dollar. This will remain the favored case as long as 2.405 holds.

As we mentioned, before, Dollar index was close to 100% projection of 95.15 to 92.49 from 94.21 at 91.55. And it touched lower channel support already. If the fall from 95.15 is a correction, the index should be close to bottoming and reversal. Break of 55 day EMA (now at 93.21) would affirm this and turn focus to 94.21 resistance for confirmation. However, another decline through 91.55 will resume the larger down trend instead.

UK Ministers urged close cooperation between regulators after Brexit

In UK, Chancellor of Exchequer Philip Hammond and Brexit Secretary David Davis published a joint article for German newspaper Frankfurter Allgemeine Zeitung. They urged close cooperation between EU and UK finance regulators after Brexit. And with that, "such a catastrophe" like 2008 global financial crisis "doesn't happen again". And they urged to "re-double our collective effort to ensure that we do not put that hard-earned financial stability at risk, by getting a deal that supports collaboration within the European banking sector, rather than forcing it to fragment."

Moody's optimistic on APAC sovereign outlook and growth

Rating agency Moody's said that APAC sovereign outlook for 2018 is stable. It noted that the region's economic strength and high levels of trade openness well positions the nations to benefit from stronger global growth. APAC emerging markets are projected to grow by 6.5% in 2018. Frontier economies are projected to grow by 5.9% while advanced economies by 1.8%. India and China will remain the fastest growing countries in the region. While there would be gradual moderation in China and temporary slowdown in India, the impact will be offset by robust growth in other countries.

On the data front

China CPI quickened to 1.8% yoy in December but missed expectation of 1.9% yoy. PPI slowed to 4.9% yoy, above expectation of 4.8% yoy. UK productions and trade balance are the main feature in European session. Canada will release building permits, UK will release import prices later in the day.

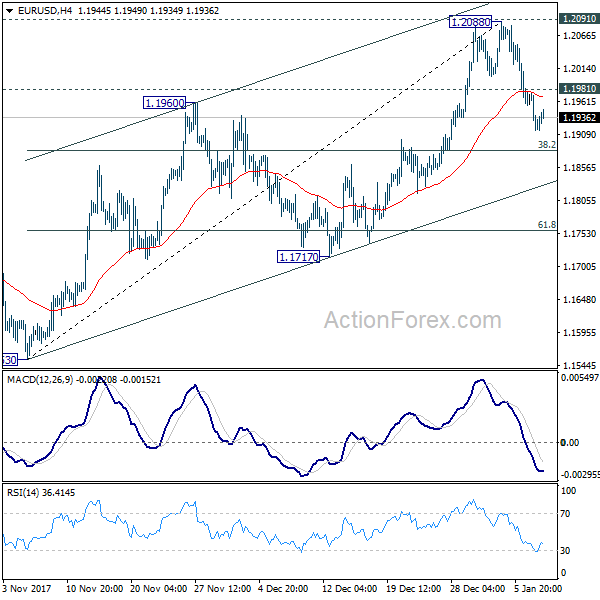

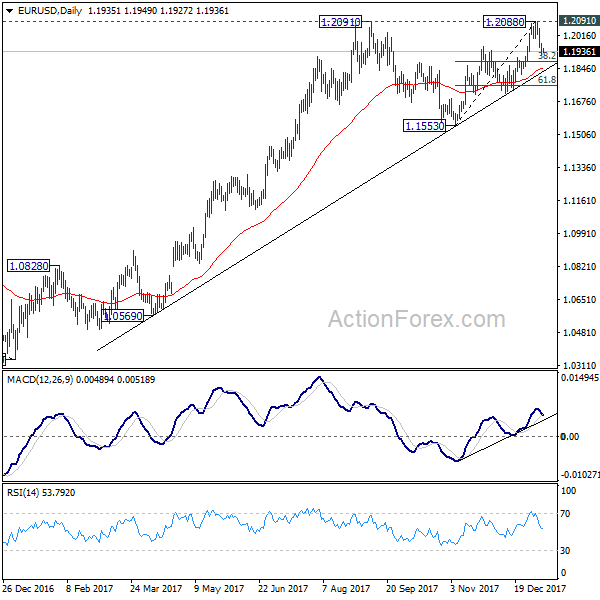

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1908; (P) 1.1942 (R1) 1.1968; More....

Intraday bias in EUR/USD remains on the downside as fall from 1.2088 is in progress. Such decline could be the the third leg of consolidation pattern from 1.2091. Break of 38.2% retracement of 1.1553 to 1.2088 at 1.1884 will target 61.8% retracement at 1.1757 and below. On the upside, above 1.1981 minor resistance will turn bias neutral first. But firm break of 1.2091 is needed to confirm up trend resumption. Otherwise, we'd expect more corrective trading in near term.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:30 | CNY | PPI Y/Y Dec | 4.90% | 4.80% | 5.80% | |

| 1:30 | CNY | CPI Y/Y Dec | 1.80% | 1.90% | 1.70% | |

| 9:30 | GBP | Industrial Production M/M Nov | 0.40% | 0.00% | ||

| 9:30 | GBP | Industrial Production Y/Y Nov | 1.80% | 3.60% | ||

| 9:30 | GBP | Manufacturing Production M/M Nov | 0.30% | 0.10% | ||

| 9:30 | GBP | Manufacturing Production Y/Y Nov | 2.80% | 3.90% | ||

| 9:30 | GBP | Construction Output M/M Nov | 0.70% | -1.70% | ||

| 9:30 | GBP | Visible Trade Balance (GBP) Nov | -11.0B | -10.8B | ||

| 13:00 | GBP | NIESR GDP Estimate Dec | 0.50% | 0.50% | ||

| 13:30 | CAD | Building Permits M/M Nov | 3.50% | |||

| 13:30 | USD | Import Price Index M/M Dec | 0.40% | 0.70% | ||

| 15:00 | USD | Wholesale Inventories M/M Nov F | 0.70% | 0.70% | ||

| 15:30 | USD | Crude Oil Inventories | -7.4M |

Elliott Wave View: DAX Still In Wave (v)

DAX Short Term Elliott Wave view suggests that pullback to 12731.46 ended Intermediate wave (X). Up from there, rally is unfolding as a 5 waves impulsive Elliott Wave structure where Minutte wave (i) ended at 12943, Minutte wave (ii) ended at 12881.5, Minutte wave (iii) ended at 13408.5, and Minutte wave (iv) is proposed complete at 13328.5. Short term, while above 13228.5, Index has scope to extend another leg higher in Minutte wave (v) before ending 5 waves up from 1/2 low (12731.46).

Minute wave ((a)) of a larger degree should end after Minutte wave (v) higher is complete. Index should then pullback in Minute wave ((b)) to correct cycle from 1/2 low before the rally resumes. Chasing the Index higher in the short term is risky, but we don’t like selling the Index either. We expect buyers to appear after Minute wave ((b)) pullback is complete in 3, 7, or 11 swing for an extension higher, provided that pivot at 1/2 low (12731.46) stays intact.

DAX 1 Hour Elliott Wave Chart

Market Morning Briefing: The Pound Is Marking Time Just Above Immediate Support At 1.3500

STOCKS

Dow (25385.80, +0.41%) is headed towards 25400-25600 as mentioned earlier and looks bullish for the coming sessions.

Dax (13385.59, +0.13%) is trading just at important resistance at 13400. In case this holds, the index could come off towards 13200 or lower; else it could move up towards 13600. We await confirmation of either a break or a rejection from current levels to get more clarity on further course of direction.

Nikkei (23796.45, -0.22%) seems to be holding below 24000 just now. But we need to see a further fall towards 23500 or lower to negate a rise past 24000 in the coming sessions. Near term likely to be bearish.

Shanghai (3428.68, +0.43%) is up strongly and is headed towards the Nov’17 high of 3450. A break above 3450 on the upside would be strongly bullish for the medium term. Watch price action near 3450.

Nifty (10637.00, +0.13%) and Sensex (34443.19, +0.26%) looks bullish just now and could be headed towards 10750-10800 and 34500-34650 levels respectively.

COMMODITIES

The US Crude stockpiles showed a decrease by 11.2mln barrels in a week against expectations of decrease by 3.9mln barrels. This has lead to a sharp rise in the Crude prices. Brent (69.21) and WTI (63.51) have moved up from levels near 68.22 and 62.25 seen yesterday morning. We now have to see if Brent stops near 70, the crucial weekly resistance or tries to move beyond that in the near term. Nymex WTI has broken above 63, faster than expected and could move up towards resistance near 65 on the weekly line charts.

Brent-WTI spread could come off to test support near 5.3-5.0 in the coming sessions before bouncing back towards 6 or higher in the longer run. Near term looks bearish.

Gold-WTI (20.66) has broken below the support near 22 and could be headed towards 19 soon. Near term looks bearish.

Gold (1311.48) has come off from 1325-1330 levels and may possibly delay the test of 1350. The current dip could extend to 1300 on the downside before rising back above 1330.

Copper (3.2300) is stable and could test 3.20 or lower in the coming sessions. Near term looks bearish to sideways.

FOREX

Dollar-Yen (112.25) has been the big mover yesterday, falling on news of BOJ reducing it's purchase of long-tenor (10-25 year) bonds. This increases the chances of a fall to 110 over the next couple of weeks.

An even bigger mover has been the Euro-Yen (134.07), which has fallen sharply from levels near 136.65 a few days ago, arresting a rise that could have otherwise targeted 138+. Now the Cross can dip towards 133.60 in the near term, which is a medium term channel Support on the weekly candles. Note that a break below 133 (not happening immediately, but if it happens at all) could be a big game changer for all markets.

This brings us to the Euro (1.1942) which is holding above the 21-day MA Support at 1.1902. It has potential to start moving up again, either from current levels or from deeper down near 1.1865. If so, the upside targets would be 1.2150-2250.

The Pound (1.3533) is marking time just above immediate Support at 1.3500 and may continue to trade sideways for a few more days within the overall uptrend that has Support in the 1.34-33 region.

We had hinted at a pause in the Aussie (0.7819) between 0.7800-60, and it has dipped within that. Further dip towards 0.7750 is possible, especially due to the new strength in the Yen.

It will be interesting to see whether the Chinese Yuan (USDCNY = 6.5288) weakens further due to Yen strength or recoups some of its losses if the Dollar weakens again.

Dollar-Rupee (63.70) looks a little Overbought in the near term and may have intra-week Resistance in the 63.80-64.00 region.

INTEREST RATES

Japanese 10 Yr Yield (0.084%) has shot up and broken resistance on the long term charts near 0.07% post the announcement of a reduction in bond purchases by the Bank of Japan. Yields had been rising for the last few days, which indicates that possibility of this policy shift was already being factored in by the markets. Consequently, the US-Japan 10 Yr yield spread has risen to 2.4654% and could rise further towards resistance near 2.52%-2.53% on the short term charts.

The US 10Yr (2.5494%), US 5 Yr (2.3274%) and US 30 Yr (2.8920%) have all risen, with the 10 Yr and 5 Yr moving past resistances on medium term and short term charts respectively. We might now see some consolidation around current levels. However, a rise in US 10 Yr towards 2.62% (last seen in Dec-16 and March-17) is possible, given that inflation expectations have risen and bearishness in global bond markets is beginning to set in. It would be interesting to keep an eye on the yields post the CPI data release on 12th Jan.

The German-US 10 Yr Yield Spread (-2.0834%) has broken support on medium term charts and might now move towards -2.10%-2.15% (last seen in Mar-Apr 2017) before moving up again. German Bund Yields (5 Yr: -0.196%, 10 Yr: 0.469%, 30 Yr: 1.316%) have all risen beyond long term resistances and we could expect some consolidation ahead.

China And Japan Stir The Pot

Unexpected moves from the Chinese and Japanese central banks threaten to shake-up the complacency in markets. The yen was the top performer Tuesday while the Swiss franc lagged. Chinese CPI is due up next. The Premium Insights locked in 145-pip gain in the EURUSD short with a detailed explanation on the next move in the pair.

USD/CNY has risen to 6.52 from 6.47 in the past two days and a big reason why might be a tweak at the PBOC. A newswire report said banks were told to adjust their use of the counter-cyclical factor. It was a factor intended to against appreciation at the time. It's worked and the yuan is close to its best levels since 2015. That strength has helped to stall investment outflows from China but with the new shift, they could once again pick up.

Ashraf has mentioned earlier this summer that the PBOC's managed appreciation of the CNY was partly forced by FX outflows into Bitcoin.

The PBOC will remain in focus in the day ahead with PPI and CPI numbers due at 0130 GMT. The CPI is expected to tick up to 1.9% from 1.7% but even with the rise, the low inflation numbers are yet-another reminder that strong growth is no guarantee of jobs.

Another move that is minor on the surface but could have major implications is the BOJ decision to trim about $20 billion of purchases of +10 year bonds. The move was seen as a possible precursor to tightening and it sent US 10-year yields to the highest since March 2017. However, it could simply be a technicality due to the yield-curve control program.

In the short-term, this will put an additional focus on the BOJ and raises the risk of further yen gains. It's complicated by the short window until the Jan 23 BOJ meeting. Look for Kuroda to try to clarify his stance then.

Shifting Narratives

G-10

Events in China and Japan have played a significant role in shaping currency markets bias over the last 24 hours and to a degree crystallising the broader-based dollar correction that started in earnest after the markets dismissed the weaker US Non-Farm Payroll number last Friday.

With the USD leaping higher in London, the PBoC surprised the market by suspending its use of the countercyclical factor in managing the exchange rate which sent a USDCNH rally in motion while adding momentum the US dollar mini-revival.The suspension does not change the longer term Yuan narrative it only removes a measure that was designed by degrees to limit the need to intervene when RMB was weakening. However, the long RMB was a well-subscribed trade this year, and the combination of stronger USD, weaker Yuan fixes, and the countercyclical surprise suggests the rampant USDCNH downtrend is temporarily snapped causing an aggressive wave of profit-taking.Local CNH traders and now in wait and see mode awaiting Pboc next manoeuvre.

This policy shift is far from a repeat of the iron-fisted Pboc moves from yesteryear. But it does appear the central banks not so invisible hand was at work curbing the rapid appreciation of the Yuan below 6.50.Expect this debate to go on.

The BOJ bond purchase reductions remains a hot topic in many circles, but the not so ” stealthy ” taper should not be interpreted as a sudden policy shift by the BoJ as they have been tapering all along.

But what’s essential for the JPY, will be the pace of the reduction given that most G-10 centeral banks are preparing to pare stimulus measures to some degree. A lot of smoke but little fire.

FX Asia

Although we could see a further wobble on USDCNH, the removal of the countercyclical is a sign of longer-term confidence in the currency in the sense the Pboc are more comfortable with how the CNY is trading and not so concerned about the threat of rapid depreciation. This policy shift is a sign of strength and confidence, but in the near term, we should expect a few hic-up on the way to a stronger Yuan.

There is no arguing the CNY complex is a considerable momentum driver for all of Asia, and the correction could dampen short-term regional sentiment as traders pause for the cause.

The Malaysian Ringgit

Structurally the MYR looks poised to rally on surging energy prices, but investors are cautious across all of EM Asia FX and tactically scaling back risk for a few reason One, the weaker Yuan fix will have a significant influence on regional inflow. Two, the recent USD dollar mini-revival has triggered profit-taking on short dollar positions globally.Three, a few Asia central banks are expressing displeasure with a stronger currency ( BOK and BoT the most vocal) Lastly, speculative views are getting a bit one-sided as a lot of investors jumped back on the regional bandwagon late 2017 early 2018 triggering some minor overbought signals.

Oil

The floor remains firm as the market continues to reiterate the core bullish sentiment drivers.

The market stirred and popped higher when the EIA bumped their global oil demand forecast for 2018. And for good measure, the American Petroleum Institute (API) reported an eye-watering draw of 11.19 million The significant inventory draw sent both WTI and Brent rocketing to 3-year highs. Traders will now look for confirmation from The U.S. Energy Information Administration report on oil inventories due to be released on Wednesday at 10:30 a.m. EDT which would cement this rally and could take WTI above 65 per barrel. No, if and or buts, the trend is your friend in the oil patch.

Gold

Gold is trading lower on the back of the resurgent USD and higher US bond yields. But stronger equity market is also taking some shine of gold as investors pare back early year equity market hedges as global stock equity markets remain on the ups.

However, much of the USD appeal is being expressed via the Euro suggesting this mini dollar revival is little more than traders unwinding overextend EUR bets and with no evidence that the broader US dollar downtrend has run its course Gold should remain sticky above USD$ 1,300.00 support levels spurred on by seasonality demand.

Gold Slides Despite Soft US Jobs Report

Gold has posted considerable losses in the Tuesday session. In North American trade, the spot price for an ounce of gold is $1310.88, down 0.72% on the day. On the release front, JOLTS Jobs Openings was unexpectedly soft, dropping to 5.88 million. This was well short of the estimate of 6.05 million. On Wednesday, the key event of the day is Import Prices.

Gold prices have shown strong gains since mid-December, leaving many investors scratching their heads. A robust US economy and a December rate hike from the Federal Reserve have increased the appetite for risk, and the stock markets have pushed higher since the New Year. This should translate into lower prices for safe-haven gold, but the base metal has jumped on the bandwagon and posted strong gains in early January. On Friday, gold touched a high of $1326, its highest level since mid-September. Will enthusiasm for gold continue? Much will depend on the strength of the US dollar – if the greenback runs into headwinds against the major currencies, gold could resume its rally.

When the Federal Reserve is in the headlines, it’s usually on the topic of interest rates. However, another important parameter is the Fed balance sheet, which has ballooned to $4.2 trillion. Starting this month, the Fed will reduce its portfolio, which grew tremendously during the financial crisis of 2008-2009. However, a strong US economy has allowed the Fed to begin trimming the balance sheet. Incoming Fed Chair Jerome Powell, who takes over in February, has estimated that the balance sheet could drop to anywhere between $2.4 trillion to $2.9 trillion after several years of cuts. Fed policymakers have not indicated a magic number for the balance sheet, but the cuts indicate a vote of confidence in the US economy.

Pound Dips Despite Soft US Jobs Report

The British pound has posted losses in the Tuesday session. In North American trade, GBP/USD is trading at 1.3523, down 0.33% on the day. In economic news, there are no major British releases on the schedule. In the US, JOLTS Jobs Openings was unexpectedly soft, dropping to 5.88 million. This was well short of the estimate of 6.05 million. On Wednesday, the UK publishes Manufacturing Production, and the US releases Import Prices.

Theresa May & Co. have not had an easy time with the Brexit negotiations, as dealing with the Europeans has been an arduous and frustrating task. Moreover, there are serious divisions within the government with regard to the talks. Compounding May’s difficulties, the British public is not impressed with May’s performance on Brexit, according to an ORB poll published on Monday. The poll found that 63% of voters are dissatisfied with the government’s handling of Brexit, and voters are almost evenly split on whether Britain will be better off after Brexit. With a razor thin majority in parliament, Prime Minister May can ill afford any mistakes, and if her government runs into trouble, she may be forced to call elections, which could shake up the markets and send the pound downwards.

When the Federal Reserve is in the headlines, it’s usually on the topic of interest rates. However, another important parameter is the Fed balance sheet, which has ballooned to $4.2 trillion. Starting this month, the Fed will reduce its portfolio, which grew tremendously during the financial crisis of 2008-2009. However, a strong US economy has allowed the Fed to begin trimming the balance sheet. Incoming Fed Chair Jerome Powell, who takes over in February, has estimated that the balance sheet could drop to anywhere between $2.4 trillion to $2.9 trillion after several years of cuts. Fed policymakers have not indicated a magic number for the balance sheet, but the cuts indicate a vote of confidence in the US economy.

UK Industrial, Manufacturing Rebound Expected to Continue in November

A weak pound and stronger global growth, particularly in the Eurozone, is driving up demand for British exports, which are boosting the UK's manufacturing sector even as domestic demand falters amid the Brexit uncertainty. Industrial and manufacturing figures out on Wednesday are expected to show output picked up in November after stalling in October.

Industrial production grew at an annual rate of 3.5% in October - the highest since December 2016, while manufacturing output was up 3.9% - also the highest since the end of 2016. Month-on-month, the figures were less impressive with no change in industrial output and manufacturing activity up just 0.1%. This would explain the expected slowdown in annual growth in November, with industrial output forecast to ease to 1.8% and manufacturing to 2.8%. However, monthly growth is expected to pick up to 0.3% for both indicators.

UK industrial output lagged the Eurozone's for much of 2017 but has been strong enough to become the bright spot of the British economy, with annual growth overtaking the dominant services sector in August. Slowing consumption, mainly as a result of a squeeze on households' disposable income from rising inflation and subdued wage growth, is weighing on services activity. Meanwhile businesses have been holding back with their investment decisions despite the upturn in the global economy as key issues about the UK's post-Brexit relationship with the EU remain unresolved.

The divergence in the fortunes of UK and Eurozone manufacturers was evident in the IHS Markit manufacturing PMI prints for December. The Eurozone's manufacturing PMI hit an all-time high of 60.6 in December, while the UK's reading missed expectations to drop 56.3 from 58.2 in November. Although this still represents a solid figure, it does underline that the British economy is growing below potential and not fully benefiting from the uptick in world growth. The outlook for the UK will likely remain clouded until at least the outline of a post-Brexit trade deal is agreed.

If the data on Wednesday beats expectations, the pound could set its eyes on the $1.36 handle again. It failed to beat the September top of $1.3656 when its recent rally stalled at $1.3612. However, after coming out unscathed from this week's cabinet reshuffle by Prime Minister May, which appears to have done little to reinforce her authority, fresh gains for sterling in the short term are possible, especially if the dollar remains subdued, and the $1.37 level could be within reach. However, if the data disappoints, the $1.35 level could provide near-term support for the pair.

NZDJPY Trades in Upward Sloping Channel in Near-Term; More Gains Expected in Long Term

NZDJPY climbed to a new three-month high of 81.29 during the Asian session and then lost some ground. The price has been moving within an upward sloping channel since December 2017 following the rebound on the 76.90 support level.

From the technical point of view, in the short-term timeframe, the price found support around the mid-level of the Bollinger band, having eased back after touching the top channel line. Despite that, the MACD oscillator dropped beneath its trigger line and is moving with weak momentum. The RSI is also pointing to reduced momentum, however, both are still standing in the positive territory. Technical indicators are signaling further losses until the 80.68 and the 80.28 barriers.

Going in the long-term timeframe, the price printed seven bullish weeks in a row and has surged more than 6% during this period. The MACD jumped above its trigger line and is trying to enter the bullish zone. Furthermore, the RSI indicator is holding above the 50 level but is flattening.

Sunset Market Commentary

Markets:

Global core bonds traded in narrow ranges today until the start of US dealings. Attracted by the very near contract low, US Treasuries faced selling pressure. The US 10-yr yield attacked 2.5% resistance and rose to the highest level since March 2017. The US yield curve bear steepens with yields up to 4.4 bps (30-yr) higher. The German yield curve shifts in similar fashion, but yield changes are more modest (+1.2 bps for 30-yr).

The yen rose against most other majors this morning as the BOJ bought fewer government with long maturities. Markets pondered whether this was a first minor step towards a less easy monetary policy further down the road. USD/JPY tried to return to the 113 mark early in European dealings, but the attempt failed. Yen strength prevailed throughout the session. That said, the dollar was a good second best. The trade-weighted dollar (DXY, currently 92.50) extended yesterday's rebound. The move was mostly technical in nature. EMU eco data (German production & exports, EMU unemployment) were again strong, but didn't help the euro. LT interest rate differentials widened in favour of the dollar, but we doubt this was an important driver for price action on the FX market. The correction/profit taking on EUR/USD and EUR/JPY longs that started after Friday's US payrolls simply continued. EUR/USD trades currently in the 1.1930 area. EUR/JPY dropped to the 134.25 area.

Sterling followed the global market trends today as there was little UK specific news to guide trading. EUR/GBP hovered in a tight sideways range in the lower half of the 0.88 big figure. The reshuffle of the UK government made little impression on markets and caused no further sterling gains. Cable declined to the low 1.35 area, mostly mirroring the over better performance of the dollar (currently 1.3520 area).

Equities maintain the positive momentum that dominated trading since the start of the new year. European equity indices show gains of about 0.5% +. The correction of the euro/rise of the dollar probably explains a slight outperformance of Europe over the US. US equities opened with modest gains of about 0.1%/0.25%. The Dow, the S&P and the Nasdaq are setting new records.

News Headlines:

German Industrial production rose a very strong 3.4% M/M and 5.6% Y/Y in November, confirming the strong momentum in Europe's biggest economy. The consensus only expected a 1.8% monthly gain. A similar picture appeared from the November foreign trade data. Exports rose 4.1% M/M (1.2% was expected). Imports rose 2.3% (0.4% expected) on strong domestic demand. The German trade surplus widened to 23.7 bn from 18.9 bn in October. The German government raised its forecast from 2017 after the publication of the data from 2.0% to 2.2%.

Euro zone unemployment declined to 8.7% in November, from 8.8% in October. It was the lowest level since January 2009. The number of unemployed in EMU fell by around 107 000 to 14.263 million, Eurostat said.

The US NFIB small business confidence declined sharply in December despite the approval of the tax reform. The headline index fell from 107.5 to 104.9, the first decline since September of last year. Series on the labour market and on compensation held up rather well. Subseries on (expected) activity eased.

The Chinese central bank took a step to loosen control over the yuan exchange rate reflecting confidence that depreciation pressures on the currency have eased. The PBOC reduced the impact of the "counter-cyclical factor" in the formula it uses to determine the mid-point reference rate for the yuan against the US dollar. That factor was designed to lessen the impact of market forces on the yuan's reference point.