Sample Category Title

Market Update – Asian Session: PBOC Resumes OMO

Headlines/Economic Data

General Trend: Asian equities trade mixed amid rise in global interest rates

Asian yield curves track steepening seen in the US

Japan 10-yr JGB yield hits highest since Oct 2017

Korea 10-year yield hits highest intraday level in 3-years

China sells 1 and 10-year bonds at lower than expected yields

Australia REIT sector underperforms amid rise in interest rates

Samsung Electronics extends losses seen post Q4 guidance

China 2017 CPI misses target as food prices decline for first time since 2003

Japan

Nikkei 225 opened -0.1%; closed -0.3%

Chip related companies decline following guidance from Samsung: Tokyo Electron -1.9%, SUMCO -1.5%

Fast Retailing -0.8%: Expected to report Q1 results on tomorrow’s session

Automakers outperform: Honda +2%, Toyota +1.7%

Mega banks track gains in the US financial sector: Sumitomo Mitsui +2.2%, Mitsubishi UFJ +1.7%, Mizuho +1%

JGB (JP) Japan MoF sells ¥2.24T v ¥2.3T indicated in 0.1% (prior 0.1%) 10-yr JGB; avg yield 0.078% v 0.059% prior; bid to cover 3.74x

(JP) Japan Financial Services Agency (FSA) said to be preparing scenarios for the ailing regional banks, including the possibility of injecting public funds and overseeing the integration of management between institutions - Nikkei

Korea

Kospi opened +0.2%, later trades lower

Continued weakness in chip sector: Samsung Electronics -2.8% (follow-through declines after Q4 guidance), Hynix -5%

Hyundai Heavy (010140.KR ) +7.5%: Said to plan to cut 2,500 jobs - South Korean Press

Financials gain amid steeper yield curve: KB Financial +1%, Woori Bank +1.7%

042660.KR May report Q4 Net loss due to cost increases and KRW - Korean press

(KR) South Korea President Moon: An increase in minimum wage is meaningful reform to economy

(KR) Moody’s comments on recent inter-Korea talks: Says the talks don’t lower the probability of a conflict for now

China/Hong Kong

Hang Seng and Shanghai Composite opened flat

Hang Seng Energy Index +1.5% (On Tuesday oil prices rose by over 2.5%), Financials +0.7%, Property/Construction +0.6%

Chow Tai Fook Jewellery +2.7%: Q3 China SSS +5% y/y

Parkson Retail Group +10% (no relevant news seen)

Great Wall Motor: -4.5%: Dec sales -16.6% y/y

(CN) PBOC may resume open market operations (OMO) soon - China Securities Journal

(CN) China PBoC OMO: Injects CNY120B combined in 7, 14-day reverse repos v skips prior; Net drains CNY0B v CNY130B prior

USD/CNY (CN) China PBoC sets yuan reference rate at 6.5207 v 6.4968 prior

(CN) CHINA DEC CPI M/M: 0.3% V 0.3%E; Y/Y: 1.8% V 1.9%E; PPI Y/Y: 4.9% V 4.8%E

China bond market remains weak in the early parts of 2018, volatility has ebbed since the beginning of November and the trend may begin to reverse - CSJ

China said to suspend 'counter-cyclical' factor in yuan (CNY) fix - US financial press

China Finance Ministry sells 1 and 10-year bonds at lower than expected yields

Australia/New Zealand

ASX 200 opened +0.1%, has since pared gains; closed -0.6%

ASX 200 REIT Index -1.3%, Telecom Services -1.1%, Energy -0.9%, Utilities -0.7%, Resources -0.5%, Financials -0.2%

(AU) Australia Nov 3-month Job Vacancies: 2.7% v 6.0% prior

(AU) China demand for Australian property is expected to moderate this year amid the impact of new state and federal taxes - Australian

Looking Ahead: Australia Nov Retail Sales due for release on Thursday

Other Asia

(PH) Philippines Budget Sec Diokno: Q4 GDP growth can be around 7% or higher (vs 6.9% in Q3)

(PH) Philippines Nov Trade Balance: -$3.8B (multi-year high for the deficit) v -$2.7Be

Taiwan Semi, 2330.TW Reports Dec Rev NT$89.9B v NT$93.2B m/m v NT$78.1B y/y, 2017 Rev NT977.5B, +3.1% y/y

North America

US equity markets ended mostly higher: Dow +0.4%, S&P500 +0.1%, Nasdaq +0.1%, Russell 2000 -0.1%

S&P500 Health Care Sector +1.2%, Financials +0.8%; Real Estate -1.1%, Utilities -1%

(US) Fed's Kashkari (dove, non-voter): inflation that's too low is a bigger concern than inflation that's too high; Economic recovery has been frustratingly slow; believes slow pace of recovery is due to psychological scarring from the financial crisis

(US) Trump Administration said it will not permit drilling off of the coast of Florida – US press

(US) Weekly API Oil Inventories: Crude: -11.2M v -5M prior

Looking Ahead: US weekly DOE Crude Oil Inventories due for release

Europe

(UK) Prime Min May reportedly has scrapped plan to create cabinet post for a no-deal Brexit situation - UK press

(UK) EU Chief Brexit Negotiator Barnier: the integrity of the single market is crucial in Brexit; risk of a disorderly Brexit has decreased; Future trade relationship with UK will not be frictionless

(UK) UK Brexit Ministry: proposes three-month window after Brexit to begin court cases under general principles of EU law

(UK) According to the EU companies in the UK may not have automatic access if there is no Brexit deal - financial press

(UK) UK Chancellor of the Exchequer Hammond and Brexit Sec Davis wrote a joint article in the German Press suggesting close cooperation between the EU and UK regulators following Brexit, as part of an expansive trade agreement that covers goods and financial services (Note: Both Davis and Hammond are expected to be in Germany on Wed)

(UK) Germany is said to show opposition to Brexit trade deal plan proposed by the UK - UK Press

(UK) British Chambers of Commerce (BCC): Survey shows UK services and manufacturing companies less confident about 2018 revenues

(IT) Five Star Party says its no longer time for Italy to leave the euro zone - Italian press

(CN) EU Ambassador to China Schweisgut: EU hopes for full China market access with reciprocity

World Bank raises global economic growth outlook at +3.1% (prior +2.9% forecasted)

Continental [CON.DE]: Reports Prelim FY17 Rev €44B v €43.9Be; Guides initial FY18 Rev ~€47B, +6.8% y/y, adj EBIT margin 10.5%

Akzo Nobel [AKZA.NL]: Shortlist of bidders for chemical unit reportedly include Carlyle Group and Bain - press

Looking Ahead: UK Nov Industrial Production, Manufacturing Production and Trade data due for release

Levels as of 01:00ET

- Nikkei225 -0.3%, Hang Seng +0.3%; Shanghai Composite -0.3%; ASX200 -0.6%, Kospi -0.4%

Equity Futures: S&P500 -0.1%; Nasdaq100 -0.1%, Dax -0.0%; FTSE100 -0.1%

EUR 1.1949-1.1928; JPY 112.79-112.17; AUD 0.7831-0.7808;NZD 0.7173-0.7140

Feb Gold -0.2% at $1,310/oz; Feb Crude Oil +0.8% at $63.45/brl; Mar Copper +0.2% at $3.23/lb

BOJ Trimmed JGBs Purchase, Aiming At Yield Curve Steepening Instead Of Policy Normalization

BOJ offered to buy 190B yen of JGBs with maturity of 10- 25 years, down 10B yen from the purchase made on December 28. It also reduced the purchase of JGBs with maturity of 25- 40 by the same amount to 90B yen. The move has heightened speculations that the central bank is preparing to trim its stimulus measures. The market reactions match with the speculations with USDJPY slipping -0.42% while EURJPY down -0.65% on Tuesday. Japanese longer- dated 20- and 40-year bond yields rose to their highest in a month. Longer- term US Treasuries were also affected by BOJ’s move with 10-year yields gaining +6 points to 2.546%. Of course, the movement of US Treasuries was also affected by the auctions this year.

We do not view this as an abrupt shift from BOJ’s monetary stance. In December, the central bank, while turning more upbeat on the recovery outlook, kept the targets for short- and long-term interest rates unchanged at -0.1% and around 0%, respectively, and the guideline for JGB purchases at an annual pace of about 80 trillion yen. We have mentioned in our October report (https://www.actionforex.com/action-insight/central-bank-views/53808-boj-left-stimulus-unchanged-downgraded-inflation-forecasts) that BOJ’s monetary base has been shrinking with the monthly JGBs purchase steadily falling since February 2017. The annual increase in JGB buying has fallen to 50-ishh trillion yen in December last year, from about 79 trillion yen in the same period in 2016. This suggests that BOJ has gradually been moving away from targeting monetary base growth, to yield curve control (since its introduction in September 2016), as the key policy instrument.

Over the past year, most of the reduction in purchases was JGBs with 1-10 year maturity, compared with the long-dated ones on Tuesday. We believe the aim of BOJ is on a steepening of the back end of its yield curve so as to provide support for banks and real money investors. A steeper yield curve would help raise profitability of financial institutions, allowing them to ease lending standards and take risks on their balance sheets. With CPI staying far below the +2% target, it still remains a long way for the BOJ to begin considering policy normalization.

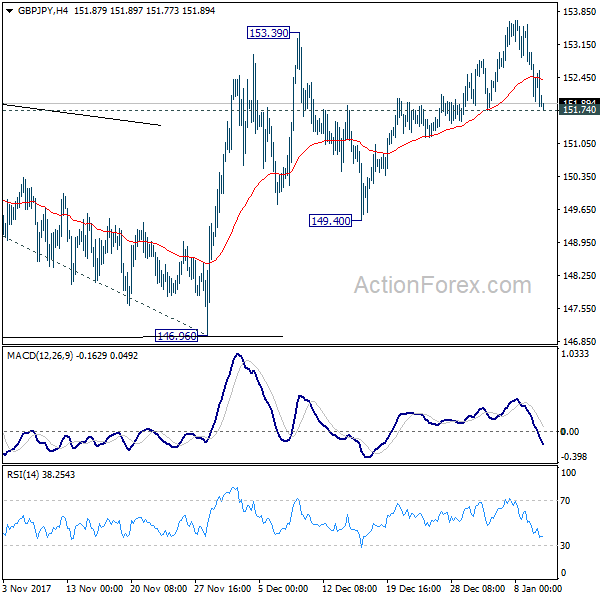

GBP/JPY Daily Outlook

Daily Pivots: (S1) 151.77; (P) 152.66; (R1) 153.40; More...

No change in GBP/JPY's outlook. As long as 151.74 minor support holds, further rally is in favor. Current rise should target 61.8% projection of 139.29 to 152.82 from 146.96 at 155.32. However, firm break of 151.74 will turn focus back to 149.40 support instead.

In the bigger picture, it now looks like GBP/JPY has finally taken out 38.2% retracement of 195.86 to 122.36 at 150.43. Medium term rise from 122.36 should be targeting 61.8% retracement at 167.78. This will now be the favored case as long as 146.96 support remains intact.

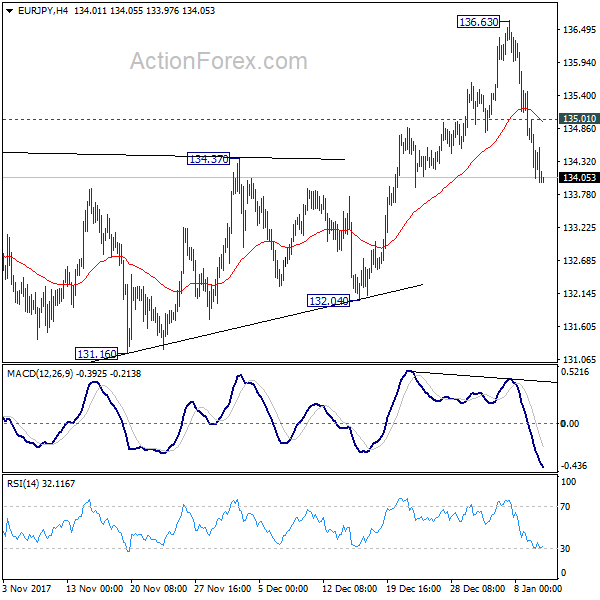

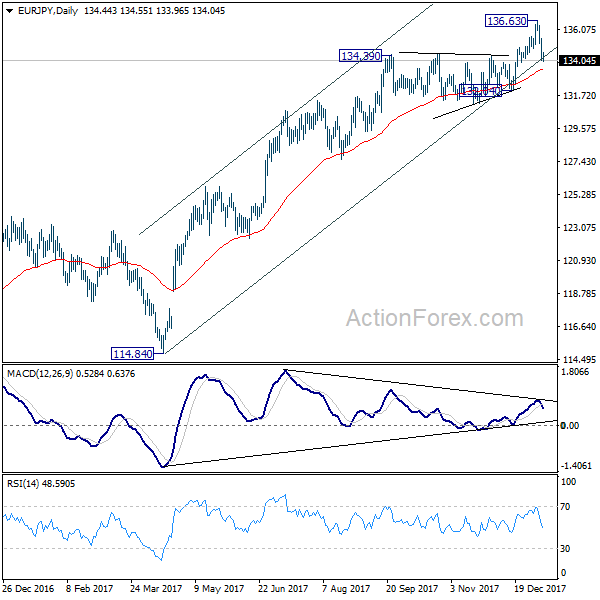

EUR/JPY Daily Outlook

Daily Pivots: (S1) 133.84; (P) 134.65; (R1) 135.27; More....

Intraday bias in EUR/JPY remains on the downside for 132.04 key support. Prior break of 134.39 resistance turned support is seen as early sign of trend reversal. But it's yet to be confirmed. On the upside, above 135.01 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 136.63 holds.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). It should now be targeting 141.04/149.76 resistance zone. On the downside, break of 132.04 support is needed to indicate medium term reversal. Otherwise, outlook will stay bullish in case of deep pull back.

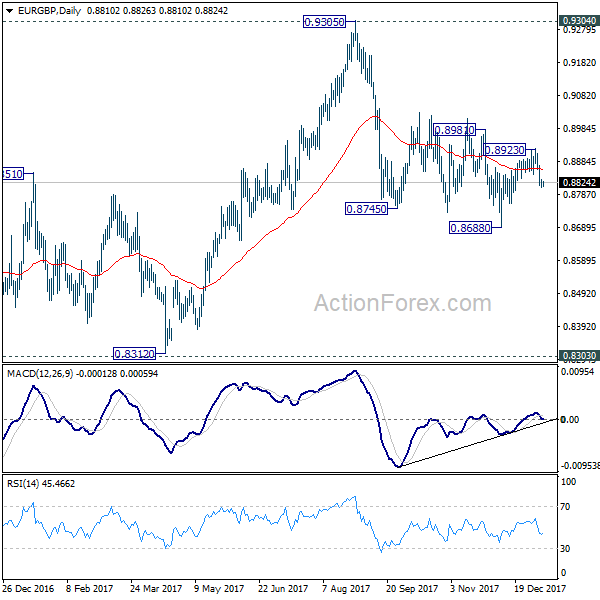

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8804; (P) 0.8819; (R1) 0.8829; More...

Intraday bias in EUR/GBP remains on the downside for the moment. Rebound form 0.8688 should have completed at 0.8923. Deeper fall should be seen to 0.8688. Break will resume whole decline from 0.9305 and target 0.8303 key support around. This will now be the favored case as long as 0.8923 resistance holds.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Aussie Trading A Tad Higher In The Asian Session

For the 24 hours to 23:00 GMT, the AUD declined 0.24% against the USD and closed at 0.7822.

LME Copper prices rose 0.1% or $7.5/MT to $7092.0/MT. Aluminium prices declined 1.6% or $34.0/MT to $2143.5/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7825, with the AUD trading slightly higher against the USD from yesterday's close.

Earlier today, in China, Australia's largest trading partner, the producer price index (PPI) climbed 4.9% on an annual basis in December, rising at its slowest pace in more than a year. The PPI had recorded a gain of 5.8% in the previous month, while investors had envisaged for a rise of 4.8%. Meanwhile, the nation's consumer price index (CPI) advanced less-than-expected by 1.8% on an annual basis in December, compared to market expectations for a rise of 1.9%. The CPI had increased 1.7% in the previous month.

The pair is expected to find support at 0.7800, and a fall through could take it to the next support level of 0.7776. The pair is expected to find its first resistance at 0.7857, and a rise through could take it to the next resistance level of 0.7890.

Looking ahead, Australia's retail sales figures for November, scheduled to be released overnight, will be on investors' radar.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

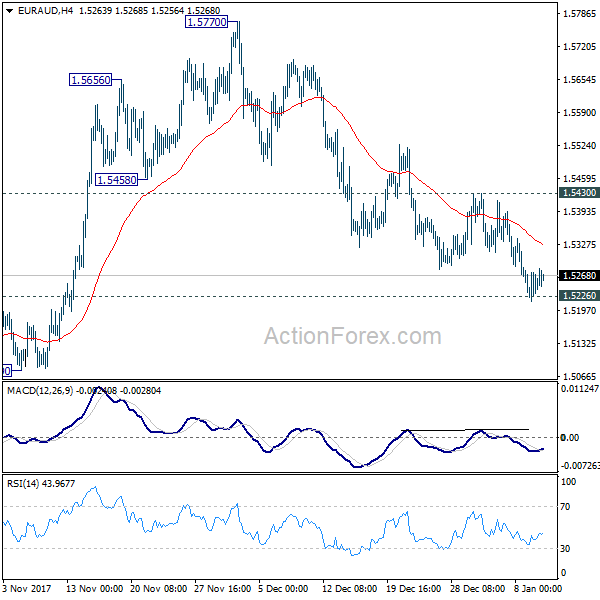

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5222; (P) 1.5248; (R1) 1.5279; More....

Focus remains on 1.5226 key support level in EUR/AUD. As long as this support holds, further rise will still be in favor. Break of 1.5430 minor resistance will now indicate completion of the correction from 1.5770 and turn bias back to the upside for retesting 1.5770. However, sustained break of 1.5226 will indicate larger reversal and target 1.4949 support next.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top (2015 high) has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. We'll hold on to this bullish view as long as 1.5226 resistance turned support holds. Firm break of 1.6587 will resume long term rise from 1.1602 (2012 low). However, sustained break of 1.5226 will indicate trend reversal and target 1.3624 again.

Euro-Zone’s Unemployment Rate Fell To Its Lowest Level Since January 2009 In November

For the 24 hours to 23:00 GMT, the EUR declined 0.28% against the USD and closed at 1.1935, shrugging off upbeat economic releases across the Euro-bloc.

Data revealed that the unemployment rate in the Euro-zone declined to a nearly 9-year low level of 8.7% in November, meeting market expectations and reflecting an enduring labour market growth. Unemployment rate had recorded a level of 8.8% in the previous month.

Separately, Germany's seasonally adjusted industrial production accelerated by the most in over 8 years, after rebounding 3.4% on a monthly basis in November, suggesting that the industrial sector is likely to gain strength in the coming months. Markets had expected industrial production to advance 1.8%, after recording a revised drop of 1.2% in the previous month. Also, the nation's seasonally adjusted trade surplus widened more-than-anticipated to €23.7 billion in November, after recording a surplus of €18.9 billion in the previous month, as growth in exports outpaced that of imports. Market participants were anticipating the nation to post a trade surplus of €21.3 billion.

In the US, data revealed that the NFIB small business optimism index surprisingly eased to a level of 104.9 in December, confounding market expectations for an advance to a level of 107.8. The index had registered a reading of 107.5 in the prior month. On the other hand, the nation's JOLTs job openings unexpectedly slid to a level of 5879.0K in November, hitting a 6-month low level, defying market consensus for a rise to a level of 6025.0K. JOLTs job openings had registered a revised reading of 5925.0K in the previous month.

In the Asian session, at GMT0400, the pair is trading at 1.1942, with the EUR trading 0.06% higher against the USD from yesterday's close.

The pair is expected to find support at 1.1914, and a fall through could take it to the next support level of 1.1885. The pair is expected to find its first resistance at 1.1973, and a rise through could take it to the next resistance level of 1.2003.

In absence of any crucial macroeconomic releases in the Euro-zone today, investors would look forward to the US MBA mortgage applications data followed by the nation's import and export price indices, both for December, slated to release later in the day.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Pound Trading Marginally Lower, Ahead Of Key Economic Releases In The UK

For the 24 hours to 23:00 GMT, the GBP declined 0.22% against the USD and closed at 1.3539.

In the Asian session, at GMT0400, the pair is trading at 1.3534, with the GBP trading slightly lower against the USD from yesterday’s close.

The pair is expected to find support at 1.3499, and a fall through could take it to the next support level of 1.3465. The pair is expected to find its first resistance at 1.3575, and a rise through could take it to the next resistance level of 1.3617.

Moving ahead, traders would look forward to UK’s industrial as well as manufacturing production, total trade balance and construction output data, all for November, set to release in a few hours. Moreover, the NIESR GDP estimate for the three months to December, scheduled to release later in the day, will be eyed by investors.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Japanese Yen Extends Its Gains In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.45% against the JPY and closed at 112.64.

In the Asian session, at GMT0400, the pair is trading at 112.26, with the USD trading 0.34% lower against the JPY from yesterday’s close.

The pair is expected to find support at 111.96, and a fall through could take it to the next support level of 111.67. The pair is expected to find its first resistance at 112.76, and a rise through could take it to the next resistance level of 113.27.

Going ahead, market participants would focus on Japan’s flash leading economic as well as coincident indices, both for November, slated to release in the early hours of tomorrow.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.