Sample Category Title

GBPUSD – Strengthens, Faces Further Bullishness

GBPUSD - The pair extended its recovery higher on Thursday to open the door for more strength. Support lies at the 1.3400 level where a break will turn attention to the 1.3350 level. Further down, support lies at the 1.3300 level. Below here will set the stage for more weakness towards the 1.3250 level. Conversely, resistance stands at the 1.3500 levels with a turn above here allowing more strength to build up towards the 1.3550 level. Further out, resistance resides at the 1.3600 level followed by the 1.3650 level. Its daily RSI is bullish and pointing higher suggesting further upside pressure. On the whole, GBPUSD looks to strength further.

Streaking Gold Pushes Towards $1300

Gold continues to move higher during Christmas week, and has climbed to its highest level since the end of November. In Thursday’s North American session, the spot price for an ounce of gold is $1294.44, up 0.56% on the day. On the release front, today’s key indicator was unemployment claims, which remained unchanged at 245 thousand. This was higher than the estimate of 240 thousand.

The US dollar is broadly lower on Thursday, and gold has taken full advantage, posting considerable gains. Gold has jumped 3.0% percent since December 11, and is within striking distance of the symbolic $1300 level, which was last breached in late October.

In the U.S, the first key indicators of the holiday week were mixed. CB Consumer Confidence slowed to 122.2, well off the estimate of 128.2 points. Pending Home Sales posted a small gain of 0.2%, beating the estimate of -0.4%. Housing numbers continue to beat expectations. Last week, Housing Starts came in at 1.30 million, beating the forecast of 1.25 million. On Tuesday, New Home Sales sparkled, with a gain of 733 thousand. This easily beat the estimate of 654 thousand, and was the highest reading since September 2007. On Thursday, the US releases unemployment claims, which is expected to drop to 241 thousand.

US housing numbers continue to beat expectations, as Pending Home Sales surprised the markets with a gain of 0.2%. Last week, Housing Starts came in at 1.30 million, beating the forecast of 1.25 million. On Tuesday, New Home Sales sparkled, with a gain of 733 thousand. This easily beat the estimate of 654 thousand, and was the highest reading since September 2007. On Thursday, the US releases unemployment claims, which is expected to drop to 241 thousand

Pound Breaks Out Of Christmas Doldrums, Hits 2-Week High

The British pound continues to have a quiet week and is showing little movement in the Thursday session. In North American trade, GBP/USD is trading at 1.3444, up 0.34% on the day. Earlier in the day, the pair climbed to its highest level since December 14. On the release front, the sole British event was High Street Lending ,which slipped below the 40-thousand threshold for the first time since September 2016. The indicator dipped to 39.5 thousand in November, shy of the estimate of 40.6 thousand. In the US, unemployment claims disappointed, remaining unchanged at 245 thousand. This was higher than the estimate of 240 thousand.

In the U.S, the first key indicators of the holiday week were mixed. CB Consumer Confidence slowed to 122.2, well off the estimate of 128.2 points. Pending Home Sales posted a small gain of 0.2%, beating the estimate of -0.4%. Housing numbers continue to beat expectations. Last week, Housing Starts came in at 1.30 million, beating the forecast of 1.25 million. On Tuesday, New Home Sales sparkled, with a gain of 733 thousand. This easily beat the estimate of 654 thousand, and was the highest reading since September 2007. On Thursday, the US releases unemployment claims, which is expected to drop to 241 thousand.

With no major British indicators during Christmas week, the pound has shown limited movement. That could change next week, with the release of PMI reports, which are highly-respected barometers of the services, manufacturing and construction sectors. The PMIs have been pointing to expansion in all three industries, with notably strong growth in manufacturing, which has received a boost for strong global demand for British exports. As well, the weak pound has also made British products less expensive.

High on Prime Minister Theresa May’s New Years’ agenda is Brexit. The talks are finally shifting to trade, much to the relief of May, who has faced harsh criticism at home over her handling of the talks with the Europeans. May has her work cut out for her, with little more than a year until Britain leaves the European Union. Her cabinet remains split on what a Brexit deal will look like, and the Europeans are in no mood to do Britain any favors, in order not to give other EU members any ideas about jumping ship. What will a trade relationship between Britain and the European Union look like? That remains unclear, but it’s no secret that the two sides remain far apart on the “end phase” of what a Brexit agreement will look like, and both Britain and the EU will have to show some flexibility in order to hammer out an agreement. Given the lack of trust between the parties, there will be more bumps on the Brexit road, which could weigh on the British pound in the coming months.

Japanese Yen Gains Ground As Retail Sales Sparkle

After an uneventful week, USD/JPY has lost ground in the Thursday session. In North American trade, the pair is trading at 112.97, down 0.32%. On the release front, Japanese indicators were strong. Preliminary Industrial Production improved to 0.6%, edging above the estimate of 0.5%. Retail Sales, the primary gauge of consumer spending, surged 2.2%, crushing the estimate of 1.1%. In the US, unemployment claims disappointed, remaining unchanged at 245 thousand. This was above the estimate of 240 thousand.

In the US, key indicators were mixed on Wednesday. CB Consumer Confidence slowed to 122.2, well off the estimate of 128.2 points. Pending Home Sales posted a small gain of 0.2%, beating the estimate of -0.4%. Housing numbers continue to beat expectations. Last week, Housing Starts came in at 1.30 million, beating the forecast of 1.25 million. On Tuesday, New Home Sales sparkled, with a gain of 733 thousand. This easily beat the estimate of 654 thousand, and was the highest reading since September 2007.

Japan has seen an impressive rebound in economic growth in 2017, and key consumer indicators, released earlier this week, beat their forecasts. Tokyo Core CPI, the primary gauge of consumer inflation, climbed 0.9%, in December its strongest gain since March 2015. This edged above the forecast of 0.8%. National Core CPI improved to 0.9%, just above the estimate of 0.8%. There was more positive news as Household Spending rebounded with an excellent gain of 1.7%, crushing the estimate of 0.6%. This reading marked a 5-month high.

Bank of Japan Core Inflation, which the BoJ relies on to measure inflation, climbed 0.6%, above the estimate of 0.5%. This marked a 3-month high. Other inflation indicators also beat their estimates, underscoring that inflation is on the move. Still, the BoJ has made it abundantly clear that it will not tighten its ultra-accommodative monetary policy until inflation is close to the Bank’s 2 percent inflation target. The minutes of the October meeting indicated that most members favored a continuation of the current ultra-accommodative policy. This could weigh on the yen, as other central banks, such as the ECB, the Federal Reserve and the Bank of Canada have tightened policy in recent months, widening divergence with the Bank of Japan.

CAC Edges Lower in Holiday-Thinned Trade

European stock markets are having a quiet Christmas week, and the CAC is showing limited movement in the Thursday session. Currently, the CAC is at 5358.30, down 0.20% on the day. There are no French indicators for the remainder of the week. The sole event on Thursday was the release of the ECB Economic Bulletin, which comes two weeks after the December ECB policy meeting.

The French economy continues to rebound, as indicators in the second largest economy in the eurozone continue to point upwards. The economy has been expanding, exports are up and unemployment has dropped. Consumer spending, a key driver of economic growth, looked sharp in November, jumping 2.2%. The impressive reading comes after a decline of 1.9% in October and marked the highest gain since February 2012.

The eurozone economy has rebounded in 2017. France has also enjoyed stronger economic conditions. The manufacturing and export sectors have benefited from stronger global demand, and unemployment levels have dropped. The election of Emmanuel Macron, who is pro-business and in favor of streamlining the economy, has impressed investors and boosted the French stock markets. The CAC has responded positively, climbing 10.6% in 2017. Fourth quarter numbers in both France and the eurozone have been steady, and expectations are that the positive trend will continue into 2018, which should translate into further gains for the CAC.

Inflation, long a sore point in the eurozone economy, has moved higher. Annual average inflation inched up to 1.5% in November, up from 1.4% in October. This marked a multi-year high. Earlier this month, in a nod to stronger economic activity in 2017, the ECB raised its forecasts for growth and inflation for the eurozone from this year through to 2019. Still, inflation remains well below the ECB target of around 2.0%, and ECB policymakers are unlikely to announce an end to their stimulus package until inflation moves closer to the 2.0% target.

Dollar Stays Weak after Economic Data, Initial Claims Unchanged at 245k

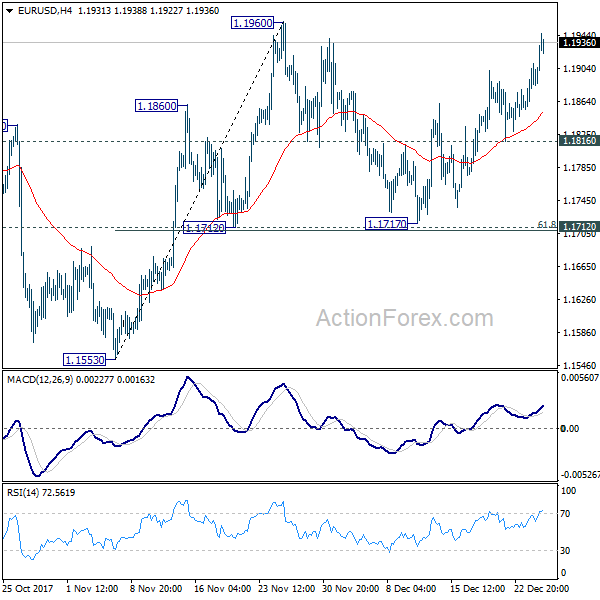

Dollar stays weak in early US session as economic data provide little inspiration. Initial jobless claims were unchanged at 245k in the week ended December 23, above expectation of 241k. Four week moving average rose 1.75k to 237.75k. Continuing claims rose 7k to 1.94m in the week ended December 14. Wholesales sales rose 0.7% in November. Trade deficit widened to USD -69.7b in November. With the broad-based selloff in Dollar, EUR/USD should now be heading for a test on 1.1960 resistance.

ECB monthly bulletin noted that the economic recovery in the Eurozone is solid and broad based. While inflation pressure remained subdued, it's expect to pick up gradually. Overall, ample degree of monetary accommodation is still needed to drive inflation back to target. Also, ECB left open the option to extend the asset purchase program beyond September 2018 if necessary.

Summary of opinions of December BoJ meetings showed that due to improving economic outlook, there were calls for discussions on raising interest rate or cutting ETF purchases. One member noted urged the central bank to consider whether "adjustments in the level of interest rates will be necessary" if inflation and economic outlook improves further. Another board member warned of side effects of ETF purchases.

Released from Japan today, retail sales rose 2.2% yoy in November, above expectation of 1.0% yoy. Industrial production rose 0.6% mom in November, above expectation of 0.5% mom.

EUR/USD Mid-Day Outlook

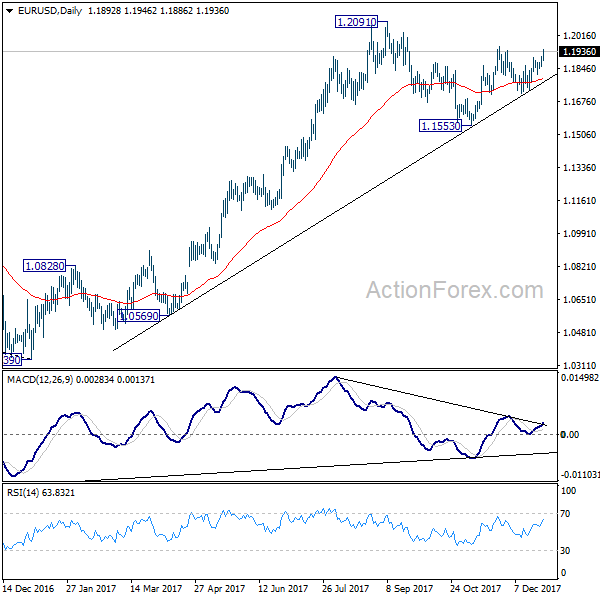

Intraday bias in EUR/USD remains on the upside for 1.1960 resistance. Break will resume whole rally from 1.1553 and target 1.2091 high. On the downside, break of 1.1816 minor support is needed to indicate completion of the rebound form 1.1717. Otherwise, near term outlook will stay cautiously bullish in case of retreat.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1435) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

USDJPY Intraday Bearish Below 113.10 Level

The U.S dollar has retreated sharply against the Japanese yen, following much better than expected Japanese economic data and overall weakness in the greenback. The USDJPY has so far found intraday support just below the 112.70 level, but remains under selling pressure around the 112.80 region. Better than expected Japanese Industrial Production and Retail Sales figures helped boost the Japanese yen, while falling U.S bond yields pushed the greenback lower. Traders now look to high-impact U.S economic data, and the key 92.60 level on the U.S dollar index.

The USDJPY pair is likely to remain intraday bearish while trading below the 113.10 level, further declines towards the 112.70 and 112.40 levels seem possible.

Should the USDJPY pair find buying demand above the 113.10 level, upside resistance is found at the 113.30 and 113.60 levels.

USDCAD Futher Bearish Below 1.2623 Level

The U.S dollar has moved to its lowest trading level against the Canadian dollar in over eight-weeks, as commodity related currencies continue to break higher. The USDCAD has so far found intraday support just above the 1.2600 level, but risks further heavy losses after breaking the two-month trading range in the pair. Going forward, the 1.2623 level remains key, with sellers firmly in control while price-action holds below this major technical level. Moving into the U.S session, USDCAD traders will likely focus on rising WTI Oil prices and falling U.S treasury-bond yields.

The USDCAD pair remains strongly bearish while trading below the 1.2623 level, further losses towards the 1.2579 and 1.2535 levels appear possible.

Should the USDCAD pair move above the 1.2623 level, buyers may attempt to push price-action back towards the 1.2672 and 1.2710 resistance areas.

Canadian Dollar Hits 9-Week High

The Canadian dollar continues to rally, and has recorded five straight winning sessions. Currently, USD/CAD is trading at 1.2616, down 0.30%. There are no Canadian releases this week. In the US, today's key event is unemployment claims, which is expected to drop to 240 thousand.

USD/CAD is down 1.9% since December 18, as the Canadian dollar has improved to its highest level since late October. Canada's GDP in October disappointed, with a flat reading of 0.0%. Still, recent consumer indicators have been strong. Retail Sales sparkled with a gain of 0.8% in October, well above the forecast of 0.4%. This was the indicator's highest gain since April. As well, CPI improved to 0.3% in November, marking a five-month high. This edged above the estimate of 0.2%. The Canadian dollar has enjoyed an excellent December, but could face some headwinds next month, as the Federal Reserve is widely expected to raise interest rates at its January meeting, following the rate hike earlier in December.

With the US economy expanding above 3% in the third quarter, the Federal Reserve remains on track for another rate hike in January. The CME Group has pegged the odds of a January hike at 100%, which could give a boost to the US dollar. If the economy continues its impressive pace of growth above 3%, the Fed could raise rates up to four times in 2018. Despite strong economic conditions, the Federal Reserve's inflation target of 2.0% remains elusive. Fed Chair Janet Yellen and other FOMC members have said that they expect that the strong labor market will lead to higher inflation. Although this is yet to materialize, of significance to the markets is the commitment of the Fed to press ahead with rate hikes despite low inflation.

US Futures Steady in Quiet Trade

Another Quiet Holiday Session Lined Up

US equity markets are poised to open a little higher on Thursday after making marginal gains a day earlier in light trade.

It's likely to be another relatively quiet day, as is often the case during the holiday period, and a lack of economic events on the calendar won't help matters. There is a few pieces of data scheduled for release, although its mostly low and medium tier data, including jobless claims, Chicago PMI and trade balance figures. We'll also get crude inventories data, as oil continues to trade near its highs with WTI pushing $60.

USD Under Pressure Again on Lower US Yields

The US dollar is trading lower for a second day on Thursday, still struggling after yields on Treasuries slipped on Wednesday. The flattening of the yield curve has triggered concerns that investors are possibly pricing in a slowing of the economy or even a recession and while this has historically happened on such expectations, I'm not convinced this is the case this time.

Given the current environment, it's possible that this is more a reflection of longer term interest rates and the low inflation environment than the economic prospects. Still, if yields on long term US debt don't rise or even fall as the Fed raises interest rates, it could fuel fears of an impending recession.

Bitcoin Tumbles as Tough Holiday Period Continues

Bitcoin is coming under selling pressure once again, with efforts by South Korean authorities to rein in speculation being blamed for the drop of around 10%. While this is likely a contributing factor, I wonder if given the pre-holiday drop, whether speculators have become more sensitive to negative news.

We saw plenty of this in reverse on the way up, with positive news triggering significant rises and negative news being brushed aside. It wouldn't surprise me if we see prices heading back below $10,000 before they find their feet again.