Sample Category Title

EUR/USD: US Pending Home Sales

The US Dollar was slighlty higher against the European single currency, following pending sales data on Wednesday. The EUR/USD currency pair fell just 5 base points or 0.04% to reveal delayed, but short-term drop entering the 1.1890 area.

Contracts to purchase previously owned houses increased in November, supported by the job growth in the strengthening US economy. The National Association of Realtors states that pending home sales indicator rose to 109.5 points to show a 0.2% gain for the month. The real estate market restored some momentum after inactivity for much of 2017 due shortage of inventory, which caused an increase in prices, and a lack of both land and labour.

CAD/CHF 1H Chart: Rate Guided By Several Patterns

CAD/CHF has been moving in a channel down since early September. The pair diminished its trading range in the given pattern during the first half of December, but managed to reach its upper boundary once again mid-Wednesday. The pair has since found support at the monthly R1 and the 100-hour SMA at 0.7780. Given that the weekly PP is likewise located nearby, bulls might still push higher in this session and re-test the senior channel near the 0.7840 mark. By and large, technical signals point to a possible price decrease within the upcoming week. This fall might not be steep due to several strong support levels, but it should nevertheless guide the Canadian Dollar towards the 0.7650 area in the medium term.

USD/ZAR 1H Chart: Senior Channel Holds

The US Dollar has been confined in a channel down against the South African Rand during the past two months. Its lower boundary was tested early in this session, when the rate was unable to move past the weekly S3 located at 12.26. This low volatility suggests that the pair might reverse from this medium-term pattern and initiate a new wave up. The steepness of two more junior patterns likewise demonstrate that the Greenback has remained near their upper boundaries, thus pointing to a possible upside breakout. The nearest resistance is set by the 55– and 100-hour SMAs circa 12.50. This area is likewise reinforced by the weekly S2 and the 200-hour SMA. Thus, the Greenback could hinder near this territory for a while prior to moving towards the upper boundary of the senior channel. In case the southern barrier does not hold, no support that could halt the pair is located nearby.

Technical Outlook: USDJPY – Fresh Bears Penetrate Daily Cloud And May Extend Towards Key Support At 112.00

The pair came under increased pressure and fell sharply on Thursday, driven by fresh dollar's sell-off. Bearish acceleration penetrated daily cloud after descending cloud top acted as solid support and limited downside attempts in past few sessions. Fresh bears dipped to 112.66, finding temporary footstep just ahead of important Fibo support at 112.64 (Fibo 61.8% of 112.02/113.63 upleg), with recovery attempts facing strong barrier at 112.83 (broken daily Tenkan-sen / cloud top). Increasing bearish outlook sees risk of further weakness on sustained break below 112.64, as daily cloud twists next week and attracts. Extension below 112.64 pivot would look for 112.29 (daily Kijun-sen) and key near-term support at 112.00 (15 Dec low) loss of which would generate strong bearish signal.

Res: 112.83, 113.02, 113.26, 113.38

Sup: 112.64, 112.40, 112.29, 112.00

Technical Outlook: GBPUSD – Fresh Bullish Acceleration Looks For 1.3500+ Extension

Cable hit two-week high at 1.3455, which also marks Fibo 61.8% retracement of 1.3549/1.3300 downleg, on fresh bullish acceleration in Asian / early European trading on Thursday.

Eventual break above week-long congestion tops at 1.3400 signaled fresh advance, confirming higher base at 1.3300 zone.

Pound received strong support from end-of-year dollar selling and looks for fresh bullish signal on close above 1.3455 Fibo barrier for extension towards psychological 1.3500 barrier and key near-term resistance at 1.3549 (01 Dec high).

Former pivotal barrier at 1.3400 zone (reinforced by broken 20SMA) is expected to keep the downside protected.

Res: 1.3500, 1.3520, 1.3549, 1.3570

Sup: 1.3429, 1.3400, 1.3387, 1.3367

Bitcoin Dropped Nearly 17% On A Regulatory News

Regulatory threats have minimal effetcs on Bitcoin

It is unfair to call retail investors not sophisticated

December 22nd's low marks the turning point

Once again, the regulatory threats have hit the crypto king, Bitcoin. After forming a high of $16416 this week, the cryptocurrency came under a selling pressure as traders showed their reaction to South Korea’s news. The country is determined to curb the speculative market and it would take measures to stop and review various crypto-exchanges.

The reality is that the market is way to overheated and no one wants the cryptocurrency popping on their door steps. However, this is surely not the first time that we have witnessed this kind of reaction in the Bitcoin price Throughout this years, we have heard many similar messages (followed by actions) from China and yet Bitcoin made a high of $19338.

Cryptocurrency market is mainly driven by retail investors and they have the ultimate control in terms of the capital flow (at least for now). It is mainly dubbed that retail investors are not sophisticated clients but we all know that institutions or so called sophisticated clients do create even more bigger blunders. So, it may be a bit unfair to think that if the currency is supported by retail clients it has no value and if it is supported by institutions than it has more value.

It would not be long before when some employers would even give an option to their employees that they can get paid in Bitcoin. Of course, the capital gain part (if the bitcoin price continue to surge) is tax free and it would be highly attractive for many employees. Thus, the day this becomes main stream, the value of Bitcoin would become more eye-catching.

The below intra-day chart of Bitcoin shows that the December 22nd low remain as a major focal point and as long it this support holds, the path of least resistance remain to the upside. The price needs to break above the 50 day moving average (shown in green) to take the control from bears. As of now, bears control the balance of power.

Dollar Broadly Down As Long-Term Yields Decline, US Data In Focus

Here are the latest developments in global markets:

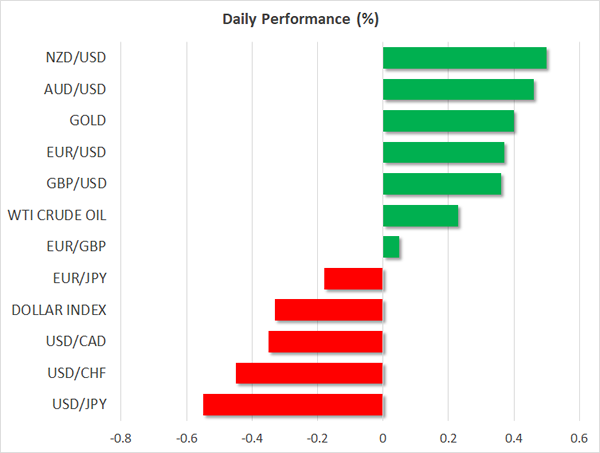

FOREX: The dollar's index against a basket of currencies headed lower, touching its lowest in nearly a month, as the greenback was hurt by falling long-term Treasury yields.

STOCKS: The Japanese Nikkei 225 lost 0.6% and Hong Kong's Hang Seng was up by 0.7%. Euro Stoxx 50 futures traded down by 0.1% at 0731 GMT, while Dow, S&P 500 and Nasdaq 100 contracts were all up by around 0.1%.

COMMODITIES: WTI and Brent crude edged higher, though their gains were limited. They both traded not far below the 2-½-year high levels tracked earlier in the week. WTI was at $59.78 per barrel and Brent at $66.62. Dollar-denominated gold continued gaining on the back of the US currency's weakness. The precious metal was up by 0.4% at $1,291.62 an ounce, trading not far below a one-month high recorded earlier in the day. Copper was posting notable gains.

Major movers: Dollar on negative footing as yields decline; rival currencies record multi-week highs versus US currency

The dollar index was 0.3% down at 92.72 after earlier touching 92.70, its lowest since December 1. Falling long-term yields were rendering the US currency less attractive relative to other currencies. Ten-year Treasury yields stood at 2.43% as European traders were beginning their trading day. This compares to last week's 2.50%, the highest level since late March.

Dollar/yen was 0.6% down at 112.71, trading at eight-day low levels. During Asian trading, Japan saw the release of data on November industrial production and retail sales, with both releases – most notably the latter – coming in above expectations.

As an additional indication of dollar weakness: euro/dollar was 0.4% up at 1.1931, trading near the day's high of 1.1936, this being the pair's highest since December 1. Pound/dollar was 0.4% up at 1.3444, not far below a two-week high recorded earlier in the day.

Commodity-linked currencies that were posting gains in previous days on the back of rising metal and oil prices, continued advancing versus the US dollar. Dollar/loonie was 0.4% down at 1.2608, just a shade above its lowest since late October hit earlier today. Aussie/dollar and kiwi/dollar were up by 0.4% and 0.5%, at 0.7802 and 0.7093 respectively, both hitting fresh multi-week highs relative to the greenback during today's trading.

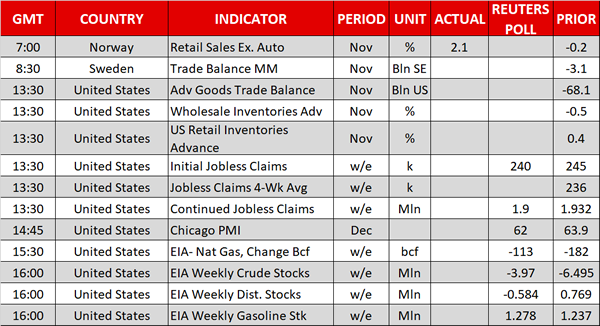

Day ahead: Dollar awaits initial jobless claims & Chicago PMI; EIA crude oil report pending

The dollar will be in the spotlight on Thursday as several economic releases out of the US have the potential to move the currency.

The first report to attract attention will be delivered at 1330 GMT and will involve initial jobless claims for the week ending December 22. The number of people applying for unemployment benefits for the first time is expected to fall by 5,000 to 240,000 in the aforementioned period, probably adding some gains to the dollar if the figure comes in lower than forecasted.

Meanwhile, preliminary readings on US wholesale and retail inventories, as well as stats on the goods trade balance for the month of November will be available along with the above labor data.

Following at 1445 GMT, the Chicago PMI which tracks business activities in the state of Chicago, is expected to retreat by 1.9 points in December to 62.0.

In energy markets, investors will be looking forward to the EIA weekly crude oil report due at 1600 GMT. After reaching the deepest fall in three months of 6.495 million barrels, forecasts are now for US crude stocks to decline by 3.970m barrels in the week ending December 22. If indeed the case, this would be the sixth consecutive week of declines and would likely push oil prices higher if crude inventories decrease more than anticipated. The report's information on gasoline and distillate stocks will also be of interest.

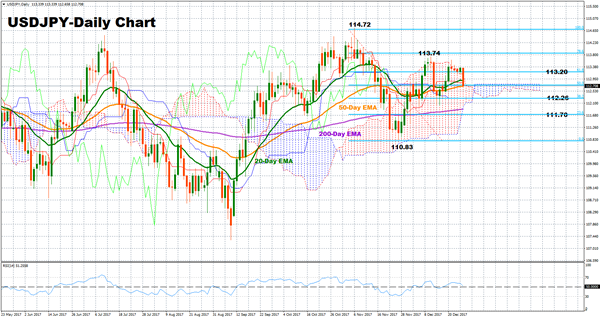

Technical analysis – USDJPY falls sharply but neutral bias still in place

USDJPY took a knock from lower US Treasury yields, diving to the 112 area and giving back earlier gains. However, the pair remains neutral in the short-term; a fall below the 38.2% Fibonacci of 112.26 of the downleg from 114.72 to 110.83 would indicate the start of bearish phase. Moreover, the RSI is currently close to its neutral level (50), suggesting that prices might move sideways in the near-term.

Below the 38.2% Fibonacci mark, additional support levels could be found at the 200-day exponential moving average at 111.90. Further downside movements from here would target the 23.6% Fibonacci at 111.70 and the swing low at 110.83.

If, on the other hand, prices head up, the 20-day EMA at 112.89 could act as resistance. Any break above of this point would shift the focus to the 61.8% Fibonacci at 113.20 and to the previous top of 113.74. The 114 key-area could also act as a barrier to upside movements.

Technical Outlook: EURUSD Surges Towards 1.20 On Fresh Dollar’s Sell-Off

The Euro surged through 1.1900 barrier in early trading of Thursday, to retest month's high at 1.1940 and open way towards key barriers at 1.1961 (27 Nov high) and psychological 1.2000 resistance.

The single currency was boosted by fresh selling of the dollar, driven by growing negative sentiment around the US currency and fresh bullish extension could accelerate further on thinning pre-holiday market.

Sustained break above 1.2000 would look for stretch towards key med-term barrier at 1.2092 (08 Sep high), the highest point of recovery rally from 1.0340 (2017 low).

Daily Tenkan-sen/Kijun-sen are forming bullish cross today, which additionally supports full bullish setup of daily chart studies.

However, consolidation before final break through 1.1961/1.2000 pivots could be expected, with initial bids at 1.1900 and broken Fibo barrier at 1.1867 expected to contain deeper dips.

Res: 1.1961, 1.2000, 1.2033, 1.2092

Sup: 1.1900, 1.1867, 1.1844, 1.1827

EURO Strongly Bullish Above 1.1910

The euro has broken above the 1.1900 level against the U.S dollar, hitting 1.1932 during early Thursday trading. The U.S dollar index has now fallen to a four-week trading low, as selling accelerated in greenback due to a dip in U.S. 10-year bond yields. The EURUSD pair now trades close to weekly price-highs, with the 1.1948 level the next major technical hurdle, ahead of the psychological 1.2000 level. With a lack of macro-economic data during the European trading session, traders with look to the key technical levels and upcoming U.S data later today.

The EURUSD remains strongly bullish while trading above the 1.1910 level, buyers may not target the 1.1948 and 1.2000 resistance levels.

Should the EURUSD pair move below the 1.1910 level, we may see a decline back towards the 1.1880 and 1.1860 support levels.

GBPUSD Further Bullish Above 1.3440 Level

The British pound has moved sharply higher overnight, reaching 1.3439 against the greenback, as the U.S dollar index moves well below the key 93.00 support level. The GBPUSD pair currently trades around the 1.3430 level, with the pair now threatening a major upside technical range break above the key 1.3440 level. With a lack of macro-economic data from the United Kingdom, sterling traders will look to Weekly Jobs, Trade Balance and PMI Manufacturing data coming from the United States economy later today.

The GBPUSD pair will turn further bullish above the 1.3440 resistance level, with buyers likely to target the 1.3500 and 1.3550 levels.

Should price-action on the GBPUSD pair fail below the 1.3440 level, sellers are likely to move price-action towards the 1.3418 and 1.3400 support levels.