Sample Category Title

USD/JPY Daily Outlook

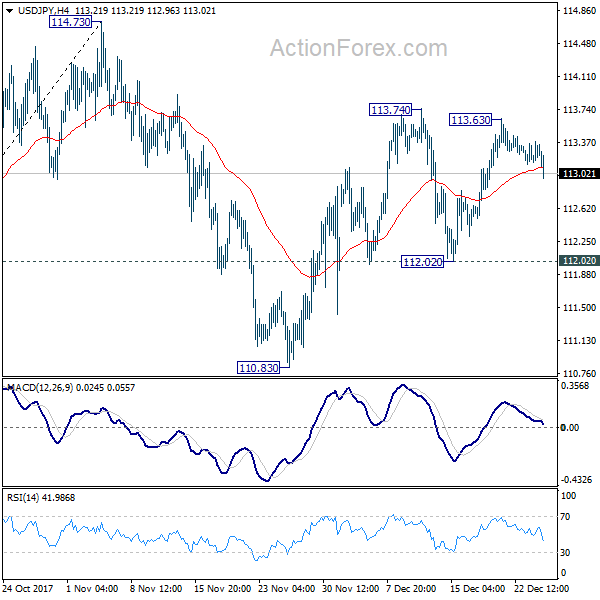

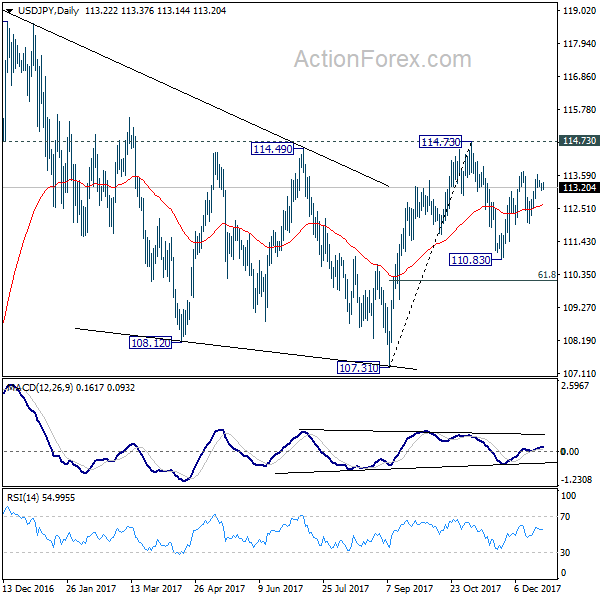

USD/JPY drops notably today but stays in range of 112.02/113.74. Intraday bias remains neutral at this point. Near term outlook remains bullish as long as 112.02 support holds. Break of 113.74 will resume the rebound from 110.83 and target 114.73 key resistance. Decisive break there will carry larger bullish implications. However, break of 112.02 will likely extend the corrective pattern from 114.73 with another leg through 110.83 support.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

USD/CHF Daily Outlook

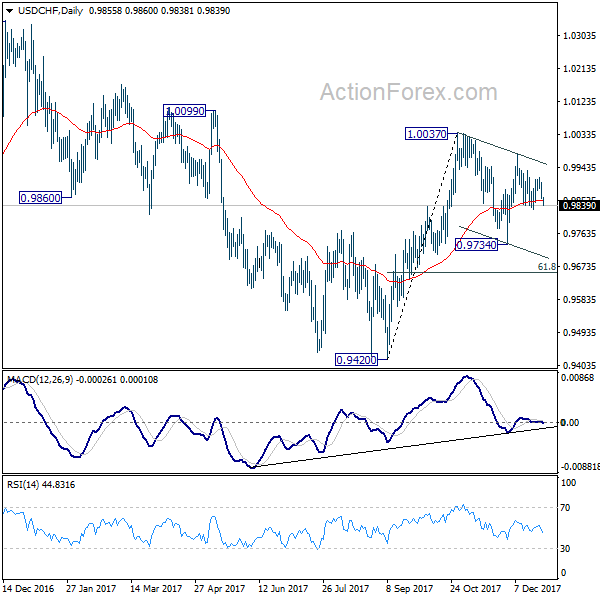

USD/CHF drops sharply today but stays above 0.9827 minor support. intraday bias remains neutral first. On the downside, below 0.9834 will probably extend the correction from 1.0037 through 0.9734. But we'd expect strong support from 61.8% retracement of 0.9420 to 0.1.0037 at 0.9656 to complete the correction from 1.0037 and bring rebound. On the upside, above 0.9977 will resume the rebound from 0.9734 for 1.0037 resistance.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

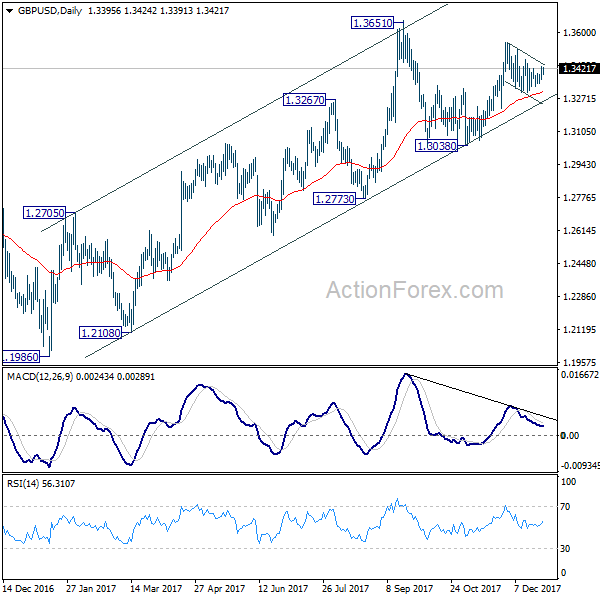

GBP/USD Daily Outlook

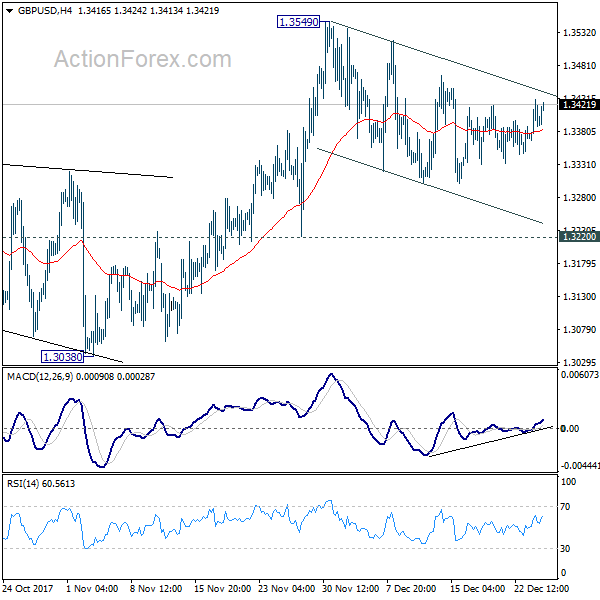

At this point, GBP/USD is still bounded in the corrective pattern from 1.3549 and intraday bias stays neutral. As long as 1.3220 support holds, we'd favor another rise. Break of 1.3549 will target 1.3651 high next. Break there will resume medium term rally from 1.1946. However, firm break of 1.3220 will turn near term outlook bearish for 1.3038 key support level.

In the bigger picture, while the medium term rebound from 1.1946 low was strong, it's limited below 1.3835 key support turned resistance. As long as 1.3835 holds, we'd view such rebound as a correction. That is, we'd expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

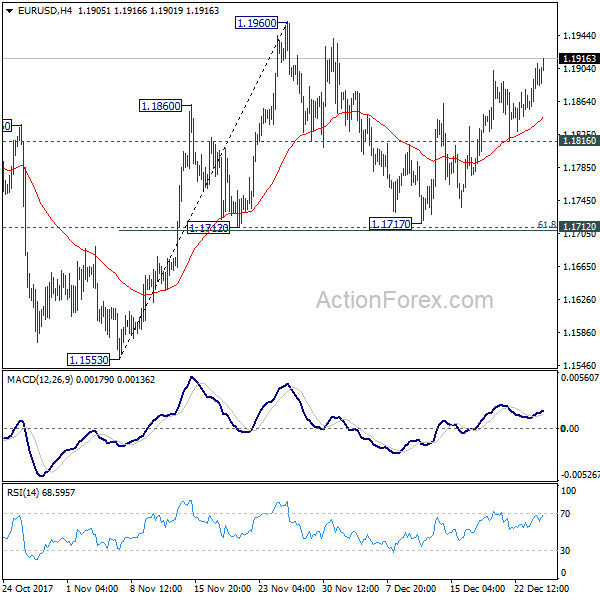

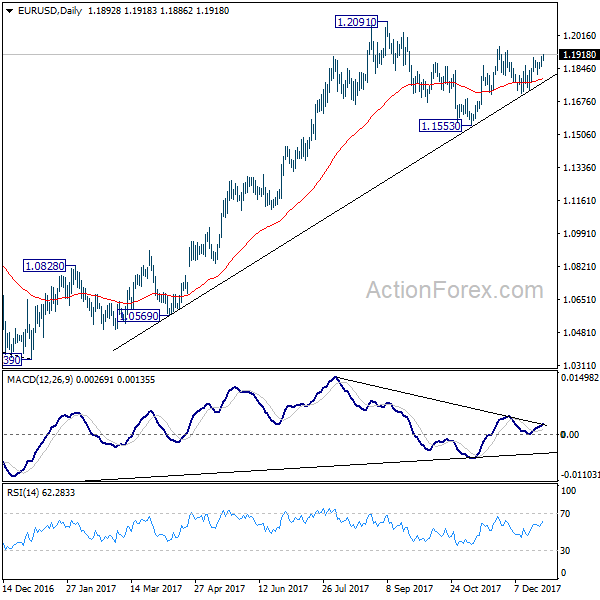

EUR/USD Daily Outlook

EUR/USD's rise continues today and reaches as high as 1.1916 so far. Intraday bias remains on the upside for 1.1960 resistance next. Break will resume whole rally from 1.1553 and target 1.2091 high. On the downside, break of 1.1816 minor support is needed to indicate completion of the rebound form 1.1717. Otherwise, near term outlook will stay cautiously bullish in case of retreat.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1435) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

Daily Report: Dollar Selloff Accelerates as Long Treasury Yields Dive

Dollar's selloff accelerates overnight on sharp selloff in treasury yields and stays weak in Asian session. 10 year yield lost -0.053 to close at 2.414, well below last week's high at 2.499. Worse than expected consumer confidence reading was seen as a factor. Conference board consumer confidence dropped to 122.1 in December versus consensus of 128.2. Year end reposition was seen as another factor in the movements in bonds. But probably, the continuous flattening of yield curve is worsening before year end as markets are not to optimistic with the Republican's tax plan.

For the momentum, near term outlook in 10 year yield is still bullish with 2.314 support intact. And rise from 2.034 is still in mild favor to extend to 2.621 resistance. But upside momentum has been clearly weak. And break of 2.314 will extend the corrective pattern from 2.621 with another decline, possibly a test on 2.034, before completion.

Summary of opinions of December BoJ meetings showed that due to improving economic outlook, there were calls for discussions on raising interest rate or cutting ETF purchases. One member noted urged the central bank to consider whether "adjustments in the level of interest rates will be necessary" if inflation and economic outlook improves further. Another board member warned of side effects of ETF purchases.

Released from Japan today, retail sales rose 2.2% yoy in November, above expectation of 1.0% yoy. Industrial production rose 0.6% mom in November, above expectation of 0.5% mom.

Looking ahead, the economic calendar is relatively light again today. ECB monthly bulletin will be a focus in European session. From US, jobless claims, trade balance, wholesale inventories and Chicago PMI will be released.

EUR/USD Daily Outlook

EUR/USD's rise continues today and reaches as high as 1.1916 so far. Intraday bias remains on the upside for 1.1960 resistance next. Break will resume whole rally from 1.1553 and target 1.2091 high. On the downside, break of 1.1816 minor support is needed to indicate completion of the rebound form 1.1717. Otherwise, near term outlook will stay cautiously bullish in case of retreat.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1435) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

EURUSD – Looks To Strengthen Further On Bull Pressure

EURUSD - The pair now looks to build up on its bull pressure following its Wednesday higher close. On the upside, resistance comes in at 1.1950 level with a cut through here opening the door for more upside towards the 1.2000 level. Further up, resistance lies at the 1.2050 level where a break will expose the 1.2100 level. Its daily RSI is bullish and pointing higher suggesting further strength. Conversely, support lies at the 1.1850 level where a violation will aim at the 1.1800 level. A break of here will aim at the 1.1750 level. Below here will open the door for more weakness towards the 1.1700. All in all, EURUSD faces further upside pressure.

Last Licks For The Dollar Bears

Last Licks for the Dollar Bears

The dollar bears are getting their last licks in for 2017 perhaps foreshadowing of things to come in 2018. The bears took their cue from The Conference Board Consumer Confidence Index which fell to its lowest level since November 2016 indicating that consumer spending may have peaked after this years blowout holiday season for shoppers. And retail sales data could struggle in the face of even the most modest of US rate hikes in 2018

The US yields continued to spill lower overnight with US 10 year yields trading towards the 2.4 percent levels as demand for year-end yield curve flatteners saw the two vs ten years basis narrow to 51 points.

However, year-end flows can be deceptive especially with asset manager rebalancing both Bond and currency exposures. And what should be the most sensitive G-10 currency to falling yields, USDJPY, barely budged overnight but USD weakness did leak into other parts of G-10 and emerging market currencies?

The US Equities

The US equity markets scratched out slight gains as tech sector winners outweighed energy losers. But with only two trading days left on the 2017 calendar, expect volumes to remain light as the New Year Party season will likely start a bit early for equity traders and rightly so after a stellar year for US stocks.

Energy Prices

There has been a pause in WTI recent run higher. But given the much stronger price response to supply disruptions in the wake of OPEC supply cuts, the market is poised to make further gains, likely held back by holiday inspired profit taking. Indeed, the markets will continue to drift towards bullish headlines, and with geopolitical risk no less sure ahead of Libyan elections next year we should expect more regional chaos and disorder to underpin OIL prices.

The Australian Dollar

Higher commodity prices and lower US yields have the Australian dollar within grasp of reclaiming the .78 level.

The supply squeeze on copper and oil are lending support to the commodity block of currencies.

The Malaysian Ringgit

Holiday thinned trading conditions continue to weigh on sentiment, however, lower US yields and higher energy prices should play out well for the MYR in early 2018.

Gold Climbs To 4-Week High, US Data A Mixed Bag

Gold continues to move higher during Christmas week, and has climbed to its highest level since December 1. In North American trade, the spot price for an ounce of gold is $1286.97, up 0.33% on the day. There were two key events on Wednesday. CB Consumer Confidence slowed to 122.2, well off the estimate of 128.2 points. Pending Home Sales posted a small gain of 0.2%, beating the estimate of -0.4%.

US housing numbers continue to beat expectations, as Pending Home Sales surprised the markets with a gain of 0.2%. Last week, Housing Starts came in at 1.30 million, beating the forecast of 1.25 million. On Tuesday, New Home Sales sparkled, with a gain of 733 thousand. This easily beat the estimate of 654 thousand, and was the highest reading since September 2007. On Thursday, the US releases unemployment claims, which is expected to drop to 241 thousand.

With the US economy posting growth above 3% for another quarter, the Federal Reserve remains on track for another rate hike in January. The CME Group has pegged the odds of a January hike at 100%, which could give a boost to the US dollar. If the economy continues its impressive pace of growth above 3%, the Fed could raise rates up to four times in 2018. Despite strong economic conditions, the Federal Reserve’s inflation target of 2.0% remains elusive. Fed Chair Janet Yellen and other FOMC members have said that they expect that the strong labor market will lead to higher inflation. Although this is yet to materialize, of significance to the markets is the commitment of the Fed to press ahead with rate hikes despite low inflation.

British Pound Remains Subdued

The British pound continues to have a quiet week and is showing little movement in the Wednesday session. In North American trade, GBP/USD is trading at 1.3394, up 0.15% since the Friday close. On the release front, there are no British events on the schedule.

In the U.S, the first key indicators of the week were mixed. CB Consumer Confidence slowed to 122.2, well off the estimate of 128.2 points. Pending Home Sales posted a small gain of 0.2%, beating the estimate of -0.4%. Housing numbers continue to beat expectations. Last week, Housing Starts came in at 1.30 million, beating the forecast of 1.25 million. On Tuesday, New Home Sales sparkled, with a gain of 733 thousand. This easily beat the estimate of 654 thousand, and was the highest reading since September 2007. On Thursday, the US releases unemployment claims, which is expected to drop to 241 thousand.

The Brexit negotiations are finally shifting to trade, much to the relief of an embattled Prime Minister May, who has faced harsh criticism over her handling of the talks with the Europeans. Still, May has her work cut out for her, with little more than a year until Britain leaves the European Union. Her cabinet remains split on what a Brexit deal will look like, and the Europeans are in no mood to do Britain any favors, in order not to give other EU members any ideas about jumping ship. What will a trade relationship between Britain and the European Union look like? That remains unclear, but it's no secret that the two sides have very different views of a future trade agreement. There was a taste of this last week regarding financial services. The EU senior negotiator, Michel Barnier, said Britain's financial services would not be included in a Brexit deal, as no free trade agreements have included financial services. BoE Governor Mark Carney took issue with Barnier, arguing that there was no reason why the UK and the EU couldn't maintain some type of free trade in financial services. Clearly, the sides remain far apart on the “end phase” of what a Brexit agreement will look like, and both Britain and the EU will have to show some flexibility in order to hammer out an agreement. Given the lack of trust between the sides, the talks will likely hit plenty of snags, and this could weigh on the British pound in the coming months.

Japanese Yen Ticks Lower, US Data Mixed

USD/JPY has shown little movement since late last week, and this trend has continued in the Wednesday session. In North American trade, USD/JPY is trading at 113.31, up 0.06%. On the release front, Japanese Housing Starts declined 0.4%, a much better reading than the forecast of -2.5%. Later in the day, Japan releases manufacturing and consumer spending reports. Preliminary Industrial Production is forecast to remain unchanged at 0.5%, while Retail Sales is expected to rebound with a strong gain of 1.1%.

In the U.S, key indicators were mixed on Wednesday. CB Consumer Confidence slowed to 122.2, well off the estimate of 128.2 points. Pending Home Sales posted a small gain of 0.2%, beating the estimate of -0.4%. Housing numbers continue to beat expectations. Last week, Housing Starts came in at 1.30 million, beating the forecast of 1.25 million. On Tuesday, New Home Sales sparkled, with a gain of 733 thousand. This easily beat the estimate of 654 thousand, and was the highest reading since September 2007. On Thursday, the US releases unemployment claims, which is expected to drop to 241 thousand.

Japan released consumer spending and inflation numbers on Monday, and the readings were strong. Tokyo Core CPI, the primary gauge of consumer inflation, climbed 0.9%, in December its strongest gain since March 2015. This edged above the forecast of 0.8%. National Core CPI improved to 0.9%, just above the estimate of 0.8%. There was more positive news as Household Spending rebounded with an excellent gain of 1.7%, crushing the estimate of 0.6%. This reading marked a 5-month high. Next up is another inflation indicator, BoJ Core Inflation. The Bank of Japan maintained monetary policy last week and the minutes of the October meeting indicated that most members favored a continuation of the current ultra-accommodative policy. This could weigh on the yen, as other central banks, such as the ECB, the Federal Reserve and the Bank of Canada have tightened policy in recent months, widening divergence with the Bank of Japan.