Sample Category Title

Daily Wave Analysis: GBP/USD Bullish Breakout Above Triangle Pattern

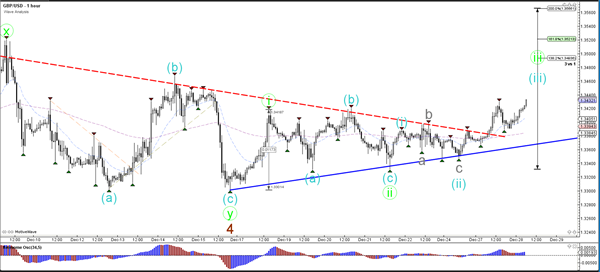

Currency pair GBP/USD

The GBP/USD broke the resistance (dotted red) of triangle chart pattern, which could be a bullish breakout within a wave 5 (brown) of wave C (green). The bullish break could see price move towards the Fibonacci targets of waves 5.

The GBP/USD has completed an ABC (blue) correction within a wave 2 (green/blue). The wave 3 becomes more likely if price manages to reach the 161.8% Fibonacci level.

Currency pair EUR/USD

The EUR/USD broke above the local resistance trend line (dotted orange) and is moving higher towards the strong resistance zone (red lines). The chart is also building a rising wedge chart pattern (red/blue lines). A bullish breakout could indicate a continuation of the uptrend whereas a bearish reversal could send the EUR/USD lower to test the wave 2 vs 1 (pink) and the Fib levels of wave Y (purple).

The EUR/USD is testing the Fibonacci levels of wave Y (orange) and the resistance trend line (red) of the rising wedge pattern.

Currency pair USD/JPY

The USD/JPY broke below the support trend line (dotted blue) which could indicate a larger bearish wave C (purple) correction within wave 2 or B (light purple).

The USD/JPY bearish breakout could see price retest the support levels around 112.

Elliott Wave View: Nasdaq Looking To Extend Higher

Nasdaq Short Term Elliott Wave view suggests that Intermediate wave (4) ended at 6232.3. Since then, Nasdaq has resumed the rally higher as a double three Elliott Wave structure. The subdivision of the first leg Intermediate wave W unfolded as a double three Elliott Wave structure where Minute wave ((w)) ended at 6427.75, Minute wave ((x)) ended at 6383, and Minute wave ((y)) of W ended at 6545.75.

Down from there, Minor wave X is proposed complete at 6432.25 in the green box. Subdivision of Minor wave X unfolded as a double three Elliott Wave structure where Minute wave ((w)) ended at 6463.25, Minute wave ((x)) ended at 6520.75, and Minute wave ((y)) of X ended at 6432.25. Near term, while dips stay above 6432.25, but more importantly as far as pivot at 12/5 low (6232.3) stays intact, expect Index to extend higher. We don’t like selling the Index.

Unless already long in a risk free trade from the green box area, we prefer to wait for the Index to break above Minor wave W at 6545.75 before buying the dips again. At this stage, until the Index breaks above Minor wave W at 6545.75, a double correction in Minor wave X still can’t be ruled out. If the Index breaks below 12/26 low (6432.25) from here, then it could open extension lower to 6234 – 6361 area next to end Minor wave X before buyers appear for at least 3 waves bounce.

Nasdaq 1 Hour Elliott Wave Chart

Market Update – Asian Session: USD Weaker Against Majors

Headlines/Economic Data

General Trend: Asian markets trade generally higher, despite mixed US equities session on Wednesday

US dollar generally weaker amid gains in Commodity and Asian currencies

Japan

Nikkei 225 opened -0.1%; closed -0.6%

TOPIX Iron/Steel Index +0.6%

Weakness in the financial sector: Mitsubishi UFJ -1.2%

Nintendo -0.5%: To delay rollout of larger Switch game cards until 2019 on technical issues , according to US financial press report

Nintendo: Said to target FY18 Switch sales of more than 20M units, said a Japanese press report [**Note: On Oct 30th, the company guided its current FY18 Switch unit sales at 14M (up from the prior forecast of 10M)]

Japan Nov Department Store Supermarket Sales y/y: 1.4% v 1.0%e

Japan Nov Retail Sales m/m: 1.9% v 0.7%e; Retail Trade y/y: 2.2% v 1.0%e

JAPAN NOV PRELIM INDUSTRIAL PRODUCTION M/M: 0.6% V 0.5%E; Y/Y: 3.7% V 3.6%E; Manufacturers see Dec production +3.4% m/m, Jan production

4.5% m/m; government raises assessment of industrial production

Japan Trade Ministry: The rise in industrial production was due to increased output of memory chips, semiconductor equipment and heavy machinery used for construction

BoJ releases summary of opinions of Dec meeting: When it is expected that economic activity and prices will continue to improve going forward, the situation may occur where the Bank will need to consider whether adjustments in the level of interest rates will be necessary

Japan Nov Vehicle Production y/y: 0.9% v 6.4% prior

Korea

Kospi opened +0.1%

Chipmakers add to gains seen on Wednesday’s session: Samsung +1.8%, Hynix +1%

Hyundai Motor -2.5%: South Korea Ministry of Land, Infrastructure and Transport orders the co and several foreign automakers to recall ~1M vehicles due to faulty parts - Korean press

Posco Steel -1.4% (tracked declines in US steelmakers)

Korean Won (KRW) +0.2% (continues to trade at more than 2-year highs; gaining for 4th straight session)

SOUTH KOREA JAN BUSINESS MANUFACTURING SURVEY: 82 V 82 PRIOR; NON-MANUFACTURING SURVEY: 78 V 80 PRIOR

South Korea Nov Cyclical Leading Index Change: -0.1 v -0.3 prior

South Korea Nov Industrial Production m/m: 0.2% v 1.3%e; y/y: -1.6% v 0.0%e; Revises Oct figures lower

South Korea Nov Retail Sales m/m: 5.6% v 1.3%e; y/y: 6.5% v 2.5%e

South Korea and the US to hold Free Trade Agreement (FTA) talks in Washington, D.C. on Jan 5th

Bank of Korea (BoK) annual monetary strategy for 2018: 2018 monetary policy to remain accommodative

South Korea and the US to hold first talks to amend Free Trade Agreement (FTA) in Washington, D.C. on Jan 5th

(KR) South Korea Financial Regulator (FSC) Vice Chairman: To make guidelines to prevent money laundering via cryptocurrency

Looking ahead: South Korea Dec CPI due for release on Friday

China/Hong Kong

Shanghai Composite opened -0.1%, Hang Seng +0.3%

Hang Seng Industrial Goods Index +1.2%, Information Tech +1%, Materials +1%, Financials +0.6%

Hang Seng Property Index +1%: China govt may keep tight control of the property market; Outbound investment to be more prudent - Chinese press

Shanghai Composite Consume Staples Index +1.5%: Liquor producer Kweichow Moutai +4.5% (guided FY17 profits +58% y/y, plans to raise prices by 18% on avg in 2018)

Geely +3.5% (announced agreement to become largest shareholder of Sweden’s Volvo AB)

Guangzhou Automobile Group: +2% (announced agreement to partner with EV maker NIO)

Herbal products company BaWang International Group +26% (declined ~31% on Wednesday): Said former CEO Wan is seeking to wind up Fortune Station and it sees no material impact to business

(CN) China 19th Central Committee to discuss changes to the constitution in January, sparking chatter Xi could have an extended term as President – Xinhua

(CN) Trump administration plans to unveil a series of trade penalties against China early next year in a move that some describe as “shock and awe” - financial press

(CN) Analysts expect China IPOs will increase in 2018 from MSCI’s decision to include A-shares in its indexes from June, a move expected to see a range of investors buy A-shares selected for inclusion

(CN) China Nov Swift Global Payments CNY: 1.75% v 1.46% prior

(CN) PBoC: Skips OMO operation for 5th straight session; Net drain CNY30B v CNY40B drain prior

USD/CNY (CN) China PBoC sets yuan reference rate at 6.5412 v 6.5421 prior

(CN) China to raise price of gasoline and diesel by CNY70/ton, effective Dec 29th

Australia/New Zealand

ASX 200 opened flat; closed +0.3%

ASX 200 Financials Index +0.2%; REIT -1.2%, Utilities -0.7%

DNA.AU Wins Injunction to close Star Paradise; +8%

Looking ahead: Australia Nov Housing and Private Sector Credit data due for release on Friday

Other Asia

(IN) India 10-year bond yield rises over 8 bps after government confirmed there might be additional borrowing in FY17/18

(TW) Taiwan’s Taiex gains as Apple suppliers rebound from losses seen earlier in week: Largan Precision +5.5%

(TW) Taiwan Dollar (TWD) hits more than 3-year high

Taiwan’s MediaTek: Sees 2018 to have a stable mobile phone market - Taiwan press

(TH) Thailand Nov Manufacturing Production Index ISIC NSA y/y: 4.2% v 1.8%e; Capacity Utilization: 64.16 v 60.45 prior

(TH) Thailand Nov Unemployment Rate: 1.1% v 1.3% prior

(SL) Sri Lanka Central Bank (CBSL) leaves Key Rates unchanged (as expected)

North America

US equity markets ended mixed: Dow +0.1%, S&P500 +0.1%, Nasdaq 0.0%, Russell 2000 0.0%

S&P 500 Utilities sector +0.4%; Energy -0.4%

(US) Fed's Rosengren (hawk, non-voter in 2018): has concerns we may start to see a reach for yield

(US) White House said to consider Richard Clarida, Lawrence Lindsey for Fed Vice Chairman position; Former Pimco exec Mohamed El-Erian also in consideration - financial press

(US) TREASURY'S $34B 5-YEAR NOTE AUCTION DRAWS: 2.245%; BID-TO-COVER RATIO: 2.36 V 2.46 PRIOR AND 2.47 OVER THE LAST 12 AUCTIONS (highest yield since Apr 2010)

(US) Weekly API Oil Inventories: Crude: -6M v -5.2M prior

Looking Ahead: US Dec Chicago PMI data and weekly DOE Crude Inventories due for release on Thursday

Europe

(UK) EU officials indicate that UK Brexit minister may have been "sidelined"; EU negotiator Barnier has been dealing directly with another UK official - The Times

(BE) National Bank of Belgium maintains countercyclical capital buffer percentage at zero for Q1'18

(FR) FRANCE NOV NET CHANGE IN JOBSEEKERS: -29.5K V +8.0K PRIOR

M&A: Accor Hotels [AC.FR]: Reportedly in discussions with investors on potential AccorInvest stake sale - press

Levels as of 01:00ET

Nikkei225 -0.6%, Hang Seng +0.7%; Shanghai Composite +0.7%; ASX200 +0.3%, Kospi +0.9%

Equity Futures: S&P500 +0.0%; Nasdaq100 +0.1%, Dax +0.0%; FTSE100 +0.2%

EUR 1.1929-1.1886; JPY 113.35-112.88; AUD 0.7796-0.7765;NZD 0.7089-0.7054

Feb Gold +0.3% at $1,294/oz; Feb Crude Oil +0.2% at $59.77/brl; Mar Copper +0.4% at $3.29/lb

GBP/JPY Daily Outlook

No change in GBP/JPY's outlook. With 150.36 minor support intact, further rise is in favor. Above 152.07 will target 153.39 first. Break will resume medium term rally. On the downside, below 150.36 minor support will turn bias back to the downside and extend the correction from 153.39. But we'd look for strong support from 146.96 to bring rebound.

In the bigger picture, outlook is mixed up a bit with last week's sharp decline. But still, as long as 146.96 key support holds, medium term outlook remains bullish. Rise from 122.36 is in favor to extend to 61.8% retracement of 195.86 to 122.36 at 167.78. However, break of 146.96 support will indicate trend reversal. And the corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.

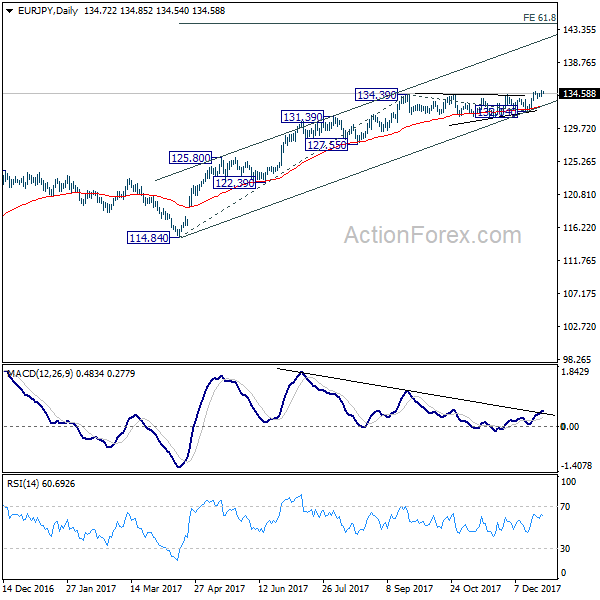

EUR/JPY Daily Outlook

EUR/JPY breached 134.87 to 134.97 but quickly retreated. Upside momentum is also weak as seen in 4 hour MACD. Intraday bias stays neutral first. Overall, near term outlook stays bullish as long as 132.04 support holds. Above 134.97 will resume medium term rally and target 61.8% projection of 114.84 to 134.39 from 132.04 at 144.12.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). Sustained break of 61.8% retracement of 149.76 to 109.03 at 134.20 will pave the way to key long term resistance zone at 141.04/149.76. However, break of 132.04 support will suggest medium term topping and will turn outlook bearish for deeper fall back 55 week EMA (now at 127.82).

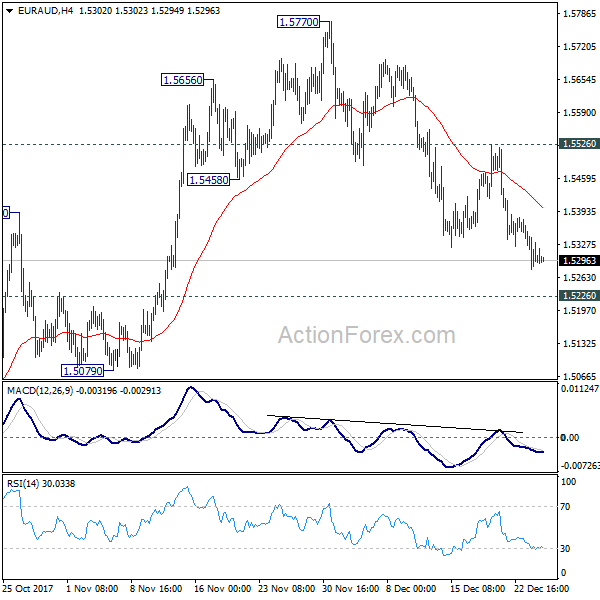

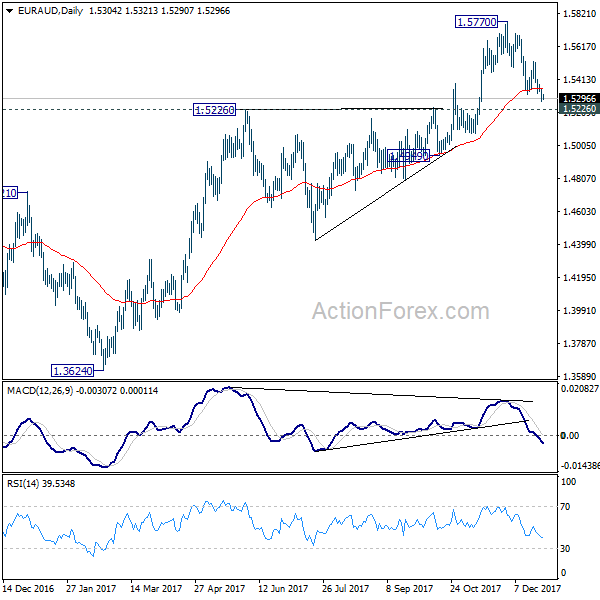

EUR/AUD Daily Outlook

The correction from 1.5770 is still extend and deeper fall could be seen in EUR/AUD. But still, outlook will remain bullish as long as 1.5226 resistance turned support holds. Above 1.5526 minor resistance will turn bias back to the upside for retesting 1.5770 resistance. However, sustained break of 1.5226 will indicate larger reversal and target 1.4949 support next.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top (2015 high) has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. We'll hold on to this bullish view as long as 1.5226 resistance turned support holds. Firm break of 1.6587 will resume long term rise from 1.1602 (2012 low). However, sustained break of 1.5226 will indicate trend reversal and target 1.3624 again.

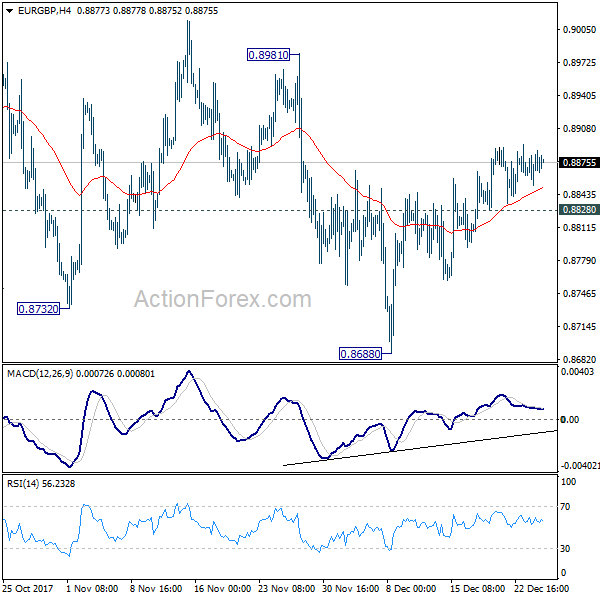

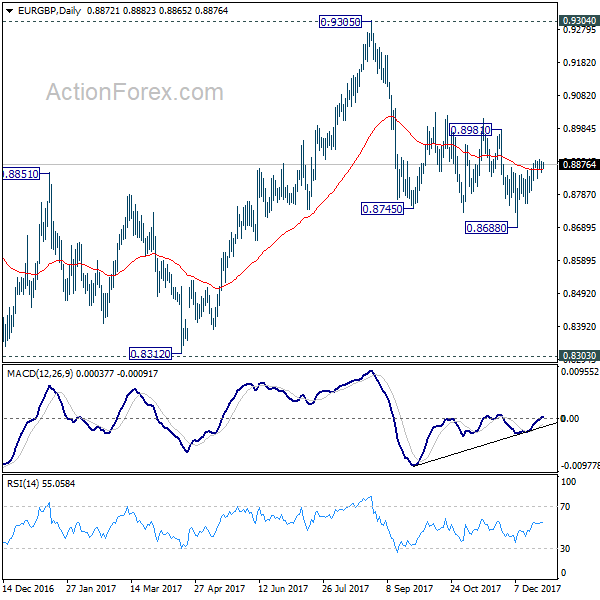

EUR/GBP Daily Outlook

No change in EUR/GBP's outlook even though upside momentum is weak. With 0.8828 minor support intact, further rise is mildly in favor for 0.8981 resistance. Sustained break there will indicate that whole decline from 0.9305 has completed. In such case, EUR/GBP will target a test on 0.9304/5 key resistance. On the downside, below 0.8828 minor support will turn bias back to the downside for 0.8668 instead.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

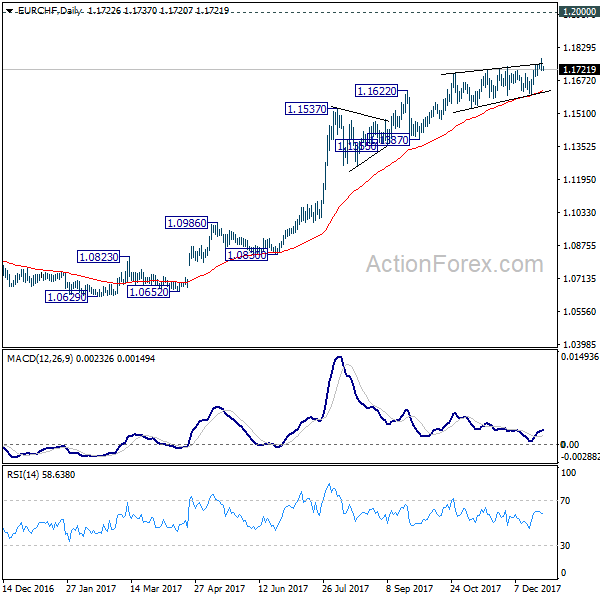

EUR/CHF Daily Outlook

Intraday bias in EUR/CHF is turned neutral again with 4 hours MACD crossed below signal line. We'd maintain that it's close to topping. And in case of another rise, strong resistance should be seen well below 1.2 handle to bring medium term reversal. On the downside, break of 1.1602 support will indicate reversal and turn outlook bearish for 1.1387 and below.

In the bigger picture, while a medium term top could be around the corner, there is no change in the larger outlook. That is, long term rise from SNB spike low back in 2015 is still in progress and would extend. As long as 1.1198 resistance turned support holds, we'll hold on to this bullish view and expect another to prior SNB imposed floor at 1.2000. Though, we'll reassess the outlook if 1.1198 is firmly taken out.

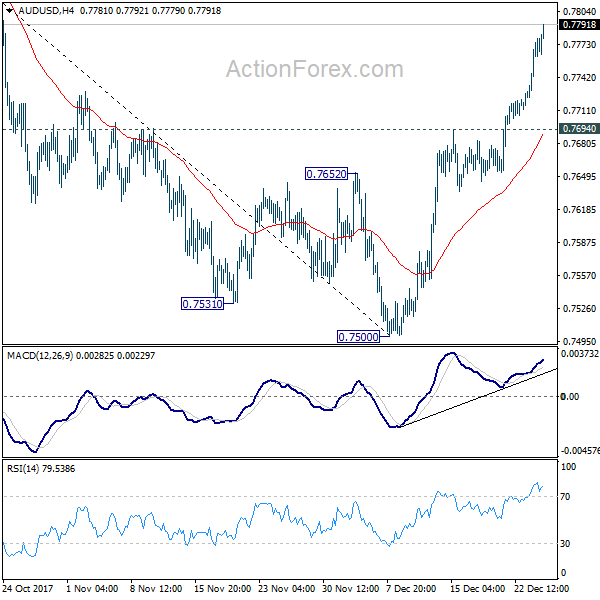

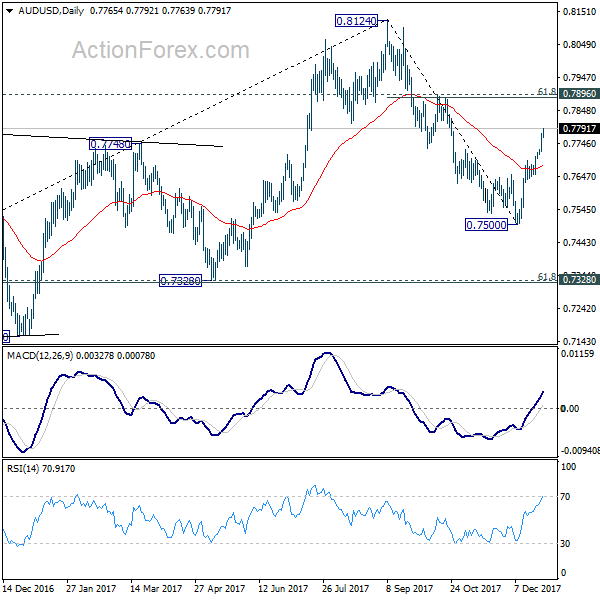

AUD/USD Daily Outlook

Intraday bias in AUD/USD remains on the upside as rebound from 0.7775 extends higher. Further rise would be seen to 0.7896 cluster resistance (61.8% retracement of 0.8124 to 0.7500 at 0.7886). On the downside, break of 0.7694 support is needed to indicate completion of the rebound. Otherwise, further rally will remain in favor in case of retreat.

In the bigger picture, we're still slightly favoring the case that corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8034). But stronger than expected rebound from 0.7500 is dampening this bearish view. On the downside, break of 0.7500 will target 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) to confirm this bearish case. But break of 0.8124 will extend the rise from 0.6826 to 38.2% retracement of 1.1079 (2011 high) to 0.6826 (2016 low) at 0.8451 before completion.

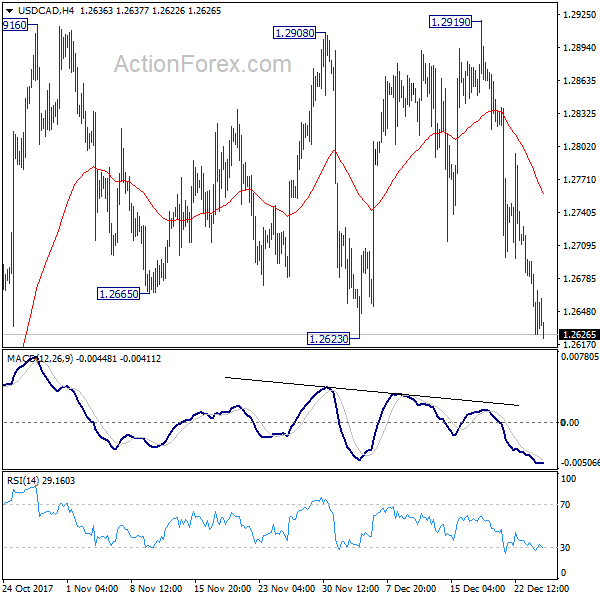

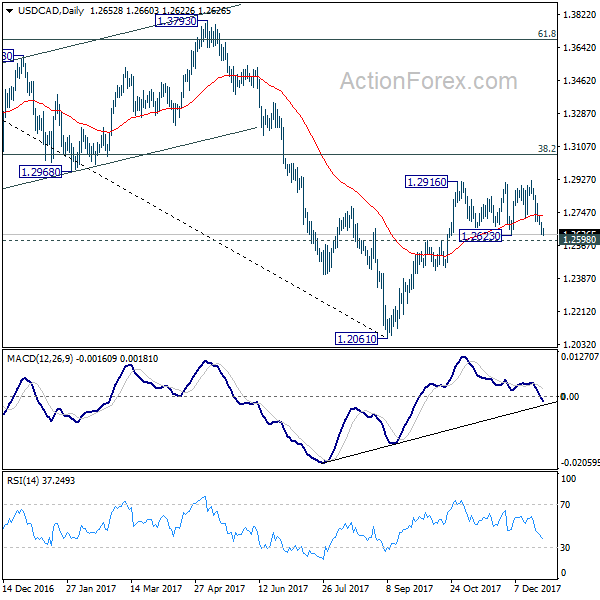

USD/CAD Daily Outlook

USD/CAD drops further today but it's staying in consolidation pattern from 1.2916. Intraday bias stays neutral at this point. As long as as long as 1.2598 resistance turned support holds, near term outlook remains bullish. On the upside, firm break of 1.2916 will resume the rise from 1.2061 and target 1.3065 medium term fibonacci level next. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2879). Near term outlook will be turned bearish in this case and deeper fall would be seen through 1.2450 support.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds. Break of 1.2450 will, however, suggests that rebound from 1.2061 has completed and bring retest of this low.