Sample Category Title

DAX Remains Subdued in Thin Trading

The DAX is showing little movement in the shortened trading week. Currently, the index is at 13,057.07, down 0.14% on the day. The sole event is the ECB Economic Bulletin, which comes two weeks after the December ECB policy meeting. On Friday, Germany releases Final CPI.

Christmas week is light on eurozone economic releases, so the markets will be paying close attention to German Preliminary CPI, which will be released on Friday. The indicator rose 0.3% in November, marking a 4-month gain. The markets are expecting a gain of 0.5% for December. In the eurozone, annual average inflation inched up to 1.5% in November, up from 1.4% in October. This marked a multi-year high. Earlier this month, in a nod to stronger economic activity in 2017, the ECB raised its forecasts for growth and inflation for the eurozone from this year through to 2019. Still, inflation remains well below the ECB target of around 2.0%, and ECB policymakers are unlikely to announce an end to their stimulus package until inflation moves closer to the 2.0% target.

Stronger economic conditions in Germany and the eurozone economy have boosted European stock markets in 2017, and the DAX has responded with strong annual gains of 13.8%. So far, fourth quarter numbers in Germany and the eurozone have been solid, and expectations are that the positive trend will continue into 2018, which bodes well for the DAX.

With the US economy expanding above 3% in the third quarter, the Federal Reserve remains on track for another rate hike in January. The CME Group has pegged the odds of a January hike at 100%, which could give a boost to the US dollar. If the economy continues its impressive pace of growth above 3%, the Fed could raise rates up to four times in 2018. Despite strong economic conditions, the Federal Reserve's inflation target of 2.0% remains elusive. Fed Chair Janet Yellen and other FOMC members have said that they expect that the strong labor market will lead to higher inflation. Although this is yet to materialize, of significance to the markets is the commitment of the Fed to press ahead with rate hikes despite low inflation.

EUR/USD Mid-Day Outlook

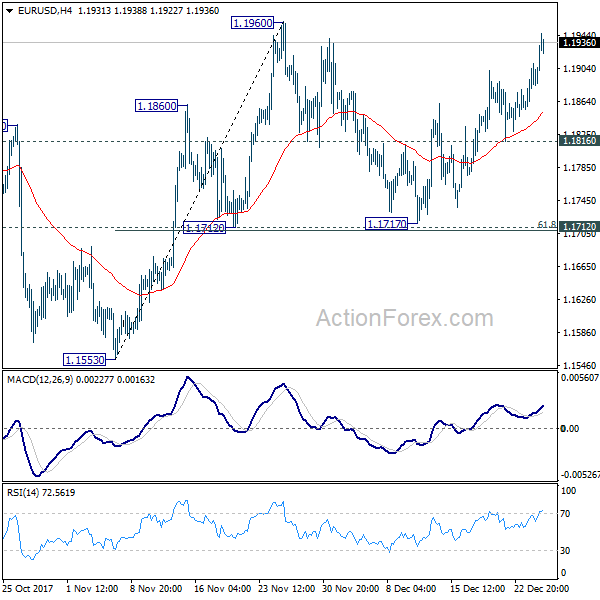

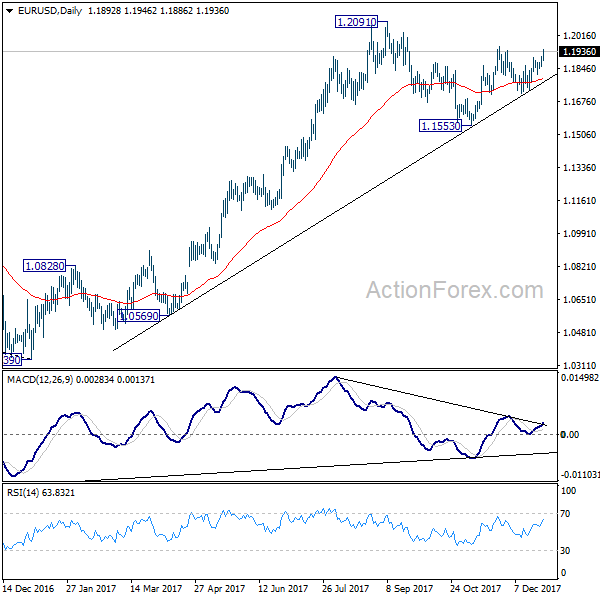

Intraday bias in EUR/USD remains on the upside for 1.1960 resistance. Break will resume whole rally from 1.1553 and target 1.2091 high. On the downside, break of 1.1816 minor support is needed to indicate completion of the rebound form 1.1717. Otherwise, near term outlook will stay cautiously bullish in case of retreat.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1435) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3350; (P) 1.3370; (R1) 1.3392; More.....

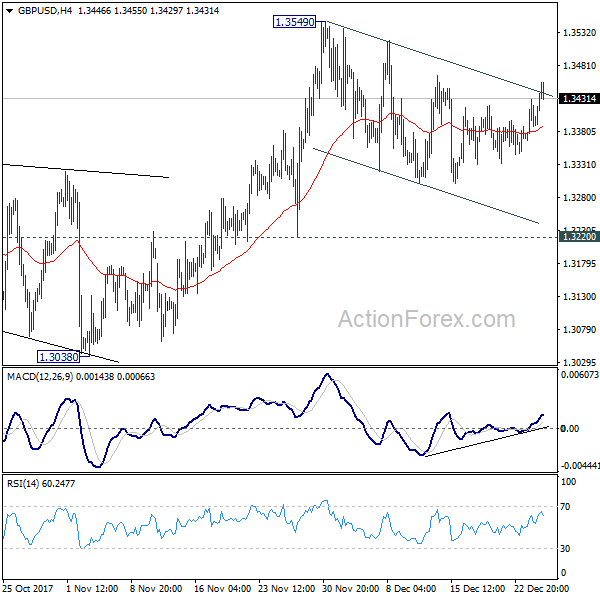

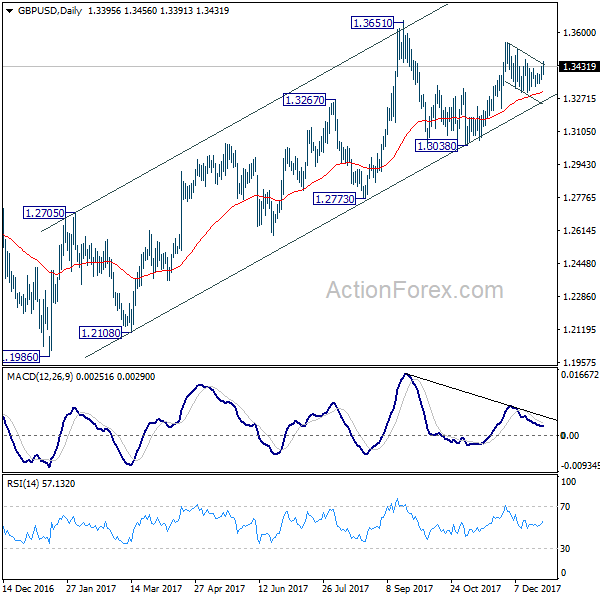

At this point, GBP/USD is still bounded in the corrective pattern from 1.3549 and intraday bias stays neutral. As long as 1.3220 support holds, we'd favor another rise. Break of 1.3549 will target 1.3651 high next. Break there will resume medium term rally from 1.1946. However, firm break of 1.3220 will turn near term outlook bearish for 1.3038 key support level.

In the bigger picture, while the medium term rebound from 1.1946 low was strong, it's limited below 1.3835 key support turned resistance. As long as 1.3835 holds, we'd view such rebound as a correction. That is, we'd expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

USD/CHF Mid-Day Outlook

Break of 0.9827 indicates USD/CHF's fall from 0.9977 has resumed. Intraday bias is back on the downside for 0.9734 and below. Price actions from 1.0037 are viewed as a correction pattern. Hence, we'd we'd expect strong support from 61.8% retracement of 0.9420 to 0.1.0037 at 0.9656 to contain downside and bring rebound. On the upside, above 0.9915 resistance will turn bias to the upside for 0.9977 resistance and above instead.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

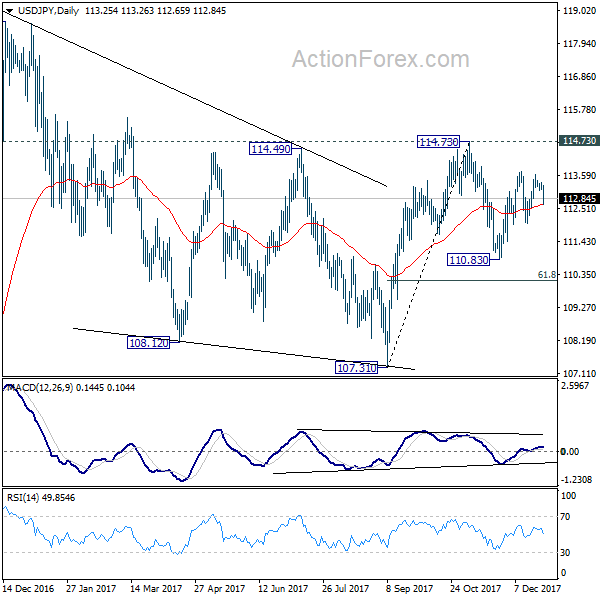

USD/JPY Mid-Day Outlook

USD/JPY dips to as low as 112.65 so far today. But it's staying in range of 112.02/113.74. Intraday bias remains neutral for the moment. Also, near term outlook stays bullish as long as 112.02 support holds. Break of 113.74 will resume the rebound from 110.83 and target 114.73 key resistance. Decisive break there will carry larger bullish implications. However, break of 112.02 will likely extend the corrective pattern from 114.73 with another leg through 110.83 support.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

Dollar Broadly Under Pressure ahead of Jobless Claims Numbers

Here are the latest developments in global markets:

FOREX: The US currency remained broadly weaker versus other major currencies in thin trading ahead of New Year celebrations. Commodity currencies maintained their positive momentum as oil and other metals remained on the rise.

STOCKS: Major European blue-chip indices were not much changed around midday. The pan-European Stoxx 600 was roughly flat, with basic materials outperforming on the back of rising commodity prices and technology once again coming under pressure; tech stocks were the worst performers within the Stoxx 600. The blue-chip Euro Stoxx 50 was down by 0.2%. Meanwhile, the UK's FTSE 100 was 0.1% up and not far below yesterday's all-time high, while the German DAX was down by 0.2% and the French CAC 40 traded lower by 0.05%. Dow, S&P 500 and Nasdaq 100 futures traded up by 0.15%, 0.1% and 0.2% respectively.

COMMODITIES: Ahead of the EIA weekly report, WTI and Brent crude were up by 0.2% and less than 0.1%, at $59.71 and $66.47 a barrel respectively. They both traded close to2-½-year high levels reached earlier in the week. Gold was 0.4% up at $1,291.83 per ounce after rising to as high as $1,293.25, this being a one-month high for the precious metal which has been benefitting on dollar weakness. Copper futures rose to touch their highest since early 2014.

Day ahead: Weak dollar as markets await weekly jobless claims and crude oil figures

The dollar index, which gauges the greenback against the currencies of six major US trading partners, was 0.3% lower at 92.72. Earlier in the day in hit 92.64, its lowest since December 1.

Ten-year Treasury yields have recovered somewhat during today's trading after falling sharply in the two days that preceded, though they still stand at a distance to last week's nine-month high of 2.5040%. They were last at 2.4341%. The decline in long-term yields is rendering the US currency less attractive relative to counterparts, while it was not associated with a fall in short-term yields, leading to yield curve flattening and once again fueling the debate on what that could mean for the economy further ahead. Dollar/yen was 0.4% down at 112.83 after falling to a nine-day low of 112.65 earlier in the day.

Euro/dollar and pound/dollar traded higher by 0.4% and 0.3% respectively. The former recorded a one-month high of 1.1946 earlier in the day, while coming within breathing distance of late November's three-month high of 1.1960. Pound/dollar recorded a two-week high of 1.3456.

The Swiss franc was another notable gainer versus the dollar. Dollar/franc was 0.6% down, trading not far above the more than more than three-week low of 0.9795 tracked earlier in the day.

The rally in metals kept supporting the aussie, while the kiwi rose in sympathy as well. Aussie/dollar and kiwi/dollar were up by 0.2% and 0.35% respectively. Both pairs recorded two-month highs earlier in the day, with aussie/dollar touching 0.7809 and kiwi/dollar hitting 0.7098.

Higher oil prices as well as rising expectations for another interest rate hike to be delivered by the Bank of Canada when it completes its meeting on monetary policy on January 17 have been supporting the Canadian dollar. Dollar/loonie was 0.4% down, trading close to 1.2601, this being its lowest since October 20 recorded earlier in the day.

In terms of the day's most important releases, US initial and continued jobless claims for the week ending December 22 will be made public at 1330 GMT, with the release having the capacity to spur positioning on the dollar. December's Chicago PMI – this being a composite measure that gauges both manufacturing and non-manufacturing activity in the area of Chicago – due at 1445 GMT might also attract some interest. The reading is expected to decline for the second straight month, though still comfortably stand above 50, this being the level that separates expansion from contraction.

Oil traders will be paying attention to the EIA report that, among others, will include information on US crude stocks for the week ending December 22. Crude inventories are forecasted to decline by around 4 million barrels, reflecting their sixth consecutive weekly decline. The release tends to generate volatility in oil prices.

Technical Outlook: WTI Oil Consolidates Under $60 Barrier, Bullish Sentiment Supportive For Further Advance

WTI oil maintains firm tone and holding within narrow consolidation under psychological $60 barrier (fresh highs in 2 1/2 years) which was dented on strong bullish acceleration on Tuesday. Oil price was boosted by stronger than expected draw in crude stocks after API report on Wednesday shows fall in US oil inventories by 6 million barrels, compared to forecasted 3.8 million barrels draw. Markets eye today's release of EIA weekly crude inventories report which could further inflate oil prices on release above forecasted 3.9 million barrels draw. Oil price maintains firm bullish sentiment on ongoing OPEC-led production cut which was extended until the end of 2018 and could boost oil prices. Bulls eye next strong barrier and target at $61.71 (13 May 2015 lower top) to generate fresh bullish signal on firm break. Meanwhile, near-term price action may remain in extended consolidation with stronger downticks not ruled out, as slow stochastic is in deep overbought territory on daily chart. Rising 10SMA ($58.31) is expected to ideally contain extended dips.

Res: 60.00, 60.25, 61.00, 61.71

Sup: 59.32, 58.86, 58.54, 58.31

Market Update – European Session: USD Limps Into Year-End

Notes/Observations

Asia:

China 19th Central Committee to discuss changes to the constitution in January, sparking chatter Xi could have an extended term as President

China Finance Ministry (MOF): Profits reinvestment by foreign firms to be temporarily exempted from provisional income tax

BoJ releases summary of opinions of Dec meeting which reiterated stance that appropriate for BoJ to continue current easy policy. As it had a long way to achieve 2% inflation target.

Japan Nov Preliminary Industrial Production M/M: 0.6% v 0.5%e; Y/Y: 3.7% v 3.6%e - South Korea Nov Industrial Production M/M: 0.2% v 1.3%e; Y/Y: -1.6% v 0.0%e

Bank of Korea (BoK) annual monetary strategy for 2018: 2018 monetary policy to remain accommodative

Europe:

EU officials indicate that UK Brexit minister may have been "sidelined"; EU negotiator Barnier has been dealing directly with another UK official

France Nov Net Change in Jobseekers: -29.5K v +8.0K prior

Americas:

President Trump legal team reportedly plans to attack former National Security Adviser Flynn's credibility

US Commerce Dept. issues final ruling on aircraft subsidies in Canada: Says subsidies were provided on some of Canada's aircraft exports

Energy:

Weekly API Oil Inventories: Crude: -6M v -5.2M prior

Economic Data:

(RU) Russia Dec Manufacturing PMI: 52.0 v 52.0e

(TR) Turkey Dec Economic Confidence: 95.0 v 97.9 prior

(FI) Finland Nov House Price Index M/M: -1.0% v -0.2% prior; Y/Y: 0.1% v 0.5% prior

(NO) Norway Nov Retail Sales W/Auto Fuel M/M: 2.1% v 1.0%e

(CN) China Q3 Final Current Account: $40.5B v $37.1B prelim

(SE) Sweden Nov Trade Balance (SEK): -3.0B v -3.1B prior

(HK) Hong Kong Nov Trade Balance (HKD): -39.7B v -41.6Be, Exports Y/Y: 7.8% v 6.0%e; Imports Y/Y: 8.6% v 8.2%e

(AT) Austria Dec Manufacturing PMI: 64.3 v 61.9 prior

(UK) Nov BBA Loans for House Purchases: 39.5K v 40.4K prior

(BR) Brazil Dec FGV Inflation IGPM M/M: 0.9% v 0.9%e; Y/Y: -0.5% v -0.5%e

Fixed Income Issuance:

(IT) Italy Debt Agency (Tesoro) sold total €4.91B vs. €3.5-5.0B indicated range in 5-year and 10-year BTP Bonds

Sold €2.41B vs. €2.0-2.5B indicated range in 0.9% Aug 2022 BTP bonds; Avg Yield: 0.60% v 0.58% prior; Bid-to-cover: 1.74x v 1.53x prior

Sold €1.5B vs. €1.0-1.5B indicated range in 2.05% Aug 2027 BTP bonds; Avg Yield: 1.86% v 1.73% prior; Bid-to-cover: 1.82x v 1.65x prior

Sold €1.0B vs. €0.5-1.0B indicated range in 2.2% Aug 2027 BTP bonds; Avg Yield: 1.83% v 1.86% prior; Bid-to-cover: 2.21.919x v 1.43x prior

(IT) Italy Debt Agency (Tesoro) sold €2.0B vs. €1.5-2.0B indicated range in Apr 2025 CCTeu (Floating Rate bond); Avg Yield: 0.48% v 0.46% prior; Bid-to-cover: 1.68x v 1.60x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx50 -0.2% at 3,544, FTSE flat at 7,620, DAX -0.1% at 13,057, CAC-40 -0.1% at 5,366, IBEX-35 -0.3% at 10,133, FTSE MIB +0.1% at 22,217, SMI -01% at 9,423, S&P 500 Futures +0.1%]

Market focal points/key themes: European markets open largely lower but adjusted to trade largely mixed as the session progressed; year-end trading remains light in final full trading day of the year; UK initial exception to downward trend; commodity prices continue to support materials stocks; energy stocks outperforming on higher oil prices ahead of US energy data; attention on US jobless data later in the session

Equities

Consumer discretionary [Ceconomy CEC.DE +2.5% (death of major shareholder)]

Financials [Banco BPM BAMI.IT +3.6% (outlook)]

Healthcare [MDxHealth MDXHH.BE -10.1% (cuts outlook), Nanobiotix NANO.FR +7.9% (continuation following IND acceptance)]

Speakers

(EU) ECB Economic Bulletin: Underlying inflation expected to gradually pick-up; region economic expansion is solid and broad-based (in-line with Draghi Dec press conference)

Germany Wisemen Bofinger noted that Chancellor Merkel should quickly agree on a coalition with SPD as a failure would be negative for the domestic economy. Next 3-4 months would be fine without a govt but needed stability in the long term

Turkey President Chief Adviser Ertem: 2018 GDP growth between 6.0-7.0% will not trigger inflation. Either a rapid rise or decline in TRY currency (Lira) would be negative. USD/TRY pair seen ending 2017 around 3.80 level; no sudden appreciation of USD expected in 2018

FX Regulator SAFE: Sound domestic economy backs stable foreign debt growth

Currencies

USD continued limping into year-end on a soft tone. Dealer continue to assess possible trends for 2018 noting that monetary policy convergence could weigh on the USD in 2018 as central banks other than the Fed had begun moving away from monetary stimulus, or started to raise interest rates. The USD having its worst year against the major G10 currencies in over a decade.

EUR/USD at 1-month highs and holding above the 1.1930 area with the greenback annual performance in the pair the worst since 2003.

Fixed Income

Bund futures trades at 161.84 down 52 ticks trading back below the 162 handle in light trade on mixed European Equity markets. The shorter end leads futures lower with the Shatz yield approaching 5bp up on the day. 10 Year yields approach 0.4%, with a reversal targeting day high at 162.36.

Thursdays liquidity report showed Wednesday's excess liquidity at €1.796T. Use of the marginal lending facility fell to €216M from €275M prior.

Looking Ahead

(ES) Spain Nov YTD Budget Balance: No est v -€12.9B prior

(EG) Egypt Central Bank Interest Rate Decision:

06:45 (US) Daily Libor Fixing

07:30 (BR) Brazil Nov Primary Budget Balance (BRL): -6.0Be v +4.8B prior; Nominal Budget Balance: -41.4Be v -30.5B prior, Net Debt to GDP: 51.2%e v 50.7 prior

08:00 (RU) Russia Gold and Forex Reserve w/e Dec 22nd: No est v $430.3B prior

08:30 (US) Initial Jobless Claims: 240Ke v 245K prior; Continuing Claims: 1.90Me v 1.932M prior

08:30 (US) Nov Advance Goods Trade Balance: -$67.9Be v -$68.1B prior (revised from -$68.3B)

08:30 (US) Nov Preliminary Wholesale Inventories M/M: +0.3%e v -0.5% prior, Retail Inventories M/M: No est v -0.1% prior ECB Forex

09:45 (US) Dec Chicago Purchasing Manager: 62.0e v 63.9 prior

10:00 (MX) Mexico Central Bank (Banxico) Dec Minutes

10:00 (CO) Colombia Nov National Unemployment Rate: No est v 8.6% prior, Urban Unemployment Rate: 9.1%e v 9.5% prior

10:30 (US) Weekly EIA Natural Gas Inventories

11:00 (US) Weekly DOE Crude Oil Inventories

13:00 (US) Treasury to sell 7-Year Notes

14:00 (CO) Colombia Central Bank Dec Minutes

14:00 (AR) Argentina Nov Industrial Production Y/Y: 2.8%e v 4.4% prior; Construction Activity Y/Y: No est v 25.3% prior

DAX30 Clear Congestion Between Two Camarilla Levels

The German Equities market has been quiet as expected during the festive season. In the absence of any German economic data or any major Dax30 company announcements the price is ranging within a rectangle consolidation.

Technically the DAX is congested between W L1 and W H1 - two basic camarilla levels that might break if we see any price momentum.13139.67 is the resistance to watch. Break above and we could see a retest of W H3 -13167.33 and only on strong momentum M H3 - 13213.42 and W H4 - 13258.95 could be reached. If it happens the price might form a right shoulder and could make a u-turn.

To the downside, pay attention to the break of 13012 where W L3 -12984.29 and W L4 12892.77 might be targets. Final bearish target is M L3 -12834.84. For any breakout to happen, we must see some movement in the market. Any profit taking before New Year might provide fresh new price momentum so watch out for it.

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

M H4 - Monthly Camarilla Pivot (Very Strong Monthly Resistance)

M L3 – Monthly Camarilla Pivot (Monthly Support)

M L4 – Monthly H4 Camarilla (Monthly Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

Euro Pushes Towards 1.20, Markets Eye German CPI

EUR/USD continues to gain ground, and has moved higher in the Thursday session, after gains on Wednesday. Currently, EUR/USD is trading at 1.1935, up 0.38% on the day. There are no eurozone data releases on the schedule. In the US, today’s key event is unemployment claims, which is expected to drop to 240 thousand. On Friday, Germany releases Final CPI.

Christmas week is light on eurozone economic releases, so the markets will be paying close attention to German CPI, which will be released on Friday. The indicator rose 0.3% in November, marking a 4-month gain. The markets are expecting a gain of 0.5% for December. In the eurozone, annual average inflation inched up to 1.5% in November, up from 1.4% in October. This marked a multi-year high. Earlier this month, in a nod to stronger economic activity in 2017, the ECB raised its forecasts for growth and inflation for the eurozone from this year through to 2019. Still, inflation remains well below the ECB target of around 2.0%, and ECB policymakers are unlikely to announce an end to their stimulus package until inflation moves closer to the 2.0% target.

US housing numbers continue to beat expectations, as Pending Home Sales surprised the markets with a gain of 0.2%. Last week, Housing Starts came in at 1.30 million, beating the forecast of 1.25 million. On Tuesday, New Home Sales sparkled, with a gain of 733 thousand. This easily beat the estimate of 654 thousand, and was the highest reading since September 2007. On Thursday, the US releases unemployment claims, which is expected to drop to 241 thousand.

With the US economy expanding above 3% in the third quarter, the Federal Reserve remains on track for another rate hike in January. The CME Group has pegged the odds of a January hike at 100%, which could give a boost to the US dollar. If the economy continues its impressive pace of growth above 3%, the Fed could raise rates up to four times in 2018. Despite strong economic conditions, the Federal Reserve’s inflation target of 2.0% remains elusive. Fed Chair Janet Yellen and other FOMC members have said that they expect that the strong labor market will lead to higher inflation. Although this is yet to materialize, of significance to the markets is the commitment of the Fed to press ahead with rate hikes despite low inflation.