Sample Category Title

Dollar Gains Versus Yen On Rising Yields And Dovish BoJ, Canadian CPI Eyed

Here are the latest developments in global markets:

FOREX: The dollar edged slightly higher versus a basket of currencies but was still trading not far above a two-week low hit yesterday. The US currency continued gaining versus the yen, being supported by rising Treasury yields.

STOCKS: The Nikkei 225 closed down by 0.1% and the Topix added 0.1% to renew its 26-year high. The Hang Seng was up by 0.5%. Euro Stoxx 50 futures were marginally lower at 0726 GMT, while Dow, S&P 500 and Nasdaq 100 equivalents were all up, though close to being flat.

COMMODITIES: WTI and Brent crude were both little changed, trading at $58.12 and $64.55 per barrel. Gold was also not much changed, trading around two-week high levels at $1,265.67 an ounce.

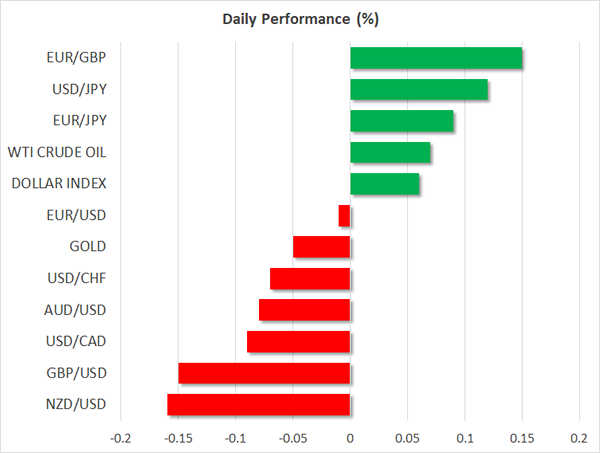

Major movers: Dollar on the rise versus yen, helped by yields and dovish stance by BoJ; euro at four-week high relative to sterling and at highest since late 2015 versus yen

The dollar index was slightly up after losing ground the three preceding days. The index was at 93.38. This comes after yesterday’s final vote in favor of tax reforms by the House of Representatives. What remains now before it passes into law, is for President Trump to sign the bill.

Dollar/yen was 0.1% up and on its third straight day of advancing. It was last at 113.53, not far below a more than one-week high recorded earlier in the day. The greenback was boosted by rising yields. Indicatively, the 10-year US Treasury yield was last at around its highest since late March at 2.49%. Meanwhile, the BoJ completed its meeting on monetary policy during the Asian session, with policymakers keeping policy unchanged as expected. A press conference by governor Kuroda followed, during which dollar/yen was moving higher as he appeared in no hurry to tighten policy.

Euro/dollar was roughly flat at 1.1868, trading around two-week high levels. Eurozone’s common currency posted hefty gains this week, being boosted by rising German bond yields. Euro/pound was trading at 0.8886, this being around four-week high levels. Euro/yen was 0.1% up at 134.77, just a shade below its highest since late 2015 hit earlier today.

Pound/dollar was 0.15% down at 1.3352 as the EU is being seen as taking a hard stance on Brexit. The antipodeans were also losing ground versus the greenback, with aussie/dollar being down by 0.1% at 0.7660 and kiwi/dollar trading lower by 0.15% and being marginally below the 0.70 handle.

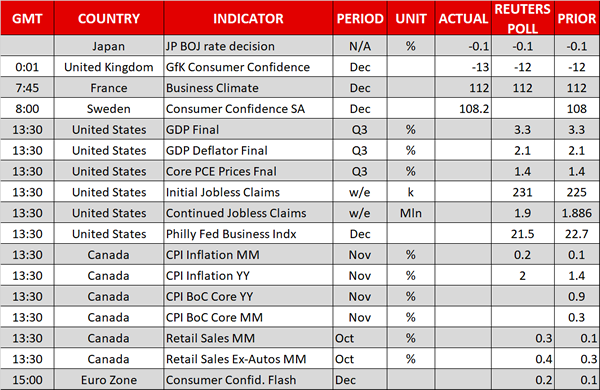

Day ahead: Canadian inflation could reach BoC target

The economic calendar will be pretty busy on Thursday, with the US, Canada and the Eurozone delivering reports ahead of the Christmas holiday.

Out of the US, final Q3 GDP growth figures are due at 1330 GMT, with analysts predicting a growth rate of 3.3% on an annualized basis as was previously reported. This would constitute the highest expansion the economy has experienced in a year.

Meanwhile, final US core PCE prices are expected to stand in line with previous estimates at 1.4% y/y in the third quarter.

US initial jobless claims are anticipated to climb by 6,000 in the week ending December 15, while Philadelphia’s Fed manufacturing index is forecasted to decline by 0.8 points to 21.5 in December.

The main focus, however, would be in Canada where data on inflation and retail sales are scheduled to be published at 1330 GMT, whilst the ADP Canadian employment report will give some evidence on the number of people employed in nonfarm sectors.

According to forecasts, the headline CPI is anticipated to rise by 0.6 percentage points to 2.0% y/y in November, hitting a nine-month high and touching the BoC’s inflation target.

Monthly retail sales are said to expand by 0.3% in October compared to 0.1% seen in September. If true, this would be the highest mark posted since July. The core measure, which excludes volatile items is projected to inch up by 0.1 percentage points to 0.4%.

Elsewhere, flash readings on Eurozone’s consumer confidence will be available at 1500 GMT, with analysts awaiting the measure to edge down to zero in December after reaching positive levels of 0.1 in the previous month for the first time since 2001. Meanwhile, Catalonia will be holding regional elections today. It will be interesting to see whether pro-independence forces come out stronger or weaker.

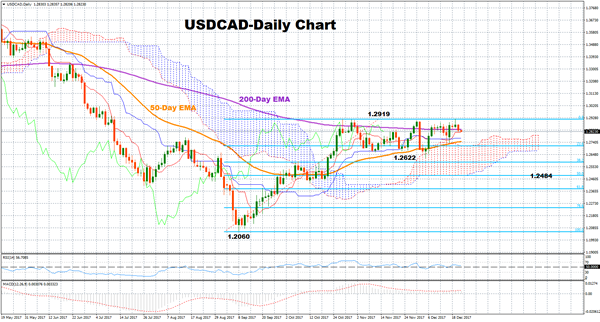

Technical Analysis: USDCAD within a range, looks neutral in short-term

USDCAD has been moving between 1.2622 and 1.2915 since the end of October. The RSI, which has been moving sideways in recent days, is projecting a neutral picture in the short-term.

Better-than-expected data out of Canada later today are expected to push the pair lower. In such a case, support could be met at around the 50-day exponential moving average at 1.2746. The lower bound of the range at 1.2622 could also act as support, while steeper declines could target the 50% Fibonacci at 1.2484 of the upleg from 1.2060 to 1.2919.

If on the other hand Canadian releases disappoint, prices could find room to rise back to the top of the range at 1.2919, with the area around this level potentially acting as a barrier to the upside. Further increases might also shift the focus towards the 1.30-1.31 key area.

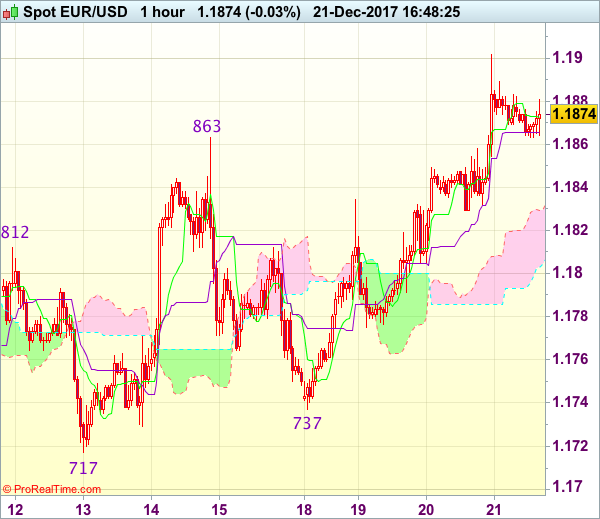

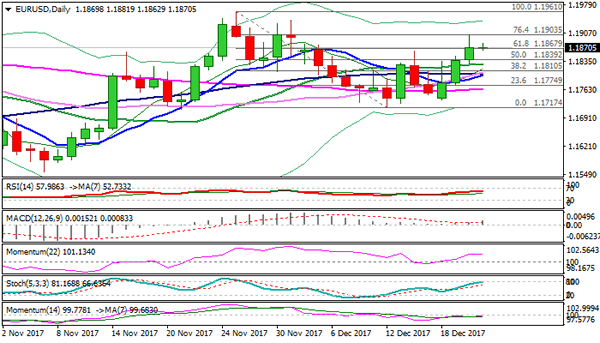

Trade Idea : EUR/USD – Buy at 1.1820

EUR/USD - 1.1880

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1872

Kijun-Sen level : 1.1867

Ichimoku cloud top : 1.1829

Ichimoku cloud bottom : 1.1804

Original strategy :

Buy at 1.1820, Target: 1.1920, Stop: 1.1785

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1820, Target: 1.1920, Stop: 1.1785

Position : -

Target : -

Stop : -

As the single currency has eased after rising to 1.1902 yesterday, minor consolidation below this level would be seen and pullback to 1.1840-50 cannot be ruled out, however, reckon 1.1805-10 would contain downside and bring another rise later, above said resistance at 1.1902 would extend the erratic upmove from 1.1717 towards resistance at 1.1940 which is likely to hold from here due to near term overbought condition.

In view of this, would not chase this rise here and would be prudent to buy euro on pullback as 1.1820 should limit downside. Below 1.1800 would bring test of 1.1775 support but only break there would suggest top is formed instead, then subsequent retreat to 1.1750 would follow but support at 1.1737 should remain intact.

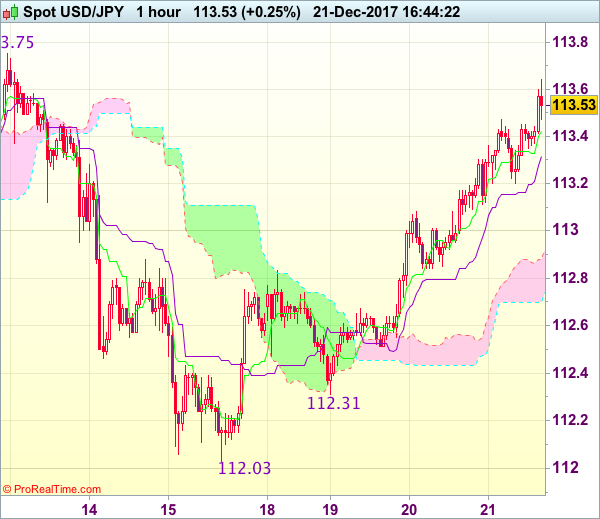

Trade Idea : USD/JPY – Buy at 112.80

USD/JPY - 113.53

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 113.42

Kijun-Sen level : 113.32

Ichimoku cloud top : 112.88

Ichimoku cloud bottom : 112.70

Original strategy :

Buy at 112.80, Target: 113.70, Stop: 112.45

Position : -

Target : -

Stop : -

New strategy :

Buy at 112.80, Target: 113.70, Stop: 112.45

Position : -

Target : -

Stop : -

As the greenback has maintained a firm undertone after staging a strong rebound from 112.03, adding credence to our bullish view for this move to bring test of resistance at 113.75, however, break there is needed to signal the rise from 110.84 low has resumed for headway towards 113.95-00, then towards 114.30-35 later.

In view of this, we are looking to buy dollar on pullback as 112.80-85 should limit downside and bring another rise later. Below 112.50-55 would suggest top is formed, bring test of 112.31 support but only break of latter level would signal the rebound from 112.03 has ended instead, bring retest of this level later.

BOJ Maintained Accommodative Policies, Kuroda Sent No Signal About Normalization

As widely anticipated, BOJ again voted 8-1 to leave the monetary policies unchanged in October. The targets for short- and long-term interest rates stay at -0.1% and around 0%, respectively while the guideline for JGB purchases remains at an annual pace of about 80 trillion yen. The central bank has turned more upbeat on the economic outlook, especially on Capex and consumption. Goushi Kataoka was again the lone dissent as he supported bond purchases so as to facilitate the decline of 10-year (or over) bond yields. Governor Kuroda's speech at the press conference has not tilted towards less easing/ policy normalization in the near-term

BOJ reiterated that domestic economic is 'expanding moderately'. Policymakers noted that 'business fixed investment has continued on an increasing trend'. This is compared with October's reference that 'business fixed investment has been on a moderate increasing trend'. Yet, they suggested that 'public investment has been more or less flat, remaining at a relatively high level'. This reference appears softened slightly from the October one noting 'public investment has been increasing'. The central bank appears less concerned about the inflation outlook, though it reiterated that 'inflation expectations have remained in a weakening phase'. It retained the view that the year-on-year rate of change in the CPI should continue 'on an uptrend and increase toward 2%, mainly on the back of an improvement in the output gap and a rise in medium- to long-term inflation expectations'.

Being the single dissenter for a third time, Kataoka repeated his stance that 'the possibility of the year-on-year rate of change in the CPI increasing toward +2% going forward was low at this point'. Therefore, 'it was appropriate for the Bank to purchase JGBs so that yields on JGBs with maturities of 10 years and longer would be broadly lowered'. He also warned that in case of 'a delay in the timing of achieving the price stability target due to domestic factors, the Bank should take additional easing measures'.

Those who had anticipated hints on policy normalization would have been disappointed. The tones of both the accompanying statement and Kuroda's press conference are in line: pledging that it would 'continue with ‘Quantitative and Qualitative Monetary Easing (QQE) with

Yield Curve Control,' aiming to achieve the price stability target of 2 percent, as long as it is ecessary for maintaining that target in a stable manner'. Kuroda has not downplayed the importance of monetary easing by discussing about the side-effects of accommodative policy,

Forex: US Tax Bill Passes And ‘Status-Quo’ For The Bank Of Japan

On Wednesday, the US Senate approved the tax bill 51 for and 48 against, while the House of Representatives gave it final approval, passing it for the second time in two days after a procedural foul-up forced another vote. The bill passed the House with a vote of 224-201, with no Democrats voting for it and some Republicans members also voting no. The bill now heads to President Trump for his signature. The markets remain concerned as to how much stimulus the bill will give to an already improving US economy. Improved growth could cause upward inflationary pressures which may result in the Federal Reserve increasing the pace of rate hikes which would see USD strength. However, it could increase fiscal deficits with little incentive for businesses to hire more workers which could stunt economic growth and see USD under pressure. Only time will tell what effect the bill will have on USD as the markets are now gradually 'winding down' for the Holiday Season.

Earlier today the Bank of Japan released its monetary policy statement opting to keep its policy unchanged. The BoJ stated that it is committed to its 5-year-old 2% inflation target, but suggested inflation expectations to be in a 'weakening phase.' It forecast that inflation would likely gradually rise thanks to tightening capacity commenting 'Industrial production has been on an increasing trend, and labor market conditions have continued to tighten steadily,' Short term interest rates will stay at -0.1% and the target for the 10-year government bond yield at zero percent. The statement was expected by the markets although many believe the BoJ will remove its stimulus (QE) in 2018. JPY has strengthened against USD recently and early Thursday trading has seen some of those gains erased as USDJPY has moved higher.

EURUSD is little changed in early Thursday trading around 1.1868

USDJPY is slightly higher in early session trading around 113.44

GBPUSD is relatively unchanged overnight trading around 1.3367

Gold is slightly higher trading around $1,266

WTI is 0.1% higher trading around $58.10

Major data releases for today:

At 09:30 GMT: the UK Office for National Statistics (ONS) will release Public Sector Net Borrowing requirement for November. Forecasts are calling for a substantially higher release of £11.163B up from October’s £7.464B. Regardless of the actual release the markets are likely to see volatility in GBP.

At 13:30 GMT: the US Bureau of Economic Analysis at the Department of Labor, will release Gross Domestic Product (GDP) for Q3 both Index and Annualized. The annualized GDP is expected to remain unchanged at 3.3% with the Index expected to be also unchanged at 2.1%.

At 13:30 GMT there are a plethora of economic data releases:

The US Bureau of Economic Analysis at the Department of Labor, will release Personal Consumption Expenditures (PCE) Price and Core (QoQ) for Q3. Core is expected unchanged at 1.4% and Prices are expected unchanged at 1.5%

The US Department of Labor will release Initial Jobless Claims for the week ended December 15th and Continuing Jobless Claims for the week ended December 8th. Initial Claims are expected to come in at 241K a higher reading than the previous 225K. Continuing Claims are forecast to come in at 1.928M being higher than the previous release of 1.886M.

Statistics Canada will release a plethora of month-on-month economic data; For October: Retail Sales are forecast to come in at 0.0% from the previous 0.1% with the ex-Auto reading expected at 0.0% from 0.3%. For November: Consumer Price Index is forecast to come in at 0.0% from 0.1% CPI Core is forecast at -0.7% from the previous 0.3%. Annualized CPI is expected to come in at 1.3%, slightly lower than the previous reading of 1.4%.

Technical Outlook: EURUSD May Correct Deeper After Strong Rejection At 1.1900

The Euro maintains firm tone on Thursday and consolidating under fresh high at 1.1900. Wednesday's close marginally above 1.1867 (Fibo 61.8% of 1.1961/1.1717) was bullish signal, despite strong upside rejection which left bullish daily candle with long upper shadow. Weaker dollar on waning optimism over US tax overhaul, keeps the Euro inflated, however, three-day rally from 1.1737 trough may take a breather as slow stochastic is entering overbought territory on daily chart. Deeper dips off 1.1900 spike high are expected to find footstep above 1.1828/23 (20SMA/daily cloud top) to keep near-term bulls in play for renewed attack at 1.1900 and extension towards 1.1961 (27 Nov high) psychological 1.2000 barrier. No releases from EU scheduled today and markets will be looking for US Q3 GDP data for fresh signals.

Res: 1.1881, 1.1900, 1.1940, 1.1961

Sup: 1.1862, 1.1828, 1.1823, 1.1810

NZDUSD Intraday Analysis

NZDUSD (0.7007): The New Zealand dollar posted some declines but price action managed to bounce off the lower median line. As price attempts to test the previous highs we see that the Stochastics oscillator has been posting a lower high. This bearish divergence could indicate a potential correction to the downside. Support at 0.6917 remains in focus while to the upside, the continued momentum could keep the NZDUSD testing the next resistance level at 0.7062.

USDJPY Intraday Analysis

USDJPY (113.39): The USDJPY managed to push higher, marking a two day gain. Price action is seen attempting to test the previous highs near 113.7. Following the breakout above the resistance level at 113.06 - 112.90, any short term declines could see price falling back to establish support at this level. To the upside, USDJPY will need to breakout above the previous highs in order to post further gains. 114.00 remains the next target to the upside, while the downside could be limited to 113.00 region.

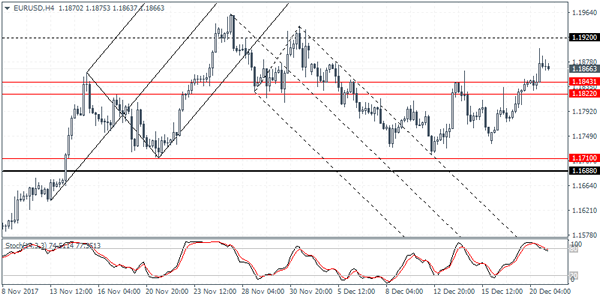

EURUSD Intraday Analysis

EURUSD (1.1866): The euro managed to post another day of gains, marking a three day winning streak. Price action managed to rise above the 1.1843 - 1.1822 region of resistance and the currency pair looks set to target the 1.1920 resistance further up. In the near term, any declines could be limited to the recently breached resistance level. Establishing support here could signal further gains in the short term and validates the upside bias. Alternately, if EURUSD fails to hold near the support we could expect to see price action decline as the currency pair is likely to settle into a range once again..

BoJ Leaves Monetary Policy Unchanged, NZD GDP Rises 0.6%

The Bank of Japan's monetary policy meeting held earlier today saw interest rates and the central bank's QQE purchases remaining unchanged as expected. The board members voted 8 -1 to keep monetary policy unchanged while keeping the government bond holdings steady at 80 trillion yen.

The BoJ Governor Kuroda is expected to hold a press conference later in the day. In the overnight session, New Zealand's GDP data showed a 0.6% increase in the third quarter as expected. The second quarter GDP was revised higher to show a 1.0% increase on the quarter. On a yearly basis, New Zealand's GDP was seen rising 2.4%.

In the U.S. trading session, the dollar was muted to the news of the Congress passing the tax reforms bill. On the economic front, the NAR reported that existing home sales rose 5.6% on the month in November.

Looking ahead, the economic calendar today will see the inflation data from Canada. The U.S. department of commerce will be releasing the final GDP for the third quarter which is expected to be confirmed at 3.3%.