Sample Category Title

Daily Wave Analysis: EUR/USD Completes Wave 5 And Reverses At Fibonacci Resistance

Currency pair EUR/USD

The EUR/USD respected the resistance zone which was indicated by the wave C (blue) of wave X (purple). Price is now in between support (blue) and resistance (red) trend lines. A bearish break would make the current wave pattern likely and could see price challenge the Fibs of wave 2 (pink).

The EUR/USD completed its 4 and 5th wave (green) yesterday as expected. Price made a reversal and is now challenging a support trend line (blue). An immediate bearish breakout could see price fall lower whereas a bullish bounce could be part of wave B (blue).

Currency pair GBP/USD

The GBP/USD is in a bullish channel (green lines) but price is close to a key resistance trend line (red).

A bullish breakout above resistance (orange/red) could see price move higher towards the Fibonacci targets of waves 5.

Currency pair USD/JPY

The USD/JPY continued lower within wave A (purple). A bullish bounce is probably part of a wave B (purple) correction within a larger wave 2/B (light purple).

The USD/JPYcould be building a wave 5 (blue) of waveA (purple). A break above resistance trend line (red) could start wave B (purple).

EU Backing For May After Loss Of Brexit Vote

Market movers today

Following the 'Central Bank Super Thursday' yesterday, we have a relatively light data calendar today.

Focus remains also on the EU summit in Brussels, where the Brexit discussions are scheduled to take place today. Following Wednesday's defeat about a parliamentary vote on the final Brexit deal, PM Theresa May's posit ion has weakened in t he negotiations.

In the US, industrial product ion for November and Empire manufacturing index for December are due to be released today.

In Russia, we expect the central bank to cut its policy rate to 8.0% from 8.25%.

In Denmark, Finance Denmark's housing market statistics for Q3 are due out .

Selected market news

The ECB left policy measures and forward guidance unchanged, while lifting its growth forecasts. As expected, the ECB reiterated that policy rates would remain at current or lower levels for an extended period and well beyond the horizon of asset purchases. Meanwhile, however, the forecast were lifted, particularly for 2018 (lifted to 2.3% from 1.8% in September). The inflation forecast was also lifted from 1.2% to 1.4% in 2018. Reflecting the stronger out look, Mario Draghi stressed that the ECB is growing more confident in its ability to meet the inflation target eventually. We expect the ECB to taper APP purchases to zero in Q4 18 and deliver the first deposit rate hike in Q2 19. See ECB review - Christmas mood leaves QE exit decisions for 2018, 14 December, for more details.

EU backing for May after loss of Brexit vote . Yesterday, several EU leaders expressed support for the UK Prime Minister after she had lost a vote on Wednesday meaning that the UK parliament will have a vote on the final Brexit deal. However, at the EU summit , there were warnings to UK MPs that the EU would not have the time nor will to renegotiate a Brexit deal.

In terms of economic data, the strong US retail sales took focus yesterday. Sales were up by 0.8% in November, well above expectations for a 0.3% rise. Also, October retail sales were revised higher to 0.5% from 0.2%, while the core retail sales rose 0.8% in November. The dollar index rose 0.1% as a result , while 10Y US Treasury yields were 2bp higher, closing at 2.35%.

Yesterday, Turkey's central bank left its benchmark repo rate unchanged at 8.00% as expected. Yet , the late liquidity rate was raised by 50bp to 12.75%, as inflation has accelerated to a multi-year highest and t he T RY's volatility has surged recently.

Market Update – Asian Session: Asian Equities Generally Track Weakness In US Session

Australia/New Zealand

ASX 200 opened -0.2%; closed -0.2%; REIT index -1%, Financials -0.5% Qantas -1%

(AU) RBA Harper (Dove): Excess capacity in labor market likely bigger than thought; Rates meed to stay supportive of the economy; 5% likely not tipping point for wage growth

(NZ) New Zealand Nov Business Manufacturing PMI: 57.7 v 57.3 prior

(NZ) NZ Fin Min Robertson: Comfortable with general trend of Kiwi (NZ$)

(NZ) New Zealand sells NZ$200M in April 2025 bonds, avg yield 2.5601%, implied bid to cover 3.86x

China/Hong Kong

Hang Seng opened -0.6%, Shanghai Composite -0.2%

Hang Seng Energy Index -1.5%, Property/Construction -1.2%, Financials -1%, Information Technology -0.9%

Property company Sunac China -9% (capital raise)

Li & Fung +5% (announced $1.1B asset sale, special dividend)

(CN) PBoC releases pledged financing business management rules; to accept more kinds of bonds for pledged financing; To accept local government bonds as collateral in certain cases; Says seeks to prevent payment and clearing risks.

(CN) PBoC OMO: CNY150B in 7 and 28-day reverse repos v CNY50B injected in 7 and 28 day reverse repos prior; Net injected CNY150B v CNY190B drain prior (leaves yields unchanged vs prior session)

(CN) PBoC sets yuan reference rate at 6.6113 v 6.6033 prior

(CN) China MOF sells 30-year bonds: Avg yield 4.3555% v 4.35%e, bid to cover 2.09x

(CN) China MOF sells 3-month bills: Avg yield 3.9275%

(HK) Hong Kong may seek to limit the voting power of dual-class shares – HK Press

Korea

Kospi opened +0.8%

Kumho Tire +30% (M&A speculation)

Moody’s raises South Korea Banking System Outlook to Stable from Negative; raises South Korea 2017 GDP growth forecast to 3.0% (2.5% prior), 2018 to 2.8% (2.0% prior)

South Korea Blockchain Association: To improve proof of identity for users of cryptocurrency trading on exchanges; new measures take effect on Jan 1, 2018

Thursday’s late session weakness in the Kospi linked to program trading – Analyst

South Korea Nov Trade Balance: $7.6B v $7.8Be

(KR) US North Korea Envoy Yun: US is open to dialogue with North Korea; has not met with North Korea officials in Thailand

(CN) PBoC Gov Zhou said to meet South Korea Vice Premier in relation to financial cooperation

Japan

Nikkei 225 opened -0.3%; closed: -0.6%

Large financials again track declines in the US: Mitsubishi UFJ -1.4%, Sumitomo Mitsui -0.8%

Rakuten’s planned entry into mobile network operator business continues to weigh on telecoms: Rakuten -5.4%, KDDI -5.5%, Softbank -2.4%

Automakers track US declines: Toyota -1.4%; TOPIX Iron & Steel index -1.4% (US Steel ended -3.4%)

Nikkei heavy component Fast Retailing +1%

Q4 Tankan Large Manufacturer sentiment hits 11-year high; Overall Tankan survey mixed

(JP) JAPAN Q4 TANKAN LARGE ALL INDUSTRY MFG INDEX: 25 V 24E (11-year high); LARGE MFG OUTLOOK 19 V 22E; LARGE ALL INDUSTRY CAPEX 7.4% V 7.5%E

Japan auto union said to again seek ¥3K base wage increase – Japanese press

Japan Auto Manufacturers Group (JAMA): Japan auto industry suffers from labor shortage

(JP) BoJ said to ‘tweak’ message as dissenter calls for more easing – US financial press; The BoJ is due to hold its Dec two-day policy meeting on Dec 20-21st (Wed and Thursday)

Japan Chief Cabinet Sec Suga: To implement additional sanctions on North Korea; To freeze assets of 19 groups

Other Asia

(ID) Indonesia Nov Trade Balance: $130M v $844Me; Imports Y/Y: 19.6% v 13.0%e

North America

US equities ended lower amid comments from Republican Senator Rubio: Dow -0.3%, S&P500 -0.4%, Nasdaq -0.3%, Russell 2000 -1.2%

S&P500 Materials Sector -1.1%, Health Care -1%

Oracle: -6.5% afterhours (guided Q3 earnings below ests)

Costco: +2.3% afterhours (Q1 results above ests)

CSX: Announces Medical Leave of CEO E. Hunter Harrison; Names COO James Foote as acting CEO

NPD: US Nov Total Video Game Sales $2.69B, +30% y/y

(US) Senator Rubio said to vote no on tax bill unless working poor tax credit is expanded - Washington Post

(US) Speaker of House Ryan (R-WI) considering retiring from Congress after 2018 – Politico

Europe

(UK) UK PM May said expected to ‘back down’ on Brexit date plan – UK Press

(UK) Germany Chancellor Merkel: EU leaders could move to Brexit Phase 2 on Friday

(ES) Survey shows Catalan separatists have lost their lead ahead of new elections - Spain press

(FR) Bank of France: Sees 2017 GDP +1.8% (v prior forecast 1.3%), sees 2018 GDP +1.7% (v prior forecast 1.5%)

(EU) ECB's Vasiliauskas (Lithuania): Does not see need for additional QE in 2018; measures implemented are showing results

(RU) EU's Tusk: The EU is united on the rollover of continuing economic sanctions on Russia

Levels as of 01:00ET

- Hang Seng -0.8%; Shanghai Composite -0.6%%; Kospi +0.5%

Equity Futures: S&P500 +0.1%; Nasdaq100 +0.1%, Dax +0.2%; FTSE100 flat

EUR 1.1765-1.1791 ; JPY 112.12-112.41; AUD 0.7655-0.7675 ;NZD 0.6979-0.7023

Dec Gold flat at $1,256/oz; Jan Crude Oil +0.3% at $57.20/brl; Dec Copper +0.2% at $3.079/lb

Aussie Dollar Trading Higher In The Asian Session

For the 24 hours to 23:00 GMT, the AUD rose 0.37% against the USD and closed at 0.766.

LME Copper prices rose 0.6% or $38.0/MT to $6723.0/MT. Aluminium prices rose 1.0% or $20.0/MT to $2017.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7668, with the AUD trading 0.1% higher against the USD from yesterday’s close.

The pair is expected to find support at 0.7653, and a fall through could take it to the next support level of 0.7637. The pair is expected to find its first resistance at 0.7682, and a rise through could take it to the next resistance level of 0.7695.

Next week, investors would keep a close watch on the Reserve Bank of Australia’s (RBA) December monetary policy meeting.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

ECB Kept Interest Rates At Record Low, Lifted Euro-Zone’s Growth Forecasts

For the 24 hours to 23:00 GMT, the EUR declined 0.47% against the USD and closed at 1.1767, after the European Central Bank (ECB) boosted the Euro-zone's 2018 economic growth and inflation forecasts, but stuck with its pledge to maintain its ultra-loose monetary policy as long as needed.

The ECB, as widely expected, maintained the key interest rate unchanged at 0.00% at its recent monetary policy meeting, and signalled that it would keep its aggressive monetary stimulus in place despite strong economic recovery in the Euro-bloc, in order to “sustain inflation” towards the ECB's target. Further, the central bank boosted the Euro-zone's growth forecast to 2.4% for 2017, up 0.2% and to 2.3% for 2018, from 1.8% predicted earlier. Inflation is expected to rise 1.4% next year, revised up from 1.2% estimated in September.

Macroeconomic data revealed that the flash Markit manufacturing PMI in the common currency region unexpectedly climbed to a record high level of 60.6 in December, confounding market expectations for a drop to a level of 59.7, thus highlighting that an upturn in the manufacturing sector continued to surge forward. The PMI had recorded a reading of 60.1 in the prior month. Moreover, the region's preliminary Markit services PMI unexpectedly rose to a level of 56.5 in December, notching its highest level in 80 months. Markets were expecting the PMI to ease to a level of 56.0, after recording a reading of 56.2 in the prior month.

Separately, growth in Germany's manufacturing sector surprisingly advanced to an all-time high level of 63.3 in December, against market expectations for a fall to a level of 62.0. In the prior month, the PMI had registered a reading of 62.5. Furthermore, the nation's services sector expanded at its fastest pace in 24 months, after it jumped to a level of 55.8 in December, beating market expectations for an advance to a level of 54.6. The PMI had registered a level of 54.3 in the prior month.

The greenback declined against its major peers, as upbeat US manufacturing sector data was offset by poor report on the services sector.

The flash Markit services PMI in the US registered an unexpected drop to a level of 52.4 in December, hitting its lowest level in over a year. In the previous month, the PMI had registered a level of 54.5, while investors had envisaged for an increase to a level of 54.7. On the other hand, the nation's preliminary Markit manufacturing PMI surprised to the upside, jumping to an 11-month high level of 55.0 in December, after recording a level of 53.9 in the prior month and defying market consensus for the index to record a steady reading.

Another set of data revealed that advance retail sales in the US grew 0.8% MoM in November, topping market expectations for a gain of 0.3%. Retail sales had risen by a revised 0.5% in the previous month. Also, the number of American filing for fresh jobless claims unexpectedly eased to a level of 225.0K in the week ended 09 December, declining to its lowest level since mid-October. Market participants had anticipated the initial jobless claims to remain steady at a reading of 236.0K recorded in the prior week.

In the Asian session, at GMT0400, the pair is trading at 1.1781, with the EUR trading 0.12% higher against the USD from yesterday's close.

The pair is expected to find support at 1.1743, and a fall through could take it to the next support level of 1.1705. The pair is expected to find its first resistance at 1.1841, and a rise through could take it to the next resistance level of 1.1901.

Looking ahead, traders would focus on the Euro-zone's trade balance numbers for October, due to release in a few hours. Additionally, the US industrial and manufacturing production data for November, due to release later in the day, will garner a lot of market attention.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

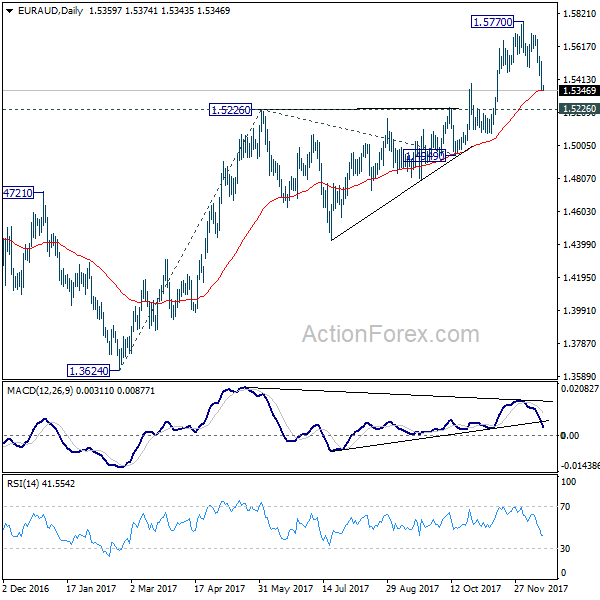

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5298; (P) 1.5409; (R1) 1.5473; More....

EUR/AUD drops further to as low as 1.5343 as correction from 1.5770 extends. At this point, we'd still expect downside to be contained above 1.5226 key support to bring rally resumption. Above 1.5482 minor resistance will turn bias to the upside for 1.5770. Break there will resume the medium term rise and target 61.8% projection of 1.3624 to 1.5226 from 1.4949 at 1.5939 first. However, sustained break of 1.5226 will carry larger bearish implications and turn outlook bearish.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top (2015 high) has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. We'll hold on to this bullish view as long as 1.5226 resistance turned support holds. Firm break of 1.6587 will resume long term rise from 1.1602 (2012 low).

BoE Held Interest Rate Steady At 0.50%, Stuck To Its Outlook For Modest Tightening

For the 24 hours to 23:00 GMT, the GBP rose 0.09% against the USD and closed at 1.3424, following better-than-expected retail sales data in the UK.

However, gains in the Pound were limited, after the Bank of England (BoE), at its latest monetary policy meeting, vowed that interest rates were likely to rise only gradually.

The BoE unanimously voted to keep its benchmark interest rate steady at 0.50% and its asset purchase facility at £435.0 billion, as widely expected. In the minutes accompanying the decision, policymakers stated that growth in the fourth quarter of this year “might be slightly softer” than in the previous quarter, while judging that inflation is likely to be close to its peak and will decline towards the 2.0% target in the medium term. The central bank also held the view that “further modest increases” in interest rates would be warranted over the next few years to help bring inflation to its target of 2.0%. On Brexit negotiations, the central bank stated that the latest developments reduce the chance of a disorderly exit from the EU.

On the macro front, Britain’s retail sales climbed more-than-expected by 1.1% on a monthly basis in November, allaying concerns of a slowdown in consumer spending. Retail sales had posted a revised gain of 0.5% in the prior month, while markets were expecting for an increase of 0.4%.

In the Asian session, at GMT0400, the pair is trading at 1.3433, with the GBP trading 0.07% higher against the USD from yesterday’s close.

The pair is expected to find support at 1.3395, and a fall through could take it to the next support level of 1.3358. The pair is expected to find its first resistance at 1.3468, and a rise through could take it to the next resistance level of 1.3504.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Japan’s Tankan Big Manufacturers’ Mood Improved To An 11-Year High Level In The Fourth Quarter Of 2017

For the 24 hours to 23:00 GMT, the USD declined 0.28% against the JPY and closed at 112.38.

In the Asian session, at GMT0400, the pair is trading at 112.27, with the USD trading 0.1% lower against the JPY from yesterday's close.

Overnight data revealed that Japan's Tankan large manufacturing index rose more-than-expected to a level of 25.0 in 4Q 2017, surging to an 11-year high level. Market participants had anticipated for a rise to a level of 24.0, compared to a reading of 22.0 in the preceding month. Meanwhile, the nation's Tankan non-manufacturing index remained steady at a level of 23.0 in 4Q 2017, while investors had envisaged for an increase to a level of 24.0.

Moreover, the nation's Tankan large manufacturing outlook index unexpectedly remained steady at 19.0 in 4Q 2017, while the non-manufacturing outlook index climbed less-than-anticipated to a level of 20.0 in 4Q 2017, after recording a reading of 19.0 in the previous month.

The pair is expected to find support at 111.93, and a fall through could take it to the next support level of 111.60. The pair is expected to find its first resistance at 112.74, and a rise through could take it to the next resistance level of 113.22.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

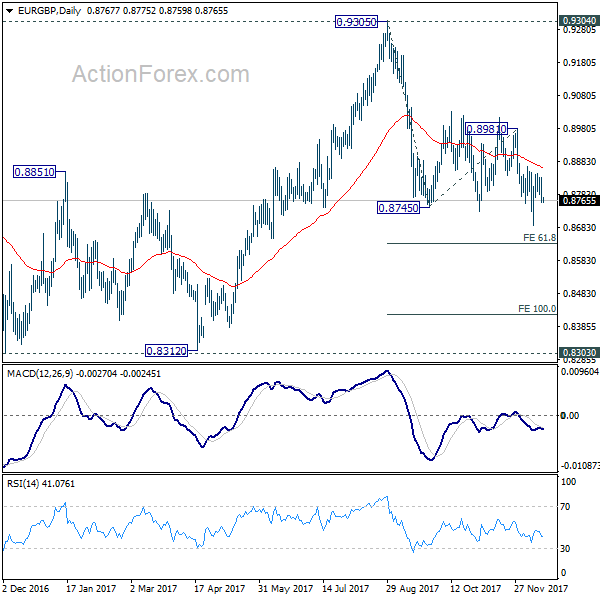

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8740; (P) 0.8787; (R1) 0.8813; More...

Intraday bias in EUR/GBP stays neutral at this point. With 0.8866 resistance intact, near term outlook remains mildly bearish and deeper fall is expected. Break of 0.8688 will extend the fall from 0.9305 and target 61.8% projection of 0.9305 to 0.8745 from 0.8981 at 0.8468 first and then 100% projection at 0.8151 next. However, break of 0.8866 resistance will indicate near term reversal and turn bias back to the upside for 0.8981 resistance instead.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

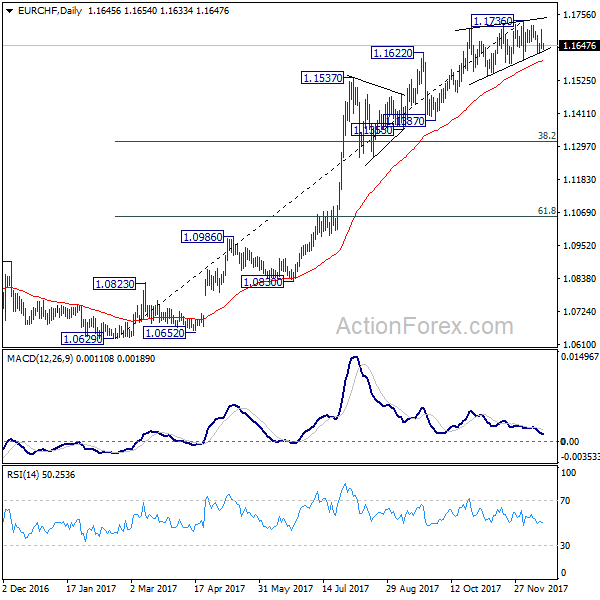

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1619; (P) 1.1662; (R1) 1.1687; More...

Intraday bias in EUR/CHF remains neutral and outlook is unchanged. It's close to topping, if not formed. This is supported by persistent bearish divergence condition in 4 hour MACD, and rising wedge like structure. On the downside, break of 1.1597 support will will be a strong sign of trend reversal and should turn outlook bearish for 38.2% retracement of 1.0629 to 1.1736 at 1.1313.

In the bigger picture, while a medium term top could be around the corner, there is no change in the larger outlook. That is, long term rise from SNB spike low back in 2015 is still in progress and would extend. As long as 1.1198 resistance turned support holds, we'll hold on to this bullish view and expect another to prior SNB imposed floor at 1.2000. Though, we'll reassess the outlook if 1.1198 is firmly taken out.