Sample Category Title

USD/JPY Bearish Breakout

USD/JPY is pushing lower. Strong resistance is given at 114.73 (06/11/2017 high) while hourly support is given at 111.99 (06/12/2017 low). The technical structure suggests nonetheless further bullish rebound.

We favor a long-term bearish bias. Support is now given at 99.02 (10/08/2013 low). A gradual rise towards the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

GBP/USD Riding Short-Term Downtrend Channel

GBP/USD continues to move lower within downtrend short-term channel. The technical structure indicates further weakness. Support is given at a distance at 1.3304 (12/12/2017 low).

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline. Long-term support can be found at 1.1841 (07/10/2017 low). Long-term resistance given around 1.35 is at stake and indicates a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

EUR/USD Bouncing Back

EUR/USD's short-term bearish momentum has abruptly ended. Hourly resistance is given at 1.1961 (27/11/2017 high). Hourly support given at 1.1713 (21/11/2017 low). Expected to show renewed decline.

In the longer term, the momentum is now turning largely positive. We favour a continued bullish bias. Key resistance is holding at 1.2252 (25/12/2014 high) while strong support lies at 1.0341 (03/01/2017 low).

Technical Outlook: WTI Oil Remains In Red Despite Another Draw In Crude Stocks

Oil price stands in red for the third straight day on Thursday and posted new low at $56.45, where Fibo 76.4% of $55.81/$58.54 upleg was met.

Oil remained under pressure despite EIA report showed stronger than expected draw in US crude stocks, which marks the fourth consecutive fall in oil inventories, as rising output continues to weigh.

Wednesday’s close below $56.91/85 pivots (daily Kijun-sen / Fibo 61.8%) was negative signal, threatening for full retracement of $55.81/$58.54 upleg and extension below $55.81 would generate strong bearish signal.

Bearish 1 & 4-hr studies are supportive for this scenario.

Broken daily Kijun-sen caps today’s action and is expected to keep the upside limited, however, extended upticks should not exceed daily Tenkan-sen ($57.17) to keep near-term bears in play.

Res: 56.91, 57.17, 57.50, 57.81

Sup: 56.45, 55.81, 55.17, 54.77

Market Update – European Session: Major European PMI Manufacturing Continues Robust Run, Norway Central Bank Brings Forward Its 1st...

Notes/Observations

Brexit woes linger for PM May as EU Leaders meet to ratify the 1st phase of negotiations

Major European PMI Manufacturing data beats expectations with both Germany and Euro Zone at record highs

UK Nov retail sales handily beats expectations

Norway Central Bank (Norges) Bank moves up its projection foe the 1st rate hike to autumn 2018 (prior was late 2019)

Asia:

China Nov Industrial Production Y/Y: 6.1% v 6.1%e

China Nov Retail Sales Y/Y: 10.2% v 10.3%e

China Commerce Ministry (MOFCOM): Domestic economy maintaining steady, improving trend; showing greater stability and resilience

China National Bureau of Stats (NBS): economy to continue steady trend in 2018; to push for structural reforms and pursue high quality growth next year

PBoC raised 7-day reverse repo rate by 5bps to 2.50% and rate on 28-day reverse repo by 5bps to 2.80% (move typical following Fed rate hike earlier today)

Japan Dec Preliminary Manufacturing PMI: 54.2 v 53.6 prior

Australia Nov Employment Change: +61.6K v +19.0Ke (14th straight monthly gain); Unemployment Rate:: 5.4% v 5.4%e

Europe:

UK govt lost a vote on EU withdrawal bill amendment by 309-305; House of Commons voted to give lawmakers final say on Brexit deal

German DIHK Chambers of Commerce: Brexit may raise Germany EU cots by €8B/year

Americas:

FOMC hiked rates for the 3rd time in 2017 by another 25bps (as expected) in a 7-2 vote (Evans and Kashkari dissent); dots lowered median forecast for end-2019 rate 2.625% (prior 2.750%) while raising median forecast for end-2020 rate 3.00% (prior 2.875%). GDP outlook raised for both 2019 and 2020; inflation outlook unchanged

Fed Chair Yellen press conference noted that saw pickup in economic growth and business investment, as well as improvement in economies abroad; Gradual rate hikes will be warranted. Fed did discuss tax policy; most of colleagues did put fiscal stimulus into projections

House, Senate leaders reach agreement in principle on tax package; final vote expected next week (as expected)

Economic Data:

(IN) India Nov Wholesale Prices (WPI) Y/Y: 3.9% v 4.0%e (8-month high)

(EU) Nov EU27 New Car Registrations: 5.9% v 5.9% prior

(FI) Finland Nov CPI M/M: 0.2% v 0.0% prior; Y/Y: 0.8% v 0.5% prior

(SE) Sweden Nov PES Unemployment Rate: 3.9% v 3.9% prior

(FR) France Nov Final CPI M/M: 0.1% v 0.1%e; Y/Y: 1.2% v 1.2%e

(FR) France Nov Final CPI EU Harmonized M/M: 0.1% v 0.1%e; Y/Y: 1.2% v 1.3%e

(FR) France Dec Preliminary Manufacturing PMI: 59.3 v 57.2e (15th month of expansion and highest since Sept 2000), Services PMI: 59.4 v 60.0e, Composite PMI: 60.0 v 59.6e

(ES) Spain Nov Final CPI M/M: 0.5% v 0.4%e; Y/Y: 1.7% v 1.6%e

(ES) Spain Nov Final CPI EU Harmonized M/M: 0.3% v 0.3%e; Y/Y:1.8% v 1.7%e

(ES) Spain Nov CPI Core M/M: 0.4% v 0.6% prior; Y/Y: 0.8% v 0.9%e

(PH) Philippines Central Bank (BSP) left its Overnight Borrowing Rate unchanged at 3.00% (as expected)

(ZA) South Africa Q3 Current Account (ZAR): -109B v -90Be, Current Account to GDP Ratio: -2.3% v -2.0%e

(CH) Swiss Nov Producer & Import Prices M/M: 0.6% v 0.5% prior; Y/Y: 1.8% v 1.2% prior

(CH) Swiss National Bank (SNB) ledt its Sight Deposit Interest Rate unchanged at -0.75% and maintained 3-Month Libor Range between -0.25 to -1.25% (both as expected)

(DE) Germany Dec Preliminary Manufacturing PMI: 63.3 v 62.0e (37th month of expansion and a record high); Services PMI: 55.8 v 54.6e, Composite PMI: 58.7 v 57.2e

(SE) Sweden Nov Unemployment Rate: 5.8% v 6.0%e v 6.3% prior, Unemployment Rate (Seasonally Adj): 6.4% v 6.6%e

(HK) Hong Kong Q3 Industrial Production Y/Y: 0.3% v 0.4% prior

(HK) Hong Kong Q3 PPI Y/Y: 3.7% v 3.7% prior

(NO) Norway Central Bank (Norges) left its Deposit Rates unchanged at 0.50% (as expected) but brought forward its 1st planned rate hike

(EU) Euro Zone Dec Preliminary Manufacturing PMI: 60.6 v 59.7e (53rd month of expansion and record high), Services PMI: 56.5 v 56.0e, Composite PMI: 58.0 v 57.2e

(IT) Italy Nov Final CPI M/M: -0.2% v -0.2%e; Y/Y: 0.9% v 0.9%e; CPI Index (ex-tobacco): 100.8 v 100.9e

(IT) Italy Nov Final CPI EU Harmonized M/M: -0.2% v -0.2%e; Y/Y: 1.1% v 1.1%e

(UK) Nov Retail Sales (Ex Auto Fuel) M/M: 1.2% v 0.4%e; Y/Y: 1.5% v 0.2%e

(UK) Nov Retail Sales (Inc Auto Fuel) M/M: 1.1% v 0.4%e; Y/Y: 1.6% v 0.3%e

(ZA) South Africa Nov PPI M/M:0.5% v 0.3%e; Y/Y: 5.1% v 4.9%e

(BR) Brazil Dec FGV Inflation IGP-10 M/M: 0.9% v 0.8%e

(GR) Greece Q3 Unemployment Rate: 20.2% v 21.1% prior

Fixed Income Issuance:

(ES) Spain Debt Agency (Tesoro)sold total €3.07B v €3.0-4.0B indicated range in 2021, 2027 and 2032 bonds

Sold €1.0B in 0.05% Jan 2021 SPGB bond; Avg yield: -0.005% v -0.022% prior, Bid-to-cover: 2.28x v 2.55x prior

Sold €1.18B in 1.45% Oct 2027 SPGB; Avg yield: 1.488% v 1.410% prior; Bid-to-cover: 1.95x v 1.46x prior

Sold €0.89B in 5.75% July 2032 SPGB; Avg Yield: 1.943% v 1.925% prior; Bid-to-cover: 1.56x v 1.47x prior

(IE) Ireland Debt Agency (NTMA) sold €500M vs. €500M indicated in 12-month bills; Avg yield -0.52% v -0.50% prior; Bid-to-cover: 2.95x v 3.4x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.1% at at 390.1, FTSE -0.2% at 7482, DAX -0.3% at 13088, CAC-40 -0.2% at 5388, IBEX-35 +0.1% at 10270, FTSE MIB +0.2% at 22442, SMI -0.1% at 9384 , S&P 500 Futures +0.1%]

Market Focal Points/Key Themes: European Indices trade mixed this morning with the Dax, Cac and FTSE trading lower with Spanish and Italian markets trading slightly higher. In Europe preliminary PMI readings came in stronger once again marking multi year highs, as French Manufacturing PMI records a 17 year high. On the corporate front, shares of Sports retailer Sports Direct trades sharply lower after declining margins and rising debt, while PZ Cussons trades lower after guiding Op profits lower. Ocado reported positive Q4 sales development and Bertrandt trades lower after reporting full year results. On the M&A front Lonmin trades sharply higher after its to be acquired by Sibanye Stillwater; Gemalto rejects Atos €46/shr offer. Looking ahead earnings include Sanderson Farms with Investor days including from Delta and Danaher.

Equities

Consumer Discretionary [ Steinhoff [SNH.ZA] -9.4% (Issues of FY17 results could also be relevant to FY16), Ocado [OCDO.UK] +0.8% (Q4 Sales), Sports Direct [SPD>UK] -7% (Earnings), PZ Cussons [PZC.UK] -5.6% (Earnings), Bertrandt [BDT.DE] -2.5% (Earnings)]

Materials [Lonmin [LMI.UK] +23% (To be acquired)]

Energy [Petrofac [PFC.UK] -1.6% (Earnings)]

Industrials [Saffran [SAF.FR] -2.5%, Dassault Aviation [AM.FR] -2.4% (Termination of Silvercrest contract)]

Speakers

SNB Policy Statement reiterated that negative interest rate and willingness to intervene in the foreign exchange market as necessary remained essential. Reiterated view that CHF currency (franc) remained highly valued. It did take note of the CHF depreciation against the Euro since Sept.

SNB Quarterly Staff projections maintained 2017 GDP growth of just under 1.0%and 2018 GDP growth forecast of ~2.0%. Raised its 2018 CPI forecast from 0.4% to 0.7% while maintaining 2019 CPI at 1.1%

SNB's Jorden post rate decision press conference reiterated that CHF currency (Franc) was still 'highly valued. Reiterated view that ultra-loose monetary policy was still needed despite the recent decline of the Swiss franc showing that safe haven currencies were currently less in demand. Major policy normalization presented a challenge; long term pressure had not increased

Norway Central bank (Norges) Policy Statement noted that the decision to keep policy steady was unanimous. Key policy rate was forecasted to remain at 0.5% in period to autumn 2018, followed by gradual increase (**Note: the prior rate path indicated a first hike in late 2019). Outlook suggested that inflation to remain below 2.5% in coming years. Uncertainty surrounding effects of monetary policy suggested a cautious approach to interest rate setting. Upturn in domestic economy was continuing, output gap appeared somewhat narrower than projected

Norway Central bank (Norges) Gov Olsen post rate decision press conference noted that it still needed expansionary monetary policy. Would be cautious ahead when raising interest rates

BrexitMin Davis: No deal Brexit is massively less probable

France Debt Agency (AFT) commented on 2018 issuance: Sees financing requirement of €202.7B. To sell €195B in medium and long term debt in 2018

Swiss KOF Institute Winter Economic Forecast raised 2018 GDP growth from 2.2% to 2.3% and set 2019 GDP at 1.7%. Raised 2018 inflation from 0.4% to 0.5% and maintained 2019 inflation at 0.5%

Russia President Putin Annual address noted that he was seeking new term to continue previous priorities

Philippines Central Bank stated that the current monetary policy setting should be kept but to be vigilant on any CPI risks. BSP to to adjust policy as needed and saw no need to stimulate economic activities

IEA Monthly Report maintained its 2017 global oil demand growth forecast at 1.5M bpd and 2018 global oil demand growth forecast at 1.3M bpd. Current outlook 2018 might not necessarily be a happy New Year for those who would like to see a tighter market

Currencies

USD began the EU session on a softer tone in the aftermath of the FOMC rate decision viewed as a Dovish Fed hike.. Dealers noted that the greenback softened as the Fed dots basically stuck to its rate projections. Market seem to keep challenging the Fed's ability and willingness to get inflation to 2%

A hawkish statement by the Norway Central Bank sent the EUR/NOK pair lower as Norges brought forward its plans for the potential 1st rate hike into autumn 2018. Some analysts now target EUR/NOK at 9.65 as a results of the change in language.

Australia's job market was red hot as the Employment Change rose for the 14th straight month.

Fixed Income

Bund futures trade 163.09 down 36 ticks, following a record high in German manufacturing PMI. Continued upside sees 163.63 then 164.25. A reversal targets 162.50 then 162.38.

Gilt futures trade at 125.69 down 15 ticks with a limited reaction from the strong UK retail sales beat. Continued upside eyeing 126.15 then 126.65. Downside targets include 125.24 then 124.75.

Thursday's liquidity report showed Wednesday's use of the marginal lending facility rose to €633M from €188M prior.

Corporate issuance saw no deals priced in primary market. Primary expected to close for the year after this week.

Looking Ahead

(EU) European Union Leaders begin 2-day Summit in Brussels

(ID) Preview: Indonesia Central Bank (BI) Interest Rate Decision expected in session (no set time); Expected to leave 7-Day Reverse Repo Rate unchanged at 4.25%

05:30 (HU) Hungary Debt Agency (AKK) to sell in 12-month Bills 30th 2017)

05:30 (HU) Hungary Debt Agency (AKK) to sell in Floating Rate Bonds

06:00 (IL) Israel Q3 Current Account: No est v $2.4B prior

06:00 (PT) Portugal Nov CPI M/M: No est v 0.3% prior; Y/Y: No est v 1.4% prior

06:00 (PT) Portugal Nov CPI EU Harmonized M/M: No est v 0.5% prior; Y/Y: 2.1%e v 1.9% prior

06:00 (IE) Ireland Nov CPI M/M: No est v -0.1% prior; Y/Y: No est v 0.6% prior

06:00 (IE) Ireland Nov CPI EU Harmonized M/M: No est v -0.1% prior; Y/Y: 0.6%e v 0.5% prior

06:00 (TR) Turkey Central Bank (CBRT) Interest Rate Decision: Expected to leave Benchmark Repurchase Rate unchanged at 8.00% (to hike Late Liquidity Window by 100bps to 13.25%)

06:45 (US) Daily Libor Fixing

07:00 (UK) Bank of England (BOE) Interest Rate Decision: Expected to leave Interest Rates unchanged at 0.50%

07:00 (UR) Ukraine Central Bank Interest Rate Decision: Expected to leave Key Rate unchanged at 13.50%

07:45 (EU) European Central Bank (ECB) Interest Rate Decision: Expected to leave Main Refinancing Rate unchanged at 0.00%

08:00 (PL) Poland Oct Current Account: +€0.2Be v -€0.1B prior; Trade Balance: €0.5Be v €0.8B prior; Exports: €18.1Be v €17.2B prior; Imports: €17.4Be v €16.4B prior

08:00 (RU) Russia Gold and Forex Reserve w/e Dec 8th: No est v $430.6B prior

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Nov Advance Retail Sales M/M: 0.3%e v 0.2% prior; Retail Sales Ex Auto M/M: 0.6%e v 0.1% prior, Retail Sales Ex Auto and Gas: 0.4%e v 0.3% prior, Retail Sales Control Group: 0.4%e v 0.3% prior

08:30 (US) Nov Import Price Index M/M: 0.1%e v 0.2% prior; Y/Y: 3.2%e v 2.5% prior

08:30 (US) Nov Export Price Index M/M: 0.3%e v 0.0% prior; Y/Y: No est v 2.7% prior, Import Price Index ex Petroleum M/M: No est v 0.1% prior

08:30 (US) Initial Jobless Claims: 236Ke v 236K prior; Continuing Claims: 1.90Me v 1.908M prior

08:30 (CA) Canada Oct New Housing Price Index M/M: 0.2%e v 0.2% prior; Y/Y: No est v 3.8% prior - 08:30 (US) Weekly USDA Net Export Sales

09:00 (CA) Canada Nov Existing Home Sales M/M: No est v 0.9% prior

09:00 (BR) Brazil to sell 2018, 2019 and 2021 LTN bills - 09:00 (BR) Brazil to sell Fixed Rate 2023 and 2027 Bonds

09:45 (US) Dec Preliminary Markit Manufacturing PMI: 53.9e v 53.9 prior; PMI Services: 54.7e v 54.5 prior; PMI Composite: No est v 54.5 prior

10:00 (US) Oct Business Inventories: -0.1%e v 0.0% prior

10:30 (US) Weekly EIA Natural Gas Inventories

12:00 (IS) Iceland Nov International Reserves (ISK): No est v 680B prior

12:00 (CA) Canada to sell 2-Year Bonds

14:00 (MX) Mexico Central Bank (Banxico) Interest Rate Decision: Expected to raise the Overnight Rate by 25bps to 7.25%

15:00 (CO) Colombia Central Bank Interest Rate Decision: Expected to leave Overnight Lending Rate unchanged at 4.75%

16:00 (CL) Chile Central Bank (BCCh) Interest Rate Decision: Expected to leave Overnight Target Rate unchanged at 2.50%

16:30 (NZ) New Zealand Nov Business Manufacturing PMI: No est v 57.2 prior

18:00 (PE) Peru Central Bank (BCRP) Interest Rate Decision: Expected to leave Reference Rate unchanged at 3.25%

USD Loses Ground Despite Fed Rate Hike, CBRT, BoE And ECB Eyed

Busy day for central banks but little action expected

The Federal Reserve opened the ball yesterday by raising borrowing costs. The central banks’ show will continue today with the SNB, Norges Bank, CBRT and ECB. As widely expected the Swiss National Bank didn’t change anything to its monetary policy set-up. Similarly, the Norges Bank left unchanged the key rate at 0.50%. However, the Norwegian central bank signalled it would start hiking rate in autumn 2018. The krone surge 1.20% against the US dollar with USD/NOK sliding to 8.2265. EUR/NOK fell 1.30% to 9.72.

In Turkey, the CBRT should leave unchanged its three key interest rate. However, the market expect that the central bank will increase the late liquidity lending rate by 1% to 13.25%, therefore charging Turkish banks more if they need to borrow just before the market close. Due to political interferences from the government, the central bank found another way to relieve the pressure on the TRY. The CBRT has the option not to provide any funding through its 1-week repurchase auction to local lenders, forcing them to borrow at a much higher rate through the late liquidity window.

In Europe, both the ECB and the BoE are holding their last meeting of the year. Given the fact that the former already trim by half its quantitative easing program back in October, Mario Draghi will most likely set back and relax. The situation is roughly the same the BoE as the central bank already increased borrowing costs back in November. Therefore, we expect little action as both central banks will not miss the opportunity to reiterate their cautious rhetoric regarding the inflation and growth outlook.

Fed raises rates for the third time this year.

As expected the Fed ends up its year by increasing rates to the window 1.25% - 1.50%. It is finally the third time in the year that the US Central Bank increases rates. According to the monetary policy statement, expectations on the job market are strong with unemployment rate should drop below 4% in 2018. On top of that Fed forecast the growth to increase by 2.1% in 2018.

Now the Fed is on the line for another set of three rate hikes in 2018 which is something that was already predicted since last September. The pace of the rate hikes won’t accelerate from this year and as we mentioned several times in this newsletter, there is no reason for the Fed to do so as it would increase the pace of the rate hikes and it would likely create potentially massive disruption on many markets. We rather believe that the Fed will not be able to raise rates three times.

The only reason why the Fed promises so much rate hikes are the confidence they are trying to maintain in the dollar. The truth is that the Fed is not really on control of all the asset bubbles.

The keywords from the Fed are “low inflation” while we believe that inflation is actually higher than what the Fed is using for deciding about the monetary policy (3% versus 2% in our view).

The Fed clearly needs stronger inflation to kill the debt without raising rates that would burst bubbles. There are bubbles in almost every US asset class now. As a result our view for next year is bullish on the Eurodollar while the dollar may still enjoy a Christmas Rally until year-end on the fact that the “2017 Fed mission is accomplished”.

SNB Raised CPI Forecasts, Acknowledged Franc’s Weakness But Pledged To Stay Cautious

While leaving the policy rates unchanged for another month and pledged to continue FX market intervention when needed, the SNB has turned less dovish in December. It has turned more upbeat over the economic recovery outlook and acknowledged the depreciation of Swiss franc and the euro and US dollar. the central bank revised modestly higher the inflation forecasts for this year and 2018, while leaving that for 2019 unchanged.

As widely anticipated, the SNB kept the sight deposit rate unchanged at -0.75%, while the target range for the three-month Libor stayed at between –1.25% and –0.25%. Again, the SNB reiterated that it would 'remain active in the foreign exchange market as necessary', while 'taking the overall currency situation into consideration'.

Regarding the 'currency situation', Swiss franc has continued to weaken against both the euro and the greenback during the intermeeting period. Over the past three months, EURCHF has gained +1.7% while USDCHF has been up about +2.3%. as such, SNB has revised its language on exchange rate to 'the Swiss franc has weakened further against the euro and, more recently, has also depreciated against the US dollar'. While acknowledging that the franc's overvaluation has 'continued to decrease', the central bank reaffirmed that it remained 'highly valued'. Policymakers attributed the recent weakness in the franc to diminished demand over safe haven assets, while cautioning over the 'fragile' developments. The central bank remained vigilant over franc's movement, noting that 'a renewed appreciation would still be a threat to price and economic developments'.

Another adjustment this month is the upward revision in the inflation forecasts. Owing to 'increased oil prices and the further weakening of the Swiss franc', the staff estimated that inflation would rise to + 0.5% this year, up from +0.4% projected in September. Inflation would then increase to +0.7% in 2018 (+0.4% previously) and then to +1.1% in 2019 (unchanged). The longer-term inflation forecast is virtually unchanged. GDP growth is expected to reach +2.5% next year.

Despite SNB's cautiousness over the franc's movement, we notice that it has adopted less intervention in recent months. As we mentioned in our report last week, the decline of FX reserve to 738.17B franc in November and the fall of sight deposit in the week ended December 1 are evidence that the central bank has found it less urgent to intervene the FX market. Obviously, this has been driven by the weakness of Swiss franc. It is likely that the central bank would maintain the status quo and the same rhetoric in 2018

Elliott Wave Analysis: USDJPY And USDCAD

USDJPY is showing evidences of a weaker buck ahead, as pair turned nicely down yesterday through a 110.83-111.98 trendline support which means that recovery can be finished and that market is underway to lower levels. 112.00 is our first objective on the way down.

USDJPY, 1h

The only pair that can be interesting for strong USD once overall dollar weakness slows down, is USDCAD, where we see five waves up from December low so current pullback is a correction that can be looking for a base tomorrow or next week around 1.2730.

USDCAD, 1h

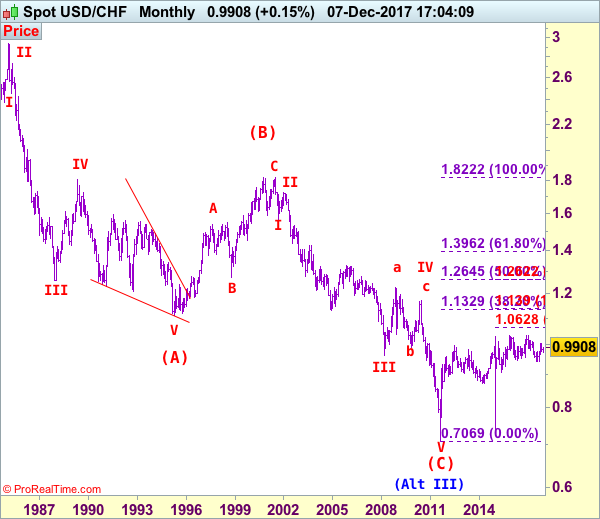

USD/CHF Elliott Wave Analysis

USD/CHF – 0.9888

Although the greenback retreated after meeting resistance at 0.9978, as the strong rebound from 0.9735 signals correction from 1.0039 has ended there, reckon downside would be limited to 0.9800-10 and bring another rise later, above said resistance at 0.9978 would add credence to this view, bring further gain to 1.0000, break there would confirm upmove has resumed for retest of 1.0039. Looking ahead, a break of 1.0039 would confirm early upmove from 0.9421 low has resumed and extend headway to previous resistance at 1.0100.

Our preferred count on the daily chart is that early selloff to 0.9630 is an end of the larger degree wave III and major correction is unfolding from there with a leg ended at 1.2298 (Nov 2008 with (a): 1.0625, (b):1.0011 and (c):1.2298), wave b ended at 0.9910 with (a): 1.0370, (b): 1.1967, (c): 0.9910. The rise from there to 1.1730 is the wave c which also marked the end of wave IV and wave V has possibly ended at 0.7068.

On the downside, expect pullback to be limited to 0.9830-35 and 0.9800 should hold, bring another rise later. Only below said support at 0.9735 would abort and signal the corrective fall from 1.0039 top is still in progress and may extend weakness to 0.9705 support, then towards 0.9640-45 but reckon previous support at 0.9589 would hold from here, bring rebound later.

Recommendation: Hold long entered at 0.9850 for 1.0050 with stop below 0.9750.

Dollar's long-term downtrend started from 2.9343 (Feb 1995) and it was unfolding as a (A)-(B)-(C) with (A): 1.1100, (B): 1.8310 (26 Oct 2000), then followed by another impulsive wave (C) with wave III ended at 0.9630 (Mar 2008). Under this count, correction in wave IV has possibly ended at 1.1730 and wave V already broke below support at 0.9630 and met indicated downside target at 0.7500 and 0.7400. The reversal from 0.7068 suggests the wave V has possibly ended and the breach of resistance at 0.9595 add credence to this view and indicated upside target at 1.0000 had been met, however, the sharp retreat from 1.0296 to 0.7401 suggests choppy trading would be seen but price should stay above said record low at 0.7068.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

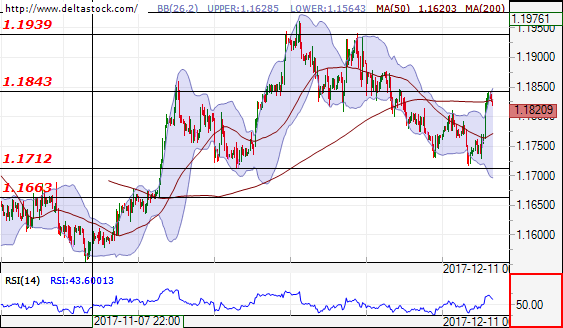

EUR/USD

Current level - 1.1820

The outlook is negative after the unsuccessful breakthrough of the resistance level at 1.1843 for test of the support level at 1.1712. In positive direction a breakthrough of the resistance level at 1.1843, might lead to the next resistance level at 1.1939.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1843 | 1.1939 | 1.1712 | 1.1690 |

| 1.1939 | 1.2090 | 1.1712 | 1.1550 |

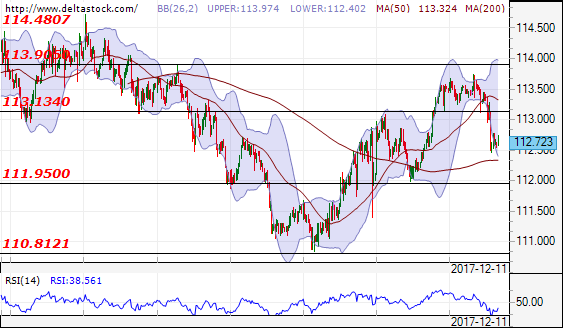

USD/JPY

Current level - 112.72

The forecast is negative for test of the support level at 111.95 and after that at 110.81. In positive direction only a breakthrough of the resistance level at 114.00 might lead to increase of the price.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 113.13 | 113.90 | 111.90 | 109.50 |

| 113.90 | 114.50 | 110.80 | 107.30 |

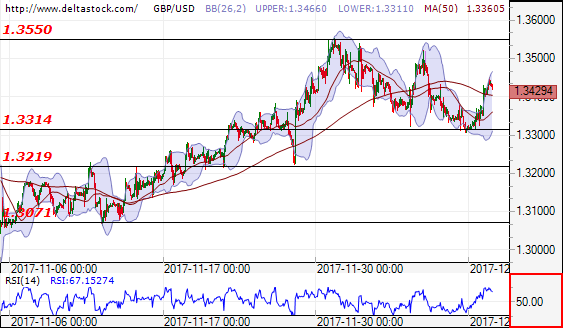

GBP/USD

Current level - 1.3429

The outlook is positive for test of the resistance level at 1.3550. In negative direction a breakthrough of the support level at 1.3314, might lead to another decrease and test of the next support at 1.3200.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3550 | 1.3660 | 1.3310 | 1.3220 |

| 1.3550 | 1.3660 | 1.3220 | 1.3070 |