Sample Category Title

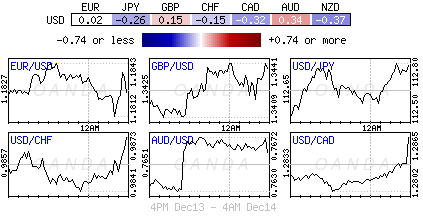

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1759; (P) 1.1795 (R1) 1.1861; More....

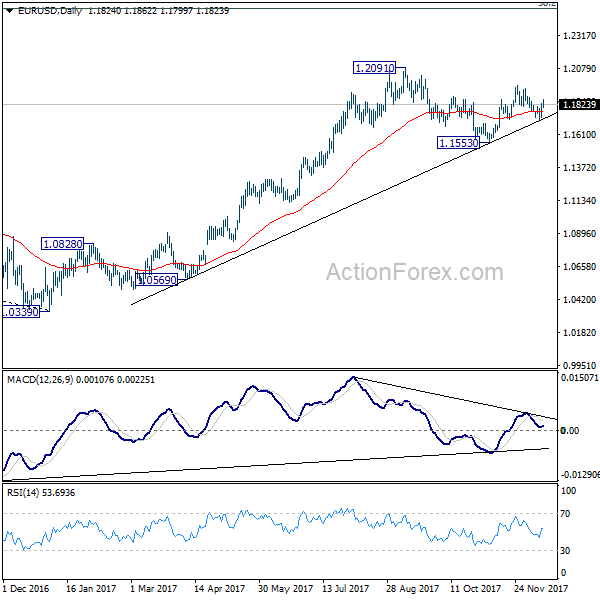

Intraday bias in EUR/USD remains on the upside for the moment. Corrective pull back from 1.1960 has completed at 1.1717 already. Also, as the pair defended 1.1712 cluster support (61.8% retracement of 1.1553 to 1.1960 at 1.1708), near term bullish outlook is retained. Further rise should be seen to 1.1960 first. Break will target 1.2029 high next. And even in case of retreat, outlook will remain bullish as long as 1.1708/12 cluster support holds.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1423) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

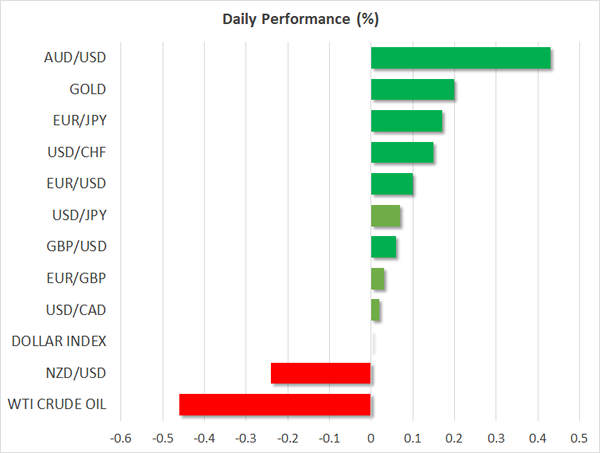

Dollar Borrows Support from Ultra-Low Jobless Claims and Strong Retail Sales, Euro Firm as ECB Upgraded Growth and Inflation...

Dollar is trying to regain some ground in early US session after ultra-low jobless claims and strong retail sales. Indeed, at the time of writing, the greenback is trading up against all but Aussie for today. Nonetheless, after yesterday's post CPI and FOMC selloff, Dollar has to do more to convince the markets of its momentum. Meanwhile, Euro is actually trading as the strongest one today, trailing Dollar closely. The common currency is lifted by strong Eurozone PMIs. ECB also raised growth and 2019 inflation forecasts in the latest projections. Elsewhere, BoE and SNB stand pat as widely expected.

US jobless claims at 225k ultralow

US initial jobless claims dropped -11k to 225k in the week ended December 9, well below expectation of 239k. Four week moving average dropped 6.75k to to 234.75k. Continuing claims dropped to 1.89m in the week ended December 1. Headline retail sales rose 0.8% mom in November, well above expectation of 0.3% mom. Ex-auto sales grew 1.0% mom, also beat expectation of 0.7% mom. Import price index rose 0.7% mom in November. Also released in US session, Canada new housing price index rose 0.1% mom in October.

We'd maintain that yesterday's FOMC announcement was not dovish at all. Growth forecasts were revised higher, unemployment forecasts revised lower. Inflation forecasts and fed funds rate projections were unchanged. The only dovish part of the voting with Chicago Fed Evans joining Minneapolis Kashkari in dissenting. That's it. Dollar's selloff was largely due to a combination of factors. That includes Republican's defeat in deep red state of Alabama Senate Election, possibly dissatisfaction on the final corporate tax rate at 21%. But more importantly, the core CPI miss. More in FOMC Hikes Rate For Third Time, With Two Dissents

ECB stands pat, raised 2018 inflation forecast

ECB left the main refinancing rate unchanged at 0% as widely expected. The central bank also maintained the pledge to keep rates low for an extend period and be open to add stimulus if needed. ECB President Mario Draghi emphasized in the press conference that very favorable financial conditions are still needed in Eurozone. Also price pressure remained low and there was no sign of a pick up yet. Nonetheless, strong Eurozone growth momentum and improved growth outlook gave ECB confidence that inflation will climb back to 2% target.

In the updated economic forecasts, ECB project 2017 growth to be at 2.4%, revised up from 2.2%. For 2019, growth is seen at 1.9%, revised from from 1.7%. 2020 growth forecast was left unchanged at 1.7%. Inflation is projected to be at 1.5% in 2017, unchanged. 2018 inflation is estimated to be at 1.4%, notably revised up from 1.2%. 2019 inflation is projected to be at 1.5%, unchanged. 2020 inflation is projected to be at 1.7%. That is, within the projection horizon, ECB is still short of its 2% inflation target.

Solid Eurozone PMIs suggests strong Q4, and firm Q1.

PMIs from Eurozone generally strengthened in December, painting a brighter outlook for early next 2018. Eurozone PMI manufacturing rose to 60.6 in December, up from 60.1 and beat expectation of 59.7. That's also the highest level on record. Eurozone PMI services rose to 56.5, up from 56.2 and beat expectation of 56.0. Germany PMI manufacturing rose to 63.3, up from 62.5, above expectation of 62.0. Germany PMI services rose to 55.8, up from 54.3, above expectation of 54.6. France PMI manufacturing rose to 59.3, up from 57.7, above expectation of 57.2. France PMI services, however, dropped to 59.4, down from 60.4, missing expectation of 59.4.

Markit chief business economist Chris Williamson noted that "the eurozone economy is picking up further momentum as the year comes to a close, ending its best quarter since the start of 2011. The PMI is signalling an impressive 0.8% GDP increase in the fourth quarter, with accelerating growth seen in both Germany and France, where fourth quarter growth rates of 1.0% and 0.7-0.8% are indicated respectively."

Also, he added that "The eurozone upturn is being led by a booming manufacturing sector, with a record PMI seen in December, but stronger domestic demand is also helping drive faster service sector growth. Demand in the region's home markets is being buoyed by the improved labour market, with new jobs being created at a pace not seen for 17 years over the past two months."

BoE blames inflation overshoot on exchange rate

The BOE voted unanimously to leave the Bank rate unchanged at 0.5% today, following a historic rate hike in the prior month. Policymakers also decided to leave the asset purchase program unchanged at 435B pound. Overshooting of inflation remains a key concern with the central bank putting its blame on British pound's weakness. Policymakers noted that recent macroeconomic data have been "mixed" and raised the concern that GDP growth might slow in 4Q17. The central bank also acknowledged the progress of Brexit negotiations, suggesting that it has helped support the pound. We expect the BOE would keep its powder dry at least for the first half of next year, unless abrupt changes in the growth and inflation developments. More in BOE Stands on Sideline after November Hike, Attributing Inflation Overshoot to Weak Currency

SNB turned upbeat after standing pat

While leaving the policy rates unchanged for another month and pledged to continue FX market intervention when needed, the SNB has turned less dovish in today's announcement. It has turned more upbeat over the economic recovery outlook and acknowledged the depreciation of Swiss franc and the euro and US dollar. the central bank revised modestly higher the inflation forecasts for this year and 2018, while leaving that for 2019 unchanged. More in SNB Raised CPI Forecasts, Acknowledged Franc's Weakness But Pledged To Stay Cautious

Also from Swiss, PPI rose 0.6% mom, 1.8% yoy in November.

Aussie surges on stunning job data

Australian Dollar remains the strongest one for today as supported by strong job data. The employment market grew 61.6k in November, more than triple of expectation of 19.2k. Full time jobs grew 41.9k while part time jobs grew 19.7k. Unemployment rate was unchanged at 5.4% as participation rate jumped from 65.2% to 65.5%. Nonetheless, there is no change in the general view that RBA will stand pat throughout 2018, unless there is a pickup in wage growth. Also from Australia consumer inflation expectation rose 3.7% in December.

Release from China, retail sales rose 10.2% yoy in November, below expectation of 10.3% yoy. Fixed assets investments rose 7.2% yoy, in line with consensus, industrial production rose 6.1% yoy, below expectation of 6.2% yoy. From Japan, industrial production was finalized at 0.50% mom in October.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1759; (P) 1.1795 (R1) 1.1861; More....

Intraday bias in EUR/USD remains on the upside for the moment. Corrective pull back from 1.1960 has completed at 1.1717 already. Also, as the pair defended 1.1712 cluster support (61.8% retracement of 1.1553 to 1.1960 at 1.1708), near term bullish outlook is retained. Further rise should be seen to 1.1960 first. Break will target 1.2029 high next. And even in case of retreat, outlook will remain bullish as long as 1.1708/12 cluster support holds.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1423) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

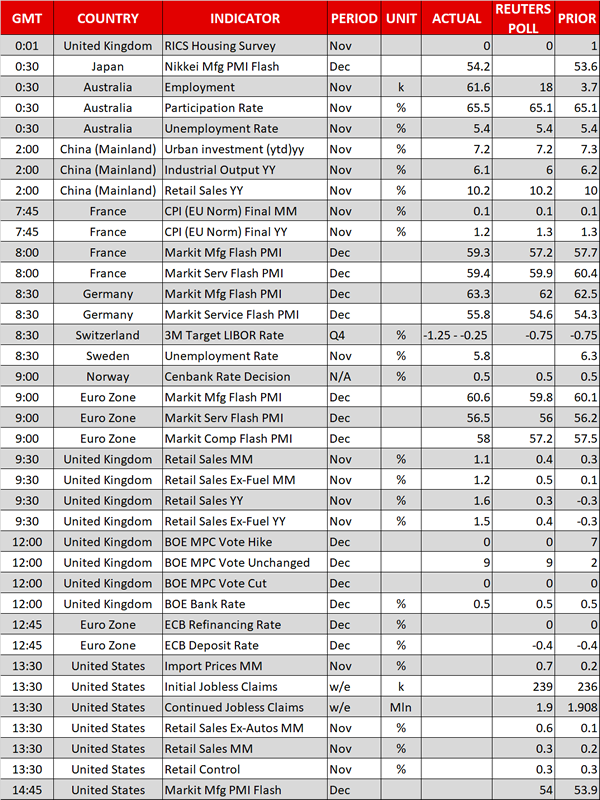

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectation Dec | 3.70% | 3.70% | ||

| 00:01 | GBP | RICS House Price Balance Nov | 0% | 0% | 1% | |

| 00:30 | AUD | Employment Change Nov | 61.6K | 19.2K | 3.7K | 7.8K |

| 00:30 | AUD | Unemployment Rate Nov | 5.40% | 5.40% | 5.40% | |

| 02:00 | CNY | Retail Sales Y/Y Nov | 10.20% | 10.30% | 10.00% | |

| 02:00 | CNY | Fixed Assets Ex Rural YTD Y/Y Nov | 7.20% | 7.20% | 7.30% | |

| 02:00 | CNY | Industrial Production Y/Y Nov | 6.10% | 6.20% | 6.20% | |

| 04:30 | JPY | Industrial Production M/M Oct F | 0.50% | 0.50% | 0.50% | |

| 08:00 | EUR | France Manufacturing PMI Dec P | 59.3 | 57.2 | 57.7 | |

| 08:00 | EUR | France Services PMI Dec P | 59.4 | 59.9 | 60.4 | |

| 08:15 | CHF | Producer & Import Prices M/M Nov | 0.60% | 0.30% | 0.50% | |

| 08:15 | CHF | Producer & Import Prices Y/Y Nov | 1.80% | 1.20% | ||

| 08:30 | CHF | SNB Sight Deposit Interest Rate | -0.75% | -0.75% | -0.75% | |

| 08:30 | CHF | SNB 3-Month Libor Upper Target Range | -0.25% | -0.25% | -0.25% | |

| 08:30 | CHF | SNB 3-Month Libor Lower Target Range | -1.25% | -1.25% | -1.25% | |

| 08:30 | EUR | Germany Manufacturing PMI Dec P | 63.3 | 62 | 62.5 | |

| 08:30 | EUR | Germany Services PMI Dec P | 55.8 | 54.6 | 54.3 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Dec P | 60.6 | 59.7 | 60.1 | |

| 09:00 | EUR | Eurozone Services PMI Dec P | 56.5 | 56 | 56.2 | |

| 09:30 | GBP | Retail Sales M/M Nov | 1.10% | 0.40% | 0.30% | |

| 12:00 | GBP | BoE Bank Rate | 0.50% | 0.50% | 0.50% | |

| 12:00 | GBP | BOE Asset Purchase Target Dec | 435B | 435B | 435B | |

| 12:00 | GBP | MPC Official Bank Rate Votes | 0--0--9 | 0--0--9 | 7--0--2 | |

| 12:00 | GBP | MPC Asset Purchase Facility Votes | 0--0--9 | 0--0--9 | 0--0--9 | |

| 12:45 | EUR | ECB Rate Decision | 0.00% | 0.00% | 0.00% | |

| 13:30 | EUR | ECB Press Conference | ||||

| 13:30 | CAD | New Housing Price Index M/M Oct | 0.10% | 0.20% | 0.20% | |

| 13:30 | USD | Initial Jobless Claims (DEC 09) | 225K | 239K | 236K | |

| 13:30 | USD | Retail Sales Advance M/M Nov | 0.80% | 0.30% | 0.20% | 0.50% |

| 13:30 | USD | Retail Sales Ex Auto M/M Nov | 1.00% | 0.70% | 0.10% | 0.40% |

| 13:30 | USD | Import Price Index M/M Nov | 0.70% | 0.80% | 0.20% | |

| 14:45 | USD | US Manufacturing PMI Dec P | 54.2 | 53.9 | ||

| 14:45 | USD | US Services PMI Dec P | 54.6 | 54.5 | ||

| 15:00 | USD | Business Inventories Oct | -0.10% | 0.00% | ||

| 15:30 | USD | Natural Gas Storage | 2B |

BoE Keeps Rates Unchanged, Draghi in Focus

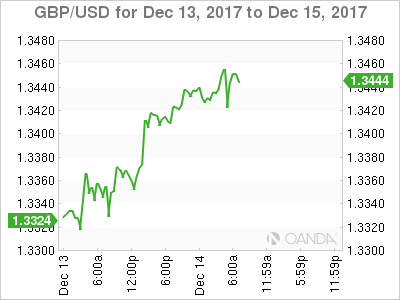

Sterling offered a fairly muted response during Thursday's trading session after Bank of England policy makers unanimously voted to leave interest rates unchanged at 0.5% in December.

Although inflation in the United Kingdom has jumped to its highest level in almost six years, it seems that the growing uncertainty over Brexit is likely to encourage the central bank to adopt a wait and see approach moving forward. While the Monetary Policy Committee maintained the view that "further modest increases" in the key rate may be needed in the coming years, Sterling's muted price action suggests this has fallen on deaf ears.

The GBPUSD appreciated during Thursday's trading session on the back of a vulnerable US Dollar. With political risk in the United Kingdom and Brexit uncertainty still weighing on the Pound, the current upside may be limited. Technical traders will continue to observe how prices react below the 1.3520 region. Weakness under 1.3380 could encourage a decline back towards 1.3300.

ECB's Mario Draghi enters the scene

The Euro edged higher on Thursday after the European Central Bank kept rates on hold in December.

With the central bank halving its monthly asset purchases back in October to €30 billion from €60 billion, it was widely expected that monetary policy would remain unchanged today. Much attention will be directed towards Mario Draghi's press conference which could heavily impact the Euro. Although Europe's steadily improving macro fundamentals could continue stimulating buying sentiment towards the Euro, a cautious sounding Draghi today, has the ability to punish the currency.

Dollar dips on dovish hike

It is interesting how the Dollar sharply depreciated against a basket of major currencies during late trading on Wednesday, despite the Federal Reserve raising US interest rates by 25 basis points.

Although the central bank expressed optimism over the US economy by projecting GDP to grow 2.5% in 2018 from the 2.1% forecast in September, this simply failed to offer any support to the Dollar. With policymakers expressing concerns over stubbornly low levels of inflation, investors are likely to deeply ponder how this could impact the central bank's ability to raise US interest rates three times in 2018.

Taking a look at the technical picture, the Dollar Index was under extreme selling pressure on the daily charts following December's dovish rate hike. Sustained weakness below 93.50 may encourage a further decline lower towards 93.20 and 90.00, respectively.

Commodity spotlight - Gold

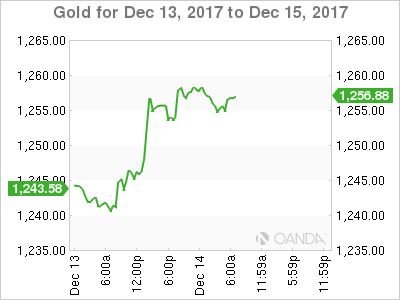

Gold sprinted to a weekly high above $1258 during Thursday's trading session on the back of a vulnerable US Dollar.

Although the Federal Reserve raised US interest rates on Wednesday as widely expected, concerns over low inflation in the US stole the show ultimately punishing the Greenback. With markets questioning the central bank's ability to raise rates three times next year amid inflation fears, Gold which is zero-yielding may receive further support.

From a technical standpoint, the yellow metal still remains somewhat pressured on the daily charts despite Wednesday's impressive resurgence. A technical bounce is in the process with the next level of interest at $1267. Alternatively, a failure of prices to keep above $1250 may trigger a decline back towards $1230.

Is Bitcoin gearing up for another record?

This has been one of those rare trading weeks where Bitcoin bulls have taken the back seat with the cryptocurrency currently ranging below the $17000 region as of writing.

With the market chatter over Bitcoin intensifying by the day and investors still rushing from all directions to acquire a piece of the crypto pie, bulls have much ammunition to attack again next week. Technical traders will continue to closely observe how prices behave with the current range with a weekly close above $17000 opening the gates to further upside.

2017 has been an incredibly bullish and phenomenal trading year for Bitcoin which has appreciated roughly 1500% YTD which is mouth-watering to any investor. $20000 is already in sight and it will be interesting to see if Bitcoin is able to maintain the upside momentum next year.

BOE Stands on Sideline after November Hike, Attributing Inflation Overshoot to Weak Currency

The BOE voted unanimously to leave the Bank rate unchanged at 0.5% in December, following a historic rate hike in the prior month. Policymakers also decided to leave the asset purchase program unchanged at 435B pound. Overshooting of inflation remains a key concern with the central bank putting its blame on British pound's weakness. Policymakers noted that recent macroeconomic data have been "mixed" and raised the concern that GDP growth might slow in 4Q17. The central bank also acknowledged the progress of Brexit negotiations, suggesting that it has helped support the pound. We expect the BOE would keep its powder dry at least for the first half of next year, unless abrupt changes in the growth and inflation developments.

Weak Sterling Pushes Inflation Higher:

UK's inflation continues to surprise to the upside in November. Headline CPI rose to +3.1% y/y in November, compared expectations of and October's +3%. Core CPI steadied at +2.7%. Policymakers attributed the overshooting of inflation above the +2% target to the weak sterling. As noted in the statement, "it remains the case that inflation has been pushed above the target by the boost to import prices that resulted from the past depreciation of sterling". In the medium term, policymakers believed that inflation would "decline towards the 2% target", as it is approaching the peak now.

Policymakers noted that "the recent news in the macroeconomic data has been mixed and relatively limited". While global growth has remained strong, the economy at home might be easing. The central bank noted that GDP growth in the fourth quarter might be slightly softer than the third quarter. They, however, indicated that "the measures announced in the Autumn Budget will lessen the drag on aggregate demand stemming from fiscal consolidation, relative to previous plans".

Brexit Progress

BOE also acknowledged the progress of the Brexit negotiations, suggesting the latest developments have reduced the chance of a "disorderly exit". They are also likely "to support household and corporate confidence". What the BOE did not mention was the defeat of Theresa May's government in the House of Commons as MPs supported an amendment to her Brexit bill with a 309-305 vote, curbing the powers of the government in the bill. On the EU side, the European Parliament has voted 556-62 to determine that "sufficient progress" has been made on the first phase of Brexit talks and to support a move to the next phase.

Pound Slips After BOE Meeting, Stocks Weaker, ECB Rate Decision Ahead

Here are the latest developments in global markets:

FOREX: The pound hit a one-month high at $1.3463 in the wake of better than expected retail sales in November. However, it soon slipped back to 1.3420 after the BOE held rates steady but signaled that GDP growth in Q4 “might be slightly softer than in Q3”. The euro rebounded to $1.1830 finding support from upbeat preliminary manufacturing PMI readings for the month of December, while versus the pound it inched up to 0.8812. The dollar continued ranging near yesterday’s lows against its major peers, while it reached intra-day highs versus the swissie at 0.9892 (+0.23%) after the SNB maintained its loose monetary policy to mitigate risks arising from an appreciated currency. The aussie consolidated gains from upbeat employment data above 0.76 key level (+0.37%) and the kiwi stretched lower to (-0.34%).

STOCKS: European stocks were in the red with tech shares being the worst performers, while bank stocks also retreated after yesterday’s not-so-hawkish comments by the Fed Chair. The benchmark STOXX 600 was down by 0.35% at 1100 GMT, the German DAX 30 fell by 0.40% and the French CAC 40 declined by 0.47%. The British FTSE 100 slipped by 0.25%.

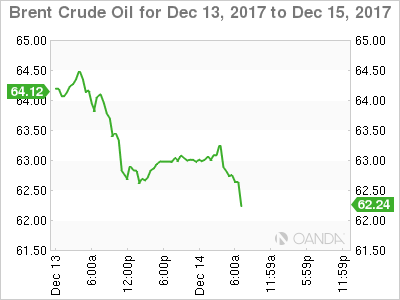

COMMODITIES: Oil prices tumbled after the International Energy Agency raised its US output growth forecasts for 2018, fueling concerns from rising US supply. WTI crude declined by 0.25% to $56.40 per barrel and Brent fell by 0.43% to $62.17. Gold was flat near one-week highs at $1,255.70 per ounce.

Day ahead: ECB policy decision pending; US data in focus

Looking forward, the European Central Bank is anticipated to keep its main refinancing rate unchanged at 0.0% (1245 GMT) respectively. However, as this is widely expected, the focus will turn on future economic projections. ECB policymakers are expected to revise up growth forecasts and give the initial estimates for 2020. The outlook for inflation however, would be of greater importance to determine the path of future interest rates given that inflation in the Eurozone has stuck below the ECB’s goal.

Moreover, following the rates decision, ECB chief Mario Draghi will hold a press conference at 1330 GMT.

On the data front, US retail sales due at 1330 GMT are forecast to rise moderately by 0.1 percentage points to 0.3% m/m in November. Meanwhile, the US labour department is also expected to report a soft increase in initial jobless claims, with analysts projecting the number of people claiming unemployment benefits to rise by 3,000 to 239,000 in the week ending December 8.

Then at 1445 GMT, IHS Markit will publish its preliminary readings on the US manufacturing and services PMI for the month of December. Both indices are said to show some improvement.

Elsewhere, the Bank of Canada’s chief Stephen Poloz will give a speech at the Canadian Club of Toronto at 1740 GMT. A press conference will follow.

DAX Slips Despite Sharp German Mfg. Report, Investors Await ECB Decision

The DAX index has posted losses in the Thursday session. Currently, the DAX is at 13,057.00, down 0.57% on the day. On the release front, manufacturing indicators continue to climb, as German and Eurozone Manufacturing PMIs improved to 63.3 and 60.6 points, respectively. There was more good news from the services sector, as Germany and Eurozone Services PMI both beat their estimates. Later in the day, the ECB is expected to maintain interest rates at a flat 0.00%.

As expected, the Federal Reserve raised the benchmark interest rate on Wednesday, to a range between 1.25% and 1.50%. This marked the third rate hike in 2017, and is reflective of a strong performance of the US economy. The Fed statement was optimistic about the economy, noting that the labor market 'remained strong'. It also lowered its unemployment forecast in 2018 from 4.1% to 3.9%, and revised growth for 2018 from 2.1% to 2.5%. Despite this rosy prognosis, the dollar was broadly down after the announcement. Why? One reason is the sore point in the economy – inflation. The Fed has not changed its September forecast for rate hikes next year, with the Fed dot plot indicating that three rate hikes are projected for 2018. This disappointed some investors who would like to see four increases next year. As well, the rate statement said that the Fed did not expect the tax reform legislation to have any long-term effect on the economy, contradicting White House claims that the legislation would trigger substantial growth in the economy.

After the Fed raised rates, attention now shifts to the ECB, which will set interest rates later on Thursday. The ECB is widely expected to maintain current rates, so investors will be focusing on the follow-up press conference with ECB President Mario Draghi. If the ECB sends out an optimistic message about the economy, the euro rally could resume. Meanwhile, German indicators continue to sparkle. Manufacturing PMI hit a new record, climbing to 63.3 points. The PMI Composite Output Index, which measures business activity, improved to 58.7, its highest level since 2011. A robust German economy has been the locomotive for the eurozone, which has rebounded in 2017 with stronger growth and lower unemployment.

(BOE) Bank Rate Maintained at 0.50%

Our Monetary Policy Committee has voted unanimously to maintain Bank Rate at 0.50%. The committee also voted unanimously to maintain the stock of corporate bond purchases and UK government bond purchases.

The Bank of England's Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 13 December 2017, the MPC voted unanimously to maintain Bank Rate at 0.5%. The Committee voted unanimously to maintain the stock of sterling non-financial investment-grade corporate bond purchases, financed by the issuance of central bank reserves, at £10 billion. The Committee also voted unanimously to maintain the stock of UK government bond purchases, financed by the issuance of central bank reserves, at £435 billion.

In the MPC's most recent economic projections, set out in the November Inflation Report, GDP grew modestly over the next few years, at a pace just above its reduced rate of potential. Consumption growth remained sluggish in the near term before rising, in line with household incomes. Net trade was bolstered by the strong global expansion and the past depreciation of sterling. Business investment, while affected by uncertainties around Brexit, was projected to continue to grow at a modest pace, supported by strong global demand, high rates of profitability, the low cost of capital and limited spare capacity.

Unemployment was expected to remain low throughout the three-year forecast period, and domestic inflationary pressures were projected to pick up gradually as remaining spare capacity was absorbed and wage growth recovered. Nevertheless, reflecting the diminishing effect of sterling's depreciation, CPI inflation was forecast to decline from around 3% to approach the 2% target by the end of the three-year forecast period.

The recent news in the macroeconomic data has been mixed and relatively limited. Global growth has remained strong. Domestically, some activity indicators suggest GDP growth in Q4 might be slightly softer than in Q3. The measures announced in the Autumn Budget will lessen the drag on aggregate demand stemming from fiscal consolidation, relative to previous plans. The labour market remains tight, and surveys suggest this will continue. Although it is too early to arrive at a comprehensive view of the effect of November's rise in Bank Rate on the economy, the impact on interest rates faced by households and firms has been consistent with previous experience.

CPI inflation was 3.1% in November. It remains the case that inflation has been pushed above the target by the boost to import prices that resulted from the past depreciation of sterling. The MPC judges that inflation is likely to be close to its peak, and will decline towards the 2% target in the medium term. In line with the procedure set out in the MPC's remit, the Governor will be writing an open letter to the Chancellor of the Exchequer, accounting for the overshoot relative to the target and explaining the MPC's policy strategy to return inflation sustainably to the target. This letter will be published alongside the minutes of the February 2018 MPC meeting and the accompanying Inflation Report.

Developments regarding the United Kingdom's withdrawal from the European Union – and in particular the reaction of households, businesses and asset prices to them – remain the most significant influence on, and source of uncertainty about, the economic outlook. The Committee noted the progress in the Article 50 negotiations between the United Kingdom and the European Union. In such exceptional circumstances, the MPC's remit specifies that the Committee must balance any trade-off between the speed at which it intends to return inflation sustainably to the target and the support that monetary policy provides to jobs and activity.

The steady erosion of slack over the past year or so has reduced the degree to which it is appropriate for the MPC to accommodate an extended period of inflation above the target. Consequently, at its previous meeting, the MPC judged it appropriate to tighten modestly the stance of monetary policy in order to return inflation sustainably to the target, while continuing to provide significant support to jobs and activity. At this meeting, the Committee voted unanimously to maintain the current monetary stance. The Committee remains of the view that, were the economy to follow the path expected in the November Inflation Report, further modest increases in Bank Rate would be warranted over the next few years, in order to return inflation sustainably to the target. Any future increases in Bank Rate are expected to be at a gradual pace and to a limited extent. The Committee will monitor closely the incoming evidence on the evolving economic outlook, including the impact of last month's increase in Bank Rate, and stands ready to respond to developments as they unfold to ensure a sustainable return of inflation to the 2% target.

Dollar Drifts On Dovish Fed Hike, TRY Plummets

Thursday December 14: Five things the markets are talking about

Global equities continue to drift as investors await the outcome of the last ECB meeting of the year (07:45 am EDT). Ahead of the U.S open, the ‘mighty' dollar has temporary halted its decline sparked by the Fed's unchanged outlook yesterday for rate increases in 2018.

Note: The Swiss National Bank (SNB) and Norges bank left rates unchanged as expected (see below), however, Norway seems to have brought forward its first planned rate hike. Turkey's central bank said it will keep monetary policy tight until the inflation outlook displays a significant improvement and becomes consistent with targets – it raised its late liquidity window rate by +50 bps.

On Wednesday, the Fed raised interest rates another +25 bps and is expected to make three more such moves next year. In her final press conference at the helm, Chair Janet Yellen made it clear there is little to be concerned about in the U.S economy. Growth is strong, hiring is robust and there are no dangerous bubbles on the horizon.

Most Fed officials now expect some boost to economic growth from the tax package now working its way through Congress. Coming tax cuts likely would raise consumer and business spending, providing “some modest lift” to economic growth in coming years.

U.S officials expect unemployment to fall to +3.9% by the end of next year, down from their earlier estimate of +4.1%. And yet, despite those signs of a stronger economy, officials see no more inflation than they anticipated in September and no cause to raise interest rates more aggressively than they expected three-months ago.

Now it's on to the ECB and BoE rate announcements this morning. Both central banks announced significant policy changes after their last meetings and the market now expect them to stand pat while officials assess developments. Investors should be looking President Draghi's comments in his press conference (08:30 am EDT) for more clues about plans to start weaning investors off its monthly bond purchases next year.

1. Stocks struggle after new records

In Japan overnight, the Nikkei share average slipped as banks and insurer shares weakened in line with lower interest rates. The Nikkei ended down -0.3%, while the broader Topix was -0.2% lower.

Down-under, Aussie shares fell on Thursday and broke a five-session run of gains, with financials and real estate stocks accounting for most of the losses. The S&P/ASX 200 index declined -0.2%. In S. Korea the Kospi closed out its session little changed.

In Hong Kong, equities were also little changed, as investors gave muted reaction to the Fed's widely expected U.S rate hike. At close of trade, the Hang Seng index was down -0.19%, while the Hang Seng China Enterprises index rose +0.1%.

In China, stocks fell on Thursday, after the PBoC nudged up money market rate (see below) following the Fed's rate hike. At the close, the Shanghai Composite index was down -0.29%, while the blue-chip CSI300 index was down -0.57%.

Note: China's central bank lifted money market rates as authorities sought to defuse financial risks without imperilling the economy.

In Europe, regional indices trade mixed this morning with the DAX, CAC and the FTSE trading lower with Spanish and Italian markets trading slightly higher.

U.S stocks are set to open in the ‘black' (+0.1%).

Indices: Stoxx600 -0.1% at at 390.1, FTSE -0.2% at 7482, DAX -0.3% at 13088, CAC-40 -0.2% at 5388, IBEX-35 +0.1% at 10270, FTSE MIB +0.2% at 22442, SMI -0.1% at 9384, S&P 500 Futures +0.1%

2. Rising U.S output threatens global oil market balance, gold higher

Oil prices remain better bid ahead of the U.S open as industry data this week revealed a larger-than-expected drawdown in U.S crude stockpiles. Also aiding prices is the markets expectation for an extended shutdown of a major North Sea crude pipeline.

Brent crude is up +19c, or +0.4% at +$64.03 a barrel, while U.S light crude (WTI) is up +15c, or +0.2%.

U.S API data on Tuesday indicated that domestic crude stocks fell by -7.4m barrels last week. That is almost twice the decline of market expectations for a drop of -3.8m barrels.

Also providing support is the news that Britain's biggest pipeline from its North Sea oil and gas fields is likely to be shut for several weeks for repairs.

Nevertheless, prices are expected to be capped in the medium term as a report from the IEA this morning stating that the global oil market will likely show a surplus in H1 of 2018, as rising U.S. supply offsets OPEC's discipline in maintaining its production cuts for the whole of next year

Gold prices hit it's highest print in a week overnight, as the dollar remains somewhat on the defensive after tumbling in the previous session following the Fed's decision on interest rates. Spot gold is up +0.1% at +$1,256.40 an ounce, after earlier touching its highest since Dec. 7 at $1,259.11 in the Euro session.

3. Central banks monetary policy decision

This morning's Swiss National Bank (SNB) rate decision was as expected with the deposit rate unchanged at -0.75% and the SNB saying it is still willing to intervene in currency markets if the franc gets too strong. Officials also stuck with their assessment that the franc remains “highly valued” and that it's too early to talk about ‘normalization' of Swiss monetary policy.

In Norway, government bonds remain stable after the Norges Bank (central bank) left its key rate unchanged at +0.50%, in line with expectations. The two-year government bond trades at a yield of +0.45%, while the 10-year bond trades at a yield of +1.49%. Officials say there is a continued need for expansionary monetary policy.

In China, the People's Bank of China (PBoC) overnight raised two key short-term interest rates in tandem with the Fed's hike. Officials raised the rates it charges commercial banks on seven-day and 28-day loans by +5 bps each. It also raised rates for a medium-term liquidity instrument. The increases were smaller than 0.10 percentage-point moves in the first quarter, and the bank left the benchmark policy rates unchanged.

Note: This surprise move suggests that China's policy makers are trying to strike a balance between easing pressure on the yuan and reducing capital flight on one hand, and managing higher borrowing costs on the other.

4. Dollar under pressure from Fed hike

Heading into the U.S session, the USD (£1.3442, €1.1830 and ¥112.74) continues to maintain its softer tone in the aftermath of the yesterday's FOMC rate decision, which is viewed as a “dovish” Fed hike.

The greenback has softened as the Fed ‘dots' basically stuck to its rate projections. It would suggest that dealers and investors alike want to keep challenging the Fed's ability and willingness to get inflation to +2%.

Elsewhere, the CHF (€1.1686) has fallen slightly after the SNB left interest rates on hold this morning, as expected, while it says the currency remains “highly valued” despite its recent depreciation. Officials indicated that while the CHF's “overvaluation” has continued to decrease, “the negative interest rate and the SNB's willingness to intervene in the FX market as necessary remain essential.”

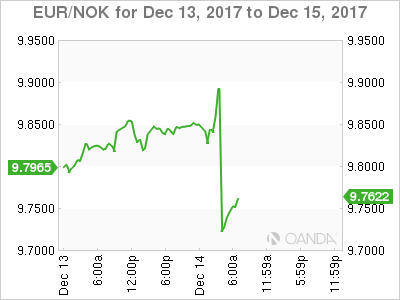

The NOK (€9.7401) has rallied more than +1% after the Norges Bank kept interest rates steady, but says “changes in the outlook and the balance of risks imply a somewhat ‘earlier' increase in the key policy rate than projected.”

The Turkish lira falls sharply after the Central Bank of the Republic of Turkey raised the late liquidity window lending rate by just +50 bps to +12.75% from +12.25%, at the lower end of markets expectations. Many had expected an increase of +100 bps. USD/TRY has jumped +2% on the day to reach a 10-day high of $3.8909.

5. U.K. retail sales accelerate last month on Black Friday deals

Data this morning shows U.K. retail sales accelerated last month as Britons flocked to shops to take advantage of Black Friday discounts.

Sales grew by +1.1% on the month in November, more than twice the pace of growth seen in the previous month, and significantly above the markets estimate of +0.5%m/m.

The figures indicated a pickup in consumer spending in Q4, a welcome sign for the largely domestic-driven economy.

Digging deeper, growth in retail was driven largely by strong sales of electrical household appliances.

Note: The U.K economy has slowed visibly this year, as accelerating inflation, spurred by the pound's (£1.3442) steep depreciation after last year's Brexit vote, squeezed consumer spending.

Euro Jumps After Fed Sounds Dovish, ECB Decision Next

The euro has paused in the Thursday session, after posting strong gains on Wednesday. Currently, EUR/USD is trading at 1.1824, down 0.01% on the day. In economic news, it’s a busy day in the eurozone and the US. Manufacturing PMIs beat their estimates in France, Germany and the eurozone, with strong readings of 59.3, 63.3, and 60.6 points respectively. On the services side, Services PMIs beat the estimates in Germany and the eurozone, but fell short in France. Later in the day, the ECB is expected to maintain interest rates at a flat 0.00%. In the US, consumer spending indicators are expected to improve in November, with Core Retail Sales and Retail Sales forecast at 0.6% and 0.3%, respectively. On Friday, the eurozone releases trade surplus and the US publishes Empires State Manufacturing Index.

There were no surprises from the Federal Reserve, which raised rates on Wednesday, bringing the benchmark rate to a range between 1.25% and 1.50%. This marked the third rate hike in 2017, testimony to the strong performance of the US economy. The Fed statement was optimistic about the economy, noting that the labor market “remained strong”. It also lowered its unemployment forecast in 2018 from 4.1% to 3.9%, and revised growth for 2018 from 2.1% to 2.5%. Despite this rosy prognosis, the dollar was broadly down after the announcement. Why? One reason is the sore point in the economy – inflation. The Fed has not changed its September forecast for rate hikes next year, with the Fed dot plot indicating that three rate hikes are projected for 2018. This disappointed some investors who would like to see four increases next year. As well, the rate statement said that the Fed did not expect the tax reform legislation to have any long-term effect on the economy, contradicting White House claims that the legislation would trigger substantial growth in the economy.

The markets will now shift to the ECB, which will set interest rates later on Thursday. The ECB is widely expected to maintain current rates, so investors will be focusing on the follow-up press conference with ECB President Mario Draghi. If the ECB sends out an optimistic message about the economy, the euro rally could resume. Meanwhile, German indicators continue to sparkle. Manufacturing PMI hit a new record, climbing to 63.3 points. The PMI Composite Output Index, which measures business activity, improved to 58.7, its highest level since 2011. A robust German economy has been the locomotive for the eurozone, which has rebounded in 2017 with stronger growth and lower unemployment.

Brexit – The Tough Negotiations Begin Now

Phase One Agreement an Important Milestone

Earlier this month, the UK and European Union reached an important milestone in Brexit negotiations, with the latter deeming that sufficient progress had been made to move the discussion on to the future relationship.

This comes 18 months after the UK voted to leave the EU and almost nine months after article 50 was triggered – officially starting the process – highlighting the snail's pace that the process has so far moved at and offering little hope that an agreement on the future relationship can be wrapped up by this time next year.

An agreement on the financial settlement, citizens' rights and the Irish border – the three issues the EU insisted must be resolved before trade talks could begin – at times looked unachievable, leading to speculation that talks may collapse before phase two even got underway, or that Theresa May could be ousted by frustrated Brexiteers in her own government.

While an eleventh hour deal was agreed – subject to approval by the European Council on Friday (8 December) – the response to the deal was more one of relief or even scepticism rather than optimism.

If phase one took this long to conclude, what hope do we possibly have that phase two can be completed in the next 12 months? Especially when the Irish border issue has been kicked down the road, rather than resolved.

What's more, Brexit Secretary David Davis' claim over the weekend that the agreement was more a statement of intent than a legally enforceable thing, will do nothing to build trust between the UK and EU ahead of trade talks. As it stands, the comments don't appear to have jeopardised the European Council's vote, but efforts will now be made to make it enforceable.

Why Did Sterling Fall After the Agreement?

As far as markets are concerned, the agreement was a positive step forward but not something to get carried away with. The pound hit a seven-month high – on a trade weighted basis – but the gains were short-lived and it is currently on course for a third consecutive intraday decline.

Of course, some of this is going to be a classic case of “buy the rumour, sell the fact”, where traders buy something on the growing expectation of a positive outcome then lock in profits (sell) once it's confirmed.

However, the fact that the gains so far have been fairly modest suggest the conclusion of phase one has not attracted the kind of optimism one may have expected. The fudged nature of it and above comments from Davis clearly won't have helped matters.

What Comes Next?

The next phase of negotiations will now begin at the turn of the year, with the two-year transition being a priority for the UK. Trade talks will likely continue to take a back seat for the EU, particularly if a transition is agreed, with other aspects of the divorce taking priority, including ironing out the details of those issues already discussed.

The next 12 months is likely to strongly resemble the last nine, which means more frustrating negotiations, slow progress and through the night talks as the deadline approaches.

A trade deal can't be signed until the UK has officially left the EU, which if the government gets its way will be signed into law for March next year, meaning much of the work will likely be done during the transition.

One thing seems clear, the drama that has engulfed negotiations over the last 12 months is unlikely to go away. Theresa May's position at home is borderline untenable and should she still be Prime Minister in March 2019, it will be quite an incredible achievement.

Her majority is being propped up by the DUP after a disastrous campaign and every day it seems one of her colleagues vying for her job is preparing to stab her in the back. Should this happen and she be replaced by a more fierce Brexiteer, negotiations could take a sudden turn for the worse.

As far as markets are concerned, we could see the pound gradually pare back its post-referendum declines over this period, assuming negotiations go to plan.

The FTSE has performed extremely well since bottoming in the days after the referendum – up around 30% at the time of writing – which has been strongly supported by the weaker pound as companies in the index make a huge proportion of their profits abroad.

If the pound does recover over the next year or two, this may therefore be a headwind for the FTSE and contribute to it underperforming its peers.