Sample Category Title

Minor Slowdown Expected in Chinese Manufacturing Activity; Aussie also in Spotlight

Chinese official manufacturing and services PMIs for the month of November are due on Thursday at 0100 GMT, while Caixin's respective measure for the manufacturing sector is scheduled for release on Friday at 0145 GMT.

According to analysts' projections, the official manufacturing PMI will decline to 51.4 in November from October's 51.6. Despite the ongoing rebalancing in the Chinese economy resulting in the services sector playing an ever more prominent role in terms of contribution to economic activity, the bulk of attention still remains on the release of manufacturing PMI figures, with no polls for services PMI being released. The Caixin manufacturing PMI, which compared to the official figure focuses more on small and mid-size businesses, is also expected to reflect a minor slowdown, falling to 50.9 from October's 51.0. A reading of 50 reflects zero sectoral growth.

Should manufacturing activity indeed decline, then this is not necessarily a negative sign - at least not in its entirety - for the world's second largest economy as it would be partially attributed to the government's efforts to curb pollution in its attempts to shift focus to the quality of growth rather than merely the quantity. Along similar lines, a clampdown of financial risks could also act as a drag on activity by virtue of higher borrowing costs. It is not just government efforts for better quality expansion that are weighing on manufacturing growth though, as weaker export orders are adding downward pressure on Chinese factories' activity as well.

It should be noted that if the official gauge of manufacturing activity comes below October's as expected, this would mark the second straight month of declining activity, though, in a sign of resilience, it would also constitute the 16th consecutive month of growth (i.e. a reading above 50).

Besides movements in the yuan, the Australian dollar will be closely watched by forex market participants when the above data become public, as the Australian currency is considered a liquid proxy for China's economy due to the two nations' strong trade ties.

An upside surprise in the figures, could push aussie/dollar higher. In such an event, the pair might meet resistance around the two-week high of 0.7644 recorded earlier in the week. Should the slowdown in activity be sharper than anticipated, then aussie/dollar is likely to head lower. In this case, the pair could find support around 0.7529, this being the five-and-a-half-month low recorded on November 21.

It should also be taken into account that Australian data that have the capacity to generate movements in the aussie will also hit the markets tomorrow. Those include building capital expenditure and private new capital expenditure due at 0030 GMT.

Yen Dips as US GDP Accelerates in Q3

The Japanese yen has posted considerable gains in the Wednesday session. In North American trade, USD/JPY is trading at 111.84, up 0.34% on the day. On the release front, Japanese Retail Sales disappointed with a decline of 0.2%. This missed the estimate of a 0.1% gain. Later in the day, Japan releases Preliminary Industrial Production, with an estimate of 1.9%. In the US, Preliminary GDP for the third quarter came in at 3.3%, matching the forecast. Pending Home Sales jumped to 3.5%, crushing the estimate of 1.1%. As well, Fed Chair Janet Yellen will testify before a congressional committee. On Thursday, the US releases Personal Spending and unemployment claims, and Japan publishes Tokyo Core CPI.

Fed Chair Designate Jerome Powell testified before the Senate Banking Committee on Tuesday. Powell said that he favored tailoring regulations for small banks, leaving the toughest regulations for the big players. Powell was cautious and diplomatic during the hearing, saying that the case is building for a December rate hike, and refused to express an opinion on the Trump tax bill. He will replace Janet Yellen in February, and is widely expected to continue Yellen's monetary stance of small, gradual rate hikes. Fed policymakers have differing views on what to do about inflation, which remains at low levels. Some members have proposed that the Fed drop its 2 percent target, in favor of a "gradually rising path" for prices. The Fed remains confounded by low inflation and wage growth, despite a labor market that is at full capacity. Still, the Fed will likely pull the rate trigger next month, and could raise rates up to 3 more times in 2018 if the economy continues to expand at its current pace.

Is the Bank of Japan rethinking its massive stimulus program? With the Japanese economy showing moderate growth, there has been speculation that the Bank of Japan is giving some thought to tapering stimulus. Any tapering to the program could give a significant boost to the yen, so the markets are closely monitoring BoJ statements and comments from BoJ policymakers, looking for clues. However, a stronger yen would hurt exports, which has been a catalyst for the stronger economy. Inflation and wage growth remain low, and if we are to take BoJ Governor Haruhiko Kuroda at his word, the Bank will not taper stimulus before inflation moves closer to the BoJ's target of around 2 percent.

USD Off Eecent Lows, But Gains Remains Modest

- European equities had a strong run today, surfing on the risk-on sentiment triggered by increased hopes of the Congressional adoption of the US tax reform. US equities opened mixed with S&P building out yesterday's gains and Nasdaq showing modest losses.

- Britain has bowed to EU demands and agreed to fully honour its financial commitments as identified by Brussels, removing one of the biggest obstacles to a Brexit divorce settlement. UK would assume EU liabilities worth up to €100 bln although net payments, discharged over many decades, could fall to less than half that amount.

- Prices in Germany rose faster than expected in November, in an encouraging sign of the resilience of inflation trends in the eurozone as the central bank prepares to start withdrawing its quantitative easing programme. Consumer prices rose 1.8% Y/Y in November, a sharp jump from last month's disappointing 1.5% Y/Y.

- US GDP grew at an annualised rate of 3.3% in Q3, the highest reading since Q3 of 2014. The improvement reflected increases in business investment, exports and private inventories. However, consumer spending expanded at a slower pace of 2.3%, down from the 3.3 per cent growth notched in Q2.

- In a prepared testimony to Congress, Fed chair Yellen gave a positive health check on the economy's recent performance and stuck with her existing line on gradual rate rises, but warned that deeper reforms would be needed to generate a "sustained boost" in economic growth without causing inflation that is too high.

- Economic recovery across the eurozone has eased pressures on its financial system according to the European Central Bank's financial stability review, but concerns over greater risk-taking by investors hunting for returns in low-volatility markets still linger.

Rates

Core bonds under moderate downward pressure

Core bonds were under pressure from the start of the European trading. A first down-leg coincided with a strong opening of equity trading. German inflation data were slightly higher-than-expected preventing any noticeable return action. A second down-leg was triggered by the publication of Yellen's written testimony before the JEC. She sees the recent low inflation due to transitory factors and calls the expansion increasingly broad-based. Financial risks are muted. She concludes that gradual further tightening is appropriate. So a third rate hike this year in December is baked in the cake. While she won't be chair anymore in 2018, she looks favourable to more rate increases in 2018.

At the time of writing, the German yield curve steepened with yields up to 4 bps higher. The US yield curve steepened too with yields up between 1.6 bp (2-yr) and 5.6 bps (30-yr). On intra-EMU bond markets, peripherals profited from the risk on climate and narrowed 2-to-4 bps.

Currencies

USD off recent lows, but gains remains modest.

Today, the dollar gained slightly further ground as yesterday's progress on a tax bill caused some USD shorts to reduce exposure. The dollar received some breathing space as its trades off its recent lows against the euro and the yen. However, US political risk isn't out of the way and the technical picture didn't improve in a profound way yet.

Overnight, Asian equities couldn't fully copy strong WS gains, trading mixed to slightly higher. Rising tensions on North Korean and uncertainty on the impact of measures to prevent excessive leverage in China, amongst others, might have played a role. Yesterday's USD rally stalled. USD/JPY touched an intraday top early in Asia, but the dollar eased slightly as the Asian trading evolved. USD/JPY traded in the 111.50 area going into the start of European dealings. EUR/USD changed hands in the 1.1860 area.

Early in Europe, interest rate differentials narrowed temporary in favour of the euro. EUR/USD touched an intraday top in the 1.1880, but the gained could not be sustained. EMU data were mixed. French spending data disappointed. EC economic confidence rose to a multi-year peak. First EMU inflation data also gave a diffuse picture. The ECB in its stability report said that EMU stability risks are contained, but mentioned a series of vulnerabilities, including a sudden re-pricing in risk premia. During the morning session, EUR/USD gradually reversed the initial uptick as the dollar found a better bid across the board. However, rising risk on a US government shutdown after Democrats didn't show up in a meeting with president Trump prevented more pronounced USD gains.

Early in US dealings, the text of Yellen's written statement before the JEC of Congress was released. Yellen sees the economic expansion as increasingly broad based. It will support faster growth in wages and incomes. Yellen expects the Fed to continue to gradually raise interest rates and reduce its balance sheet. The headlines from Yellen's speech were less soft than markets expected/feared. US bond yields and the dollar extended their intraday rise. The US Q3 GDP was revised marginally higher to 3.3% Q/Qa, but was largely ignored. USD/JPY took the lead in the USD rebound and tries to regain the 112 big figure. EUR/USD dropped to the 1.1820 area and is currently changing hands in the 1.1835 area. Later today, the Fed will publish its Beige Book, preparing the December 13 Fed meeting. Pressure on the dollar eased as it drifted somewhat further away from the recent lows. That said, the gap is still not big, given the US political risks (Tax bill and potential government shutdown) that are still not yet out of the way.

Sterling extends gradual rebound on Brexit progress

Today, sterling kept a cautiously positive bias, building on yesterday's gains. The preliminary EU/UK agreement on a divorce bill raises chances that negotiations on the future relationship start after the December EU summit. Ireland's EU commissioner also suggested that a break-through on the issue of the Irish border could follow soon. Earlier this morning, the UK money supply and lending data came out on the softer side of expectations. EUR/GBP trades currently in the 0.8830 area. Cable trades in the 1.34 area and tries to extend gains beyond the 1.3350 range top, even as the dollar is also better bid. So, sentiment on sterling improved. However the gains are not spectacular indicating that markets still see a lot of Brexit work to be done.

Dollar and Pound March Higher; Euro Extends Declines

The US dollar and the British pound remained the day's biggest winners in European trading on Wednesday on increased hopes of big tax cuts in the United States and the UK and the EU edging closer to a deal on the Brexit divorce terms. Most majors came under pressure from the stronger greenback, including the euro, which headed for a third straight day of losses, but the resurgent pound capped the dollar index's gains.

European equities headed higher after another record close on Wall Street overnight, with investors shrugging off a fresh threat by North Korea, which yesterday conducted another missile test. The UK's FTSE 100 bucked the trend as it was hurt by a firmer sterling, while gold drew no interest from safe-haven flows, dropping 0.5% to $1287 an ounce.

The euro hit a session low of $1.1816, retreating further from Monday's two-month peak of $1.1960. Another set of solid business survey release out of the Eurozone failed to lift the single currency. The European Commission's economic sentiment index rose to a 17-year high of 114.6 in November, in line with forecasts. Its business climate index was also up, climbing from 1.44 to 1.49 to a 10-year high, though this was below estimates of 1.53. In an encouraging sign for the European Central Bank, inflation expectations strengthened, with the index increasing from 14.7 to 16.0 in November.

There was little reaction to the ECB's bi-annual Financial Stability Review but the euro found some support from stronger-than-expected German inflation data. Germany's harmonized measure of the consumer price index rose from 1.5% to 1.8% year-on-year in November's flash reading, beating expectations of 1.7%. The data helped the euro recover to around $1.1835 in late session.

Sterling hit a two-month high of $1.3430 on reports that the UK and the EU have agreed the outlines of a deal on the Brexit divorce bill, thought to be around €50 billion. The issue of the Northern Irish border remains a sticking point, but hopes are high that the EU's chief negotiator, Michel Barnier, will recommend to EU leaders that there has been sufficient progress on the divorce terms for the talks to move on to the next phase at the December summit.

The pound eased a little however, after Bank of England lending figures showed consumer credit growth in the UK hit an 18-month low in October. Sterling was last trading around $1.34, up 0.5% on the day, while the euro was down a similar amount at 0.8830 pounds.

The greenback moved towards one-week highs, with dollar/yen flirting with the 112 level and the dollar index hitting a session high of 93.435. The US currency got a boost yesterday after the Senate Budget Committee gave the go-ahead for a full Senate vote on the tax bill on Thursday. Senators will be debating the bill today with further amendments expected given that several Republican Senators are still opposed to the legislation in its current form.

Uncertainty about tomorrow's vote, as well as concerns about a possible US government shutdown on December 8 after senior Democrats cancelled a meeting with President Trump to discuss a deal on a new spending bill, have been limiting the dollar's advance. However, the greenback got an added boost from an upward revision to US GDP. Annualized GDP growth in the third quarter was revised up from 3.0% in the preliminary estimate to 3.3% in the second reading, beating expectations of 3.2%. The figure is the highest quarterly growth since 2014 and is up from 3.1% in the second quarter.

Fed Chair Janet Yellen's prepared remarks for her semi-annual testimony before the Joint Economic Committee in Congress didn't attract the usual fanfare as the outgoing Fed chief didn't add anything new to the monetary policy outlook. Yellen repeated that the recent fall in inflation is likely to be due to "transitory factors" and reiterated that "additional gradual rate hikes" will be appropriate, but avoided specifically mentioning December as the timing for the next increase.

Commodity-linked currencies underperformed today, with the Australian dollar sliding to a one-week low of $0.7552 and the New Zealand dollar dropping to around $0.6885. The Canadian dollar was also down, weighed by weaker oil prices, with dollar/loonie hitting a 4-week high of 1.2859.

Crude oil prices remained under pressure amid doubts about whether major oil producers will agree to an extension of the output cut deal at Thursday's meeting in Vienna between OPEC and some non-OPEC countries. OPEC sources today suggested that an expected extension of nine months beyond March 2018 could be accompanied by an interim review in June, meaning the deal may end sooner, according to Reuters.

Both WTI and Brent crude stood slightly down on the day at $57.89 and $63.56 a barrel respectively, ahead of the EIA's weekly US inventory report.

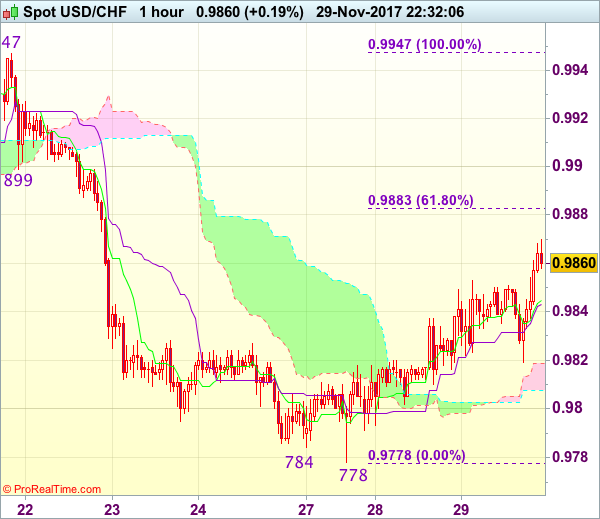

Trade Idea Wrap-up: USD/CHF – Sell at 0.9885

USD/CHF - 0.9859

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9845

Kijun-Sen level : 0.9845

Ichimoku cloud top : 0.9819

Ichimoku cloud bottom : 0.9808

Original strategy :

Sell at 0.9875, Target: 0.9775, Stop: 0.9910

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9885, Target: 0.9785, Stop: 0.9920

Position : -

Target : -

Stop : -

Dollar’s rebound after falling to 0.9778 earlier this week suggests consolidation above this level would be seen and marginal gain from here cannot be ruled out, however, reckon upside would be limited to 0.9876 (previous support) and bring another decline later, below 0.9815-20 would bring a retest of said support at 0.9778, break there would extend recent decline from 1.1038 top towards 0.9730-37 support area but reckon support at 0.9705 would hold from here, bring rebound later.

In view of this, we are looking to sell dollar again on further subsequent recovery as previous support at 0.9876 should turn into resistance and limit upside. Only break of 0.9895-00 would defer and signal a temporary low is formed instead, bring a stronger rebound to 0.9920 but price should falter well below resistance at 0.9947.

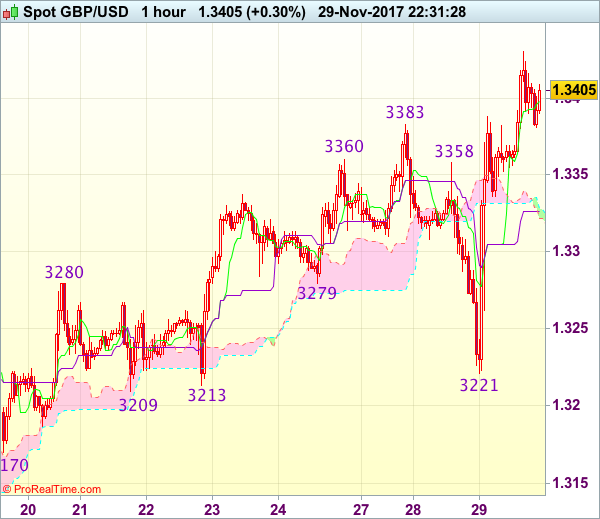

Trade Idea Wrap-up: GBP/USD – Stand aside

GBP/USD - 1.3409

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3406

Kijun-Sen level : 1.3326

Ichimoku cloud top : 1.3328

Ichimoku cloud bottom : 1.3321

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite falling briefly to 1.3221, as cable found renewed buying interest there and has staged another rally, suggesting the erratic rise from 1.3027 low is still in progress, hence near term upside bias remains for this move to extend further gain to 1.3435-40, however, overbought condition should prevent sharp move beyond previous resistance at 1.2455 and price should falter below 1.2475-80, bring retreat later.

In view of this, would not chase this rise here and would be prudent to stand aside in the meantime. Below 1.3355-60 would suggest an intra-day top is formed instead, bring weakness t the Kijun-Sen (now at 1.3315) but reckon downside would be limited to 1.3260-65, bring another rise later.

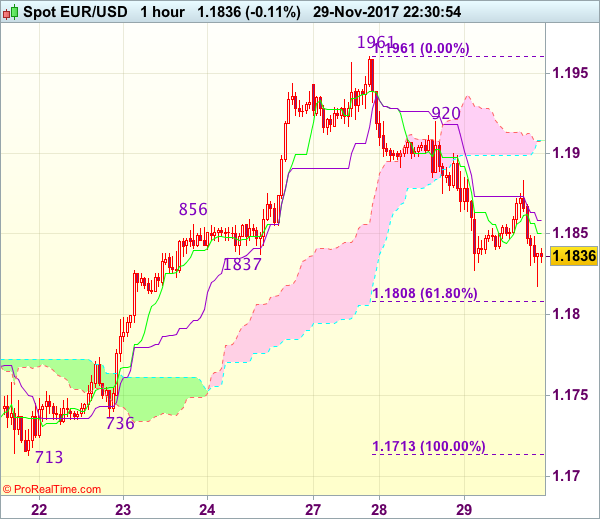

Trade Idea Wrap-up: EUR/USD – Stand aside

EUR/USD - 1.1837

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1850

Kijun-Sen level : 1.1858

Ichimoku cloud top : 1.1908

Ichimoku cloud bottom : 1.1908

Original strategy :

Bought at 1.1845, stopped at 1.1825

Position : - Long at 1.1845

Target : -

Stop : - 1.1825

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As the single currency has fallen again after meeting renewed selling interest at 1.1883, dampening our bullishness and near term downside risk remains for the fall from 1.1961 top to bring retracement of recent upmove to 1.1805-10 (61.8% Fibonacci retracement of 1.1713-1.1961), however, oversold condition should prevent sharp fall below 1.1770 and price should stay well above support at 1.1736, bring rebound later.

In view of this, would not chase this fall here and would be prudent to stand aside for now. Above said resistance at 1.1883 would suggest an intra-day low is formed instead, bring a stronger rebound to 1.1900 but break of 1.1920 is needed to signal the retreat from this week’s high at 1.1961 has ended, bring retest of this level first.

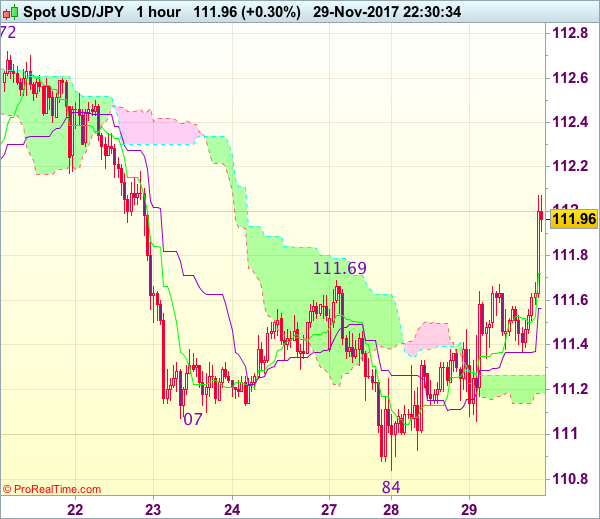

Trade Idea Wrap-up: USD/JPY – Buy at 111.40

USD/JPY - 111.96

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 111.72

Kijun-Sen level : 111.57

Ichimoku cloud top : 111.27

Ichimoku cloud bottom : 111.18

Original strategy :

Buy at 111.00, Target: 112.00, Stop: 110.65

Position : -

Target : -

Stop : -

New strategy :

Buy at 111.40, Target: 112.40, Stop: 111.05

Position : -

Target : -

Stop : -

As the greenback has surged again after brief pullback, adding credence to our view that low has been formed at 110.84 earlier this week, hence consolidation with upside bias remains for this rebound to bring retracement of recent decline, then further gain to 112.20 and possibly 112.40 would be sen, however, near term overbought condition should limit upside and price should falter below resistance at 112.72, bring retreat later this week.

In view of this, we are still looking to buy dollar on dips as 111.35-40 would limit downside. Below 111.05-10 would abort and signal the rebound from 110.84 has ended, bring retest of this level, break there would signal recent decline has resumed and extend weakness to 110.70 and possibly towards 110.50.

The Meaning Behind $1.38 GBP/USD

What has happened to all of the prophetic statements about the British pound falling below $1.15/$1.10 and remaining there?

After crashing last year to $1.1840, a 31-year low (some prices suggest $1.1500), it is now up by 12%. The pound is the only currency in G10 FX to rise against the US dollar over the past 3 months. Will the pound recover above the $1.50 level next year? Or will Brexit dynamics force the currency back under $1.20? In this piece, I shall focus on the technical forces shaping the GBP/USD pair in the medium run and will not discuss macro fundamentals, Brexit or political risk.

Different catalysts, one support

The most striking development in the 35-year chart of the GBP/USD below is the manner in which the $1.3800 support was finally broken in 2016 after three failed attempts spanning over a 7-8 year cycle. The duration of the cycle is not as important as the recurring emergence of $1.38 to act as a crucial foundation in each of the selling attacks sustained by the pound.

The two episodes of 1992 and 2016 share similar catalysts in the sense that they were both triggered by a singular event — the UK's decision to abandon supporting the pound vs the Deutsche mark under the Exchange Rate Mechanism in 1992; and the fateful Brexit referendum of June 2016, ending Britain's 40-year economic and political relationship with the European Union. Indeed, the pound had been weakening considerably ahead of each of those events, but both occasions were highlighted by a singular announcement/outcome.

The sterling's selloffs of 2000-2001 and 2007-2008 were triggered by global economic catalysts as well as UK-specific events, yet, are also highlighted by the $1.38 support.

After the break

The enormity of the Brexit implications is underlined by the fact that $1.38 had finally floundered after surviving three major attacks. Keeping fundamental factors and economic/political analysis aside, technical analysis raises 2 questions: Will GBP/USD return to $1.37-$1.38? And will GBP/USD succeed in breaking above $1.38? The answer to the first question is strong "yes". As long as $1.28 is sustained and the 200-day MA holds, the probability of regaining $1.37 has more than 75% chance probability of occurring. A breach above $1.38 would mean the 2nd violation of a level that once held for more than three decades. In order for such occurrence to manifest itself, chances remain below 30%.

SPOT GOLD Eases Below Daily Cloud as Greenback Rallies after Yellen

Spot Gold dipped below daily cloud after Fed Yellen's remarks inflated dollar, which received further support on better than expected US q3 GDP numbers (3.3% vs 3.2% f/c). Fresh bearish acceleration and extension through cloud base weakened near-term structure, seeing increased risk of further easing.

Initial negative signal was generated on Monday's strong rejection just ahead of psychological $1300 barrier and Tuesday's Doji candle.

Close below daily cloud today would be additional bearish signal for further retracement of $1263/$1299 recovery leg.

Bearish acceleration found footstep at $1285 (Fibo 38.2% of $1263/$1299) which marks next pivot.

Break here would open $1281 (50% retracement/daily Kijun-sen) and $1277 (Fibo 61.8%) in extension.

Broken cloud base marks immediate resistance at $1288, with return and close in the daily cloud expected to ease bearish pressure.

However, stronger recovery needs to regain session high at $1296 to shift near-term focus higher again.

Res: 1288; 1290; 1296; 1299

Sup: 1287; 1285; 1281; 1277