Sample Category Title

Market Morning Briefing: The Aussie Disappointed By Breaking Below The 0.7600 Support Yesterday

STOCKS

Dow (23271.28, -0.59%) has come down as expected and could soon head towards our mentioned target of 23200-23000 in the next few sessions. Note that 23000 is an important near term support and is likely to hold in the medium term producing a bounce back to levels near 23400/500 in the next week.

The downward momentum from levels below 13600 has been fast and sharp in Dax (12976.37, -0.44%). While the momentum continues it may possibly not stop at 12900 levels. A break below 12900 could then take it lower towards 12800-12600 in the next couple of weeks.

Nikkei (22210.45, +0.83%) is trading slightly higher than yesterday's close at 22028.3, but has scope of falling towards 21800 in the medium term (maybe by end of Nov'17). Dollar Yen (112.98) trades below 113 just now and in case it continues to fall further, Nikkei would also eventually come down. Near term looks bearish.

Shanghai (3398.91, -0.11%) has come down as expected and could test 3380 as mentioned yesterday. Note that the 3380-3450 is an important region of trade for the near term and is likely to hold for some time.

Nifty (10118.05, -0.67%) made an intra-day low of 10090 yesterday exactly as expected and bounced back slightly to close above 10100. Note that 10000-10100 is an important near term support which is likely to hold in the first attempt producing a bounce back towards 10300/400. But in case 10000 breaks on the downside (it could happen next week if the Bears continue to remain strong) then the index could be vulnerable to a sharp fall by end of the month.

COMMODITIES

1260-1280 continues to remain as strong support for the near term and while that holds, some movement within 1300-1260 is possible before the upward rally resumes in Gold (1278.20). The price seems to be stable and quiet for the last few sessions and may remain so this week.

Silver (16.98) is down in line with our expectation. Sideways trade within 16.60-17.20 is possible in the near term.

Brent (61.93) could test some support near 61.00-60.85 and if that holds, a bounce back towards 63-64 would be on the cards contrary of our expectation to a fall to 60 just now.

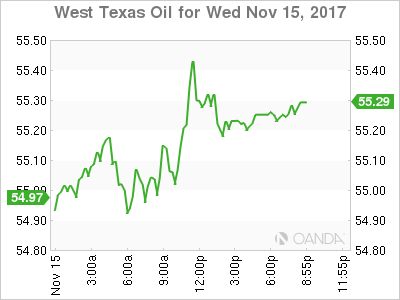

WTI (55.33) could trade in the 54.90-56.00 region (could extend to 54.70 and 57 on either side) for a few sessions. Only a break below 54.90, if seen could take it lower towards 54 in the medium term.

Copper (3.0555) has broken immediate support levels and could now be headed lower to test 3.00-2.95 in the coming sessions.

FOREX

Yesterday, we suggested a range of 1.1850-1500 for the Euro (1.1781) for some weeks. A high of 1.1861 was seen yesterday and the Euro has come off a bit from there, despite a further dip in US yields (see Interest Rates below). Look for a near-term range of 1.1850-1710.

Dollar-Yen (113.02) has also recovered a bit from an intra-day low of 112.47 seen on break below 113.00. Possibly we may see sideways trade between 112.50-114.35 for the next several days if 112.50 turns out to be a decent Support.

The Euro-Yen (133.15) has come down a bit as the Resistance at 134.00 held well enough. However, the overall trend might be biddish while above 132.

The Pound (1.3173) is a prime candidate for range trade between 1.3025-3275 for the next several days. Good time for those who have the ability to buy low/ sell high and then reverse the trade and then do it again.

The Aussie (0.7598) disappointed by breaking below the 0.7600 support yesterday and has seen a low of 0.7559 so far today. If it does not see a sharp bounce from here, it could be vulnerable to some more downside to 0.7500.

Dollar-Rupee (65.2150) may trade between 65.10-30 over the next few days.

INTEREST RATES

US Bond yields have dipped some more after the US October CPI (+2.05% y/y) came in lower than the previous reading of 2.23%. The 10Yr (2.34%) and 30Yr (2.78%) are down from 2.38% and 2.83% respectively. We have to see if they bounce from current levels or not.

There is fresh concern in the markets about the continued flattening of the US Yield Curve, but perhaps the 10-2 Spread (0.29%) will find Support near current levels.

While there is concern in the USA about yield flattening (will someone please tell once and for all whether Inflation will rise or not), there is concern in India that Inflation will indeed rise. And that has been pushing the 10Yr GOI (7.0170%) higher. Levels below 6.8% seem to be outside consideration now.

No Conviction

No conviction

Picking bottoms on the USD is an exercise in futility even more so after the washout in near-term currency ranges that transpired this week

Indeed, a risk-off point of view continued to influence the market structure overnight with global interest rates rallying; traders becoming increasingly long on theory but short on execution when it comes to rationalizing a flatter the US yield curve

The Euro

To be honest, there are few plausible explanations as to why EUR USD got paid at 1.1859 overnight other than when risk-off mode permeates, and with few EU politic fissures hitting the headlines; the EURO performs admirably as a funding currency.

But other than the than the EUR ramp, the markets have become little more than a pin the tail on the donkey exercise, and despite lower lows and lower highs on the USD this week, there are signs an intransigent greenback is getting ready to stare down the bears. ( forever the eternal USD bull)

Japanese Yen

The break of 113 was nowhere near as severe as anticipated. But with the Nikkie on a massive losing streak from this point forward, it should be a risk-off storyline given that the Tokyo sell-off was the core driver behind this weeks move.

The Australian Dollar

With a mere 25 bps priced in the 2018 rates curve and the RBA downgrading their inflation trajectory, is there any better signal to Sell the AUD?

Weak wages are not a new theme in Australia but yesterday’s data all but reinforced the notion that things are likely to get worse

The AUD employment figures have sparked a small short-covering move on the revisions, but with traders in a fade mode, the AUDUSD is unlikely to challenge.7625

Employment change was +3.7k vs 18.8k expected. However looking at the details, part-time employment fell -20.7k, undermining the +24.3k in full-time jobs. As a consequence, the unemployment rate unexpectedly edged lower to 5.4%.

The initial decision was AUD lower on the headline, but the currency has since recovered

EM Asia FX

The long end of the US rates curve is driving sentiment.After yesterday USD regional meltdown with USDKRW plunging below the 1110 support level and USDPHP broke through 51.00 I think its safe to say investors like Asian currencies despite the sell-off in regional equities. Ok so there is a massive break in logic but price action must be respected.

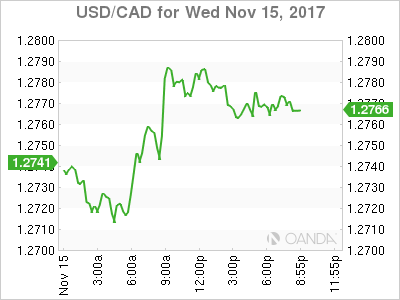

USD/CAD Canadian Dollar Lower On Weak Oil And Upcoming NAFTA Talks

The Canadian dollar depreciated on Wednesday. The loonie lost 0.30 percent versus the greenback after solid inflation and strong retail sales data show the U.S. Federal Reserve is ready to announce a rate hike in December. Positive inflation growth and gains in retail sales will make it harder for the doves within the Federal Open Market Committee (FOMC) to vote against an interest rate lift at the end of the December monetary policy meeting. The meeting will mark the last influential decision of Fed Chair Janet Yellen’s helm at the central bank.

US core consumer prices rose 0.2 percent in October and an unexpected rise by retail sales by 0.2 percent when the forecast called for a flat reading boosted the USD across the board and validating the telegraphed announcement by the Fed that it would hike in December. The market focused on fundamentals on Wednesdays after a couple of weeks with little data to chew on with the tax overhaul in the US as the biggest factor in currencies.

The fall in oil prices as US inventories showed a hefty buildup when a drawdown was expected put more pressure on the CAD. Oil prices surged after the Saudi Arabia Crown Prince Mohammed bin Salman triggered a power play that ended up with various prices and influential business men under arrest and raised questions on how well would the de facto leadership of the Organization of the Petroleum Exporting Countries (OPEC) handle rising diplomatic infighting between members.

The USD/CAD gained 0.30 percent on Wednesday. The currency pair is trading at 1.2769 after the December rate hike chances have been boosted by strong inflation and retail sales data in the US. The market has already priced in a rate move in December, but with a slowdown in inflation and incomplete data due to the tropical storms in September the Fed could keep from raising rates this year. The expected wider gap between Canadian interest rates and the Fed funds rate added pressure to a loonie that was slowly losing momentum due to the losses in oil prices.

Bank of Canada (BoC) Deputy Governor Wilkins spoke today in New York. She reiterated that the central bank will be cautious on its monetary policy decisions which was a departure from the comments in June when the BoC hiked rates in July with a hawkish tone to be followed by a surprise back to back hike in September. NAFTA unknowns remains a concern as it could negatively effect the Canadian economy with the fifth round getting underway in Mexico City.

The NAFTA renegotiation talks will be without the Trade Ministers and will hope to take on less contentious topics such as textiles, services, labor and intellectual property. The last round ended with little progress and Canadian and Mexican negotiators unhappy at the America first proposals from the Trump Administration.

NAFTA has been a target for Trump supporters, but the agreement has the backing of some republican congress members who have sided with their democrat counterparts urging the President to leave US requirements for autos as the original agreement. The move was considered a poison pill as it would unfairly favour US production in the detriment to the other two nations.

The price of oil is net weekly lows after for the second week in a row there was a surprise buildup of US crude inventories. The prices of West Texas Intermediate is trading at $55.20 after the Energy Information Administration (EIA) published a rise of 1.9 million barrels. The market was expecting a miss on the forecast after the API reported an overnight rise of 6.5 million barrels. The Industry group data and the US movement’s are not correlated 1 to 1. The market had already sold off crude, but since the scale of the official buildup was lower some investors reentered their long positions.

The IEA had cut demand forecasts earlier in the week contradicting the estimates form the Organization of the Petroleum Exporting Countries (OPEC). The price of oil has been trading higher after the events in Saudi Arabia but with no new or development, prices are discounting the political uncertainty in the Kingdom.

The battle between the rise in production in the US and the cut agreement between OPEC and other major producers will continue. The Russian Energy Minister Alexander Novak spoke today to reassure that Russian producers are committed to the agreement to cut output, but he did not mention if they will go ahead with an extension of said agreement. The OPEC and major producers will meet in Vienna on November 30.

Market events to watch this week:

Thursday, November 16

4:30am GBP Retail Sales m/m

8:30am USD Unemployment Claims

Friday, November 17

8:30am CAD CPI m/m

8:30am USD Building Permits

Gold Slightly Lower As Markets Digest Consumer Spending And Inflation Numbers

Gold prices have posted small losses in the Wednesday session. In the North American session, the spot price for an ounce of gold is $1278.34, down 0.14% on the day. On the release front, the focus was on consumer indicators. CPI and Core CPI matched the forecasts, with gains of 0.1% and 0.2%, respectively. Consumer spending reports were a mix – retail sales gained 0.1%, below the estimate of 0.2%. Core Retail Sales came in at 0.2%, beating the forecast of 0.0%. As well, the Empire State Manufacturing Index slowed to 19.4 points, well short of the estimate of 25.3 points. This reading marked a 4-month low.

Gold is showing volatility on Wednesday. The metal pushed to a high of $1289.50, its highest level since October 20. However, the metal has given up these gains in the North American session, after the release of retail sales and CPI. We could continue to see movement from gold, as investors keep a close eye on the tax overhaul bill which is on its way to Congress. If the bill gains steam, we are likely to see the dollar move higher, which could weigh on gold prices.

Although consumer price index numbers remain weak, there was better news from producer price index reports on Wednesday. Core PPI and PPI remained unchanged at 0.4%, beating their estimates. PPI increased at an annualized rate of 2.8%, its fastest gain since February 2012. Inflation levels are being closely monitored by the Federal Reserve, as stronger inflation levels would likely result in a rate hike in early 2018. The markets are very bullish on higher rates, with a December hike priced in at 93% and a January raise priced in at 89%.

The heads of central banks met on Tuesday at an ECB event, with a focus on communication with the markets and the public. Federal Reserve Chair Janet Yellen acknowledged that the FOMC committee of 19 members posed problems, as members did not always speak with a unified voice. This led to the markets picking up on differences between policymakers, often leading to market volatility. Yellen admitted that this problem would not be solved anytime soon, saying it was “a work in progress”.

Yen Gains Ground as US Inflation Remains Weak

The yen has improved in the Wednesday session. In North American trade, USD/JPY is trading at 113.03, down 0.38% on the day. On the release front, Japanese Preliminary GDP gained 0.3%, missing the forecast of 0.4%. In the US, CPI and Core CPI matched the forecasts, with gains of 0.1% and 0.2%, respectively. Consumer spending reports were a mix – retail sales gained 0.1%, shy of the estimate of 0.2%. Core Retail Sales came in at 0.2%, beating the forecast of 0.0%. There was disappointing news on the manufacturing front, as the Empire State Manufacturing Index slowed to 19.4 points, well short of the estimate of 25.3 points. This reading marked a 4-month low.

There were no surprises from consumer inflation and spending data for October. Inflation indicators showed small gains, as a strong US economy has not led to higher prices. Consumer spending was unexpectedly strong in September, with Core Retail Sales posting an impressive gain of 1.6 percent. However, the October reading slowed to just 0.2 percent. These early third quarter numbers are somewhat disappointing, coming just weeks before the busy Christmas season. The Federal Reserve is keeping a close eye on inflation numbers, as an uptick in inflation indicators could mean additional rate hikes in 2018. The markets expect some action from the Fed, having priced in a rate hike in December at 91% and a January hike at 89%.

Japan's economy continues to expand, but Preliminary GDP for the third quarter slowed to 0.3%, down from 0.6% in Final GDP for Q2. This marks the longest expansion since 2001, but a stronger economy has not translated into higher inflation levels. Earlier in the week, BoJ Governor Haruhiko Kuroda acknowledged the inflation issue, saying "it is not easy to quickly dispel the deflationary mindset that has formed over the course of 15 years of deflation." Kuroda added that he expects inflation levels to rise, and that the BoJ would continue its massive monetary easing, a key component of the "Abenomics" program.

October’s UK Retail Sales Could Feed Pound Bears

Inflation readings on Tuesday suggested that British pockets will remain squeezed ahead of the Christmas shopping season, as consumer prices continued growing steadily by 3.0% in October, potentially flagging another disappointing month for retailers. With Brexit negotiations trapped in a deadlock and British real wage growth showing no signs of a significant rise, annual retail sales in October are expected to post a negative performance on Thursday, reducing the odds of another interest rate hike this year and therefore deteriorating the outlook for the British pound.

Analysts forecast retail sales to contract in October for the first time since April 2013, declining by 0.6% y/y after rising by 1.2% in September. Recall that September's reading, which constituted the weakest growth observed since June, drove the quarterly gauge to a four-year low of 1.5%. Month-on-month, though, household spending is anticipated to recover by 0.1% following a fall of 0.8% in the previous month. Excluding auto sales and fuel, the core equivalent is estimated to slip by 0.4% y/y compared to a rise of 1.6% seen previously.

A monthly report published by the British Retail Consortium last week gave the first signs of a slowing retail sector, with like-for-like sales sinking by 1.0% in October, offsetting to a large extent the 1.9% growth seen in September. In-store sales of non-food products decreased by 2.9% over the three months to October, reaching a record low since the start of the survey in 2012. Overall, though, the survey revealed a 0.2% annual growth in the industry.

Although the British economy has to a large extent weathered the negative forecasts following the Brexit vote, uncertainty on the Brexit front firmly remains on the table, clouding the outlook. The UK and the EU Brexit negotiators have failed to reach sufficient progress in the talks, raising the probability of a cliff-edge scenario for business leaders. Lacking clarity on the UK's future relationship with the block, firms are reluctant to pay higher wages but instead are prepared to exercise their contingency plans in case of a "hard" or no-deal Brexit. Hence, consumers might cut back on spending as their budgets come under pressure.

Unless actual numbers beat forecasts, the pound will likely move downwards to meet support at the previous bottom at 1.3023. Any violation of this point might also open the way towards August's low of 1.2770.

Alternatively, better-than-expected readings could see the 50-day simple moving average of 1.3253 and the previous top at 1.3337 acting as resistance, while a bigger positive deviation from estimates would shift focus to the 1.35 key-level (previously a support level).

Aussie Again on Spotlight as Employment Figures Eyed

Following a disappointing report on Australian wage growth on Wednesday, the Australian Bureau of Statistics is due to give an outline on the state of the labor market at 0030GMT on Thursday. Unlike wage forecasts which projected a rise in earnings, analysts anticipate the economy to create fewer jobs in October, maintaining the unemployment and participation rates steady at their previous levels. If the numbers fail to meet expectations or otherwise fail to impress, then the aussie could get another shake tomorrow as a slow-growing jobs market would keep wage growth subdued for longer, harming household spending which is a crucial contributor to economic growth.

In October, analysts anticipate 17,500 additional workers to join the labor market in Australia compared to the 19,800 seen in September, marking 13 consecutive months of gains. They also project the unemployment rate to hold flat at a four-year low of 5.5%, which is slightly above the RBA's rate under full employment, and the participation rate to remain steady at a two-year high of 65.2%.

However, the change in full-employment positions will also gather attention as an increase in such jobs has the capacity to push the unemployment rate even lower given that the ratio is calculated factoring in full-time workers rather than part-time ones. Such a development would be good news for RBA policymakers who believe that the unemployment rate will decline to 5.25% by the end of 2019. In September, 6,100 full-time positions were added in the economy, well below the number of 39,500 observed in August.

Still, the RBA might get dashed if low-income industries absorb a larger proportion of workers, restraining wage growth from rising faster and hence limiting inflation which has stuck under the central bank's target band of 2-3%. Consumers will also find it difficult to repay their overloaded debt obligations, meaning that household spending will narrow as well.

Should the data miss forecasts, aussie/dollar will likely extend its downtrend towards the 0.75 key level which acted as a barrier to upside movements in May, while the area around the 0.7326 mark, the lowest level reached since the beginning of the year, could also provide support given a sharper down movement.

Alternatively, if the data surprise to the upside, the 200-day simple moving average (SMA) of 0.7697 could provide resistance ahead of 0.7818, this being the 50-day SMA.

Dollar and Stocks Falter; Euro and Yen Shine

Markets remained in risk-off mode in European trading on Wednesday, with risk assets coming under pressure while safe-havens flourished. The US dollar extended its losses against the yen despite another batch of solid data out of the United States today. The euro rallied to a one-month high against the greenback, but the pound remained range-bound.

The yen was the day's strongest currency, though its driver was not the upbeat third quarter GDP figures released in Japan earlier in the day but safe-haven flows. Risk sentiment failed to recover during the course of the day, with a sell-off in commodities and doubts about the US tax reforms weighing heavily on investors. Major stock indices in Europe were all in the red, following on from declines in Asia today and on Wall Street overnight. US indices looked set for a second straight day of losses after opening lower.

The Swiss franc also benefited from safe-haven demand, rising against the dollar and the euro, but gold's advances were more constrained. The precious metal hit a 3½-week high of $1289.09 an ounce but had fallen back to around $1280 towards the close of European trading.

Long-term US treasury yields continued to decline as a plan by Senate Republicans to link a repeal of the individual mandate that requires Americans to buy health insurance – a key component of Obamacare – with the tax reforms raised concerns that it would make it harder for the legislation to pass. The development undermined the dollar's recent bullish run, with dollar/yen sliding to a 4-week low of 112.46 yen before recovering to around 112.90 in late session. The dollar index also fell to a 4-week low, hitting 93.40.

There was little support for the greenback from the latest US inflation and retail sales figures. The annual CPI rate eased from 2.2% to 2.0% in October as expected, but core CPI came in slightly above forecasts at 1.8%, up from 1.7% in September – the first gain since January. Retail sales impressed, growing by 0.2% month-on-month in October, beating forecasts of no change and follows an upwardly revised 1.9% jump in September. The retail control measure, which is used in GDP calculations, missed expectations of 0.4% to rise by 0.3%, but the prior month's figure was revised up from 0.4% to 0.5%. Also released today was the Empire State Manufacturing index, which missed estimates of 26.0 to sharply drop to 19.4 in November.

The euro reached a high of $1.1860 and was up against most major currencies. It stood 0.2% higher against the pound at 0.8980 in late trading, having earlier broken above 0.90 pounds to touch a near 4-week peak. It was down against the yen however, sliding by 0.5% to 133.15.

Sterling was mixed and saw limited reaction to today's UK jobs data. Britain's unemployment rate was unchanged at 4.3% in the three months to September. But there was an unexpected fall in employment of 14,000 during the period, raising fears that the slowing economy may be starting to impact the labour market. However, there was a positive surprise from wage growth. Average weekly earnings rose by 2.2% year-on-year in the three months to September. It compares with expectations of 2.1% and an upwardly revised 2.3% in August. Excluding bonuses, earnings also rose by 2.2%, in line with estimates.

The pound touched a session low of $1.3131 after the data but later rebounded slightly to around $1.3160. There was some support for the pound after the first day of debate for the UK government's EU Withdrawal bill passed without any hurdles on Tuesday, in a boost for the prime minister, Theresa May.

Meanwhile, the Bank of England's Deputy Governor Ben Broadbent today defended the Bank's rate increase earlier this month, though he gave little away about the path of future hikes.

Commodities continued to struggle on Wednesday, particularly base metals and energy. Copper was down sharply for a second day, slipping 0.75% to $3.037 a ton. Crude oil also extended its losses, falling by over 1% on the day. WTI crude was last trading just under $55 a barrel and Brent crude stood at $61.37. Oil prices came under further pressure today from a surprise build in US crude and gasoline stocks in the Energy Information Administration's latest weekly report.

EURGBP – Bulls Hesitate ahead of Daily Cloud Top

The cross eases below 0.9000 handle which was dented on today's spike to 0.9013, showing strong hesitation at key 0.9026 barriers (daily cloud top/former highs of 10/20 Oct). The price is holding within thick daily cloud and maintaining firm tone, favoring probes above daily cloud.

Meanwhile, some profit-taking on recent rally from 0.8791 may delay immediate bulls, with overbought slow stochastic on daily chart supporting scenario.

Broken 100SMA which holds today's action marks initial support at 0.8947, with daily cloud base (0.8927) expected to hold corrective dips before fresh push higher. Daily Tenkan-sen/Kijun-sen bull-cross which was formed yesterday underpins the action.

Eventual break above daily cloud would open next barrier at 0.9087 (Fibo 61.8% of 0.9306/0.8732 descend).

Res: 0.9013; 0.9026; 0.9046; 0.9087

Sup: 0.8947; 0.8927; 0.8902; 0.8882

USD Losing Positions Without Prospects of Tax Reform

The euro's upward trajectory continues as the greenback falls and more positive macro data is released from the Eurozone. USD investors are frustrated by the decreasing probability of tax reforms being passed by the legislative branch in the US. Expectations of tax cuts were among the main growth drivers for the US dollar throughout this year. At the same time, the EUR/USD bulls were cheered by positive news on the trade balance surplus in the Eurozone which grew to 25.0 billion in September against the 21.2 billion expected.

Even the better than expected retail sales in the US, which came in 0.2% for October, were not able to change the mood on the market. We should note that consumer price index growth by 0.1% in October was in line with the average predictions and has not led to significant changes in the probability of the interest rate hike by the Fed in December.

The British pound has shown a slight increase in volatility following the release of labour market data, according to which the unemployment rate remained at 4.3%. The average earnings index declined by 0.1% to 2.2%, which is 0.1% better than expected.

The preliminary report on GDP in Japan revealed a slowdown in the pace of expansion to 0.3% in the third quarter of this year compared to the 0.4% forecasted. Despite the disappointing news, the USD/JPY kept falling due to investors negative sentiment of the US dollar.

Tomorrow traders will turn their focus to Australian labour market data due at 00:30 GMT and industrial production in the US at 14:15 GMT.

EUR/USD

The EUR/USD keeps growing today and overcoming 1.1825 may become an additional stimulus for continued price increases with potential targets at 1.1925 and 1.2000. Correction is possible down to the support at 1.1730. The MACD signal line has turned around and its decline points to a possible price consolidation or decline soon.

GBP/USD

The British pound was unable to overcome the inclined resistance line and returned to the support at 1.3150. In case of the fall continuing, within the limits of the channel, the quotes may reach 1.3050 and 1.2950. On the other hand, in order to change the trend to positive, quotes need to gain a foothold above 1.3200.

USD/JPY

The USD/JPY price accelerated the pace of decline and touched the lower limit of the descending channel and in case of further decline within the limits of the channel, quotations may reach 111.70. We should note that RSI on the 15-minute chart came close to the oversold territory which signals a possible rebound with potential the target at 113.00.