Sample Category Title

Euro-Zone’s Trade Surplus Surprisingly Widened In September

For the 24 hours to 23:00 GMT, the EUR declined 0.18% against the USD and closed at 1.1775.

On the macro front, the Euro-zone's seasonally adjusted trade surplus surprisingly widened to a record high of €25.0 billion in September, thus countering concerns about the impact of a stronger Euro on exporters. Market participants had anticipated the region's trade surplus to remain steady at €21.0 billion.

The US Dollar trimmed some of its prior losses against other currencies, after a surprise rise in October retail sales as well as an uptick in consumer inflation cemented expectations for an interest rate hike in December.

Data showed that the US consumer price index (CPI) edged up 0.1% on a monthly basis in October, at par with market expectations, after jumping 0.5% in September. Further, the nation's advance retail sales surprised to the upside, rising 0.2% MoM in October, offering further evidence of strength in US consumer spending. Investors had envisaged retail sales record a flat reading, after surging by a revised 1.9% in the prior month. Also, the nation's MBA mortgage applications climbed 3.1% in the week ended 10 November, following a flat reading in the prior week.

Meanwhile, the nation's business inventories remained flat in September, meeting market expectations. In the prior month, business inventories had registered a revised rise of 0.6%. On the other hand, the New York Empire State manufacturing index fell to a level of 19.4 in November, more than market consensus for a drop to a level of 25.1. The index had registered a reading of 30.2 in the prior month.

Meanwhile, the Federal Reserve (Fed) Bank of Boston President, Eric Rosengren, advocated for a December interest rate hike and stated that falling unemployment and sustained economic growth calls for gradual interest rate hikes.

In the Asian session, at GMT0400, the pair is trading at 1.1777, with the EUR trading marginally higher against the USD from yesterday's close.

The pair is expected to find support at 1.1744, and a fall through could take it to the next support level of 1.1710. The pair is expected to find its first resistance at 1.1836, and a rise through could take it to the next resistance level of 1.1894.

Going ahead, traders would keep a close watch on the Euro-zone's final inflation numbers for October, scheduled to release in a few hours. Later in the day, the release of US initial jobless claims followed by industrial and manufacturing production data for October as well as the NAHB housing market index for November, will pique significant amount of market attention.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

UK’s ILO Unemployment Rate Remained Steady At A 4-Decade Low In The Three Months To September

For the 24 hours to 23:00 GMT, the GBP marginally rose against the USD and closed at 1.3169, after UK's ILO unemployment rate remained steady at a 42-year low of 4.3% in the three months to September, meeting market expectations. Further, the nation's average earnings including bonus advanced more-than-anticipated by 2.2% in the July-September period, but remained firmly behind inflation, indicating that the squeeze on consumers may continue for some time. Average earnings including bonus had registered a revised gain of 2.3% in the June-August period, while markets were expecting for a rise of 2.1%.

However, the number of people employed in the nation unexpectedly fell by 14.0K in the July-September period, declining for the first time since October 2016. Markets were expecting employment to rise 52.0K, following an increase of 94.0K in the June-August 2017 period.

In the Asian session, at GMT0400, the pair is trading at 1.3170, with the GBP trading a tad higher against the USD from yesterday's close.

The pair is expected to find support at 1.3131, and a fall through could take it to the next support level of 1.3093. The pair is expected to find its first resistance at 1.3211, and a rise through could take it to the next resistance level of 1.3253.

Moving ahead, market participants will focus on Britain's retail sales data for October, due to release in a few hours. Also, a speech by the Bank of England (BoE) Governor, Mark Carney, due later in the day, will keep investors on their toes.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Japanese Yen Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.52% against the JPY and closed at 112.86.

In the Asian session, at GMT0400, the pair is trading at 113.03, with the USD trading 0.15% higher against the JPY from yesterday’s close.

The pair is expected to find support at 112.58, and a fall through could take it to the next support level of 112.13. The pair is expected to find its first resistance at 113.38, and a rise through could take it to the next resistance level of 113.73.

Amid no major macroeconomic releases in Japan today, Yen investors would look forward to global macroeconomic factors for further direction.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading Marginally Lower This Morning

For the 24 hours to 23:00 GMT, the USD slightly declined against the CHF and closed at 0.9893.

In the Asian session, at GMT0400, the pair is trading at 0.9894, with the USD trading a tad higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9857, and a fall through could take it to the next support level of 0.9820. The pair is expected to find its first resistance at 0.9921, and a rise through could take it to the next resistance level of 0.9948.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Canada’s Existing Home Sales Advanced For A Third Consecutive Month In October

For the 24 hours to 23:00 GMT, the USD rose 0.25% against the CAD and closed at 1.2768.

Macroeconomic data revealed that Canada's existing home sales rose 0.9% on a monthly basis in October, climbing for a third straight month, thus indicating that the nation's housing market remains on a strong footing in the final quarter of the year. Existing home sales had recorded a gain of 2.1% in the previous month.

In the Asian session, at GMT0400, the pair is trading at 1.2767, with the USD trading marginally lower against the CAD from yesterday's close.

The pair is expected to find support at 1.2724, and a fall through could take it to the next support level of 1.2680. The pair is expected to find its first resistance at 1.2800, and a rise through could take it to the next resistance level of 1.2832.

Ahead in the day, Canada's manufacturing shipments for September, will be on investors' radar.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Daily Wave Analysis: Bullish EUR/USD Retraces Tto 50% Fib Level Of Wave-4

Currency pair EUR/USD

EUR/USD reached the 161.8% Fibonacci target of wave 3 (pink) after breaking above the 1.1750 resistance. The current bearish price action could be a retracement within this impulsive wave 3 pattern (pink).

The EUR/USD is probably building multiple wave 3s now. The Fibonacci levels of wave 4 (purple) could act as support and create a potential bouncing spot for a continuation of wave 3 (pink).

Currency pair GBP/USD

The GBP/USD is unable to break the support (blue) and resistance (red) trend lines. A breakout is needed before a larger directional move can be expected, although a bullish breakout still faces resistance from the Fibonacci levels of wave 2 (orange).

The GBP/USD could be expanding the choppy correction via a complex correction of WXY (green).

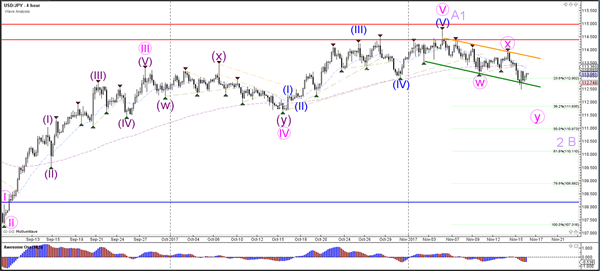

Currency pair USD/JPY

The USD/JPY's choppy bearish trend channel bounced at the 23.6% Fibonacci level. A bearish breakout below the 23.6% Fib could see a drop lower to the Fibonacci levels of wave 2 or wave B (light purple).

The USD/JPY is testing the Fibonacci support and trend line (blue). Price could be building an ABC (blue) within wave B (blue).

Market Update – Asian Session: Aussie Employment Change Lower Than Expected, KRW 13-Month Higher

Headlines/Economic Data

Japan

As of the time of writing, the Nikkei 225 is higher by over 0.7%, after opening down by 0.2%. Nikkei heavy component Fast Retailing has gained over 0.8%.

In the technology space, Canon has moved higher following press speculation that it may raise its annual dividend by ~7%. Meanwhile, shares of Softbank have risen by more than 0.9%.

Casualty insurers are lower amid press speculation that their FY profits may miss forecasts on exposure to hurricanes in the US. USD/JPY has traded steady ahead of the US House vote on its tax bill, expected later on Thursday.

(JP) Japan GDP seen at 1.6% for FY17 v 1.3% in FY16; lifted by strong exports and businesses investing in labor-saving measures – Nikkei

(JP) JAPAN Q3 HOUSING LOANS Y/Y: 2.9% V 3.3% PRIOR

(JP) Japan MoF sells ¥800B v ¥1.0T offered in 0.6% 20-yr JGBS; avg yield 0.573%; bid-to-cover 4.13x

(JP) Japan PM Abe top economic advisory panel in a draft will suggest they see economy closer to deflation exodus - financial press

Korea

The Kospi has gained over 0.3%, amid more than 0.5% gains in shares of Samsung Electronics.

More action has, however, been seen in the currency markets, as the Korean Won has hit the highest level against the US dollar since Oct 2016. On Wednesday, the Bank of Korea and Bank of Canada announced a bilateral currency swap agreement.

The agreement is expected to have limited direct impact on FX rates, says a Bank of Korea Deputy Gov. Even still, South Korea’s Finance Ministry reiterated that it would closely monitor markets in cases of ‘severe volatility.’

USD/KRW Onshore opens at KRW1,106 (13-month high) v KRW1,112 prior close

China/Hong Kong

The Shanghai Composite opened the session -0.3%, while the Hang Seng opened +0.4%. The Information Technology index in Hong Kong has risen by over 1%. Component, Tencent, has gained over 1.7% after reporting better than expected Q3 results.

The Hang Seng Energy index is trading lower by over -0.1%. Gasoline and diesel prices may be raised in China by as soon as Friday, according to a press report.

The Hang Seng Property Index is little changed. Banks in China are said to be conducting stress tests related to loans made to the property sector, according to a local press report.

China Legislature Official Huang said China should levy a property tax as it curbs speculation. China should also reform its FX reserves system and have the MOF play a larger management role, says the official.

Separately, the PBoC’s Research Head said there could be the risk of a ‘big crisis’ if economic reforms are too slow.

(CN) China port names moving higher on chatter that China could cut shipping fees

(CN) China may raise gasoline prices by CNY265/ton and diesel prices by CNY250/ton as of Friday

USD/CNY (CN) PBOC sets yuan reference rate at 6.6286 v 6.6263 prior

(CN) China PBoC Open Market Operations (OMO): CNY330B v CNY330B injected in 7, 14 and 63-day reverse repos prior; Net injection CNY310B v CNY220B prior

(CN) China Oct YTD Outbound Investments $86.3B, -40.9% y/y in USD terms

Australia/New Zealand

(AU) AUSTRALIA OCT EMPLOYMENT CHANGE: +3.7K V +18.8KE; UNEMPLOYMENT RATE: 5.4% V 5.5%E

Full-Time Employment Change: 24.3K v +6.1K prior

Part-Time Employment Change: -20.7K v +13.7K prior

Participation Rate: 65.1% v 65.2%e

AUD was little changed after an initial spike higher, little reaction in the bond market

(AU) Australia Nov Consumer Inflation Expectation y/y: 3.7% v 4.3% prior

(NZ) New Zealand Nov ANZ Consumer Confidence Index: 123.7 v 126.3 prior; M/M: -2.1% v -2.8% prior (7-month low)

(NZ) New Zealand sells NZ$200M in Apr 2025 bonds; avg yield 2.6711%

Other Asia

In the Philippines, the Peso currency and equity markets are moving higher following Q3 GDP data. The y/y figure rose by a better than expected 6.9%.

The economy is still not overheating, according to the Philippines Central Bank Chief Espenilla.

North America

(CA) Bank of Canada (BOC) Wilkins: Reason for caution is desire to avoid policy reversal, motivated by lower than expected inflation

(US) Christie's auction sells last privately held Leonardo da Vinci painting entitled 'Salvator Mundi' for record $450M (expected $100M+)

Ahead of the expected vote, US President Trump said tax cuts are getting ‘close.’

Various US companies have priced secondary offerings following the NY close and ahead of the expected tax vote (including JELD, STKS, NCLH, ACHN and GDI). Floor & Décor Holdings also priced a 6.5M share secondary, which was below the originally planned 9M shares.

Levels as of 23:00ET

Nikkei +0.7%, Hang Seng +0.5%; Shanghai Composite -0.1%; ASX200 +0.1%, Kospi +0.5%

Equity Futures: S&P500 +0.2%; Nasdaq100 +0.3%, Dax +0.2%; FTSE100 +0.1%

EUR 1.1792-1.1769; JPY 113.05-112.76; AUD 0.7609-0.7569;NZD 0.6878-0.6850

Dec Gold +0.1% at $1,278/oz; Dec Crude Oil +0.0% at $55.34/brl; Dec Copper +0.2% at $3.06/lb

Equities notable movers

Australia/New Zealand

STO.AU Not currently engaged in talks, received earlier takeover approach from Harbour Energy at A$4.55/shr; +11%

RKN.AU Sells Accountants Practice Management business to MYOB (as expected) for A$180M cash; to pay special dividend; +33%

Hong Kong/China

700.HK Reports Q3 (CNY) Net 18.0B v 15.7Be, Rev 65.2B v 61Be; +1.5%

410.HK Approves special interim dividend of CNY0.576; +8.7%

4.HK Announces share price adjustment after spinoff of Wharf Estates; -63%

US

TIME Said to be in talks regarding selling itself to Meredith - US press

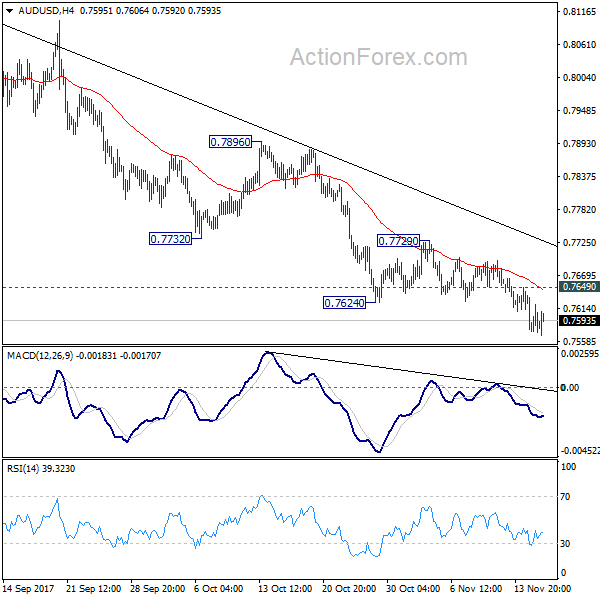

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7563; (P) 0.7598; (R1) 0.7622; More...

Intraday bias in AUD/USD remains on the downside with 0.7649 minor resistance intact. Current fall from 0.8124 is expected to target next key cluster level at 0.7322/8. On the upside, above 0.7649 minor resistance will turn intraday bias neutral. But outlook will stay bearish as long as 0.7729 resistance holds.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8067). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7896 near term resistance holds.

Dollar Recovering Mildly as Sentiments Stabilized, Aussie Stays Weak after Job Data

US equities generally lower overnight as the global market rout continued, but sentiments stabilized in Asian session. DOW lost -138.19 pts, or -0.59% to end at 23271.28. It breached 23251.11 near term support during the day, which could seen as a sign of near term reversal. 10 year yield also followed lower, down -0.046 at 2.335 but it s held well above 2.273 structural support so far. Meanwhile, Dollar is trying to recovery after the deep selloff, in particular against Euro, earlier in the week. Overall, the sell off in oil is seen as a factor driving risk aversion. But WTI might now be stabilizing around 55 handle. Another risk averse factors emerges as US politicians are raising doubts on the legislation of the tax plan.

Senator Johnson and Collins oppose Republican tax bill

In US, Republican effort to push through the tax cuts before year end suffered serious setbacks yesterday. Republican Senator Ron Johnson openly expressed his opposition to both the Senate and House versions of the tax bill. He criticized that the plan benefits large corporations at the expense of the others, including smaller companies. Republican Senator Susan Collins also criticized the move to include the never-ending repeal of Obamacare in the tax bill.

Boston Fed Rosengren supports December hike

Boston Fed President Eric Rosengren, a hawk, said yesterday that "it is quite likely that unemployment will fall below 4 percent, which is likely to increase pressures on inflation and asset prices." And, "that suggests the need to continue to gradually remove monetary policy accommodation, which is quite consistent with market expectations of another increase in December."

ECB Praet talked the move back to conventional measures

ECB Chief Economist Peter Praet laid out the path that the central bank is moving from unconventional measures to conventional measures in policy setting. He noted that "as we progress towards a sustained adjustment in the path of inflation and approach the time when net purchases will gradually come to an end, the residual monetary support needed to assist the economy in its transition to a new normal will increasingly come from forward guidance on our policy rates." Then, "policy rates will eventually regain their status as the main instrument of policy, and our forward guidance will revert to a singular approach."

ECB Hansson: The world looks better to us

ECB Governing Council member Ardo Hansson sounded optimistic as he said "the world looks better to us" and the economy is enjoying "strong growth". Also, "with greater confidence in the outlook for the real economy there is some scope for a prudent but obvious recalibration of policies." Regarding policy, he emphasized that "one of my colleagues always likes to say monetary policy is not a solo, it's a quartet: you have the asset purchases, the accumulated stock of purchases, the re-investment policy and forward guidance."

AU job growth missed, unemployment rate at 4.5 year low

Australian Dollar recovers mildly today after job data, but stays near term bearish. Employment market grew 3.7k in October, slowed from prior month's 26.6k and missed expectation of 18.9k. Nonetheless, full time jobs grew 24.3k while part time jobs dropped -20.7k. Also, Unemployment rate, dropped to 5.4%, down from 5.5%. That's also the lowest reading since February 2013. Also from Australia, consumer inflation expectation rose 3.7% in November.

RBA Assistance Governor Luci Ellis said yesterday that there more growth engines in the country other than mining. She pointed out that infrastructure spending, tourism and services as some examples. Also, the economy would be supported by relatively fast population growth and pickup in participation. In addition, there will be "indirect effects" from better infrastructure that boost productivity.

Looking ahead

UK retail sales will be the main focus in European session. Eurozone will release CPI final. Later in the data. US will release jobless claims, Philly Fed survey, import price index, industrial production and NAHB housing index. Canada will release manufacturing sales and international securities transactions.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7563; (P) 0.7598; (R1) 0.7622; More...

Intraday bias in AUD/USD remains on the downside with 0.7649 minor resistance intact. Current fall from 0.8124 is expected to target next key cluster level at 0.7322/8. On the upside, above 0.7649 minor resistance will turn intraday bias neutral. But outlook will stay bearish as long as 0.7729 resistance holds.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8067). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7896 near term resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:00 | AUD | Consumer Inflation Expectation Nov | 3.70% | 4.30% | ||

| 0:30 | AUD | Employment Change Oct | 3.7K | 18.9K | 19.8K | 26.6K |

| 0:30 | AUD | Unemployment Rate Oct | 5.40% | 5.50% | 5.50% | |

| 9:30 | GBP | Retail Sales M/M Oct | 0.20% | -0.80% | ||

| 10:00 | EUR | Eurozone CPI M/M Oct | 0.10% | 0.40% | ||

| 10:00 | EUR | Eurozone CPI Y/Y Oct F | 1.40% | 1.50% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Oct F | 0.90% | 0.90% | ||

| 13:30 | CAD | Manufacturing Sales M/M Sep | -0.20% | 1.60% | ||

| 13:30 | CAD | International Securities Transactions (CAD) Sep | 9.85B | |||

| 13:30 | USD | Initial Jobless Claims (NOV 11) | 234k | 239k | ||

| 13:30 | USD | Philly Fed Manufacturing Index Nov | 24.1 | 27.9 | ||

| 13:30 | USD | Import Price Index M/M Oct | 0.40% | 0.70% | ||

| 14:15 | USD | Industrial Production M/M Oct | 0.50% | 0.30% | ||

| 14:15 | USD | Capacity Utilization Oct | 76.30% | 76.00% | ||

| 15:00 | USD | NAHB Housing Market Index Nov | 67 | 68 | ||

| 15:30 | USD | Natural Gas Storage | 15B |

Elliott Wave View: SPX Intra-Day

SPX Intra Day Elliott Wave view suggests that the rally to 2597.02 ended Intermediate wave (3). Intermediate wave (4) pullback is currently in progress as a double three Elliott Wave structure. Down from 2597.02, Minor wave W of (4) ended at 2566.33 and Minor wave X of (4) ended at 2587.66. While staying below 2597.02, expect the Index to continue lower towards 2538 – 2557 area to finish Intermediate wave (4) before Index resumes the rally or bounce in 3 waves at least. We don’t like selling the Index and expect dip buyers to appear from the aforementioned area for at least a 3 waves bounce.

SPX 1 Hour Elliott Wave Analysis