Sample Category Title

Elliott Wave View: FTSE Short-Term

Short term FTSE Elliott Wave view suggests that Primary wave ((4)) ended with the decline to 7199.5. The rally up from there is unfolding as a zigzag Elliott Wave structure where Intermediate wave (A) ended at 7565.11 and Intermediate wave (B) ended at 7437.42. Intermediate wave (A) has a subdivision of an impulse Elliott Wave structure where Minor wave 1 ended at 7327.5, Minor wave 2 ended at 7289.75, Minor wave 3 ended at 7527.72, Minor wave 4 ended at 7493.68, and Minor wave 5 of (A) ended at 7565.11.

Intermediate wave (B) pullback unfolded as a double three Elliott Wave structure. Minor wave W of (B) ended at 7485.42, Minor wave X of (B) ended at 7560.04, and Minor wave Y of (B) ended at 7437.42. Intermediate wave (C) is currently in progress in 5 waves. The rally from 7437.42 low is unfolding as a diagonal where Minute wave ((i)) ended at 7532.36, Minute wave ((ii)) ended at 7478.88, Minute wave ((iii)) ended at 7580.93, and Minute wave ((iv)) ended at 7541.91. Near term, expect the Index to see another leg higher in Minute wave ((v)) before Minor wave 1 is complete and cycle from 10/25 low ends. Afterwards, Index should pullback in Minor wave 2 to correct cycle from 10/25 low in 3, 7, or 11 swing before the rally resumes. We don't like selling the Index.

FTSE 1 Hour Elliott Wave Analysis

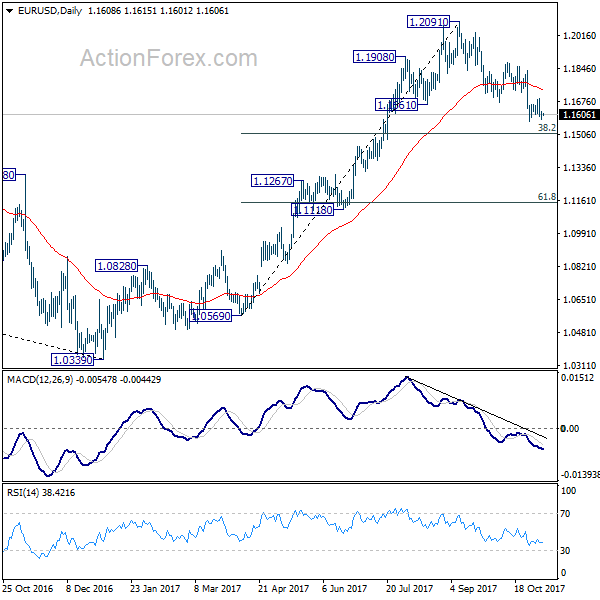

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1585; (P) 1.1604 (R1) 1.1629; More...

EUR/USD is still bounded in consolidation from 1.1574 and intraday bias stays neutral. But after all, break of 1.1879 resistance is needed to confirm completion of the decline from 1.2091. Otherwise, near term outlook will stay bearish. Below 1.1574 will target 38.2% retracement of 1.0569 to 1.2091 at 1.1510.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be cautious on 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

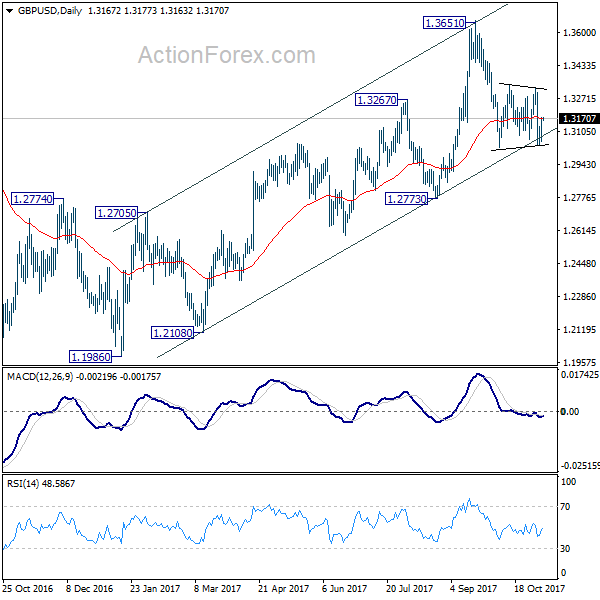

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3095; (P) 1.3135; (R1) 1.3211; More....

Strong rebound from 1.3038 suggests that fall from 1.3651 is not ready to resume yet. And, consolidation from 1.3026 is extending with another leg. While further rise cannot be ruled out, upside should now be limited below 1.3337 to bring fall resumption eventually. Break of 1.3038 will now resume decline from 1.3651 to 1.2773 key support level. However, decisive break of 1.3337 will indicate that pull back from 1.3651 is completed and medium term rise from 1.1946 is resuming.

In the bigger picture, as noted before, GBP/USD hit strong resistance from the long term falling trend line. Current development is starting to favor that corrective rebound from 1.1946 low has completed at 1.3651. Decisive break of 1.2773 will confirm this bearish case and target a test on 1.1946 low next, with prospect of resuming the low term down trend. Nonetheless, break of 1.3320 resistance will restore the rise from 1.1946 for 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

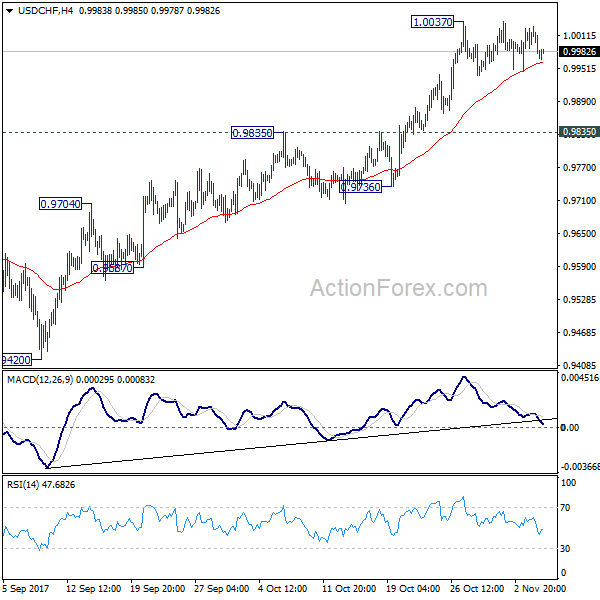

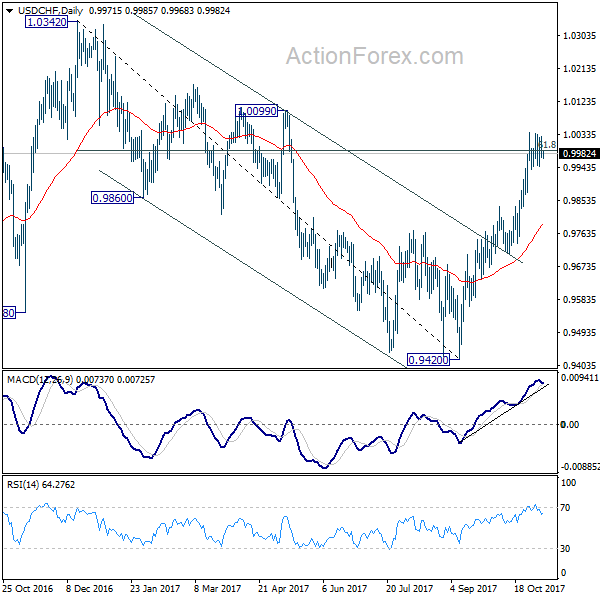

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9954; (P) 0.9991; (R1) 1.001; More....

Intraday bias in USD/CHF remains neutral as consolidation from 1.0037 is still in progress. Deeper retreat could be seen. But downside should be contained above 0.9835 resistance turned support and bring rally resumption. On the upside break of 1.0037 will resume whole rally from 0.9420. And with sustained trading above 61.8% retracement of 1.0342 to 0.9420 at 0.9990, USD/CHF should then target a test on 1.0342 key resistance.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could is a medium term up move and should target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9736 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

USD/JPY Daily Outlook

Daily Pivots: (S1) 113.35; (P) 114.04; (R1) 114.39; More...

USD/JPY failed to sustain above 114.49 key resistance and retreated. Intraday bias is turned neutral again. As long as 112.95 support holds, near term outlook remains bullish and further rally is in favor. Sustained trading above 114.49 will pave the way to retest 118.65 high. However, break of 112.95 support will now indicate rejection from 114.49 and turn bias to the downside for 111.64 support and below.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming.

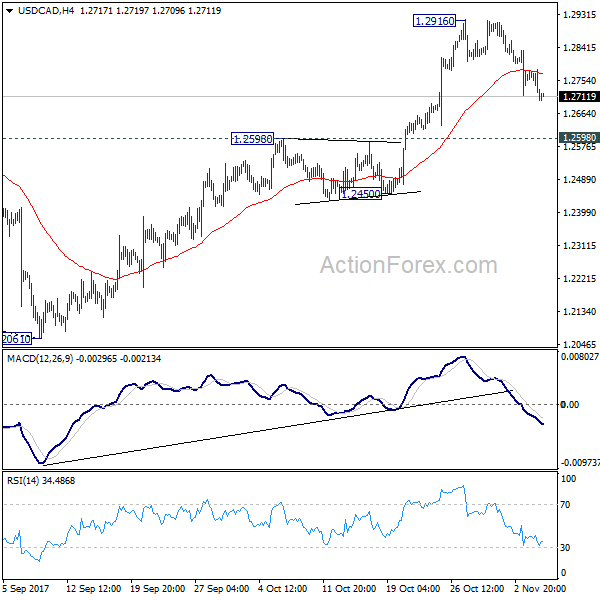

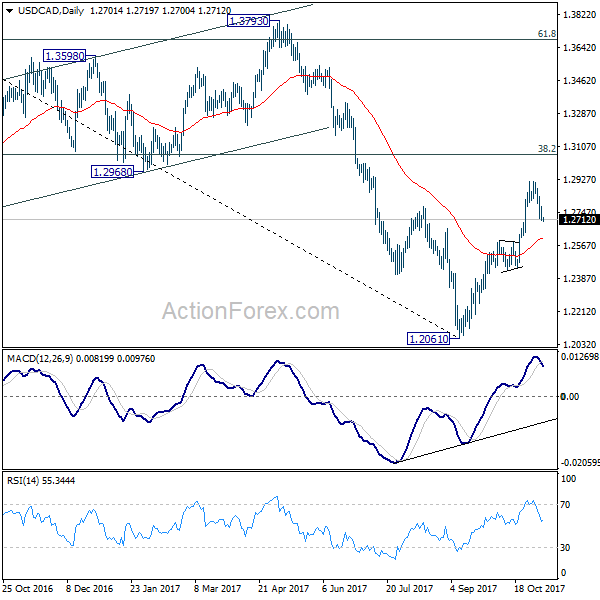

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2677; (P) 1.2729; (R1) 1.2756; More....

USD/CAD's pull back from 1.2916 extended lower but it's still kept well above 1.2598 8 resistance turned support. Near term outlook stays bullish and another rise is expected. On the upside, break of 1.2916 will extend the rise from 1.2061 to 38.2% retracement of 1.4689 to 1.2061 at 1.3065. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2916). Near term outlook will be turned bearish in this case.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

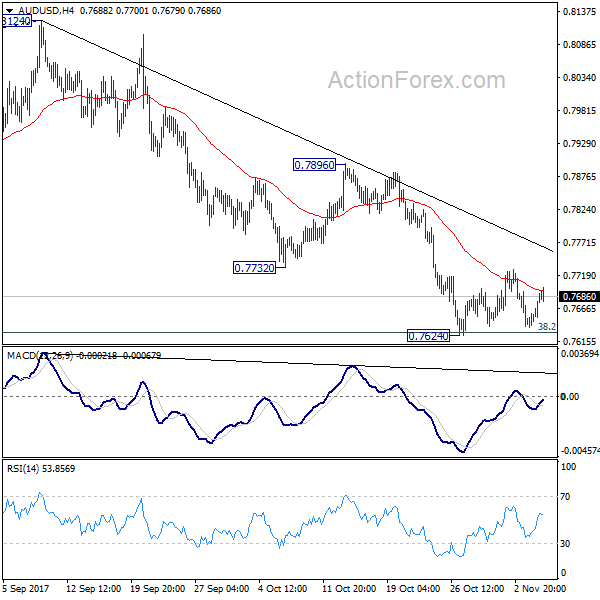

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7655; (P) 0.7673; (R1) 0.7708; More...

AUD/USD recovers ahead of 0.7624 support as consolidation continues. Intraday bias remains neutral first. Near term outlook remains bearish with 0.7896 resistance intact and deeper fall is expected. Decisive break of 0.7624 will resume whole decline from 0.8124. And, AUD/USD should target next key cluster level at 0.7322/8 next.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8067). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7896 near term resistance holds.

Risk Appetite Stays in Financial Markets, Aussie Steady after RBA

The financial markets continued to trade with risk appetite this week. DOW managed to make another record high despite a mere 9.23 pts rise. S&P 500 and NASDAQ performed slightly better and gained 0.13% and 0.33% respectively, both at new records. FTSE was also firm yesterday and gained 0.03% to new record close at 7562.28. While that was below intraday record at 7598.99, that was enough to help lift Sterling for a rebound. GBP/USD is temporary safe after failing to break through 1.3026 key support following post BoE selloff. Meanwhile, Aussie trades steadily after RBA left cash rate unchanged at 1.50% as widely expected, with a carbon copy statement.

NAO warned of Brexit risks to public finances

In a report by National Audit Office, Head Amyas Morse warned that "public and private borrowing are high, kept affordable by record low interest rates, and quantitative easing continues 10 years after the crisis it responded to". The report pointed out that since 2009, UK government borrowing had increased by 61%. Interest payments have already cost the government GBP 222b. And with the use of index-linked gilts, a rise of 1% in inflation could add GBP 26b in interest between 2016-18 and 2020-21.

Morse added that "there are significant risks to the public finances and any unexpected developments, potentially including consequences of leaving the EU could exacerbate them. In these circumstances, the Treasury needs to constantly monitor these risks and be ready to react quickly and flexibly. It has taken steps to increase its capacity to respond."

More reports on Brexit assessments will be published this week. John Bercow, the Speaker of the House of Commons, has set the government a deadline of Tuesday evening to publish the Brexit assessments demanded by parliament. That came after the parliament voted unanimously last week to call on Brexit Secretary David Davis to release all the details.

Eurogroup agree to ECB approach on bad loans

Eurogroup head Jeroen Dijsselbloem said in a press conference after the meeting of Eurozone finance ministers yesterday. He noted that there was "a general agreement" on ECB's approach to tackle bad loans of banks in the region. And, it's believed that it's the right time to proceed with tougher measures to avoid the build up of so called non-performing loans by Eurozone financial institutions. EUR 1T of bad loans were accumulated after the financial crisis. And that has only be reduced to EUR 0.8T decently.

German Merkel to complete exploratory coalition talks in 10 days

In Germany, Chancellor Angela Merkel named out the clearly differences between her potential coalition partners. But she wants to end the exploratory talks to complete by November 16 and launch serious negotiations then.. Merkel noted that immigration and climate policy are the most contentious issues between the pro-business Free Democrats and the Greens.

NY Fed Dudley confirmed early retirement

The influential New York Fed President William Dudley confirmed his plan of early retirement, just four days after Jerome Powell was named as nomination to take our Janet Yellen as Fed chair by President Donald Trump. Dudley gave special thank to former Treasury Tim Geithner, former Fed chair Bernanke and Yellen for "giving me the opportunity to work closely with them during the crisis and the subsequent economic recovery."

Together with Yellen and former Vice Chair Stanley Fischer who stepped down in October, the Fed will be missing the three most important figures starting next year. The overhaul in Fed could bring fresh ideas into the most important central bank of the world. But at the same time, drastically reduce the experience level in crisis management.

On the data front

Japan labor cash earnings rose 0.9% yoy in September. UK BRC retail sales monitor dropped -1.0% yoy i9n October. German industrial production, Swiss, foreign currency reserves, Eurozone retail sales and retail PMI will be featured today.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7655; (P) 0.7673; (R1) 0.7708; More...

AUD/USD recovers ahead of 0.7624 support as consolidation continues. Intraday bias remains neutral first. Near term outlook remains bearish with 0.7896 resistance intact and deeper fall is expected. Decisive break of 0.7624 will resume whole decline from 0.8124. And, AUD/USD should target next key cluster level at 0.7322/8 next.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8067). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7896 near term resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:00 | JPY | Labor Cash Earnings Y/Y Sep | 0.90% | 0.50% | 0.90% | 0.70% |

| 0:01 | GBP | BRC Retail Sales Monitor Y/Y Oct | -1.00% | 0.90% | 1.90% | |

| 3:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 7:00 | EUR | German Industrial Production M/M Sep | -0.80% | 2.60% | ||

| 8:00 | CHF | Foreign Currency Reserves (CHF) Oct | 724B | |||

| 9:10 | EUR | Eurozone Retail PMI Oct | 52.3 | |||

| 10:00 | EUR | Eurozone Retail Sales M/M Sep | 0.60% | -0.50% |

Market Morning Briefing: Dollar-Yen Had Risen To 114.73

STOCKS

Dow (23548.42, +0.04%) is almost stable but the upside is open to test 23800 in the coming sessions. Near to medium term looks bullish.

Dax (13468.79, -0.07%) is likely to trade sideways in the 13500-13400 region for a few sessions before again resuming the uptrend. A break below 13400, if seen could take it down to 13300-13200 in the longer term.

Nikkei (22724.86, +0.78%) continues to rise higher and our earlier target of 22666 was unable to stop the upward momentum. Looking at the 3-day candles, there is scope of testing 23000-23500 levels in the coming sessions before a medium term top formation takes place. Important to see if 115 could be a decent top for the medium term on Dollar Yen. A corrective dip in Dollar Yen could prevent further rise in Nikkei.

Shanghai (3406.62, +0.54%) bounced back from 3360 as expected and could now move up towards 3425-3430 levels in the near term. Overall the short term upward channel from May’17 is likely to remain intact with an upside potential of 3450 in the medium term.

Nifty (10451.80, -0.01%) stayed above immediate support near 10400 and while that holds, the index could be sideways range-bound in the 10400-10500 region. In case it breaks below 10400, we could see a test of 10300 or slightly lower in the medium term.

COMMODITIES

Gold (1279.64) has bounced back from immediate support near 1265 as expected. Range-trade within 1260-1290 is accounted for the week with a possible extension towards 1295-1300 levels. Note that 1260 is a decent support as seen on the daily candles and is likely to hold in the coming sessions.

Both the Brent (64.14) and the WTI (57.25) have moved up sharply yesterday after news of high profile arrests in Saudi Arabia on an anti-corruption crackdown. Brent is trading near immediate resistance and could possibly pause before again moving up higher while WTI can test 59 before coming off from there.

Copper (3.1535) looks bullish towards 3.25-3.30 for the coming sessions and could well remain above support of 3.05 this week. Near to medium term looks bullish.

FOREX

Slight dip in the Dollar Index (94.78) which has come down from an overnight high near 95.07. The Euro (1.1608) has also recovered a bit from a low near 1.1580. However, the overall uptrend in the Dollar Index remains in force while above 94.50 and the overall downtrend remains in force on the Euro while below 1.1620 (immediate Resistance) and 1.1670 (higher Resistance). The targets are 95.50 on Dollar Index and 1.1550-30 on the Euro.

Dollar-Yen (113.78) had risen to 114.73 yesterday morning but came off sharply from there. It may try to test lower levels of 113.40 over the next couple of days while below 114.50. The Euro-Yen (132.16) has come down alongwith Dollar-Yen. Look for a relatively wide range of 131-134 over the coming days.

As it turns out, the Pound (1.3166) held above trendline Support near 1.3050 and has moved higher. A test of 1.33 looks more possible now. The Aussie (0.7686) also moved up a bit from 0.7630 but looks mixed between 0.7630-7730 for a few days.

Dollar-Yuan (USDCNY = 6.6265) trades a wee bit lower and could spend some time sideways between 6.61-65 for a few days. Dollar-Rupee (64.68) trades a little lower near 62.65 on the NDF. Support should be available in the 64.60-55 region.

INTEREST RATES

Bond Yields continue to dip across the globe even though Brent (64.10) has seen a sharp rise. This is a bit of a surprise for us.

In USA, the 30Yr (2.80%) may have an important Support near 2.78%. This is to be watched. The Yield Curve has been flattening sharply over the last few days but maybe there is some scope for a bounce from near current levels for the 30-5 (0.81%) and 30-10 (0.47%).

The German 10Yr (0.34%) has dipped further and now trades well below 0.40% suggesting that the uptrend since -0.1% (Oct-16) could be breaking.The German-US 10Yr Spread (-1.99%) has bounced from -2.05% over the last few days, but could be vulnerable to a fresh fall from current levels.

Japanese Yields (10Yr 0.03%, 5Yr -0.12%) have been falling over the last few days. The 5Yr may find Support near -0.14%.

(RBA) Statement by Philip Lowe, Governor: Monetary Policy Decision

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

Conditions in the global economy are continuing to improve. Labour markets have tightened and further above-trend growth is expected in a number of advanced economies, although uncertainties remain. Growth in the Chinese economy is being supported by increased spending on infrastructure and property construction, with the high level of debt continuing to present a medium-term risk. Australia's terms of trade are expected to decline in the period ahead but remain at relatively high levels.

Wage growth remains low in most countries, as does core inflation. Headline inflation rates are generally lower than at the start of the year, largely reflecting the earlier decline in oil prices. In the United States, the Federal Reserve has started the process of balance sheet normalisation and expects to increase interest rates further. In a number of other major advanced economies, monetary policy has become a bit less accommodative. Equity markets have been strong, credit spreads have narrowed and volatility in financial markets remains low.

The Bank's forecasts for growth in the Australian economy are largely unchanged. The central forecast is for GDP growth to pick up and to average around 3 per cent over the next few years. Business conditions are positive and capacity utilisation has increased. The outlook for non-mining business investment has improved, with the forward-looking indicators being more positive than they have been for some time. Increased public infrastructure investment is also supporting the economy. One continuing source of uncertainty is the outlook for household consumption. Household incomes are growing slowly and debt levels are high.

The labour market has continued to strengthen. Employment has been rising in all states and has been accompanied by a rise in labour force participation. The various forward-looking indicators continue to point to solid growth in employment over the period ahead. The unemployment rate is expected to decline gradually from its current level of 5½ per cent. Wage growth remains low. This is likely to continue for a while yet, although the stronger conditions in the labour market should see some lift in wage growth over time.

Inflation remains low, with both CPI and underlying inflation running a little below 2 per cent. In underlying terms, inflation is likely to remain low for some time, reflecting the slow growth in labour costs and increased competitive pressures, especially in retailing. CPI inflation is being boosted by higher prices for tobacco and electricity. The Bank's central forecast remains for inflation to pick up gradually as the economy strengthens.

The Australian dollar has appreciated since mid year, partly reflecting a lower US dollar. The higher exchange rate is expected to contribute to continued subdued price pressures in the economy. It is also weighing on the outlook for output and employment. An appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast.

Growth in housing debt has been outpacing the slow growth in household income for some time. To address the medium-term risks associated with high and rising household indebtedness, APRA has introduced a number of supervisory measures. Credit standards have been tightened in a way that has reduced the risk profile of borrowers. Housing market conditions have eased further in Sydney. In most cities, housing prices have shown little change over recent months, although they are still increasing in Melbourne. In the eastern capital cities, a considerable additional supply of apartments is scheduled to come on stream over the next couple of years. Rent increases remain low in most cities.

The low level of interest rates is continuing to support the Australian economy. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.