Sample Category Title

Market Update – Asian Session: RBA Leaves Rates, Higher Oil Prices Lend Regional Names Strength

Asia Summary

Asian equity markets are trading generally higher following Monday's gains in the NY trading session. The Nikkei 225 has traded at a 25-year high, as the Topix Securities broker index has risen by over 1%.

Australia's ASX 200 index has traded at the highest level since Feb 2008. BHP and Rio Tinto have gained over 2%, and the overall ASX Resources index is up more than 1.5%.On yesterday's session, copper prices rose by 1%, while oil prices gained over 3%.

With the recent gain in crude oil prices, the ASX and Hang Seng Energy indices have gained over 1% on the session.

The Hong Kong property, conglomerates and consumer goods indices are also currently gaining. South Korean department store operator, Shinsegae, has risen by over 7%, as its Q3 revenues rose by more than 34%.

South Korean chip makers are trading mixed. Shares of Samsung Electronics have gained on the session. Hynix has, however, lagged amid the earlier decline seen in the share price of Micron. Taiwan Semi is trading up by over 0.6%. In Q1, contract prices for DRAM may rise on demand from Apple, according to a Taiwanese press report. In Hong Kong, the Information Technology Index has gained over 0.5%, as shares of Tencent have risen by more than 1%. The company's eBook business, China Literature, has risen by over 30% in the gray market ahead of its IPO in Hong Kong. Softbank has traded marginally lower, following its recent earnings report.

Steelmakers in Japan are trading mixed. Nippon Steel and JFE have gained over 1.5%, while shares of Kobe Steel have lagged. In the auto space, Toyota, has traded lower by over 0.6%, ahead of its later today earnings report. In Hong Kong, Geely Automobile has traded higher by over 3%, as it reported record vehicle sales for the month of October. The ASX 200 REIT index has gained over 0.9%

Australia's 3-year bond yields are higher on the session and the Aussie is little changed amid the Reserve Bank of Australia's decision to keep rates unchanged (as expected). The central bank, however, in its policy statement said core inflation is likely to remain low for some time on slow growth in labor costs and higher competitive pressures, particularly in retailing. The central bank also said one continuing source of uncertainty is the outlook for household consumption. These comments came, as Australia's retail sales have missed market expectations for 3 straight months.

Looking ahead, the RBA is due to release its Quarterly Monetary Statement and economic forecasts on Friday's session.

Japanese companies expected to report earnings later today include, Ajinomoto, Asahi Kasei Corp, Brother Industries, COMSYS Holdings, Daikin Industries, Fuji Oil Holdings, Istean Mitsukoshi Holdings, Kubota, Nikon Corp, NTT Data and Sumitomo Electric.

Key economic data

(AU) RESERVE BANK OF AUSTRALIA (RBA) LEAVES CASH RATE TARGET UNCHANGED AT 1.50%; AS EXPECTED (15TH CONSECUTIVE HOLD IN CURRENT EASING CYCLE)

(JP) Japan Sept Labor Cash Earnings Y/Y: 0.9% v 0.5%e; Real Cash Earnings Y/Y: -0.1% v -0.2%e

(AU) Australia Oct AiG Performance of Construction Index 53.2 v 54.7 prior

Speakers and Press

Japan

(JP) Japan Fin Min Aso: US forces are important for Japan security, will not pursue FTA to reduce US trade deficit

(JP) Japan Dep Chief Cabinet Sec Nishimura: Trump and Abe did not discuss any bilateral Free trade Agreement (FTA)

Korea

(KR) South Korea FX Official: Closely monitoring FX markets, FX policy stance stays the same as Fin Min comments last week

Australia/New Zealand

(NZ) New Zealand PM Arden: Not at all concerned about recent declines in NZ$

(NZ) New Zealand Fin Min Robertson: Expect business confidence to recover

(NZ) New Zealand Fin Min Robertson and acting Gov Spencer have signed an unchanged Policy Targets agreement (PTA)

(NZ) New Zealand Treasury: Q3 GDP may be 0.6%, slower than expected; GDP growth is expected to pick up in Q4 - Monthly Economic Indicators

China/Hong Kong

(CN) China Commerce Ministry (MOFCOM):foreign trade conditions are expected to be generally favorable in 2018 amid a steadily improving global economy

(CN) China Banking Association economist Ba Shusong: China should strengthen efforts to internationalize the yuan - China Financial News

Asian Equity Indices/Futures (23:00ET)

Nikkei +1.3%, Hang Seng +1.2%; Shanghai Composite +0.6%; ASX200 +0.8%, Kospi -0.1%

Equity Futures: S&P500 +0.1%; Nasdaq100 +0.2%, Dax +0.1%; FTSE100 +0.2%

FX ranges/Commodities/Fixed Income (23:00ET)

EUR 1.616-1.1602; JPY 113.94-113.70; AUD 0.7701-0.7679;NZD 0.6954-0.6933

Dec Gold -0.1% at $1,280/oz; Dec Crude Oil +0.1% at $57.41/brl; Dec Copper -0.2% at $3.15/lb

(CN) PBoC OMO: injects CNY180B in 7-day, 14-day and 63-day reverse repos prior v skips prior; Net drain CNY80B v injection CNY160B prior (1st injection after 3 consecutive skips)

USD/CNY *(CN) PBOC SETS YUAN REFERENCE RATE AT 6.6216 V 6.6247 PRIOR

(TH) Thailand Central Bank sells THB115B in 3-month, 6-month and 301-day central bank bonds

Equities notable movers

Australia/New Zealand

TWR.NZ Suncorp will not appeal NZCC's decision to decline its application to acquire Tower; -6.8%

Japan

6005.JP Reports H1 Net ¥4.8B +25% y/y; Op ¥6.70B +15.8% y/y; +9.5%

6849.JP Reports H1 Net -¥546M v ¥1.7B y/y; Op ¥3.1B v ¥3.8B y/y; -6%

Korea

000720.KR Receives KRW582.06B contract in Busan; +8%

Hong Kong

1169.HK Controlling shareholder unit planning exchangeable bond sale; -4.4%

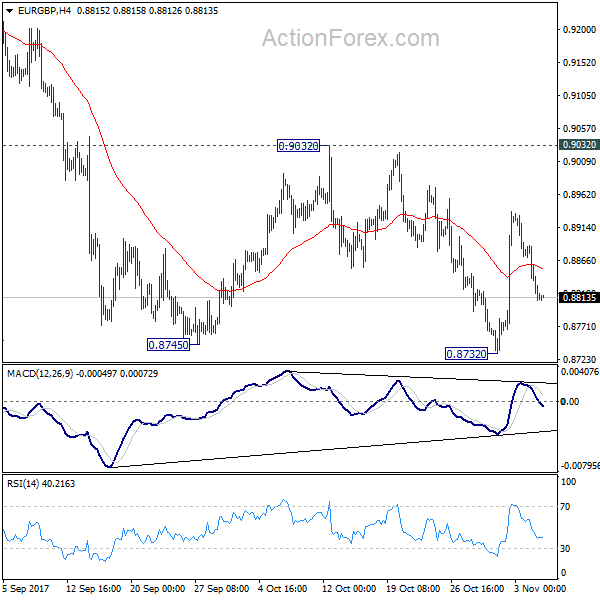

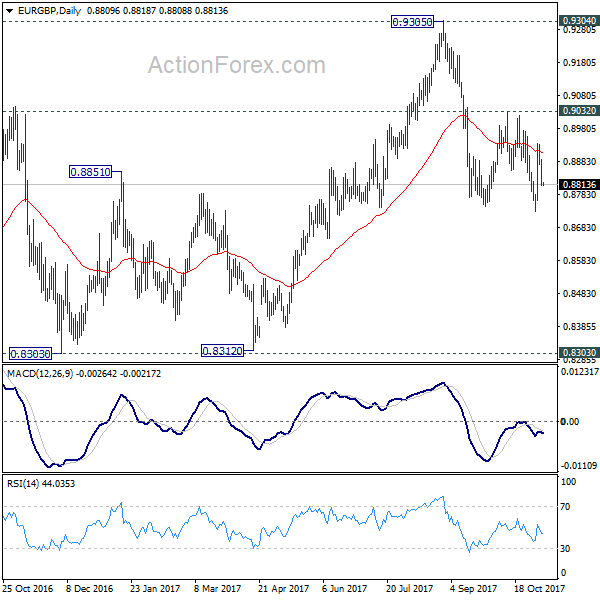

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8785; (P) 0.8837; (R1) 0.8863; More...

At this point, intraday bias in EUR/GBP remains neutral at the moment. On the upside, decisive break of 0.9032 will confirm completion of the decline from 0.9305. In such case, intraday bias will be turned back to the upside for retesting 0.9305 key resistance. On the on the downside, break of 0.8732 will resume the fall and target 0.8303 key support level instead.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

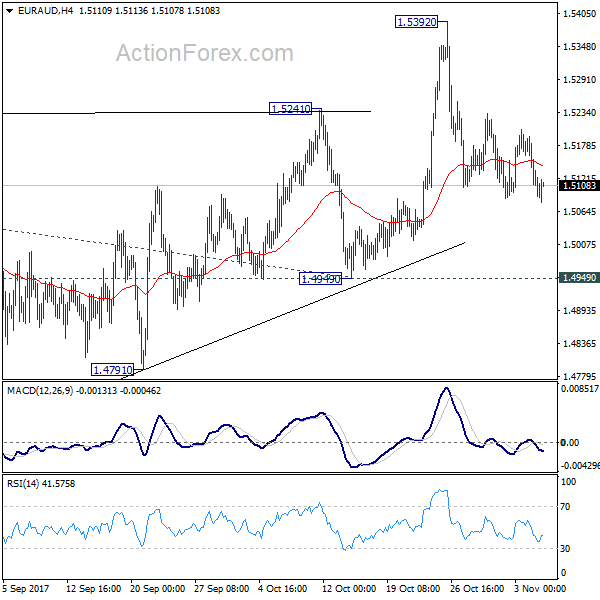

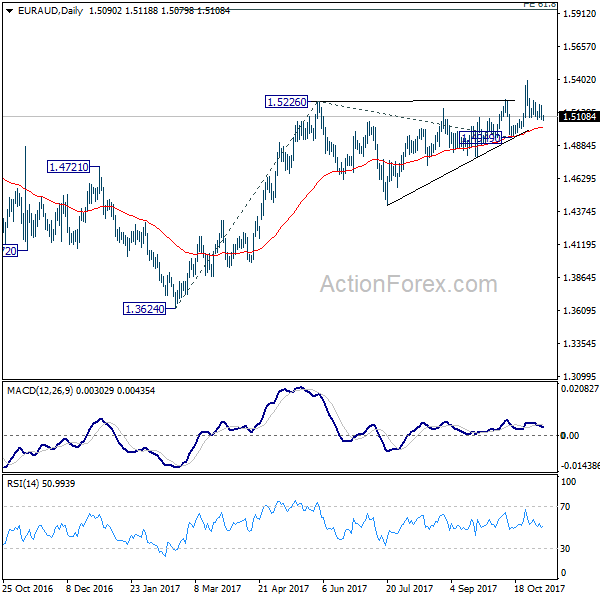

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5058; (P) 1.5126; (R1) 1.516; More....

Intraday bias in EUR/AUD remains neutral as consolidation from 1.5392 continues. As long as 1.4949 support holds, outlook remains bullish. Medium term rally from 1.3624 is in favor to continue. On the upside, break of 1.5392 will resume medium term rise from 1.3624 and target 61.8% projection of 1.3624 to 1.5226 from 1.4949 at 1.5939 first. However, decisive break of 1.4949 will carry larger bearish implication and turn bias to the downside.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. However, break of 1.4949 support will dampen our view and argue that rise from 1.3624 has completed. In that case, EUR/AUD would turn southward for retesting 1.3624 low.

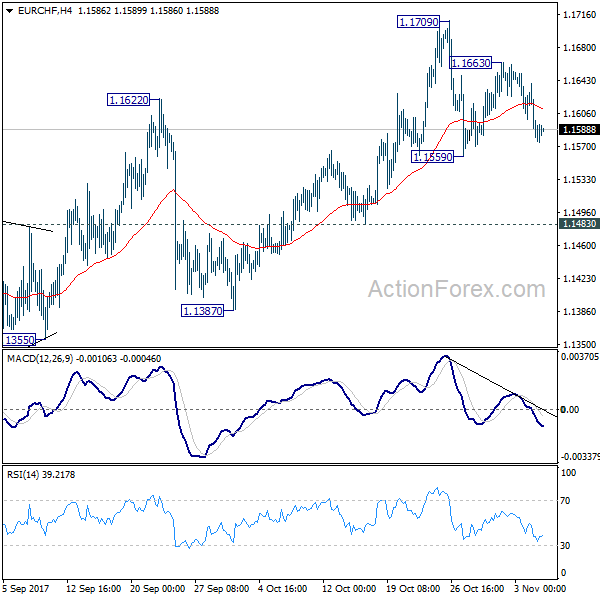

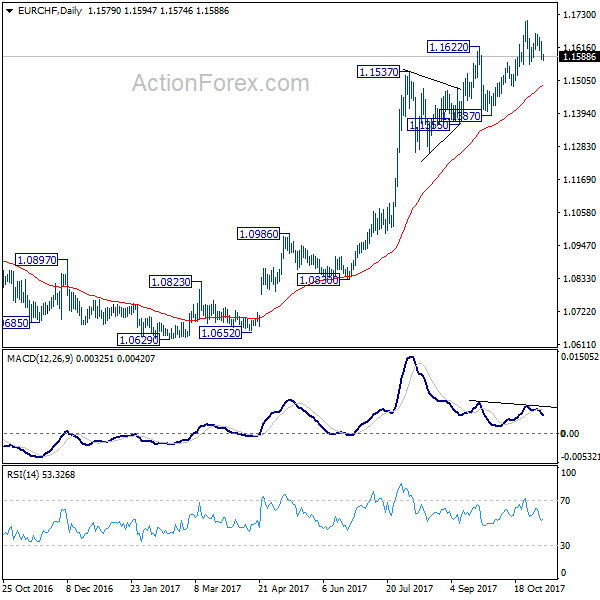

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1557; (P) 1.1598; (R1) 1.1621; More...

Intraday bias in EUR/CHF remains neutral at this point. Consolidation from 1.1709 is still in progress and break of 1.1559 minor support will bring deeper fall. But overall outlook will stays bullish as long as 1.1483 support holds. Above 1.1663 will turn bias back to the upside for 1.1709 high. Break will resume medium term rally to 1.2 key level. However, break of 1.1483 will be an early sign of reversal. In that case, deeper decline should be seen back to 1.1355 support.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1355 support holds. However, break of 1.1355 will indicate medium term topping. In that case, EUR/CHF should head back to 55 week EMA (now at 1.1104) and possibly below.

RBA Kept Its Interest Rate Unchanged At 1.50%

For the 24 hours to 23:00 GMT, the AUD rose 0.43% against the USD and closed at 0.7685.

LME Copper prices declined 0.2% or $12.0/MT to $6902.5/MT. Aluminium prices fell 0.6% or $13.0/MT to $2152.0/MT.

The Reserve Bank of Australia (RBA), at its latest policy meeting, decided to keep its cash rate steady at 1.50%, citing weakness in inflation and slowdown in the housing market. The central bank kept its forecast for the nation’s economic growth largely unchanged and it expects inflation to gradually rise in the coming months. However, the central bank remained concerned about the outlook for household spending.

In the Asian session, at GMT0400, the pair is trading at 0.7689, with the AUD trading marginally higher from yesterday’s close.

The pair is expected to find support at 0.7657, and a fall through could take it to the next support level of 0.7625. The pair is expected to find its first resistance at 0.7711, and a rise through could take it to the next resistance level of 0.7733.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Eurozone Services PMI Fell In October, Investor Confidence Surged To The Highest Level Since July 2007

For the 24 hours to 23:00 GMT, the EUR marginally declined against the USD and closed at 1.1610.

On the data front, Eurozone final services PMI slid less than previously expected to 55.0 in October from 55.8 in September. The preliminary reading had recorded a fall to 54.9. Meanwhile, the region’s investor confidence index climbed to 34.0 in November, beating market expectations of a rise to a level of 31.0.

In the previous month, the index had registered a reading of 29.7.

In Germany, the seasonally adjusted factory orders showed an unexpected rise of 1.0% on a monthly basis in September, against expectations for a drop of 1.1%. In the prior month, factory orders had registered a revised rise of 4.1%. However, the nation’s final services PMI was downwardly revised to 54.7 in

October from a six-month high of 55.6 in September. The preliminary figures had indicated a fall to 55.2.

The US Dollar remained weak against its peers after the Federal Reserve (Fed) Bank of New York confirmed that William Dudley plans to retire earlier than expected in mid-2018, thus raising questions over leadership at the US Fed.

In the Asian session, at GMT0400, the pair is trading at 1.1611, with the EUR trading a tad higher from yesterday’s close.

The pair is expected to find support at 1.1588, and a fall through could take it to the next support level of 1.1565. The pair is expected to find its first resistance at 1.1626, and a rise through could take it to the next resistance level of 1.1641.

Moving ahead, Eurozone retail sales for September and a speech by the European Central Bank (ECB) President, Mario Draghi, due today, would be closely monitored by investors. Also, German industrial production data for September would be watched by market participants. In the US, JOLTS job openings and consumer credit figures, both for September, set to release later today would attract significant market attention.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Pound Trading Marginally Higher This Morning

For the 24 hours to 23:00 GMT, the GBP rose 0.73% against the USD and closed at 1.3172.

Overnight data revealed that UK BRC like-for-like sales declined 1.0% in October, led by weak sales of non-food items, from a gain of 1.9% reported in the prior month. Markets had expected the retail sales to rise 0.8%.

In the Asian session, at GMT0400, the pair is trading at 1.3174, with the GBP trading marginally higher from yesterday’s close.

The pair is expected to find support at 1.3102, and a fall through could take it to the next support level of 1.3030. The pair is expected to find its first resistance at 1.3212, and a rise through could take it to the next resistance level of 1.3250.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading Lower In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.45% against the JPY and closed at 113.81.

In the Asian session, at GMT0400, the pair is trading at 113.91, with the USD trading 0.09% higher from yesterday’s close.

The pair is expected to find support at 113.60, and a fall through could take it to the next support level of 113.28. The pair is expected to find its first resistance at 114.33, and a rise through could take it to the next resistance level of 114.74.

Amid a lack of economic releases in Japan today, trading in the currency pair would be determined by global macroeconomic events.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Swiss Consumer Prices Advanced As Expected In October

For the 24 hours to 23:00 GMT, the USD declined 0.24% against the CHF and closed at 0.9977.

Macroeconomic data showed that the consumer price index (CPI) rose 0.7% in Switzerland on a yearly basis in October, meeting analysts’ expectations. In the previous month, CPI had recorded a similar rise.

Also, Switzerland’s total sight deposits declined to a level of CHF577.8 billion in the week ended 03 November, from a level of CHF578.5 billion reported in the prior week.

In the Asian session, at GMT0400, the pair is trading at 0.9982, with the USD trading marginally higher from yesterday’s close.

The pair is expected to find support at 0.9960, and a fall through could take it to the next support level of 0.9939. The pair is expected to find its first resistance at 1.0016, and a rise through could take it to the next resistance level of 1.0051.

With no major economic releases in Switzerland today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Loonie Trading Marginally Lower, Ahead Of BoC Governor’s Speech

For the 24 hours to 23:00 GMT, the USD declined 0.43% against the CAD and closed at 1.2711.

Data indicated that the seasonally adjusted Ivey PMI in Canada rose more-than-expected to 63.8 in October. In the previous month, the Ivey PMI had registered a level of 59.6.

In the Asian session, at GMT0400, the pair is trading at 1.2712, with the USD trading a tad higher from yesterday's close.

The pair is expected to find support at 1.2682, and a fall through could take it to the next support level of 1.2653. The pair is expected to find its first resistance at 1.2762, and a rise through could take it to the next resistance level of 1.2813.

Investors will await a speech by the Bank of Canada's (BoC) Governor, Stephen Poloz, scheduled later in the day, to get insights about the monetary policy.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.