Sample Category Title

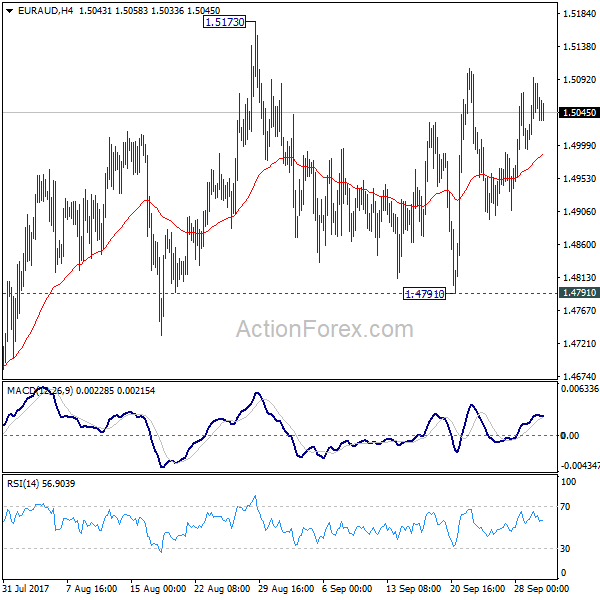

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5012; (P) 1.5053; (R1) 1.5115; More....

Intraday bias in EUR/AUD remains neutral for consolidation in range of 1.4791/5173. On the upside, break of 1.5173/5226 resistance zone will finally resume larger rise from 1.3624. In that case, EUR/AUD will target 1.5644 resistance first. On the downside, break of 1.4791 support will turn bias to the downside and extend the fall from 1.5173 to retest 1.4421 support.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. The corrective structure of the price actions from 1.5226 is affirming this view. Above 1.5226 will target a test on 1.6587 key resistance. However, break of 1.4421 support will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

Euro To Retest 1.1700 Vs US Dollar?

Key Highlights

- The Euro tumbled this past week and broke the 1.1860 support against the US Dollar.

- There was a break below two important bullish trend lines with support near 1.1870 on the 4-hours chart of EUR/USD.

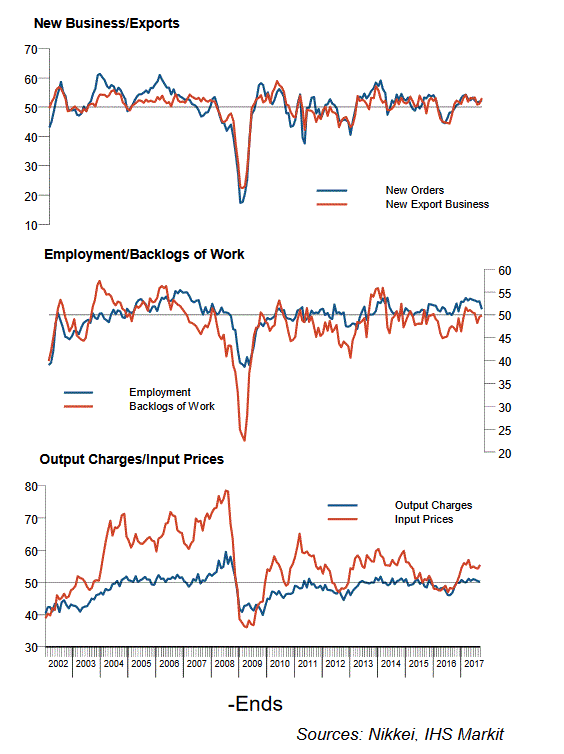

- Japan's Nikkei Manufacturing PMI in September 2017 posted a rise from 52.6 to 52.9.

- Japan's Tankan Large Manufacturing Index in Q3 2017 rose from 17 to 22.

EURUSD Technical Analysis

The Euro started a downside move from 1.1960 against the US Dollar and declined sharply. The EUR/USD pair broke many supports such as 1.1860 and 1.1820 to move into the bearish zone.

Looking at the 4-hours chart of EUR/USD, there was a break below two important bullish trend lines with support near 1.1870. The pair also broke the 100 and 200 simple moving averages (H4) to trade towards 1.1710.

Later, after forming a low at 1.1717, the pair started a correction. It traded towards the 38.2% Fib retracement level of the last decline from the 1.2004 high to 1.1717 low where sellers appeared.

The pair is once again gaining downside momentum and eyeing a retest of 1.1720-1.1700. As long as the pair is below 1.1860, it might continue to struggle in the near term.

Japan's Nikkei Manufacturing PMI and Tankan Large Manufacturing Index

Today, Japan saw a few major economic releases such as Nikkei Manufacturing PMI (Sep 2017) and the Tankan Large Manufacturing Index (Q3 2017).

First, the Tankan Large Manufacturing Index for Q3 2017 was released by the Bank of Japan. The market was looking for a rise in the index from 17 top 18. The actual result was above the forecast, as there was an increase to 22.

The Tankan large Manufacturing Outlook was forecasted to increase from 15 to 16, but again the actual was positive as the index rose to 19.

The Tankan Large All Industry Capital Expenditure was forecasted to rise by 8.3% in Q3 2017. However, the result was a bit lower, as the increase was 7.7%, which was also less than the last 8%.

Moreover, the Nikkei Manufacturing PMI for September 2017 was published today. The forecast was slated for no change in the PMI from 52.6. The actual was positive, as there was a rise from 52.6 to 52.9.

Commenting on the report, the Principal Economist at IHS Markit, Annabel Fiddes, stated:

Latest data signalled a further improvement in growth momentum across Japan's manufacturing sector with the PMI rising to a four-month high in September.

The results favored the Japanese Yen, but the USD/JPY pair remains in an uptrend and looks set to gain pace above 113.00 in the near term.

Forex: UK Output Data Falls But Expectations Rise

On Sunday, The Confederation of British Industry released their monthly indicator of output for UK manufacturers, retailers and service companies. The release, of +11, was down from +14 for the June to August period. CBI Chief Economist Rain Newton-Smith commented that 'Growth in the economy has held steady through the summer, although at a slightly slower pace than expected by many firms'. Overall output expectations for the following 3 months edged higher to +18 (+2 from August). The data is unlikely to influence Bank of England Policy makers as long as the economy is growing and prices are rising. So, a UK rate hike is still a strong likelihood before this year is over – possibly as early as November.

Data released on Friday indicated US Consumer spending hardly rose in August, with Harvey blamed for lower than expected Auto sales. Further data indicated that US inflation, annualized, grew at its slowest pace in more than 24-months. With such lethargic data, it is highly likely that US economic growth is likely to be somewhat subdued for Q3.

Friday’s Eurostat data release of Eurozone inflation data was below forecasts. The poor growth of inflation endorses the European Central Bank’s stance that stimulus within the Eurozone should be pared back gradually.

On the Geo-Political front, there has been no new 'war of words' between the US and North Korea over the weekend. However, on Sunday, President Trump dismissed the prospects of talks with North Korea as a waste of time. This followed a comment made on Saturday by the US Secretary of State who said 'the United States was maintaining open lines of communication with North Korean leader Kim Jong Un' – according to the White House 'Pyongyang had shown no interest in dialogue'.

EURUSD loss nearly 0.3% in early Monday trading, as the markets watched the referendum in Catalonia – early suggestions are that 90% of the 'unofficial' vote have called for independence from Spain. Currently, EURUSD is trading around 1.1765.

USDJPY is 0.2% higher in early Monday trading, even with a higher than expected factory data release from Japan earlier in the trading session. Currently, USDJPY is trading around 112.90.

GBPUSD is slightly lower following calls from senior government officials that Theresa May’s tenure as Prime Minister may be coming to an end. GBPUSD is currently trading around 1.3350.

Gold is down 0.5% in early trading, as risk-on sentiment has pushed the precious metal down to levels last seen over 7 weeks ago. Currently, Gold is trading around $1,274.

WTI is little changed from Friday, currently trading around $51.70pb.

Major economic data releases for today:

At 15:00 BST, Markit Economics will release the Markit Manufacturing PMI for September. As manufacturing forms a major component of total GDP, this release is an important indicator of business conditions and the overall economic condition in the US.

At 15:00 BST, the US Institute for Supply Management (ISM) will release Manufacturing PMI and Prices Paid for September. Akin to the Markit PMI released at the same time, the ISM PMI is also an important indicator as to the 'health' of the US economy. PMI is expected to come in at 58 (Prev. 58.8) and prices paid are expected to come in at 64 (Prev. 62).

Catalonia’s Independence Vote Drags The Euro

The Euro came under pressure early Monday, falling more than 0.4% against the USD, after preliminary results from the weekend's Catalonia referendum showed that 90% of Catalans are in favor of independence.

There's a high chance that Spain may be headed towards a new crisis, especially if Catalonia's President, Carles Puigdemont, declares independence as he has promised to do in the next 48 hours. This will lead to more violence and probably an intervention from EU leaders, who will come under pressure to take action.

Traders should be monitoring spreads between Spanish and German bond yields in the next couple of days. If spreads widen significantly, investors will become seriously worried about the outcome of the referendum vote, leading to a further selloff in the Euro, but this is not evident yet.

Catalan's referendum is not the only reason for the fall in EURUSD. In fact, the dollar is rising across the board, as the U.S. Treasury's yield curve shifted upwards. Given that there wasn't any new fundamental information released over the weekend, reports that former Federal Reserve Governor Kevin Warsh had met with President Trump and Treasury Secretary Steven Mnuchin, for a possible nomination to chair the Fed, is the only explanation for the shift in the yield curve. We do not yet know how Warsh would lead the Fed in the Trump Era, but given the reaction seen in bond markets, investors see him as a more hawkish candidate than Yellen.

Speculation around the Fed Chair appointment will keep fixed-income traders busy in the days to come, and currency traders will benefit from the moves in yields. However, this speculation should end, when the President announces the name of his nominee in two to three weeks.

The European economic calendar is relatively light this week. Traders will be focusing on PMI data from the U.K., the jobs reports from the U.S. and Canada, and the Reserve Bank of Australia interest rate decision. The U.S. NFP is likely to deviate hugely from this year's average. Economists are currently anticipating a figure less than 100K. However, I do not think this will have a negative impact on the dollar, given that investors know Hurricanes Harvey and Irma will distort the data.

Fed speak will likely continue guiding traders, and Janet Yellen will again appear on Wednesday to deliver the opening remarks at the 21stCentury Conference in St. Louis. Fed officials Robert Kaplan, Jerome Powell, Patrick Harker, and Bill Dudley, are all due to speak this week.

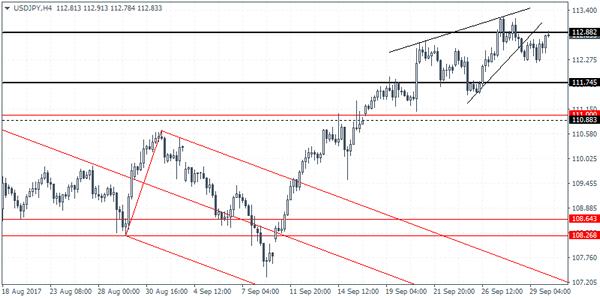

USDJPY Intraday Analysis

USDJPY (112.83): The USDJPY managed to post some gains although price action struggles to breakout from the resistance level of 112.88. The 4-hour chart shows the ascending wedge pattern from which price broke out briefly before retracing these losses. As long as price does not breakout from the resistance level, we can expect to see some downside price action. The rising wedge pattern will be validated on a decline towards the support level of 111.74. A breakout above 112.88 could, however, invalidate the bearish wedge pattern with price action likely to test further highs.

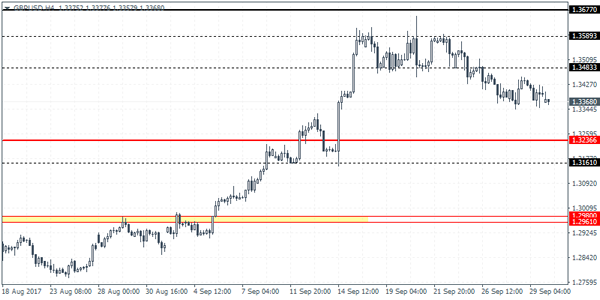

GBPUSD Intraday Analysis

GBPUSD (1.3368): GBPUSD is seen opening on a weaker note this morning following the downside breakout in prices below 1.3483. We expect the declines to continue towards the lower support level at 1.3236. Price action has broken to the downside following the failure of the bullish flag pattern. The correction to 1.3236 marks a retest of the previously breached resistance level. Establishing support here could keep prices range bound, but further downside cannot be ruled out. The next lower support is seen at 1.3161 which could potentially be tested as well.

EURUSD Intraday Analysis

EURUSD (1.1774): Although the EURUSD managed to post some gains towards Friday, price action stalled near the resistance level of 1.1822. Initial signs show a reversal at this level, but this could be confirmed only on a daily bearish close off the 1.1822 resistance level. The next support level is seen at 1.1688, followed by a decline to 1.1440. The decline to 1.1688 will mark the 161.8% measured move of the descending triangle. Thus, we could expect price action to potentially at this level before moving into a sideways range for the near term.

Markets Look To A New Trading Week, ISM Manufacturing PMI In Focus

The US dollar was seen trading close the week on a mixed note. Economic data released on Friday showed that the personal consumption expenditure rose at a weaker than expected pace.

The headline PCE index rose just 0.1% on the month, below estimates of 0.2%. On a year over year basis, the PCE rose 1.3%, slightly below 1.4% that was registered the month before while the core PCE grew at the same pace of 1.4% as the previous month.

Over the weekend, the Catalonian referendum was the major event. Despite the courts calling it unconstitutional, the referendum went ahead with the results showing over 90% of the voters backing for statehood. The weekend referendumwas met with chaos and violence.

Looking ahead, the new trading week and a month, as well as the quarter,is likely to see speculators focusing on the upcoming fundamentals. In the US, the ISM's manufacturing PMI is expected to be released this week.

Economists expect that index to fall to 58.0, down from 58.8 in August which marked a 6-year high. From the Eurozone, the services and manufacturing PMI will also be released today.

Currencies: EUR/USD Modestly Lower As Catalan Tensions Persist

Sunrise Market Commentary

- Rates: Catalan headache for Spanish bonds?

European markets showed a lot of resilience in the run-up to the Catalan secession vote. Madrid's impertinent behaviour and Catalan President Puigdemont's hint at a unilateral declaration of independence might change that today, resulting in Spanish spread widening and an outperformance of the Bund vs the US Note future. - Currencies: EUR/USD modestly lower as Catalan tensions persist

The dollar outperforms this morning, supported by higher US yields. EUR/USD returns south after a rebound at the end of last week. Tension in Catalonia might be slightly negative for the euro, but USD strength prevails. Will the US ISM be strong enough to reactivate the reflation trade and support further USD gains?

The Sunrise Headlines

- US equities had a good run Friday, closing the quarter with moderate gains (and new highs for S&P and NASDAQ). IT is still the outperformer. Asian stocks trade slightly positive too, but the Golden week keeps many bourses closed.

- Catalan separatist leaders signalled they may be moving toward unilateral independence as early as this week after many activists were injured as they tried to stop Spanish police from shutting down an illegal referendum.

- The Q3 Japanese Tankan report nurtured economic optimism. Large and small manufacturing firms were much more optimistic than expected about the current situation and the outlook. Large and small non-manufacturing firms' results were respectively slightly better and slightly worse than expected.

- The official Chinese PMI survey showed an improvement of sentiment. The manufacturing PMI was up to 52.4 from 51.7 in August and the non-manufacturing PMI rose to 55.4 from 53.4. The Caixin PMI (more private sector oriented) slowed though to 51 from 51.6 (51.5 expected).

- President Trump admonishment of Secretary of State Tillerson for 'wasting his time' in seeking negotiations with N-Korea highlighted differences within the administration on how best to get Kim Jong Un to halt his nuclear program

- President Trump met with former Fed governor Warsh to discuss potentially nominating him as the next Fed chairman. Warsh has a more hawkish instinct that current chairwoman Yellen. It moved bond markets with a bear flattening.

- EMU & UK PMI and the US ISM surveys are the key eco indicators today. ECB Praet, Fed Kaplan speak (little impact?) and UK PM May speak

Currencies: EUR/USD Modestly Lower As Catalan Tensions Persist

Dollar rebound to resume?

On Friday, the dollar corrected slightly further lower after eking out gains earlier last week. However, the move petered out as core/US yields rose later in the session. US eco data were mixed and had no lasting impact on USD trading. EUR/USD returned temporary north of the 1.1823 previous range bottom, but closed the session at 1.1814. USD/JPY finished the quarter at 112.51.

Overnight, several Asian markets including China are closed. Chinese PMI's were fairly strong. Still, the PBOC eased the reserve requirements from lending to small companies. This news helps regional sentiment. The Japan Tankan confidence report was constructive with especially manufacturing and smaller non-manufacturing firms more optimistic. . The headline manufacturing index improved from 17 to 22. There was no reaction of the yen. USD/JPY profits from overall USD strength. Markets are pondering the chances/potential impact of a US tax cut. There is also speculation that Trump might choose a more hawkish new Fed-chairman. EUR/USD declines to the 1.1775 area. USD strength prevails, but there might also a minor fall-out from the tensions in Catalonia.

In EMU, the manufacturing PMI is to be confirmed at a very strong 58.2. The EMU unemployment rate is expected to have declined to 9% in August from 9.1%. In the US, the manufacturing ISM is expected to have declined to 58 from August's 58.8, which was near the peak of the previous cycle (2007). Regional surveys, including Friday's Chicago PMI, were strong. So, the risks are on the upside of consensus.

The dollar rallied last week, as investors realised that the chances on a Dec. Fed rate hike have risen and as the US government stepped up its efforts to put the tax reform on the rails. Both factors propelled US yields and the dollar, but the dollar rebound ran into resistance at the end of last week. The dollar clearly needs good eco news and higher US yields. A strong US manufacturing ISM and a constructive risk sentiment might be slightly supportive for US yields and for the dollar. We also keep an eye on the developments in Catalonia/Spain. The tension won't help the euro, but for now we think it won't be a source of substantial euro losses. It looks like the dollar might start the week with a cautious positive bias

From a technical point of view EUR/USD hovered in a consolidation pattern between 1.1823 and 1.2070. It took time to break below the 1.1823 range bottom, but the break occurred earlier last week. There was some hesitation in the USD rebound at the end of last week, but EUR/USD closed below the 1.1823 previous range bottom. The rise in US yields looks solid and may support the USD rebound. Next support in EUR/USD comes in at 1.1662. The day-to-day momentum in USD/JPY was constructive recently, but it was primarily due to yen weakness. USD/JPY regained the 110.67/95 previous resistance, a short-term positive. The day-to-day momentum remains constructive. The 114.49 correction top is the next important reference.

EUR/USD revisits 1.1823 range bottom, but test rejected

EUR/GBP

Sterling still looking for a clear trend.

On Friday, markets focused on two negative eco topics. UK Q2 Y/Y figure was reduced from 1.7% Y/Y to 1.5% Y/Y due to downward revisions in Q3 and Q4 of 2016. At same time, output growth in the key services sector declined in July. Sterling already felt some headwinds in the run-up to the data and the move accelerated afterwards. EUR/GBP extended its rebound north of 0.88. Admittedly, part of this move mirrored an overall rise of the euro. EUR/GBP closed the session at 0.8820. Cable closed the session at 1.3398.

In the weekend, the rift between UK PM May and foreign Secretary Boris Johnson on Brexit flared up. For now, the issue has no big negative impact on sterling. Overnight, sterling is losing slightly ground against an overall strong dollar, but gains a few ticks against the euro. The topic will remain in the spotlights during the conference of the Tories that ends Wednesday. Today, the UK manufacturing PMI is expected to decline from 56.9 to 56.2. However, this is still a good level that allows the BoE to raise rates if deemed necessary. So, the market context looks neutral for sterling (EUR/GBP) at the start of the week.

EUR/GBP made an impressive uptrend from April to set a MT top at 0.9307 late August. UK price data amended the dynamics and hawkish BoE comments reinforced a sterling rebound. Medium term, we maintain a EUR/GBP buy-on-dips approach as we expect the mix of euro strength and sterling softness to persist. However, the prospect of (limited) withdrawal of BOE stimulus puts a solid floor for sterling ST term. We look how far the current correction goes. EUR/GBP is nearing support at 0.8743 and 0.8652, which we consider difficult to break. We gradually look to buy EUR/GBP on dips.

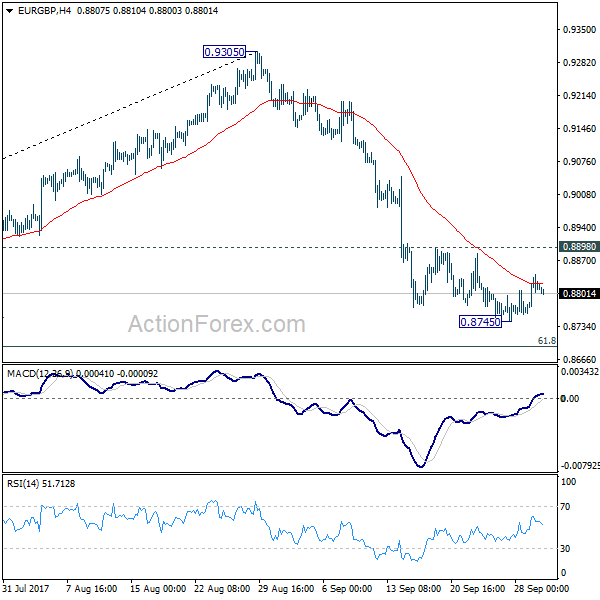

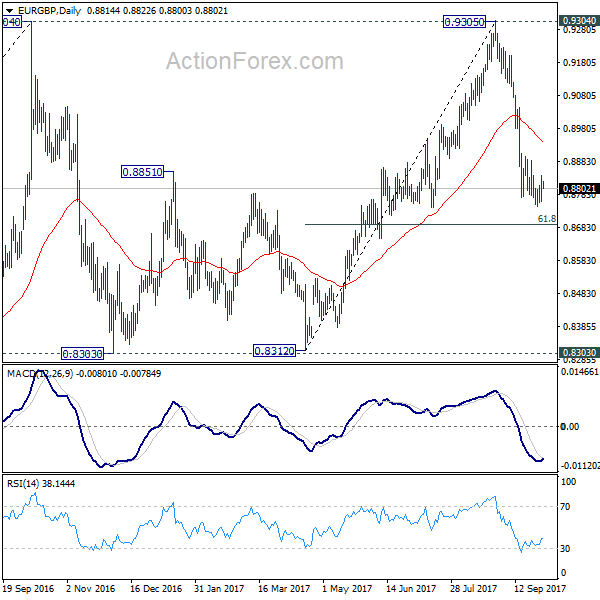

EUR/GBP: downtrend shows tentative signs of slowing

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8772; (P) 0.8806; (R1) 0.8849; More...

EUR/GBP dips mildly today but it's staying above 0.8745 temporary low. Intraday bias remains neutral first. Below 0.8745 will target 61.8% retracement of 0.8312 to 0.9305 at 0.8691 and below. Fall from 0.9305 is seen as the third leg of consolidation pattern from 0.9304. We'll look for bottoming signal again at it approaches 0.8303 support. On the upside, break of 0.8898 will indicate near term reversal and turn bias back to the upside for 55 day EMA (now at 0.8945) first.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's still in progress with fall from 0.9305 as the third leg. Break of 0.8303 could be seen. But even in that case, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes.