Sample Category Title

Euro Lower as Catalonian Referendum Turned into Chaos by Police Violence

Euro opens the week broadly lower as the Catalonian referendum for independence on Sunday turned into chaos. Legally recognized or not, preliminary results show that 90% votes were in favor of independence with a turnout rate of 42.3% (2.3M votes). What shocked the world is that the the peaceful campaign had met with violent suppression of the Spanish government, with brutal attack by the national police (firing rubber bullets, seizing ballot boxes from polling stations, etc). It's believed the violence of the government provoked more "yes" vote for independence.

Catalan President Carles Puigdemont declared that "the citizens of Catalonia have won the right to have an independent state". He pledged to act in line with the referendum law, which could lead to a unilateral declaration of independence within 48 hours after notifying the regional parliament of the voting results. Calling the referendum illegal, the Spanish prime minister, Mariano Rajoy, noted that the vote "only served to cause serious harm to coexistence" among Spaniards. The EU leaders have yet to comment on the results, as well as the act of Spanish national police. A huge strike has been called across Catalonia on October 3 in response to the violence.

Tankan large manufacturers index hit decade high

In Japan, the quarterly Tankan survey painted a positive picture for the economy. The large manufacturers index jumped to 22 in Q3, up from 17 and beat expectation of 18. That's also the highest reading in a decade since 2007. Large manufacturers outlook rose to 19, up from 15 and beat expectation of 16. That is seen as a result from a weaker Yen, that helped exports. However, non-manufacturing index was unchanged at 23, missing expectation of 24. Non-manufacturing outlook improved to 19, missing expectation of 21. All industrial capex rose 7.7%, slowed from 8.0% and missed expectation of 8.4%. The overall upbeat data could provide Prime Minister Shinzo Abe a mild lift going into the snap election on October 22.

China PBoC cut RRR, PMI upbeat

In China, PBoC announced targeted cuts to the reserve requirement ratio (RRR) ranging from 0.5% to 1.5%. The moves should apply to the majority of banks (90% of city commercial banks, and 95% of rural commercial lenders) in order to spur lending to small firms. This is the first reduction in RRR since February 2016. An RRR cut is regarded as an accommodative monetary policy in nature and the PBOC's move is estimated to release around RMB300-400B to the market. But the central bank claimed that it has not derailed from the prudent and neutral policy stance.

The official manufacturing PMI added 0.7 points to 52.4 in September, highest since April 2012. Looking into the details, the new orders index gained 1.7 points to 54.8 while the new export orders index added 0.9 point to 51.3. The input prices index jumped 3.1 points to 68.4, highest since December 2016. The Caixin manufacturing PMI, however, slipped -0.6 points to 51 for the month. On the non-manufacturing sector, official PMI added 2 points to 55.4, highest since May 2014.

Economic data return to spotlights

Looking ahead, focus will be back on economic data this week. US ISM indices and non-farm payroll will be part of the features. UK will release PMIs too. Canada will also release job data. Meanwhile, Australia will release retail sales and trade balance. On central bank activities, RBA is widely expected to stand pat on Tuesday. ECB will release monetary policy meeting accounts on Thursday. A number of Fed officials will also speak this week including Fed Chair Yellen, regional Fed presidents Kaplan, Powell, Williams, Harker, George, Bostic, Dudley, Bullard and Rosengren. Here are some highlights for the week ahead:

- Monday: Swiss retail sales, SVME PMI; Eurozone PMI manufacturing final, unemployment rate; UK PMI manufacturing; US ISM manufacturing

- Tuesday: Japan monetary base; RBA rate decision, Australia building approvals; Japan consumer confidence; UK construction PMI; Eurozone PPI

- Wednesday: Eurozone PMI services final, retail sales; UK PMI services; US ADP employment, ISM non-manufacturing

- Thursday: Australia retail sales, trade balance; Swiss CPI; ECB meeting accounts; US jobless claims, trade balance, factory orders; Canada trade balance

- Friday: Japan average cash earnings, leading indicators; German factory orders; Swiss foreign currency reserves; Canada employment, Ivey PMI; US non-farm payroll

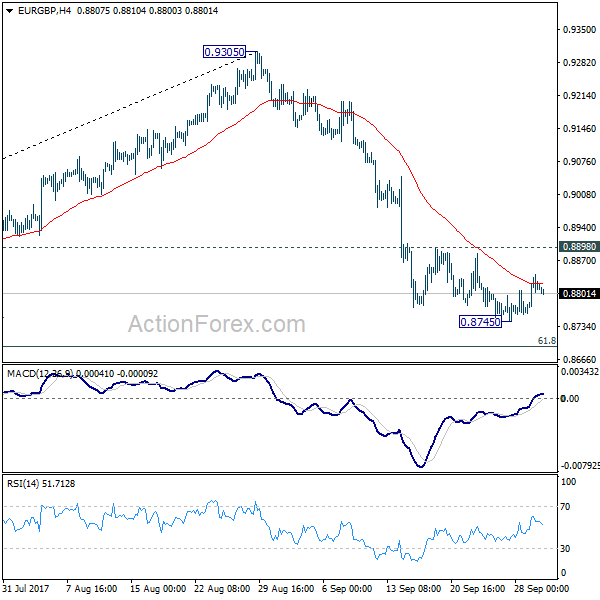

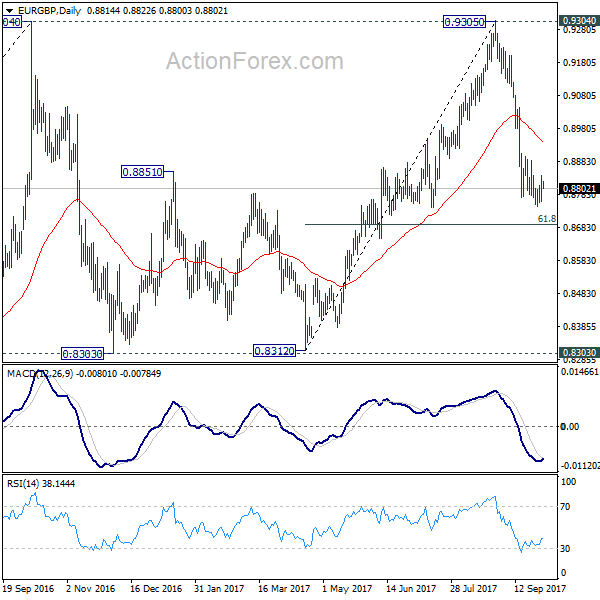

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8772; (P) 0.8806; (R1) 0.8849; More...

EUR/GBP dips mildly today but it's staying above 0.8745 temporary low. Intraday bias remains neutral first. Below 0.8745 will target 61.8% retracement of 0.8312 to 0.9305 at 0.8691 and below. Fall from 0.9305 is seen as the third leg of consolidation pattern from 0.9304. We'll look for bottoming signal again at it approaches 0.8303 support. On the upside, break of 0.8898 will indicate near term reversal and turn bias back to the upside for 55 day EMA (now at 0.8945) first.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's still in progress with fall from 0.9305 as the third leg. Break of 0.8303 could be seen. But even in that case, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Tankan Large Manufacturers Index Q3 | 22 | 18 | 17 | |

| 23:50 | JPY | Tankan Large Manufacturers Outlook Q3 | 19 | 16 | 15 | |

| 23:50 | JPY | Tankan Non-Manufacturing Index Q3 | 23 | 24 | 23 | |

| 23:50 | JPY | Tankan Non-Manufacturing Outlook Q3 | 19 | 21 | 18 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q3 | 7.70% | 8.40% | 8.00% | |

| 23:50 | JPY | Tankan Small Mfg Index Q3 | 10 | 8 | 7 | |

| 23:50 | JPY | Tankan Small Mfg Outlook Q3 | 8 | 6 | 6 | |

| 23:50 | JPY | Tankan Small Non-Mfg Index Q3 | 8 | 7 | 7 | |

| 23:50 | JPY | Tankan Small Non-Mfg Outlook Q3 | 4 | 2 | 2 | |

| 0:00 | AUD | TD Securities Inflation M/M Sep | 0.30% | 0.10% | ||

| 0:30 | JPY | PMI Manufacturing Sep F | 52.9 | 52.6 | 52.6 | |

| 7:15 | CHF | Retail Sales (Real) Y/Y Aug | 0.50% | -0.70% | ||

| 7:30 | CHF | SVME PMI Sep | 60.5 | 61.2 | ||

| 7:45 | EUR | Italy Manufacturing PMI Sep | 56.8 | 56.3 | ||

| 7:50 | EUR | France Manufacturing PMI Sep F | 56 | 56 | ||

| 7:55 | EUR | Germany Manufacturing PMI Sep F | 60.6 | 60.6 | ||

| 8:00 | EUR | Eurozone Manufacturing PMI Sep F | 58.2 | 58.2 | ||

| 8:30 | GBP | PMI Manufacturing Sep | 56.2 | 56.9 | ||

| 9:00 | EUR | Eurozone Unemployment Rate Aug | 9.00% | 9.10% | ||

| 13:30 | CAD | Canada Manufacturing PMI Sep | 54.6 | |||

| 13:45 | USD | Manufacturing PMI Sep F | 53 | 53 | ||

| 14:00 | USD | ISM Manufacturing Sep | 58 | 58.8 | ||

| 14:00 | USD | ISM Prices Paid Sep | 64 | 62 | ||

| 14:00 | USD | Construction Spending M/M Aug | 0.40% | -0.60% |

Australia’s Manufacturing Sector Growth Sharply Slowed In September

For the 24 hours to 23:00 GMT, the AUD declined 0.1% against the USD and closed at 0.7841 on Friday.

LME Copper prices rose 1.3% or $80.0/MT to $6485.0/MT. Aluminium prices rose 0.4% or $8.0/MT to $2110.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7822, with the AUD trading 0.24% lower against the USD from Friday's close, after overnight data indicated that Australia's AiG performance of manufacturing index fell to a level of 54.2 in September, compared to a reading of 59.8 in the prior month.

Elsewhere in China, Australia's largest trading partner, the NBS manufacturing PMI recorded an unexpected rise to a level of 52.4 in September, expanding at its fastest pace in five years. Markets were expecting the PMI to fall to a level of 51.6, compared to a reading of 51.7 in the prior month. Moreover, the nation's non-manufacturing PMI rose to a level of 55.4 in September, after recording a level of 53.4 in the previous month.

Also, the nation's Caixin/Markit manufacturing PMI eased to a level of 51.0 in September, compared to a reading of 51.6 in the prior month, while markets were anticipating the PMI index to ease to a level of 51.5.

The pair is expected to find support at 0.7808, and a fall through could take it to the next support level of 0.7794. The pair is expected to find its first resistance at 0.7845, and a rise through could take it to the next resistance level of 0.7868.

Going ahead, traders would closely monitor the Reserve Bank of Australia's (RBA) interest rate decision, due in the early hours of tomorrow. Additionally, Australia's HIA new home sales and building permits, both for August, slated to release overnight, will be on investors' radar.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Annual Inflation Grew At A Softer Pace In September

For the 24 hours to 23:00 GMT, the EUR rose 0.3% against the USD and closed at 1.1816 on Friday.

In economic news, the Euro-zone's flash consumer price index (CPI) climbed less-than-anticipated by 1.5% on an annual basis in September, indicating that economic expansion across the common currency region has yet to translate in stronger inflation dynamics. The CPI had registered a similar rise in the prior month, while market participants had expected for an advance of 1.6%.

Separately, Germany's seasonally adjusted unemployment rate unexpectedly declined to a new record low of 5.6% in September, painting a robust picture of the nation's labour market. Markets had expected the unemployment to remain steady at 5.7%. On the other hand, the nation's retail sales registered an unexpected drop of 0.4% MoM in August, defying market consensus for a gain of 0.5%. In the previous month, retail sales had fallen 1.2%.

Macroeconomic data released in the US indicated that personal income rose 0.2% in August, meeting market expectations and compared to a revised advance of 0.3% in the previous month. Moreover, the nation's personal spending registered a rise of 0.1% in August, in line with market expectations. In the prior month, personal spending had advanced 0.3%. Moreover, the nation's Chicago Fed purchasing managers index unexpectedly rose to a three-year high level of 65.2 in September, confounding market consensus for a drop to a level of 58.7. The index had registered a reading of 58.9 in the prior month.

In other economic news, the US final Reuters/Michigan consumer sentiment index fell more than initially estimated to a level of 95.1 in September, compared to a preliminary print indicating a fall to a level of 95.3. In the previous month, the index had registered a reading of 96.8.

In the Asian session, at GMT0300, the pair is trading at 1.1777, with the EUR trading 0.33% lower against the USD from Friday's close.

The pair is expected to find support at 1.1754, and a fall through could take it to the next support level of 1.1732. The pair is expected to find its first resistance at 1.1816, and a rise through could take it to the next resistance level of 1.1856.

Moving ahead, investors will focus on the final Markit manufacturing PMI for September across the Euro-zone along with the region's unemployment rate for August, slated to release in a few hours. Moreover, in the US, the ISM manufacturing and the final Markit manufacturing PMI, both for September along with the nation's construction spending data for August, all set to release later today, will garner significant amount of market attention.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

UK Interest Rates To Rise In The Near-Term: Mark Carney

For the 24 hours to 23:00 GMT, the GBP declined 0.27% against the USD and closed at 1.3398 on Friday, following dismal UK GDP growth report.

Data showed that Britain's final gross domestic product (GDP) climbed 1.5% on an annual basis in the three months to June 2017, revised down from an expansion of 1.7% indicated in the preliminary figures, thus stoking concerns over the likelihood of an interest rate hike by the Bank of England (BoE) in the near-term. In the prior quarter, GDP had climbed 2.0%. Further, the nation's mortgage approvals fell to a level of 66.6K in August, more than market expectations for a decline to a level of 67.3K. Mortgage approvals had registered a revised reading of 68.5K in the prior month.

In other economic news, the nation's net consumer credit rose £1.6 billion in August, growing by the most three months, justifying the BoE Governor's worries regarding lending by British lenders. Consumer credit had risen by £1.2 billion in the prior month, while markets had anticipated for an advance of £1.4 billion.

Separately, the BoE Governor, Mark Carney, confirmed that central bank is close to an imminent interest rate hike, stating that it may be appropriate to raise interest rates “in the relatively near-term”, if the British economy continues to show signs of strengthening. Carney also warned against “reckless” household borrowing, outlining that personal lending was becoming a “little frothy and should be addressed”.

In the Asian session, at GMT0300, the pair is trading at 1.3369, with the GBP trading 0.22% lower against the USD from Friday's close.

The pair is expected to find support at 1.3337, and a fall through could take it to the next support level of 1.3306. The pair is expected to find its first resistance at 1.3413, and a rise through could take it to the next resistance level of 1.3458.

Going ahead, market participants will keep a close watch on UK's Markit manufacturing PMI for September, scheduled to release in a few hours.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Japanese Tankan Business Confidence Hits 10-Year-High In 3Q 2017

For the 24 hours to 23:00 GMT, the USD rose 0.17% against the JPY and closed at 112.58 on Friday.

In the Asian session, at GMT0300, the pair is trading at 112.83, with the USD trading 0.22% higher against the JPY from Friday's close.

Overnight data indicated that Japan's final Nikkei manufacturing PMI rose more than initially estimated to a level of 52.9 in September, following a level of 52.2 in the prior month. The preliminary figures had recorded an advance to a level of 52.6.

Additionally, the nation's Tankan large manufacturing index registered a rise to a level of 22.0 in 3Q 2017, topping market expectations of a rise to a level of 18.0 and notching its highest level since September 2007. In the prior quarter, the index had recorded a reading of 17.0. Further, the nation's Tankan non-manufacturing index remained unchanged at a level of 23.0 in 3Q 2017, while markets were expecting the index to climb to a level of 24.0.

The pair is expected to find support at 112.4, and a fall through could take it to the next support level of 111.96. The pair is expected to find its first resistance at 113.09, and a rise through could take it to the next resistance level of 113.34.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Switzerland’s KOF Leading Indicator Sharply Advanced In September

For the 24 hours to 23:00 GMT, the USD declined 0.21% against the CHF and closed at 0.9685 on Friday.

In economic news, Switzerland's KOF leading indicator rose to a level of 105.8 in September, exceeding market expectations for a rise to a level of 105.5. The index had registered a revised level of 104.2 in the prior month.

In the Asian session, at GMT0300, the pair is trading at 0.9700, with the USD trading 0.15% higher against the CHF from Friday's close.

The pair is expected to find support at 0.9674, and a fall through could take it to the next support level of 0.9647. The pair is expected to find its first resistance at 0.9724, and a rise through could take it to the next resistance level of 0.9747.

Going forward, Switzerland's retail sales for August and SVME–PMI for September, both due to release in a few hours, will pique a lot of market attention.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Canadian Economic Growth Stagnated In July

For the 24 hours to 23:00 GMT, the USD rose 0.35% against the CAD and closed at 1.2478 on Friday.

The Canadian Dollar lost ground against the USD, after data showed that Canada's gross domestic product (GDP) remained flat on a monthly basis in July, dragged by tumbling oil and automobile production and a slowdown in housing market. Market participants had envisaged the nation's GDP to rise 0.1%, after recording an advance of 0.3% in the prior month.

In the Asian session, at GMT0300, the pair is trading at 1.2490, with the USD trading 0.1% higher against the CAD from Friday's close.

The pair is expected to find support at 1.2427, and a fall through could take it to the next support level of 1.2365. The pair is expected to find its first resistance at 1.2542, and a rise through could take it to the next resistance level of 1.2595.

Ahead in the day, investors would eye Canada's Markit manufacturing PMI for September.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Trump Has So Far Met With current Fed Chair Janet Yellen

Market movers today

In Europe , final PMIs and euro area unemployment rate for August are due out . We estimate the unemployment rate declined from 9.1% to 9.0%. Despite the decline, there is still some slack, which together with low inflation expectations and slow productivity growth is weighing down on wage growth.

In the US, the main release is the ISM manufacturing index for September. Given that regional PMIs have increased, there is also room for ISM manufacturing to increase to around 60 despite PMI manufacturing being stable at a much lower level in September. This big gap between PMI manufacturing and ISM manufacturing is still puzzling and we think the truth is likely somewhere in the middle, but note markets tend to focus more on ISM.

In the UK, the Conservative Party conference began yesterday and ends on Wednesday. The Conservative Party remains hugely divided on Brexit and PM Theresa May's position has been clearly weakened since the general election in June. May is expected to deliver a speech on Brexit and reiterate that the UK will leave the single market and the customs union.

In the Scandies, focus turns to PMI manufacturing releases in Sweden and Norway.

Selected market news

In Spain, a constitutionally declared illegal vote on Catalan independence took place on Sunday. Catalan authorities reported several injuries from clashes with police forces. Given the legal status of the ‘leave' result and lack of external support , the markets seem to expect calmer days going forward even with the EUR weakening slightly. For more details see e.g. Reuters.

On Friday, US PCE core inflation disappointed market expectations by printing a yearly rate of 1.3% (down from 1.4%). Headline PCE also fell short of expectations, which overall leaves the PCE contradicting the strong CPI reading in August . However, given the Fed's focus on a tight labour market , we do not think it will change the Fed's view on monetary policy for now.

Having said this, future Fed monetary policy will depend on who President Trump's nominates as board members (it is said he will pick two nominees). On Friday, several news agencies ran stories that Trump had met with possible candidates for the job as Fed Chair. According to Bloomberg, Trump has so far met with current Fed Chair Janet Yellen, National Economic Council Director Gary Cohn, Fed Governor Jerome Powell and former Fed Governor Kevin Warsh. According to Trump, a decision will be made ‘over the next two or three weeks'.

In Sweden, the Riksbank has extended current governor Stefan Ingves' mandate by five years. Also, First Deputy Governor Kerstinaf Jocknick's mandate was extended by six years. Both decisions were unanimous by the General Council. Much speculation had preceded the announcement , which is why EUR/SEK rose on the announcement .

Over the weekend in China, the Caixin and the official manufacturing PMI painted slightly different out looks for the manufacturing sector. While the former suggested a slightly slower acceleration pace (still above 50) by dropping to 51.0 (from 51.6) the latter rose to 52.4 (from 51.7). Going forward we project a slowdown in the Chinese economy on the back of a tightening in financial conditions, a cooling housing market and infrastructure spending slowing. Importantly, we do not expect a hard landing, as we pencil in solid external demand (exports) and fairly low housing inventories to cushion the slowdown.

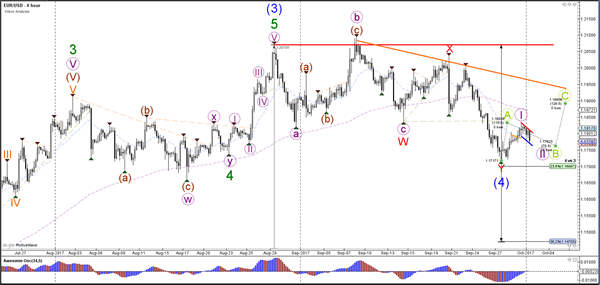

Daily Wave Analysis: EUR/USD, GBP/USD Bounce Or Break Spot At 23.6% And 38.2% Fibs

Currency pair EUR/USD

The EUR/USD bullish bounce at the 23.6% Fibonacci level could create a larger ABC (green) or a new uptrend (123 purple). These 2 scenarios are invalidated if price breaks below the 23.6% Fib. In that case, price will most likely make a bearish breakout towards the 38.2% Fibonacci level of wave 4 vs 3, which in turn could act as potential support.

The EUR/USD channel, indicated by the red and blue trend lines, could be a corrective pattern as long as price stays above the 100% level of wave B vs A. A break above resistance (red) could start the wave 3 or wave C.

Currency pair GBP/USD

The GBP/USD bounce at the 38.2% Fibonacci level of wave 4 (blue) has so far been unable to break above the resistance trend line (red). A break below the 38.2% Fibonacci level could indicate a bearish breakout towards the 50% Fib of wave 4 vs 3 and the support trend line (blue).

The GBP/USD is testing the support trend line (green) and 78.6% Fibonacci level of wave 2 vs 1. A break below support (green) could indicate a bearish breakout whereas a break above resistance (red) could indicate a bullish breakout.

Currency pair USD/JPY

The USD/JPY bounced at the support trend line (blue), which could indicate the continuation within wave 5 (blue).

The USD/JPY could potentially have completed an ABC (orange) correction within wave 4 (purple) and price could be in a wave 5 as long as it stays above support (blue).

Market Update – Asian Session: China Selectively Cuts RRR, PMI Shows Growth

Asia Summary

Asian equity markets opened higher after stronger China PMI over the weekend and a RRR cut. China (closed all week), Hong Kong, India and South Korean markets closed for holidays so liquidity remained light. Indonesia stock market reached a fresh record high of 5,929. According to analysts today's Japan Tankan survey could be a leading indicator signaling an improvement in earnings of Japanese companies, which will start reporting later this month. USD remained stronger against the yen and slightly weaker against A$ and NZ$. US 10-yr treasury yield up over 1.0% in the session.

Over the weekend China's PBOC cut reserve requirement ratio (RRR) for some banks that meet certain requirements for lending to small business and agricultural sector (1st cut since Feb 2016); affirms prudent and neutral monetary policy. Should be noted this is different from previous changes to RRR in that it was a delayed cut that will not go into effect until next year. (See headline at 10:12:56ET for full details) Markets seemed to have little reaction. China also released Sept Caixin PMI manufacturing remaining in expansion at 51, tracking in line with the official figure of 52.4 (14th month of expansion and highest level since 2012) released on Friday.

EUR/USD fell to 1.1770 as Spain's Catalonia is now on track towards a declaration of independence. According to regional officials, results showed 90% of voters backed independence (with a turnout of 2.3M vote, 42%). This is notable as the mock referendum also showed 2.3M votes. Catalan President Puigdemont vowed to declare independence in the event of a ‘yes' vote, and later stated that Catalonia had won the right to become an independent state. There were reports of police entering various polling stations to try to seize materials related to the voting and more than 800 injured in clashes with Spanish riot police.

Key economic data

(CN) CHINA SEPT CAIXIN PMI MANUFACTURING: 51.0 V 51.5E

(JP) JAPAN Q3 TANKAN LARGE MANUFACTURING INDEX: 22 V 18E; MANUFACTURERS OUTLOOK: 19 V 16E; ALL-INDUSTRY CAPEX: 7.7% V 8.4%E

(JP) JAPAN SEPT FINAL PMI MANUFACTURING: 52.9 V 52.6 PRELIM

(HK) Macau Sept Gaming Rev MOP21.4B, +16.1% y/y v 14.5%e

(SG) Singapore Q3 URA Private Home Prices Q/Q: +0.5% v -0.1% prior (1st rise in 4-yrs)

(AU) Australia Sept CoreLogic House Price m/m: 0.3% v 0.1% prior; Prices of detached housing in Sydney -0.3% (first decline in 1.5 years)

(TH) Thailand Aug CPI M/M: 0.6% v 0.3%e; Y/Y 0.9% v 0.5%e; Core Y/Y: 0.5% v 0.5%e

Speakers and Press

China/Hong Kong

(CN) PBOC Q3 meeting of monetary policy committee: To cut reserve requirement ratio (RRR) for some banks that meet certain requirements for lending to small business and agricultural sector (1st cut since Feb 2016); affirms prudent and neutral monetary policy

Korea

(KR) Sec State Tillerson has been encouraged to not talk with North Korea by President Trump - Korean press

Japan

(JP) Japan ruling Liberal Democratic Party will pledge to raise the consumption tax as planned to 10% in 2019 in its manifesto for the general election on Oct 22

(JP) Moody's: Even if Japan govt raises the sales tax to 10% (from 8%) in 2019, as scheduled, its overall fiscal balance won't change materially

Asian Equity Indices/Futures (00:00ET)

Nikkei +0.2%, Hang Seng closed; Shanghai Composite closed; ASX200 +1.1%, Kospi +0.9%

Equity Futures: S&P500 +0.1%; Nasdaq100 +0.1%, Dax +0.2%, FTSE100 +0.1%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1816-1.1770; JPY 112.91-112.40; AUD 0.7847-0.7816;NZD 0.7226-0.7189

Dec Gold -0.5% at $1,278/oz; Nov Crude Oil -0.3% at $51.53/brl; Dec Copper +0.8% at $2.97/lb

Equities notable movers

Australia/New Zealand

BPT.AU Completes A$201M rights offering, take-up rate over 98%; +15%

A2M.AU Receives CFDA registration to allow exports of a2 Milk Co's China label infant formula to China to continue; +5.5%

Japan

7201.JP Suspended new auto registrations because domestic factories did not follow processes agreed with the Japanese Ministry of Land, Infrastructure and Transport; now fixed and registrations have resumed; -3.4%

7649.JP Reports H1 Net ¥8.7B v ¥7.4B y/y; Op ¥12.6B v ¥11.7B y/y; Rev ¥229.5B v ¥217.8B y/y; -5.2%